Your salary slip shows a deduction labelled “Employee PF” every month. Your offer letter CTC includes a line called “Employer PF.” And when you log into the EPFO portal, your passbook shows numbers that don’t match either of those. This is the exact confusion that the employee PF vs employer PF contribution question is designed to solve. The two contributions are different in amount, in purpose, and in where they ultimately go — and understanding the split will permanently change how you read your payslip, your CTC, and your retirement balance.

Most salaried employees assume employer PF is simply a mirror of what gets deducted from their salary. It is not. Part of the employer’s share goes to a separate pension fund — not your EPF account — and the math behind it matters far more than you think.

Quick Answer: Employee PF vs Employer PF Contribution

Employee PF vs employer PF contribution means your PF deduction and the company’s PF share are not the same. Usually employee PF is 12% of eligible wages, employer also contributes but part may go to EPS pension, so your salary slip and EPF passbook must be read together.

Key Takeaways

- Employee PF contribution is 12% of your basic wages + DA — deducted from your salary every month and deposited entirely into your EPF account.

- Employer contributes 12% too, but the money is split: 8.33% (capped at ₹1,250/month based on a ₹15,000 wage ceiling) goes to the Employees’ Pension Scheme (EPS), and the remaining amount goes into your EPF account.

- If your basic salary is ₹40,000/month, your EPF passbook receives ₹4,800 from you and ₹3,550 from your employer — not ₹4,800. The remaining ₹1,250 of your employer’s contribution goes to EPS, not your EPF balance.

- The EPS portion funds a monthly pension after retirement (age 58+) — it does not appear as a lump-sum balance in your EPFO passbook and cannot be withdrawn the way EPF can (after 10 years of EPS membership).

- Employer PF is part of your CTC. It does not increase your take-home pay. It is a cost to your employer that you do not receive monthly — ever.

- Only the EPF portion of both contributions earns annual EPF interest announced by EPFO. The EPS portion earns a separate government-specified yield and is paid out as pension, not as a balance.

- If your employer is not depositing PF on time, your EPF passbook will show gaps or lower-than-expected employer credits — always verify through your UAN account monthly.

Key Facts at a Glance

| Parameter | Employee PF | Employer PF |

|---|---|---|

| Contribution rate | 12% of basic wages + DA | 12% of basic wages + DA (split into EPS + EPF) |

| Goes to EPF account | 100% of contribution | 12% × wages minus ₹1,250 (for wages above ₹15,000) |

| Goes to EPS pension | Nothing | 8.33% of wages, capped at ₹1,250/month |

| EPS wage ceiling | Not applicable | ₹15,000/month |

| Reduces take-home salary | Yes — deducted from gross pay | No — part of employer’s CTC cost |

| Visible in EPF passbook | Yes — full amount monthly | Only the EPF portion (not EPS) |

| Tax on withdrawal | Tax-free after 5 continuous years of service | Tax-free on EPF portion after 5 years; EPS paid as pension |

