What is conveyance allowance, is it taxable, and how does it actually affect your in-hand pay? A plain-language guide for salaried employees.

You open your offer letter or revised salary slip and spot a line: “Conveyance Allowance — ₹2,000 per month.” Your immediate assumption is probably that this is tax-free. Most first-time salaried employees make that assumption. The problem is, it is often wrong — and getting it wrong can quietly affect your ITR filing.

Conveyance allowance meaning is one of those salary terms that looks obvious but hides real complexity. There is a difference between a fixed monthly allowance in your payslip, official-duty travel reimbursement, and the old commuting exemption that many employees still think applies. They are not the same, and the Income Tax Act does not treat them the same way.

This article breaks it down clearly: what conveyance allowance actually is, when it is taxable, when it may not be, how the old and new tax regime affect it, and exactly what to check in your Form 16 before you file. Tax rules here apply based on the relevant assessment year — always verify current provisions at incometax.gov.in before acting on any figure in this article.

Quick Answer: Conveyance Allowance Meaning

Conveyance allowance meaning refers to money paid by an employer to cover travel or transport expenses related to work. In salary, it may be taxable unless it qualifies as an official-duty allowance or permitted transport exemption, such as ₹3,200 per month for eligible disabled employees. Whether any exemption applies depends on the purpose of the payment, your employer’s documentation process, and the tax regime under which you are assessed. Verify current figures at incometax.gov.in before filing your ITR.

Key Takeaways

- Conveyance allowance is a salary component paid for travel or transport expenses — being listed separately in your payslip does not make it automatically tax-free.

- The flat monthly transport allowance exemption for daily commuting (₹1,600 per month) was abolished from FY 2018–19 and replaced by the standard deduction; most salaried employees no longer have a separate commute exemption.

- Eligible employees with a disability may qualify for a transport allowance exemption of up to ₹3,200 per month under Section 10(14) — verify the current notified limit at incometax.gov.in before claiming it.

- Conveyance for official-duty purposes may be exempt to the extent of actual expenditure incurred under Section 10(14) of the Income Tax Act, provided your employer accounts for it correctly in salary processing.

- Under the new tax regime, most allowance exemptions — including conveyance-related ones — are not available; a fixed monthly component is typically fully taxable.

- A fixed monthly conveyance allowance in salary with no official-duty mechanism forms part of your gross taxable salary — check Part B of your Form 16 to confirm how your employer has treated it.

Key Facts at a Glance

| Item | What You Need to Know |

|---|---|

| What it is | Money paid by an employer for employee travel in connection with work duties |

| Where it appears | CTC breakup, monthly salary slip, and salary annexure of Form 16 |

| Taxable? | Depends on purpose, employer’s payroll treatment, and your tax regime — not automatic |

| Relevant law | Section 10(14), Income Tax Act, 1961; Rule 2BB, Income Tax Rules |

| Disabled employee exemption | Up to ₹3,200 per month transport allowance — verify current limit at incometax.gov.in |

| General commuting exemption | Abolished FY 2018–19; replaced by standard deduction for salaried employees |

| New tax regime | Most allowance exemptions unavailable — confirm your regime before filing ITR |

