Most salaried employees in India make the same calculation when they get an offer letter: divide the CTC by 12. The number looks good. Then the first salary hits the bank — and it is noticeably smaller. If you have ever searched for a take home salary calculator India, this is exactly why.

Your monthly in-hand salary is not CTC divided by 12. Employer contributions to EPF, gratuity, and group insurance are included in CTC but never reach your account. Employee deductions — EPF, professional tax, TDS — are subtracted from your gross pay before the credit. On a ₹12,00,000 CTC, these differences can reduce monthly in-hand by ₹20,000–₹30,000 compared to a back-of-envelope estimate.

This guide explains the formula, walks through a realistic ₹12 LPA example, and shows you exactly what to check before accepting an offer or planning your monthly budget.

Quick Answer: Take Home Salary Calculator India

A take home salary calculator India helps you estimate monthly in-hand pay by subtracting EPF, professional tax, income tax, insurance, and other deductions from gross salary. For example, ₹10,00,000 CTC may not mean ₹83,333 monthly take-home because employer benefits and deductions reduce net pay. Actual in-hand salary depends on your employer’s salary structure, your state of employment, and the tax regime you have chosen.

How to Calculate Monthly In-Hand Salary from CTC

The formula itself is short. The numbers inside it are what most employees never fully see.

In-Hand Salary = Monthly Gross Salary − Monthly Deductions

Monthly Gross Salary = (Annual CTC − Annual Employer-Side Costs) ÷ 12

Step 1 — Start with your annual CTC. This is the total amount your employer spends on you in a year — every benefit, contribution, and allowance included.

Step 2 — Subtract employer-side costs. Your employer’s contribution to EPF (12% of basic salary, subject to wage ceiling), gratuity (approximately 4.81% of basic), and group health insurance are part of CTC but never appear in your bank account. For a ₹12,00,000 CTC with ₹40,000/month basic, employer EPF alone adds up to ₹4,800/month — money that goes to your PF account or accrues as future gratuity, not your wallet today. For a full breakdown of how both sides of the PF equation work, see our guide on employee PF contribution.

Step 3 — Arrive at monthly gross salary. Once employer-side costs are removed from annual CTC, divide by 12. This is the figure on the earnings side of your payslip — basic + HRA + all allowances.

Step 4 — Subtract your monthly deductions. From monthly gross, deduct: employee EPF (12% of basic, subject to statutory wage ceiling), professional tax (state-specific, typically ₹200/month in Maharashtra), TDS/income tax, and any employer-deducted insurance premiums or other voluntary contributions.

Step 5 — The result is monthly in-hand salary. This is what clears your bank account on payday.

Use Ridhi’s take home salary calculator to run these steps instantly with your own CTC and structure inputs — no spreadsheet needed.

| Annual CTC | Approx. Monthly Gross | Approx. Monthly In-Hand |

|---|---|---|

| ₹6,00,000 | ₹45,500 | ₹43,000 |

| ₹12,00,000 | ₹84,000 | ₹75,200 |

| ₹20,00,000 | ₹1,46,000 | ₹1,26,000 |

These figures are illustrative only. Actual amounts depend on your salary structure, employer EPF computation method, state professional tax, tax declarations, and applicable income tax slabs. Verify all rates before making financial decisions.

Key Takeaways

- CTC is the total cost your employer pays for you — not your monthly salary. Dividing annual CTC by 12 almost always overstates what you actually receive.

- Employer EPF (12% of basic, subject to wage ceiling) and gratuity (~4.81% of basic) are included in CTC but are never credited to you as monthly pay.

- Employee EPF, professional tax, and TDS are deducted from your monthly gross before the bank credit — reducing in-hand by ₹5,000–₹25,000/month depending on income.

- On a ₹12,00,000 CTC with ₹40,000/month basic, employer EPF alone is ₹57,600/year — money that sits in your PF account but inflates the CTC figure.

- Variable pay, annual bonuses, and ESOPs in your CTC may not be paid monthly — or at all if performance targets are missed.