Understanding Employee PF vs Employer PF Contribution in Full

What “Eligible Wages” Means for EPF

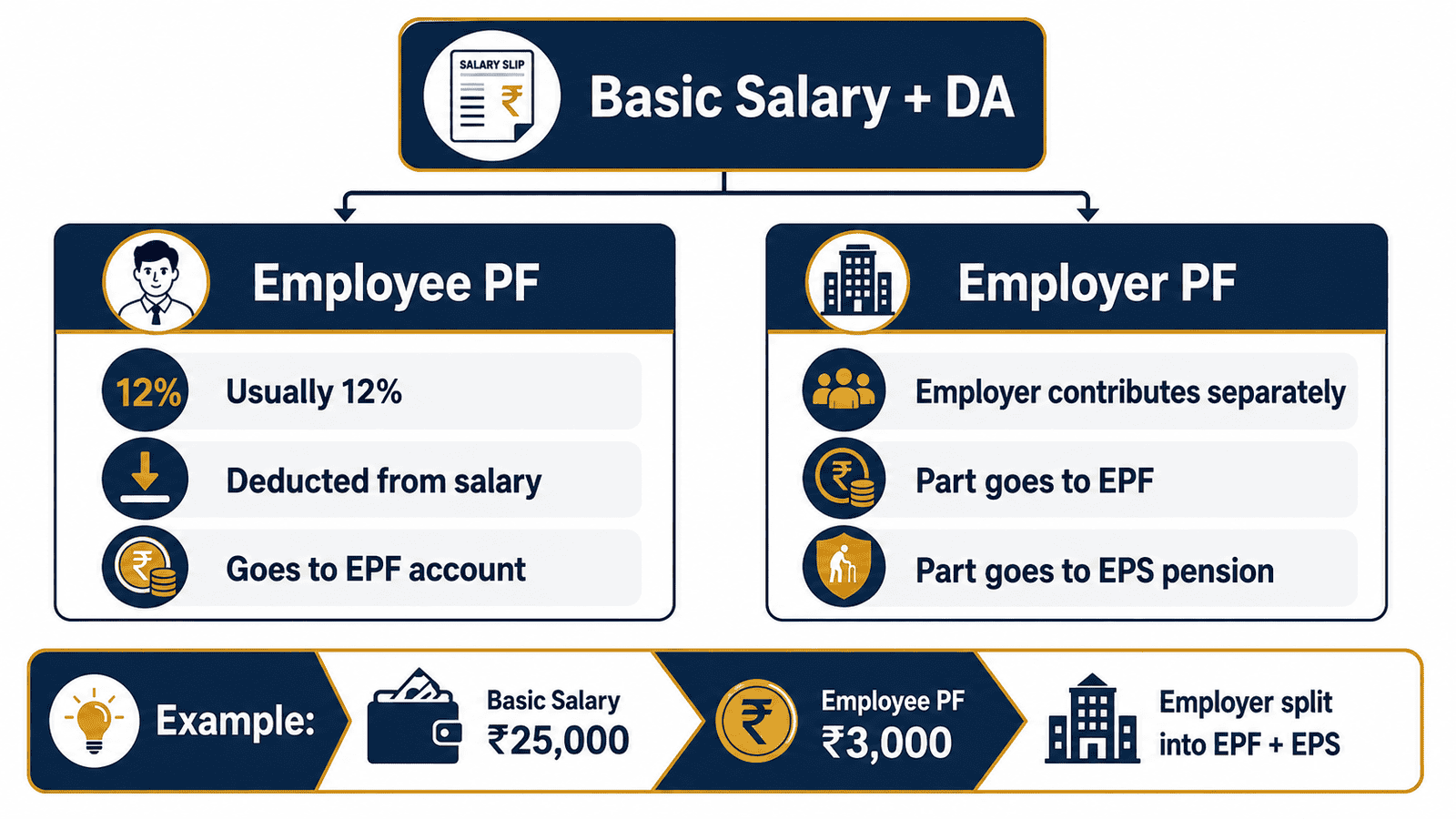

Both employee and employer PF contributions are calculated on “basic wages + Dearness Allowance (DA)” — commonly labelled “EPF wages” on your payslip. This is almost always lower than your gross salary. HRA, LTA, travel reimbursements, and most variable allowances are excluded from the EPF calculation base. If your gross is ₹80,000 but your basic + DA is ₹40,000, all PF arithmetic happens on ₹40,000.

This matters because a lower EPF wage reduces how much flows into your retirement account every month. Some employers deliberately structure salary to limit EPF liability — which is legal within bounds but reduces your long-term corpus. Understanding exactly what is included in your EPF wages is the first step; a close reading of salary slip components will show you which pay heads qualify and which do not.

Employee PF Contribution: The Straightforward Half

Your contribution is clean and simple: 12% of your EPF wages is deducted from your salary every month and deposited entirely into your EPF account (EPFO Account No. 1). If your basic + DA is ₹40,000, ₹4,800 leaves your in-hand pay and appears as a monthly credit under “Employee Share” in your EPFO passbook.

Every rupee of your employee contribution earns the annual EPF interest rate declared by EPFO. You own this money outright and can withdraw it — subject to EPFO conditions — when you leave employment, retire, or meet specific withdrawal criteria (housing, medical, marriage, etc.).

You can also contribute more than the mandatory 12% through VPF (Voluntary Provident Fund). The additional amount earns the same EPF interest, qualifies under Section 80C within the ₹1.5 lakh annual ceiling, and goes entirely into your EPF account. Your employer is not legally required to match your VPF contributions.

Employer PF Contribution: The Split That Confuses Everyone

Your employer also contributes 12% of your EPF wages — but that amount does not all go into your EPF account. According to EPFO guidelines, the employer’s 12% is allocated as follows:

- 8.33% goes to EPS (Employees’ Pension Scheme, Account No. 10) — but only on wages up to ₹15,000/month. If your basic salary is ₹60,000, the EPS calculation still uses ₹15,000 as the ceiling. Maximum EPS monthly contribution: 8.33% × ₹15,000 = ₹1,250.