| Verification source | Income Tax Department — incometax.gov.in |

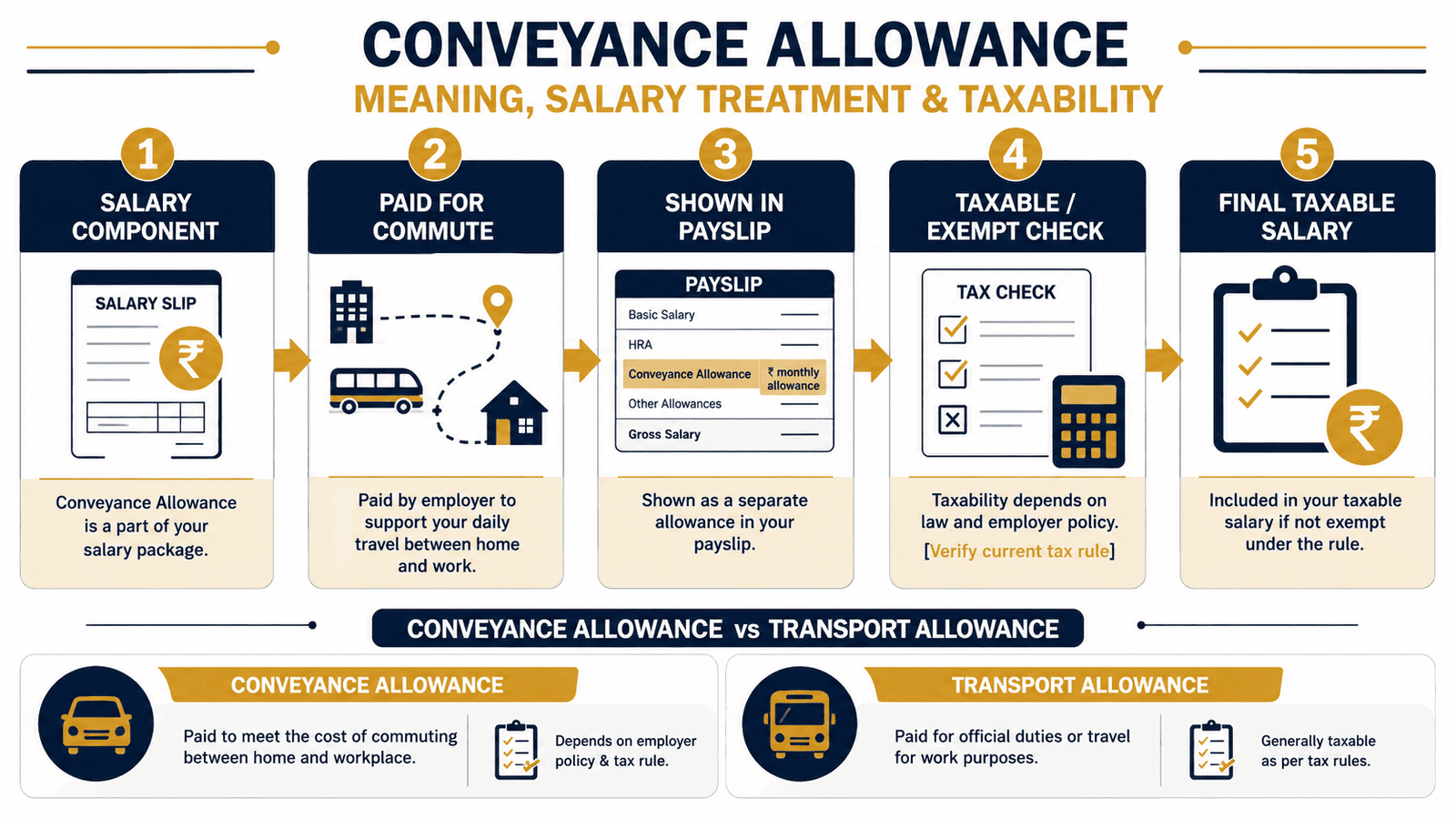

What Does Conveyance Allowance Mean in Your Salary?

Conveyance allowance is money your employer pays to cover expenses incurred while travelling for work. The key phrase is “for work” — not between your home and office, but in connection with your official duties. Think: visiting a client site, travelling between company locations, attending an official meeting outside your regular workplace.

Most employers include it as a named line item in the CTC breakup or monthly salary slip — typically somewhere between ₹1,500 and ₹3,000 per month. Seeing it listed separately can make it appear to be a special benefit. Whether it actually is depends on how your employer treats it in payroll and what the current provisions say for the assessment year you are filing for.