- Your tax regime choice (old vs new) and investment declarations submitted to HR directly affect your monthly TDS and therefore your actual in-hand salary.

- No online calculator can guarantee your exact take-home — your employer’s offer letter and payslip are the only fully accurate source for your specific structure.

Key Facts at a Glance

| Term | What It Means | Used For |

|---|---|---|

| CTC (Cost to Company) | Total annual employer cost: gross salary + employer EPF + gratuity + insurance + benefits | Comparing job offers; hike negotiations |

| Gross Salary | Earnings before deductions — basic + HRA + all allowances. Does not include employer PF or gratuity | TDS calculation; loan eligibility; Form 16 |

| Taxable Salary | Gross salary minus permitted adjustments: standard deduction, HRA exemption, and other claims | Income tax computation; ITR filing |

| Net / In-Hand Salary | Amount credited to your bank: gross minus EPF, professional tax, TDS, insurance deductions | Monthly budgeting; EMI planning |

| Employee EPF Contribution | 12% of basic salary deducted from pay each month; statutory wage ceiling applies | Retirement corpus; tax deduction under 80C (old regime) |

| Professional Tax | State-levied tax on salary income — applies in some states (Maharashtra, Karnataka) but not all | State-specific monthly deduction |

| TDS on Salary | Income tax deducted at source by employer — based on projected annual income, regime, and declarations | Advance tax compliance; adjusts monthly in-hand |

| Standard Deduction | Flat deduction from gross salary before computing income tax — available in both old and new regimes | Reduces taxable income; increases effective in-hand |