- The remainder goes into your EPF account — this is the employer’s EPF credit you see in your EPFO passbook. For wages above ₹15,000, this is calculated as: (12% × actual wages) minus ₹1,250.

You will often see the figure “3.67%” cited for the employer’s EPF rate. This is accurate only when EPF wages equal exactly ₹15,000 (since 3.67% + 8.33% = 12%). For most salaried employees with basic salaries above ₹15,000, the employer’s actual EPF passbook credit is higher than 3.67% of wages — because EPS is capped at ₹1,250 while the total employer share keeps growing with salary. For a basic of ₹40,000: employer EPF = ₹4,800 − ₹1,250 = ₹3,550. That is 8.875% of wages, not 3.67%.

What Is EPS and Why Does It Matter?

EPS is the Employees’ Pension Scheme — a government-administered pension pool within the EPFO framework. When your employer deposits ₹1,250/month to EPS, that money is merged into a collective fund. You do not see an individual EPS balance in your passbook. Instead, EPS credits your service years — and after 10 years of EPS membership and reaching age 58, you become eligible for a monthly pension calculated on your last pensionable salary and total service years.

If you leave employment before completing 10 years of EPS membership, you can apply to withdraw the EPS accumulation as a lump sum (the amount is calculated per a government formula — it is not the sum of all ₹1,250 deposits). After 10 years, lump-sum withdrawal is replaced by pension entitlement. This distinction is critical for anyone planning early retirement or frequent job changes.

Why Your CTC and EPF Passbook Don’t Match

Your employer includes the full 12% contribution in your CTC. For a basic of ₹40,000/month, that is ₹4,800/month or ₹57,600/year. But your EPF passbook employer credit is only ₹3,550/month — because ₹1,250 of the employer’s contribution goes to EPS instead. Over a year, that is a ₹15,000 gap between what your CTC shows and what your EPF passbook actually receives from the employer. This is not an error. This is the EPS split working exactly as designed.

Real Example: Aarav’s Salary Slip and EPF Passbook

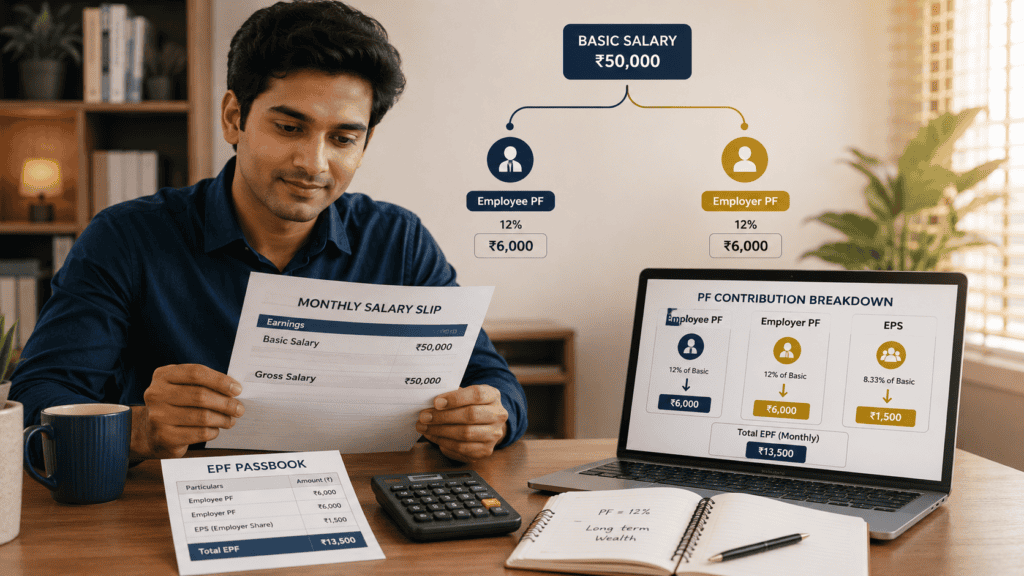

Aarav, 28, is a software engineer at a product company in Bengaluru. His annual CTC is ₹12 lakh. His monthly CTC breakup: basic salary ₹40,000, HRA ₹16,000, special allowance ₹26,720, and employer PF ₹4,800 — totalling ₹87,520 CTC per month before annualising. His actual monthly in-hand pay is around ₹73,920 after his own PF deduction, professional tax, and income tax TDS.