Why Employers Include It in the Salary Structure

Employers use named salary components partly for practical reasons — matching roles to expense patterns — and partly because historical tax provisions once rewarded specific component structures. Many of those blanket exemptions no longer exist, but the component names persist. Understanding where conveyance allowance sits within your full salary breakup starts with knowing all your components. Your salary slip components — basic, HRA, special allowance, conveyance, and deductions — together determine your gross salary, your taxable salary, and your actual in-hand pay each month.

Allowance vs Reimbursement: The Distinction That Changes Tax Treatment

This is where most employees get confused. An allowance is a fixed monthly amount paid as part of salary — whether or not you actually spent it on travel. A reimbursement is money paid against actual bills and proof of expense, usually processed outside regular payroll.

The distinction matters because a fixed monthly allowance in your salary is generally taxable as part of gross salary unless a specific exemption provision applies and your employer processes it accordingly. A reimbursement for official-duty travel claimed against bills may not form part of your taxable salary at all — because it represents actual expense recovery, not income. Many employers use these terms interchangeably in payslips. The Income Tax Act does not.

Section 10(14) and Rule 2BB: The Legal Framework

Under Section 10(14) of the Income Tax Act, certain allowances granted to employees to meet specific expenses incurred in the performance of their duties can be exempt from tax — either fully or up to a notified limit. The specific conditions and limits are prescribed under Rule 2BB of the Income Tax Rules. Conveyance allowance for official duties falls under this provision.

However, the exemption under Section 10(14) is limited to the amount actually spent on official travel — not the full allowance amount. If your employer pays ₹2,000 per month as conveyance but you spend only ₹1,200 on verifiable official travel, only ₹1,200 is defensible as exempt. The balance remains taxable. In practice, most employer payrolls treat a fixed monthly conveyance component as fully taxable — the safer and more common approach unless a formal reimbursement mechanism is in place.

What Happened to the Commuting Transport Allowance Exemption?

Until FY 2017–18, salaried employees could claim a flat exemption of ₹1,600 per month (₹19,200 per year) on transport allowance paid for commuting between home and office. Budget 2018 abolished this exemption from FY 2018–19. In its place, the government introduced the standard deduction — a flat deduction from gross salary available to all salaried employees without any bills or proof. The current standard deduction amount should be verified at incometax.gov.in, as it may have been revised in subsequent Budgets.

If any article, old salary template, or offer letter still refers to a ₹1,600/month commuting exemption as an active benefit — it is outdated. That exemption no longer applies for general employees.

Transport Allowance for Employees With a Disability

Employees with a disability — as defined under the relevant Income Tax provisions — may still be eligible for a separate transport allowance exemption under Section 10(14). The notified monthly limit has historically been ₹3,200 per month. This exists because employees with disabilities may incur higher costs to commute to work. As with all tax provisions, verify the current applicable limit at incometax.gov.in for the relevant assessment year before claiming it.

New Tax Regime and Conveyance Allowance

Under the new tax regime — the default from FY 2023–24 — most allowance-based exemptions are not available. This includes conveyance and transport allowance exemptions for official duties. If you are assessed under the new tax regime, your fixed monthly conveyance allowance will typically form part of your taxable gross salary regardless of its label in your payslip. Under the old tax regime, specific Section 10(14) exemptions may still apply depending on the nature of the allowance — subject to current provisions.

Real Example: Rohit’s Salary Slip in Pune

Rohit is 28, a software analyst at a mid-size IT firm in Pune, earning ₹9.5 lakh per year. His monthly gross salary is ₹75,000, broken down as follows:

- Basic salary: ₹37,500

- HRA: ₹15,000

- Special allowance: ₹20,500

- Conveyance allowance: ₹2,000

Rohit’s employer does not ask him to submit travel bills for the ₹2,000. It is a fixed monthly credit, paid regardless of actual travel. Payroll treats it as fully taxable — and it appears in gross salary in Part B of his Form 16 with no separate exemption entry. His annual conveyance component is ₹24,000 (₹2,000 × 12), and every rupee of it is taxable at his applicable slab rate.