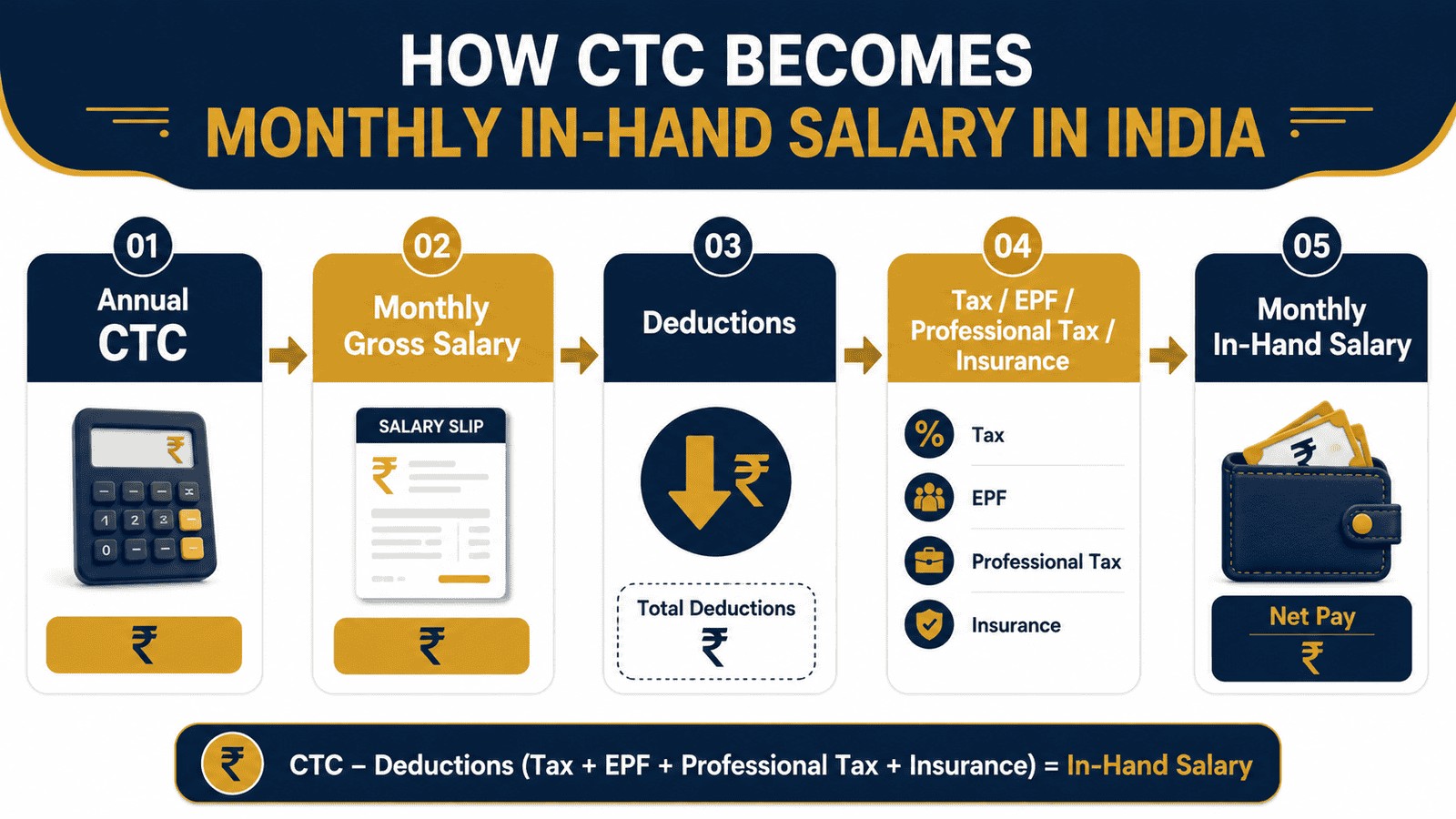

Understanding the Full Salary Journey: CTC to In-Hand

Most salaried employees encounter three different salary figures across their career — the CTC in the offer letter, the gross salary on their payslip, and the amount credited to their bank account. These are three distinct numbers, and conflating them causes real financial planning errors.

Why CTC Is Not Your Salary

Cost to Company is exactly what the name says — the total annual expense your employer incurs to keep you on the payroll. It includes your gross salary, yes, but also your employer’s own contributions to EPF, gratuity, health insurance, and any other benefits provided. These employer-side costs never appear as salary in your account. They are the company’s share, routed separately to government schemes or accrued as future liabilities.

On a ₹12,00,000 CTC with ₹40,000/month basic salary, here is what the employer side looks like:

- Employer EPF (12% of ₹40,000): ₹4,800/month — credited to your PF account, not your bank

- Employer gratuity (~4.81% of ₹40,000): ₹1,924/month — accrues and is paid only on exit after five years of service

- Group health insurance: paid by employer, typically absorbed into CTC without any monthly credit to you

Together, these can account for ₹80,000–₹1,00,000 or more of your annual CTC. For a detailed walkthrough of why this gap exists, see our guide on the CTC and in-hand difference.

Monthly Gross Salary: What Your Payslip Actually Shows

Monthly gross salary is the sum of all fixed earnings listed on the earnings side of your payslip, before any deductions are applied. Typically: basic salary + HRA + special allowance + any other fixed monthly allowances. This is the number your employer uses when computing TDS, issuing Form 16, or writing a salary certificate for a loan application.

Gross salary does not include your employer’s EPF or gratuity contribution. Those are already netted out when the CTC is split into gross vs employer costs.

How Basic Salary Drives Everything Else

Basic salary is the single most consequential figure in your payslip — not because it is necessarily the largest component, but because multiple downstream calculations depend on it. Your employee EPF contribution (12% of basic), your employer’s EPF match (another 12%), your HRA exemption eligibility, and your gratuity entitlement all reference basic salary as the base. A higher basic means higher EPF deductions — but also higher HRA exemption if you pay rent, and a larger retirement corpus building over time.

Employers sometimes keep basic salary low to reduce their own PF liability. This might appear to help your in-hand in the short run, but it also compresses your retirement savings and gratuity payout. Understanding how basic salary impact ripples through PF, gratuity, HRA, and tax is essential before comparing two offers with identical CTCs.