His salary slip shows a deduction of ₹4,800 for Employee PF. When Aarav logs into his UAN passbook, he expects to see a matching ₹4,800 employer credit. Instead, he sees ₹3,550. Here is exactly why:

- EPF wages: ₹40,000 (basic salary only, no DA component in his salary)

- Employee PF: 12% × ₹40,000 = ₹4,800 → credited to EPF passbook

- Employer total contribution: 12% × ₹40,000 = ₹4,800

- Employer EPS: 8.33% × ₹15,000 (wage ceiling applies) = ₹1,250 → goes to EPS pension pool, not passbook

- Employer EPF: ₹4,800 − ₹1,250 = ₹3,550 → credited to EPF passbook

Aarav’s total EPF passbook deposit every month is ₹8,350 (₹4,800 from him + ₹3,550 from his employer). His employer also deposits ₹1,250 to EPS — but Aarav will only see that as pension income after age 58, provided he accumulates 10+ years of EPS service. The key insight: the ₹4,800 “Employer PF” line in Aarav’s CTC is not the same as the ₹3,550 employer credit in his EPF passbook.

How to Calculate the EPF Contribution Split

Employee EPF = 12% × (Basic Salary + DA)

Employer EPS = 8.33% × lower of (Basic + DA, ₹15,000) — maximum ₹1,250/month

Employer EPF (passbook credit) = (12% × Basic + DA) − Employer EPS

Applying the formula to Aarav’s figures step by step:

- Basic + DA: ₹40,000

- Employee PF: 12% × ₹40,000 = ₹4,800

- Employer total: 12% × ₹40,000 = ₹4,800

- Employer EPS: 8.33% × ₹15,000 = ₹1,250 (wage ceiling applies since ₹40,000 > ₹15,000)

- Employer EPF passbook credit: ₹4,800 − ₹1,250 = ₹3,550

- Total monthly EPF passbook deposit: ₹4,800 + ₹3,550 = ₹8,350

| Scenario | Basic Salary | Total Monthly EPF Passbook Credit |

|---|---|---|

| Entry-level employee | ₹20,000/month | ₹3,550 (₹2,400 employee + ₹1,150 employer) |

| Aarav — mid-level engineer | ₹40,000/month | ₹8,350 (₹4,800 employee + ₹3,550 employer) |

| Senior engineer | ₹80,000/month | ₹17,950 (₹9,600 employee + ₹8,350 employer) |

Use the PF calculator guide to see how these monthly deposits compound over your career. Or go straight to the EPF contribution calculator to enter your exact basic salary and get the full monthly breakdown instantly.

Comparison: Employee PF Contribution vs Employer PF Contribution

| Parameter | Employee PF | Employer PF |

|---|---|---|

| Who funds it | You | Your company |

| Rate | 12% of EPF wages | 12% of EPF wages (split into two pools) |

| Goes to EPF passbook | 100% | Partial — 12% × wages minus ₹1,250 |

| Goes to EPS pension | No | Yes — up to ₹1,250/month |

| Reduces take-home pay | Yes | No |

| Earns EPF interest | Yes — full amount | Only the EPF passbook portion |

| Accessible on resignation | Yes — full balance | EPF portion yes; EPS as lump sum or pension |

| Shows in CTC | No | Yes — full 12% in CTC |

How to Decide What’s Right for You

You want to grow your EPF corpus faster without taking market risk — THEN activate VPF (Voluntary Provident Fund) through HR. Every extra rupee goes entirely into your EPF account, earns the same EPF interest rate, and qualifies under Section 80C within ₹1.5 lakh. Your employer’s EPS/EPF split does not affect VPF contributions.

You are evaluating two job offers and comparing CTC figures — THEN subtract employer PF from both CTCs before comparing. Employer PF is a retirement contribution you cannot access monthly, and it inflates CTC without affecting take-home. Understanding how CTC and in-hand differ will help you make an accurate comparison.

You have been contributing to EPS for 8 or 9 years and are considering resigning — THEN crossing 10 years of EPS membership qualifies you for a lifelong monthly pension after age 58. One more year of EPS service could make a meaningful difference to retirement income. Factor this in before finalising any job change timeline.