If Rohit’s employer had instead structured this as a reimbursement-against-bills arrangement — where he submits official travel receipts and receives payment only against those — the treatment could have been different. But a fixed monthly credit without a bills-based process is simply taxable salary income.

To see exactly how each salary component affects what actually lands in your account after TDS and deductions, try the monthly in-hand pay calculator.

How to Calculate the Tax Impact of Conveyance Allowance

Taxable Conveyance Amount = Monthly Allowance × 12 (if fully taxable)

If partially exempt: Taxable Amount = Total Paid − Exempt Portion Confirmed by Employer

Using Rohit’s salary structure, here is how three common scenarios compare:

| Scenario | Annual Amount Paid | Annual Taxable Amount |

|---|---|---|

| Fixed monthly allowance, no bills, no reimbursement process | ₹24,000 | ₹24,000 (fully taxable) |

| Official-duty reimbursement — ₹18,000 in bills submitted, ₹6,000 unsubstantiated | ₹24,000 | ₹6,000 (unsubstantiated balance is taxable) |

| Eligible employee with disability — transport allowance exemption applied | ₹38,400 (₹3,200 × 12) | Potentially ₹0 up to exemption limit — verify current limit at incometax.gov.in |

The number that matters for your ITR is the taxable salary figure in Part B of your Form 16 — not your offer letter alone. Your employer processes TDS and any applicable exemptions first; you verify the output when you file. If the Form 16 figures look inconsistent with what you expect, raise it with payroll before submitting your ITR.

For a complete walkthrough of how to arrive at your taxable income from salary — including how exemptions, deductions, and allowances interact — see our guide on taxable salary calculation.

Comparison: Conveyance Allowance vs Transport Allowance

These terms are used interchangeably in most workplaces, but their tax treatment differs meaningfully. Here is the practical distinction:

| Feature | Conveyance Allowance (Official Duty) | Transport Allowance (Home-to-Office Commute) |

|---|---|---|

| Purpose | Travel incurred while performing official duties | Daily commute between home and place of work |

| Old tax regime | May apply — exempt to extent of actual official expense under Section 10(14) | Abolished FY 2018–19 — replaced by standard deduction |

| New tax regime | Not available | Not available |

| Disabled employees | N/A | Separate exemption up to ₹3,200/month may apply — verify at incometax.gov.in |

| Proof required | Depends on employer’s reimbursement policy | No longer applicable for general employees |

| Appears in Form 16 | Yes — in salary annexure; exempt portion shown separately if applicable | Yes — in gross salary; no separate exemption entry for general employees |

And here is how a fixed salary allowance compares to a reimbursement-based arrangement — a distinction that affects your taxable salary more directly:

| Feature | Fixed Salary Allowance | Travel Reimbursement Against Bills |

|---|---|---|

| How it is paid | Fixed monthly credit in salary, regardless of actual travel | Paid against submitted bills and receipts, outside regular payroll |

| Tax status | Generally taxable as part of gross salary | Not typically treated as income — it is expense recovery |

| Bills required | No | Yes — original bills and receipts required |

| New regime impact | Fully taxable | Reimbursement is not salary income — not directly impacted |

| Appears in Form 16 | Yes — included in gross salary | May not appear in Form 16 if processed as non-salary reimbursement |

Understanding which arrangement your employer uses helps you read your payslip and Form 16 correctly. For a full picture of how your regime choice affects exemptions across your entire salary, see our guide to the old and new tax regime for salaried employees.

How to Decide What’s Right for You

Whether conveyance allowance benefits you — or simply adds to your taxable salary — depends on a few specific things you can check right now.

Your conveyance allowance is a fixed monthly credit in salary with no requirement to submit travel bills — then it is part of your taxable gross salary. Do not expect any automatic exemption from this component.