What Gets Deducted: From Gross to Net

Your net salary — the amount cleared to your bank — is monthly gross minus every deduction your payroll team processes. The main ones:

- Employee EPF contribution: 12% of your basic salary, subject to the statutory wage ceiling. This goes into your EPF account — it is your money, but locked and not accessible as monthly spending cash.

- Professional tax: A state-level levy deducted monthly. Maharashtra and Karnataka charge it; Delhi, Haryana, and several others do not. The annual cap varies by state and by income bracket within the state.

- TDS (income tax): Your employer deducts tax at source each month based on your estimated annual income, your regime choice, and any deduction declarations you have submitted. The monthly figure can be ₹0 (for incomes below the taxable threshold) or several thousands, depending on your level.

- Health insurance premium: Some employers deduct a small employee contribution toward group cover. Others absorb the full cost within CTC without any payslip deduction.

- Voluntary deductions: NPS contributions, voluntary PF top-ups, or salary advance recoveries can add further lines to your deduction column if you have opted for them.

Variable Pay: The Part of CTC That Comes With Conditions

Performance bonuses, annual incentives, joining bonuses, and ESOPs frequently appear in offer letters as CTC components. They are real — but they are not monthly. A ₹1,50,000 annual performance bonus listed in your ₹12,00,000 CTC is paid quarterly or annually, and only if you meet the applicable performance targets. When you estimate expected monthly in-hand salary, build your budget on fixed, guaranteed monthly components only. Treat variable pay as additional — something to plan around when it actually arrives.

Real Example: Aarav’s ₹12 LPA Offer in Pune

Aarav is 29, a software engineer in Pune evaluating a new offer of ₹12,00,000 annual CTC. He wants to know exactly how much will reach his bank account every month before he accepts.

His offer letter shows this CTC breakup:

- Basic Salary: ₹40,000/month

- HRA: ₹20,000/month

- Special Allowance: ₹24,000/month

- Employer EPF (12% of basic): ₹4,800/month — routed to PF, not bank

- Employer Gratuity (~4.81% of basic): ₹1,924/month — accrues, paid on exit

- Group Health Insurance: ₹1,276/month — employer’s share

Monthly Gross Salary (Basic + HRA + Special Allowance): ₹84,000

Monthly deductions from gross:

- Employee EPF (12% of ₹40,000): ₹4,800

- Professional Tax (Maharashtra): ₹200

- TDS — new tax regime, approximate: ₹3,800

Estimated monthly in-hand: ₹75,200 — not the ₹1,00,000 that dividing CTC by 12 would suggest.

The gap of ₹24,800/month comes from employer contributions that inflate CTC, plus deductions that reduce gross to net. These figures are illustrative; Aarav’s actual in-hand will depend on his employer’s exact EPF computation method, his tax declarations, and whether any additional deductions apply. The structure, not the number, is what to check first.

Comparison: CTC vs Gross vs Taxable vs Net Salary

These four terms appear on different documents and are used for different purposes. Confusing them leads to wrong expectations at every stage. For a more detailed explainer with worked examples, see our guide on gross and net salary differences.

| Salary Term | What It Includes / Excludes | Use This Number For |

|---|---|---|

| CTC | Everything: gross pay + employer EPF + gratuity + benefits. Highest figure on your offer letter | Comparing offers; negotiating increments |

| Gross Salary | Basic + HRA + all fixed allowances. No employer PF or gratuity. What your payslip shows before deductions | TDS computation; loan eligibility letters; Form 16 |

| Taxable Salary | Gross minus standard deduction, HRA exemption, and other permitted adjustments. Lower than gross | Computing income tax; filing ITR; checking tax liability |

| Net / In-Hand Salary | Gross minus EPF, PT, TDS, insurance deductions. Lowest figure — the actual bank credit | Monthly budgeting; deciding on EMI commitments |

How to Decide What’s Right for You

A salary calculator gives you a number — but knowing how to use that number is what matters when evaluating an offer or planning your finances.