Your EPF passbook shows zero or unusually low employer credits for recent months — THEN your employer may have missed deposit deadlines. File a complaint at the EPFO grievance portal (epfigms.gov.in) immediately. Delayed deposits mean lost EPF interest, and the employer is liable for penalty.

Your basic salary is below ₹15,000/month — THEN the EPS wage ceiling does not cap your employer’s EPS contribution. The full 8.33% of your actual basic goes to EPS, leaving only 3.67% of your basic as the employer EPF credit. Your EPF passbook employer credit will be relatively small.

You do not plan to stay employed in India for 10+ cumulative years of EPS membership — THEN do not count on EPS pension income for retirement planning. Budget only your EPF corpus and any separate instruments (NPS, mutual funds). Rely on EPS only once you have secured 10 qualifying service years.

Common Mistakes to Avoid

Assuming the Full Employer PF in CTC Goes to Your EPF Passbook

Many employees see ₹4,800 as employer PF in CTC and expect a matching ₹4,800 employer credit in their EPFO passbook.

For a basic of ₹40,000, the actual employer EPF passbook credit is ₹3,550 — not ₹4,800. The gap of ₹1,250/month is ₹15,000/year that goes to EPS, not your EPF balance. Over 25 years, misunderstanding this can cause a significant shortfall in retirement corpus estimates.

Always calculate your employer EPF passbook credit as: (12% × your basic) minus ₹1,250, not as a flat 12%.

Not Verifying Employer Deposits Every Month

EPFO requires employers to deposit contributions by the 15th of the following month. Many smaller employers delay. Some skip months entirely — which is illegal.

Late deposits mean you lose EPF interest on that month’s contribution. Missing deposits mean your retirement savings are being withheld. The loss is invisible unless you actively check your passbook.

Log into your UAN account every month and cross-check that the employer credit matches approximately (12% × your basic) minus ₹1,250.

Treating EPS as a Savings Balance You Can Withdraw Freely

EPS is a pension pool — not a personal savings account. You cannot see an individual EPS balance on your passbook. You cannot withdraw EPS like EPF whenever you want.

Before 10 years of EPS service, you can take a lump-sum withdrawal calculated on a specific government formula. After 10 years, you can only claim a monthly pension — not a lump sum. Withdrawing EPF and EPS together on every job change destroys your pension entitlement and requires restarting the 10-year count from zero.

Assuming EPS Earns EPF Interest

Only the EPF balance in your passbook earns the annual EPF interest rate announced by EPFO. The ₹1,250/month flowing to EPS goes into a government pool with a different actuarial yield — it does not compound the same way.

Do not add an estimated “EPS balance” to your EPF balance when projecting your retirement corpus. The two pools have completely different payout structures.

Thinking PF Is Automatically Calculated on Gross Salary

PF is calculated on basic wages + DA only. If your gross is ₹90,000 but basic + DA is ₹30,000, your employee PF deduction is ₹3,600, not ₹10,800. A low basic salary structure — common in CTC-heavy packages — drastically reduces your EPF accumulation over time.

Review your EPF wages component annually, especially after a salary revision. If your basic salary has not grown proportionally, your EPF corpus will fall short.

Withdrawing EPF Instead of Transferring It on a Job Change

Every EPF withdrawal on resignation resets your EPS service record if done before 10 cumulative years. You also lose the interest compounding chain, break your 80C contribution history, and may owe tax if you have less than 5 continuous years of service at the time of withdrawal.

Use the EPFO online transfer facility every time you change jobs. Transfer, not withdraw, is almost always the better financial decision.

Ignoring VPF as a Low-Risk 80C Savings Tool

Some employees want to save more than 12% but default to PPF, not realising that VPF (Voluntary Provident Fund) offers the same EPF interest rate and Section 80C benefit with far simpler mechanics — it routes through your existing payroll rather than requiring a separate bank investment.

If you are in the 30% bracket and have unused 80C space, ask HR to activate VPF before the financial year begins. You cannot usually start mid-year in most payroll systems.

When This May Not Be the Right Choice

EPF is a well-designed long-term savings instrument for salaried employees — but the contribution structure has real limitations for specific situations:

- If you are on contract, gig, or freelance work — employers who are not registered under the EPF Act have no legal obligation to contribute. Self-employed individuals and freelancers cannot participate in EPF at all. There is no employer contribution to count on.