Your employer has a formal reimbursement process where you submit bills for official-duty travel and receive payment against those receipts — then the substantiated amount may not be treated as taxable income. Confirm this with HR and cross-check against your Form 16.

You are assessed under the new tax regime — then conveyance and transport allowance exemptions are not available. The full amount of any fixed monthly allowance is taxable, regardless of its label in your payslip.

You are on the old tax regime and your role involves genuine official-duty travel — visiting clients, travelling between office locations, attending site events — then check with your payroll team whether a Section 10(14) arrangement can be structured. This requires your employer to process it correctly in salary and TDS.

You have a certified disability and receive a transport allowance — then a specific exemption up to the notified monthly limit may apply. Verify the current limit at incometax.gov.in and ensure your Form 16 reflects it before filing.

You have no official-duty travel requirement, no disability-based entitlement, and are on the new tax regime — then the conveyance allowance line in your salary has no tax-saving value. It is simply part of your taxable CTC, and you should not expect any benefit from the component label.

Understanding how your CTC components translate into actual in-hand pay — including how each allowance interacts with tax — is explained step by step in our guide on CTC and take-home salary.

Common Mistakes to Avoid

Assuming Every Named Allowance Is Tax-Free

Just because a salary component has a specific name — conveyance, transport, medical — does not attach a tax exemption to it automatically.

Under current rules, most flat monthly allowances are taxable. Many employees underreport their gross taxable salary by assuming named components carry automatic exemptions, which creates a mismatch with their employer’s TDS records and can invite a demand notice from the Income Tax Department.

Always check your Form 16 before filing. Do not assume — verify the actual treatment your employer has applied.

Confusing Daily Commute Allowance With Official-Duty Conveyance

The daily commute exemption of ₹1,600 per month was abolished from FY 2018–19. Official-duty conveyance under Section 10(14) still exists — but only to the extent of actual official expenses, not as a blanket commuting exemption.

Mixing these up can lead to claiming an exemption that no longer applies or missing a legitimate official-duty claim. Ask your employer how each salary component is classified before filing.

Not Checking Form 16 Before Filing ITR

Form 16 is the definitive record of how your employer has treated every salary component for tax. Many employees file their ITR based on the payslip or the income tax portal’s pre-filled data without reconciling against their Form 16 salary annexure.

If your employer has already included conveyance allowance in taxable salary and deducted TDS accordingly, claiming an additional exemption without checking Form 16 creates a filing error. Reconcile first, then file.

Claiming an Exemption Without Eligibility or Employer Support

Section 10(14) exemptions and the disabled employee transport allowance come with specific eligibility conditions. Claiming them without meeting those conditions — or without your employer processing them correctly in Form 16 — creates a discrepancy between your ITR and your employer’s records. This can trigger a scrutiny notice. Verify with a qualified tax professional before making any such claim independently.

Using Outdated Exemption Limits From Old Articles or Offer Letters

Many online articles and legacy offer letter templates still quote the ₹1,600/month commute exemption as an active benefit. It has not applied since FY 2018–19. Always verify current exemption limits for the relevant assessment year directly at incometax.gov.in — not from a three-year-old salary guide.

Treating a Fixed Allowance and a Reimbursement as the Same Thing

Your payslip may show ₹2,000 as “conveyance allowance” while a colleague’s shows ₹2,000 as “travel reimbursement.” These can have entirely different tax implications depending on how the employer processes each. A fixed monthly credit is generally taxable income. A bills-based reimbursement is expense recovery. Know which one you have before you file your ITR.

When This May Not Be the Right Choice

There are specific situations where having a conveyance allowance component in your salary adds no real value — and may quietly work against you.

If your employer provides company transport or a cab reimbursement separately, a fixed monthly conveyance allowance in salary is simply a taxable reshuffling of your CTC. You are not receiving a benefit — you are relabelling income that still gets taxed in full.