You are comparing two job offers — check monthly in-hand fixed pay, not headline CTC. Ask each employer for a complete salary breakup: basic, allowances, variable component, and employer contribution split. A ₹14,00,000 CTC with 30% variable pay may credit ₹8,000–₹12,000 less per month than a ₹12,00,000 CTC with fully fixed guaranteed pay.

You have rent, EMIs, or dependents — calculate net monthly in-hand before committing to any new financial obligation. Fixed monthly obligations ideally should not exceed 50–60% of net salary. Run the numbers before you accept, not after.

Your offer letter shows a large annual bonus or ESOP component in CTC — treat it as uncertain until credited. Budget only on your fixed monthly gross. Variable pay enriches your year when it arrives; it cannot pay rent when it does not.

You are in the 20% or 30% tax bracket and have not submitted investment declarations to HR — your monthly TDS is likely higher than necessary. Submitting HRA rent receipts, 80C proofs (old regime), or NPS contributions can reduce TDS immediately in the same payroll cycle.

You recently switched tax regimes or joined a new company mid-year — inform HR so TDS is recalibrated from your joining date. A mismatch between your actual regime and HR’s assumption can result in either over-deduction (resolved at ITR) or a tax demand at year-end.

Your compensation is primarily commission-based, project-linked, or driven by a variable incentive structure — this calculator cannot give you a reliable monthly in-hand estimate. Your actual take-home depends on performance cycles and payout timing that standard salary calculators are not designed for.

Common Mistakes to Avoid

Treating CTC ÷ 12 as Monthly Take-Home

This is the most expensive planning error most new employees make.

On a ₹12,00,000 CTC, the simple division gives ₹1,00,000/month. After removing employer PF, gratuity, and group insurance, then deducting employee PF, professional tax, and TDS, the actual monthly credit is typically ₹70,000–₹78,000. Locking in an EMI or rent commitment based on the ₹1,00,000 figure creates immediate cash-flow stress.

Always run the full deduction calculation — or use a salary breakup calculator — before making any monthly financial commitments.

Not Accounting for Employer PF and Gratuity in CTC

Employer EPF (12% of basic) and gratuity (~4.81% of basic) are real money — but they inflate CTC without adding to monthly bank credit.

For a ₹40,000/month basic, that is ₹6,724/month or ₹80,688/year of CTC that never reaches you as salary. Both eventually come back to you — EPF on withdrawal, gratuity on exit — but neither improves your monthly cash position today.

When negotiating, ask whether the quoted CTC is inclusive or exclusive of these contributions.

Counting Variable Bonus as Monthly Income

A ₹2,00,000 annual performance bonus in CTC does not mean ₹16,667 extra every month.

Variable pay may be quarterly, annual, performance-linked, or contingent on the company’s financial results. Employees who budget assuming the full CTC÷12 figure — including variable — regularly face mid-year cash shortfalls when bonuses are deferred, reduced, or missed entirely.

Budget on fixed monthly gross only. Treat every variable credit as a bonus when it arrives.

Forgetting Professional Tax Varies by State

Professional tax is a small but consistent deduction that differs significantly by state of employment.

Maharashtra charges up to ₹2,500/year. Karnataka charges ₹2,400/year above a monthly income threshold. Delhi and Haryana do not charge professional tax at all. Employees who relocate for a job or switch between states sometimes discover their in-hand changes by ₹150–₹300/month for this reason alone.

Check your state’s applicable rate and factor it in. Review your salary slip components carefully to identify this and other smaller deductions.

Not Submitting Investment Declarations to HR

If you have 80C investments, home loan interest, NPS contributions, or HRA claims — but have not declared them to HR — your employer will deduct TDS on full taxable salary without applying those benefits.

You will get the benefit back when you file your ITR, but throughout the year your monthly in-hand is lower than it should be. On a ₹12–₹15 lakh income with full 80C utilisation, this difference can be ₹2,000–₹4,000/month.