- If your employer structures a very low basic salary — a basic of 20–25% of CTC means your EPF wages are minimal. Your cumulative EPF corpus over 20–30 years may be substantially lower than someone with a 40–50% basic, even at identical CTC levels. EPF alone may not be sufficient for retirement in this case.

- If you have high near-term liquidity needs — EPF has strict withdrawal rules and a five-year lock-in for tax-free exits. If you expect to need access to savings in the next two to three years, locking a significant amount into EPF (where early withdrawal can attract tax) may create problems.

- If you are close to retirement with less than 10 years of cumulative EPS service — the EPS pension benefit will not be available. Factor in only your EPF balance for retirement income projections and supplement aggressively with NPS or other instruments.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

EPF contribution rates, EPS wage ceilings, interest rates, and withdrawal conditions are set by EPFO and the Ministry of Labour and Employment. These figures change with government notifications — sometimes without widely publicised announcements. Always verify the current numbers before making any salary negotiation, job change, or retirement planning decision.

- EPFO — epfindia.gov.in (contribution rates, EPS rules, passbook access, grievance filing, withdrawal forms)

- Income Tax Department — incometax.gov.in (tax treatment of EPF withdrawal, employer contribution taxability, Section 80C rules)

To verify your actual EPF balance and confirm that your employer is depositing on time, check PF balance directly on the EPFO member portal. You will need to understand your UAN first — your Universal Account Number is the login credential for all EPFO self-service functions, including passbook, transfer requests, and grievances.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Reconcile your EPF passbook every quarter — download it from the EPFO member portal and verify the employer credit against your own calculation: (12% × basic) minus ₹1,250. If the actual credit is off by more than ₹100 for two consecutive months, raise it with HR and then with EPFO’s grievance portal before the financial year closes.

- Negotiate a higher basic salary when joining a new company — a higher basic increases both your EPF accumulation and your EPS pensionable salary. Yes, your monthly PF deduction goes up too, but the long-term compounding on a higher EPF base can significantly outweigh the short-term take-home reduction.

- Activate VPF if you are in the 30% tax bracket and have unused 80C space — VPF earns the same rate as EPF, has zero market risk, and does not require a separate bank account or investment form. Ask HR to activate it before April 1 — most payroll systems cannot process VPF start requests mid-year.

- Before resigning, check your total EPS service years on the EPFO portal — if you are at 8 or 9 cumulative years, staying one or two more years takes you past the 10-year threshold and makes you eligible for a monthly pension at age 58. This is a retirement benefit most employees overlook entirely.

- Always transfer EPF when changing jobs, never withdraw — online transfer via the EPFO member portal typically completes in 7–20 working days. It preserves your EPS service count, keeps your EPF interest compounding unbroken, and avoids tax on early withdrawal.

- If employer EPF credits are missing for two or more months, act immediately — file a grievance at epfigms.gov.in. Delayed employer deposits attract penalty and interest from the employer. EPFO will enforce the deposit; your EPF account will be credited with the applicable interest once the compliance is enforced.

Frequently Asked Questions

What is the exact difference between employee PF and employer PF contribution?

Employee PF is 12% of your basic wages + DA, deducted from your salary and deposited entirely into your EPF account. Employer PF is also 12% of basic wages + DA but split: 8.33% (capped at ₹1,250/month) goes to EPS pension, and the balance goes into your EPF account. So your passbook shows your full 12% plus only the employer’s remaining share after the EPS deduction.

Why does my employer’s EPF passbook credit not equal the employer PF shown in my CTC?

Because ₹1,250/month of your employer’s contribution is routed to the Employees’ Pension Scheme (EPS), which does not appear as an individual balance in your EPFO passbook. Only the portion remaining after the EPS deduction — which is (12% × your basic wages) minus ₹1,250 — is credited to your personal EPF account. The EPS amount is pooled and converted into pension after retirement.

Is employee PF contribution eligible for tax deduction?

Yes. Your employee EPF contribution qualifies as a deduction under Section 80C of the Income Tax Act, within the combined ₹1.5 lakh annual ceiling that also covers PPF, ELSS, life insurance premiums, and other eligible items. This deduction is available only under the old tax regime — if you opt for the new tax regime, Section 80C deductions are not available.

What happens to my EPS amount if I resign before completing 10 years of service?

If you resign before 10 cumulative years of EPS membership, you can withdraw the EPS accumulation as a lump sum. The amount is calculated per a government-prescribed formula based on your last drawn pensionable salary and total EPS service — it is not simply the sum of all ₹1,250 monthly deposits. After 10 years of EPS membership, lump-sum withdrawal is replaced by eligibility for a monthly pension from age 58 onwards.