If you work in a role with no official travel requirement, you will never spend the ₹2,000 per month the allowance notionally represents. Yet it still sits in your taxable gross salary every month.

If you are on the new tax regime, the allowance carries no exemption benefit whatsoever. In this case, a cleaner structure — such as a higher special allowance without a separately named conveyance component — may be simpler to manage, though any restructuring involves trade-offs with PF and gratuity that warrant separate evaluation.

And if your job involves heavy official travel, a reimbursement-against-bills policy is typically more efficient than a fixed taxable allowance — provided your employer has a formal process to support it.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Conveyance allowance taxability is governed by Section 10(14) of the Income Tax Act, 1961, read with Rule 2BB of the Income Tax Rules. Both can be updated through Finance Acts, Budgets, or CBDT notifications — which is why you must verify current provisions for the specific assessment year you are filing for, rather than relying on guides written in a prior year.

- Income Tax Department — incometax.gov.in: Primary source for Section 10(14), Rule 2BB, current exemption limits, ITR forms, and Form 16 guidance. This is your first stop for any verification.

- Your Form 16: Part A shows TDS deducted; Part B shows how your employer has treated each salary component. This is the most practical starting point to understand your own specific situation.

- Your employer’s payroll or HR team: Can confirm whether your conveyance component is a taxable fixed allowance or a reimbursement processed against bills — two things that look identical in a payslip but differ entirely in tax treatment.

- A qualified tax professional: Recommended for edge cases — especially if you believe a Section 10(14) exemption applies but your Form 16 does not reflect it.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

When you are ready to file your ITR, knowing how to read your Form 16 is the most practical first step before entering any income or exemption figures.

Expert Tips

- When you receive a new offer letter or CTC revision, ask HR directly whether the conveyance allowance is a fixed taxable component or a reimbursement-based benefit. These are processed differently in payroll — the difference shows up in your in-hand salary and your Form 16, not just your offer letter.

- Before filing your ITR each year, download your Form 16 Part B and locate the “Exemptions under Section 10” row. If conveyance appears as a separately listed exemption, your employer has applied a specific provision. If it is rolled into gross salary with no exemption entry, it is taxable — file accordingly.

- If you are on the old tax regime and your role involves regular official travel, ask your payroll team whether your employer has a mechanism to process this as a Section 10(14) reimbursement against bills. Many employees do not know this option may exist at their employer — raising it with HR is a simple first step.

- Never use a salary optimisation guide or legacy offer letter as your reference for exemption limits. Budget 2018 removed the general commute exemption. Provisions in this area may be updated further. Always verify what is currently applicable for your assessment year at incometax.gov.in before claiming anything.

- Use an income tax calculator to see how your full salary structure — including all allowance components — affects your final tax under both regimes. Even ₹24,000 per year in a 30% slab adds ₹7,200 to your tax bill. The income tax calculator lets you compare old and new regime impact side by side with your actual figures.

- When changing jobs, review the new employer’s salary structure carefully. Two offer letters may both show “conveyance allowance: ₹2,000” — but one employer processes it as a taxable component and another has a reimbursement mechanism. The label is not the tax treatment. Ask before you accept.

Frequently Asked Questions

What is conveyance allowance in salary?

Conveyance allowance is a fixed monthly payment made by an employer to cover travel or transport expenses incurred by an employee in connection with work duties. It appears as a named component in your CTC breakup, monthly salary slip, and the salary annexure of Form 16. Whether it is taxable or exempt depends on its purpose, how your employer processes it in payroll, and the tax regime under which you are assessed for that financial year.

Is conveyance allowance taxable or not?

It depends on three things. First, whether it is a fixed monthly credit in salary or a reimbursement against actual bills — fixed credits are generally taxable. Second, whether a specific exemption under Section 10(14) applies to your case and whether your employer processes it correctly. Third, whether you are on the new or old tax regime — under the new regime, most allowance exemptions are not available and the component is taxable. Check your Form 16 to see how your employer has actually treated it.