Submit declarations and investment proofs to HR at the start of the financial year — not in January when it is too late to make a meaningful TDS difference.

Misunderstanding the EPF Wage Ceiling

EPF contributions are mandatory only on basic salary up to ₹15,000/month. So the maximum mandatory employee EPF deduction is ₹1,800/month — even if your basic salary is ₹80,000/month.

However, some employers compute EPF on actual basic salary (not capped), which can increase monthly deductions by ₹2,000–₹7,000 on mid-to-senior salaries. Neither approach is wrong, but not knowing which one your employer follows leads to consistently incorrect in-hand estimates.

Check your payslip or ask HR directly which EPF computation method applies to your payroll.

When This May Not Be the Right Choice

A standard take home salary calculator India gives a reliable planning estimate for most salaried employees with a regular fixed monthly pay structure. It may significantly underestimate or misrepresent your actual in-hand salary if:

- Your CTC contains a large variable component — performance bonuses, incentives, or commissions that are paid quarterly, annually, or tied to individual or company targets.

- Your package includes ESOPs, RSUs, or stock-linked compensation. These have vesting timelines, market value fluctuations, and tax treatment that no salary calculator can model accurately.

- Your company uses a flexi-benefit or flexible pay structure where you allocate components at the start of the year — the taxable vs tax-free split affects net salary differently from a standard fixed-allowance structure.

- You experienced a mid-year salary revision, a tax regime change, or a restructured payroll — any of these can make the calculator’s estimate diverge from your current month’s actual payslip.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Salary deduction rules, income tax slabs, EPF rates, and professional tax regulations are governed by different bodies and are subject to change with each Union Budget or regulatory notification. Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- Income Tax Department — incometax.gov.in: For current income tax slabs, standard deduction amount, TDS rules under both regimes, Section 87A rebate eligibility, and the online tax calculator for salaried employees.

- EPFO (Employees’ Provident Fund Organisation) — epfindia.gov.in: For EPF contribution rates, the current statutory wage ceiling, voluntary PF contribution rules, and your EPF passbook balance.

- Your state government’s finance or revenue department: For professional tax slabs applicable in your state. Professional tax is a state subject — rates, income thresholds, and applicability differ. See our professional tax impact guide for a state-by-state overview.

- Your employer’s HR or payroll team: For the exact CTC structure, EPF computation method (actual basic vs ₹15,000 ceiling), and any employer-specific deductions that a generic calculator cannot know.

Expert Tips

- Ask HR for a salary breakup document before accepting any offer. Request a month-by-month view that separates fixed pay, variable pay, and employer contributions. This single document tells you more than any calculator. Many candidates only see this breakup after their first payslip — by then the offer is already accepted.

- Compare annual guaranteed cash — not headline CTC. Guaranteed annual cash = (basic + HRA + fixed allowances) × 12. Exclude bonuses, ESOPs, and employer PF when setting your monthly budget. This is the floor your lifestyle actually depends on.

- Submit investment declarations to HR in April, not February. Submitting early applies the benefit across all 12 TDS computations. Submitting in January or February means you only benefit in the last 2–3 months. The earlier you declare, the higher your monthly in-hand throughout the year.

- Confirm whether your employer caps EPF at the ₹15,000 wage ceiling or computes it on actual basic salary. On a ₹60,000/month basic, the difference is ₹7,200 per month in deductions versus ₹1,800. Knowing this changes your in-hand estimate significantly on higher salaries.

- Recalculate your estimated in-hand after every salary hike, bonus, or tax declaration change. Most employers recalculate TDS quarterly. A mid-year hike can increase monthly TDS deduction from the very next payroll cycle — a fact that catches many employees off guard when they expected a larger net increase.

- Use the calculator output as a planning floor, not a guaranteed figure. Especially in your first month at a new employer — payroll set-up delays and declaration mismatches are common. Build your budget on the lower end of your estimate until two full payslips have confirmed the structure.

Frequently Asked Questions

Is CTC the same as in-hand salary?