Can I ask my employer to increase their EPF contribution above 12%?

No — employers are legally required to contribute 12% of EPF wages and are not obligated to contribute more. You can increase your own contribution through VPF (Voluntary Provident Fund), but the additional amount does not trigger any employer matching. A small number of large companies offer enhanced employer PF as a benefit — check your offer letter or ask HR specifically about this.

Is the employer PF contribution taxable in my hands?

Employer contributions to EPF are tax-free up to a combined annual limit covering EPF, NPS, and superannuation together. If the total employer contribution across all three schemes exceeds ₹7.5 lakh in a financial year, the excess is taxable as a perquisite. For most salaried employees with a basic salary below ₹5 lakh per month, this threshold will not be crossed. Verify the current threshold at incometax.gov.in before salary negotiations.

What is the EPS wage ceiling and how does it affect my retirement?

The EPS wage ceiling is ₹15,000/month — this is the maximum pensionable salary used to calculate both the employer’s EPS contribution and your eventual monthly pension. Even if your basic salary is ₹1 lakh/month, EPS is calculated on ₹15,000. This means the maximum monthly pension payable under EPS is based on a relatively modest wage, which significantly limits pension income for high-earning employees. Supplement EPS with NPS or other instruments for adequate retirement income.

What is the difference between EPF and EPS?

EPF (Employees’ Provident Fund) is your personal savings account — contributions accumulate, earn annual interest, and are paid as a lump sum on retirement or resignation (after five continuous years for tax-free exit). EPS (Employees’ Pension Scheme) is a pension pool — the employer’s ₹1,250/month is pooled across all members and paid as a monthly pension after age 58 for members with 10+ years of service. Both are administered by EPFO but function entirely differently at payout.

How do I verify that my employer is depositing PF correctly and on time?

Log into the EPFO member portal (unifiedportal-mem.epfindia.gov.in) using your UAN and password. Download your passbook and check the employer share credits month by month. The employer credit should roughly equal (12% × your basic wages) minus ₹1,250. Any month showing zero employer credit or a significantly lower amount may indicate a missed or delayed deposit. File a grievance at epfigms.gov.in if deposits are consistently missing.

Does PF contribution apply to all salary components or just basic salary?

PF contribution applies only to “EPF wages” — basic salary plus any Dearness Allowance (DA). HRA, LTA, food coupons, travel reimbursements, and most special allowances are excluded. Some employers keep basic salary low specifically to reduce both the employee’s EPF deduction and the employer’s own PF liability. This is legal within limits, but it reduces your long-term EPF corpus. Check your payslip to identify exactly what is included in your EPF wages.

Final Verdict

The employee PF vs employer PF contribution split is one of the most misunderstood parts of the Indian salary structure — and the confusion costs people real money in retirement planning. Your 12% deduction goes entirely into your EPF account. Your employer’s 12% is split: the portion remaining after the ₹1,250 EPS deduction lands in your EPF passbook, and ₹1,250/month goes to EPS pension. These are two separate pools, with two separate payouts, and two separate rules. Understanding this helps you read your payslip accurately, estimate your retirement corpus honestly, and decide whether to activate VPF, negotiate your basic salary, or simply verify that your employer is actually depositing on time. For further planning, explore the EPF contribution calculator to model different scenarios with your own salary figures. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Raghav Menon writes about employment-linked retirement benefits in India, including EPF, PF, UAN, gratuity, EPS pension, EDLI, VPF, superannuation, and NPS-related salary benefits. His content is designed for employees who see deductions and benefit components in their salary structure but do not fully understand how those amounts work over time.

He covers practical topics such as EPF contribution, employer PF, employee PF, PF withdrawal rules, PF transfer after job change, UAN activation, PF balance checks, EPFO claim status, multiple PF account merging, EPF nomination, gratuity calculation, EPS pension eligibility, EDLI benefits, and tax treatment of PF withdrawals. His articles are useful for freshers, job switchers, employees planning resignation, and families thinking about retirement-linked savings.

Raghav’s writing is rule-focused, patient, and structured around common employee doubts. He aims to simplify official processes without overpromising outcomes. Since EPFO procedures, interest rates, withdrawal rules, contribution limits, and tax treatment may change, readers should verify current rules from EPFO, Income Tax Department, and relevant official sources.