What is the conveyance allowance exemption limit?

For general salaried employees, the flat monthly commuting exemption of ₹1,600 per month was abolished from FY 2018–19 and replaced by the standard deduction. No general commuting exemption currently exists for regular employees. For employees with a disability, a transport allowance exemption of up to ₹3,200 per month may apply under Section 10(14) — but verify the current notified limit at incometax.gov.in for the relevant assessment year, as it may have been updated.

Is conveyance allowance available under the new tax regime?

No. Under the new tax regime, most allowance-based exemptions — including conveyance and transport allowance exemptions — are not available. A fixed monthly conveyance component in your salary will form part of your taxable gross salary under the new regime regardless of its label. Verify the current provisions for your specific assessment year at incometax.gov.in before filing your ITR.

What is the difference between transport allowance and conveyance allowance?

Conveyance allowance typically refers to money paid for official-duty travel — visiting clients, travelling between offices, attending external meetings. Transport allowance traditionally referred to a fixed monthly amount for home-to-office commuting. The commuting exemption was abolished in Budget 2018 for general employees. For employees with a disability, a separate transport allowance exemption may still apply. In everyday payslip usage, both terms are often used loosely — but the tax treatment depends on the underlying purpose and how the employer processes it, not the label.

Where does conveyance allowance appear in the payslip and Form 16?

In your monthly payslip, it appears as a named row in the earnings section — usually between HRA and special allowance. In Form 16, it appears in Part B (the salary annexure). If your employer treats it as fully taxable, it will be included in the gross salary figure. If a specific exemption is applied, it may appear as a separate entry under “Exemptions under Section 10.” Always cross-check both documents before filing your ITR — the Form 16 is the authoritative record, not the payslip.

Can I claim a conveyance allowance exemption if my employer has not applied it?

This depends on your eligibility and the specific provision. If you believe a Section 10(14) exemption applies to your situation but your Form 16 does not reflect it, raise it first with your HR or payroll team — there may be an administrative reason for the omission, or the component may genuinely not qualify. For any unresolved discrepancy, consult a qualified tax professional before making an independent claim in your ITR. Filing inconsistently with your Form 16 can trigger a mismatch notice from the Income Tax Department.

What happens to my conveyance allowance if I change jobs mid-year?

Each employer may treat the component differently in their payroll. When you change jobs mid-year, you receive two Form 16s — one from each employer. Both must be consolidated when you file your ITR. The total income from both employers, along with any exemptions each applied, must be accurately reported. Do not assume the new employer’s treatment mirrors the old one — verify by asking HR when you join.

Is conveyance allowance included in the standard deduction?

No — they operate at different points in the taxable income calculation. Conveyance allowance is a salary component that forms part of your gross salary. The standard deduction is then applied on top of gross salary as a flat deduction for salaried employees. The standard deduction replaced the old commuting transport allowance exemption from FY 2018–19 — it is not the same thing, and the two are not interchangeable. Verify the current standard deduction amount applicable to your assessment year at incometax.gov.in.

Final Verdict

Conveyance allowance meaning is simple in principle — money paid for work-related travel. Its tax treatment is not. For most salaried employees today, a fixed monthly conveyance component in salary is taxable income, not a tax-saving benefit. The old blanket commuting exemption was abolished in Budget 2018, and the new tax regime removes most remaining allowance exemptions entirely.

Where a legitimate official-duty reimbursement structure exists — with proper documentation and employer processing — there may still be value for employees on the old tax regime. For employees with a disability, a specific transport allowance exemption may also apply. But these are defined, verifiable cases — not assumptions to be carried forward from an old offer letter.

Start with your Form 16. Do not rely on your payslip label or what a salary guide from three years ago said. Verify what applies to your situation under the current assessment year rules at incometax.gov.in. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.