No. CTC is the total annual cost your employer incurs — it includes your gross salary plus employer contributions to EPF, gratuity, health insurance, and other benefits. These employer-side costs are part of CTC but are never credited to your bank account. Your monthly in-hand salary is typically 20–35% lower than your CTC divided by 12, depending on your salary structure and income level.

How do I calculate monthly in-hand salary from CTC?

Subtract employer-side costs (employer EPF, gratuity, group insurance) from annual CTC to get annual gross salary. Divide by 12 for monthly gross. Then subtract employee EPF (12% of basic, subject to wage ceiling), professional tax (state-specific), TDS based on your income and regime, and any other deductions. The result is your estimated monthly in-hand. Scroll to the “How to Calculate” section above for the step-by-step formula with a worked ₹12 LPA example.

Does EPF reduce my take-home salary?

Yes — your employee EPF contribution (12% of basic) is deducted from gross salary before the bank credit, which reduces monthly in-hand. However, this money goes into your own EPF account, earns tax-free interest, and is accessible on withdrawal. It is forced savings, not a loss. Employer EPF is a separate contribution — it is part of CTC and also goes to your PF account, but it was never part of your gross pay to begin with.

Does professional tax apply in every Indian state?

No. Professional tax is a state-level levy and is not universal. Maharashtra (up to ₹2,500/year), Karnataka (₹2,400/year above a monthly income threshold), and several other states charge it. Delhi, Haryana, Uttarakhand, and a number of others do not. Verify the applicable rate for your state of employment before finalising your in-hand estimate.

Why is my salary credited lower than expected?

The most common reasons are: employer EPF and gratuity included in CTC but not credited; employee EPF, professional tax, and TDS deducted from gross; variable pay not included in the current month’s payout; health insurance or loan recovery deductions; and tax declarations not yet processed by HR. Pull up your payslip line by line — every deduction must be itemised there.

Can two people with the same CTC have different in-hand salaries?

Yes, and this is very common. Salary structure (basic-to-allowance ratio), tax regime choice, investment declarations, state professional tax, employer EPF computation method (capped vs actual basic), health insurance deduction policy, and variable pay proportion can all differ between companies. Two offers with identical ₹12,00,000 CTCs can produce monthly in-hand salaries that differ by ₹5,000–₹15,000 for these reasons alone.

What is the standard deduction for salaried employees?

The standard deduction is a flat amount deducted from gross salary before computing income tax — available under both the old and new tax regimes. The applicable amount for the current financial year should be verified directly from incometax.gov.in, as it is subject to revision with each Budget announcement.

How does my tax regime choice affect monthly in-hand?

Your regime choice directly changes your monthly TDS computation. The new regime generally suits employees with fewer eligible deductions or lower incomes; the old regime can deliver better outcomes if you have significant 80C, HRA, NPS, or 80D claims. Inform HR of your regime preference at the start of the financial year. A wrong assumption by HR can result in higher-than-necessary TDS throughout the year — refunded only after ITR filing.

Is variable pay included in the take home salary calculator estimate?

Standard salary calculators estimate in-hand based on fixed monthly components only. Variable pay — bonuses, incentives, and quarterly payouts — is not included because it is uncertain in timing and amount. For monthly planning, add variable pay to your estimate only when it is actually credited to your account, not when it appears in your CTC.

Final Verdict

A take home salary calculator India is most useful when you run it before signing an offer — not after wondering why your first payslip does not match your expectations. Input your CTC, remove employer-side costs, account for EPF, professional tax, and TDS, and arrive at a monthly in-hand figure you can actually plan around.

For salaried employees with a straightforward fixed pay structure, the calculator gives a reliable planning estimate. For those with heavy variable components, ESOP-driven CTCs, or non-standard payroll structures, treat the output as a floor and validate the specifics with HR, your offer letter, and your first actual payslip.

The calculator works best when you understand what goes into it. For the fundamentals of how salary flows from offer letter to bank account, our guide on the CTC and in-hand difference is the right place to start. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.