You earn ₹95,000 a month, you want to put away ₹10,000 or ₹15,000 every month, and someone told you a SIP calculator India can show exactly how much wealth that monthly habit will eventually become. You punch in the numbers — and a corpus figure appears that looks almost too large to believe. Right after that comes the question that stops every thoughtful first-time investor: is this a promise or a projection?

A SIP calculator India does one thing very well — it shows how compound growth works on regular monthly investments, using a fixed assumed rate of return. What it cannot show you is the actual future. Markets move up and down, fund performance varies, and inflation quietly erodes purchasing power. This guide explains how to use the calculator correctly, how to read the output honestly, and how to convert an estimated corpus into a goal you can actually plan around.

Quick Answer: SIP Calculator India

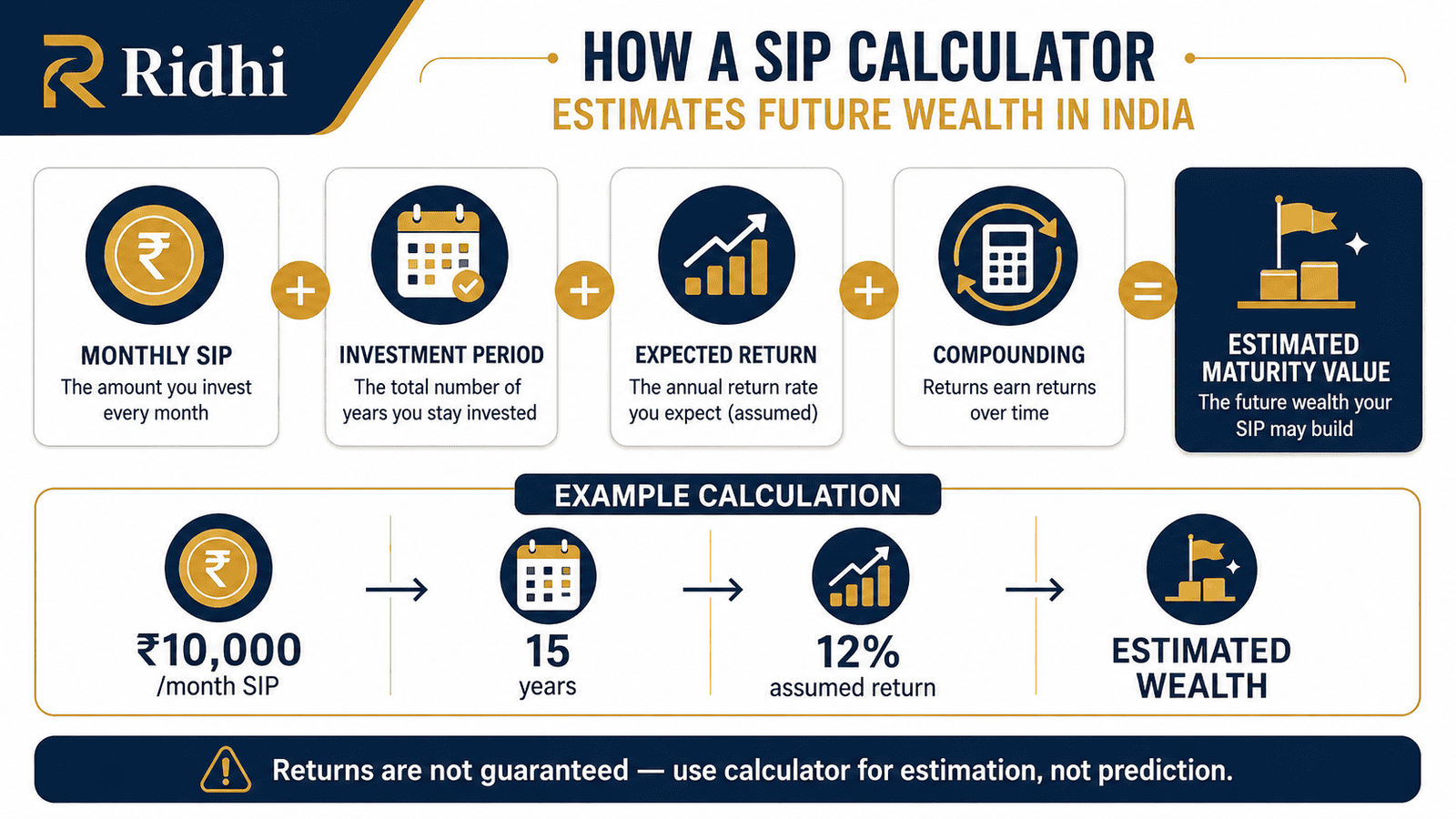

SIP calculator India helps you estimate how a monthly mutual fund investment may grow over time. For example, a ₹10,000 monthly SIP for 15 years at an assumed 12% annual return can show an estimated corpus, but actual returns depend on market performance, fund choice, costs, and investment discipline.

How to Calculate Your SIP Maturity Value

Every SIP calculator India runs the same compound-interest formula for periodic investments. Here it is in plain form:

M = P × {[(1 + r)^n – 1] ÷ r} × (1 + r)

M = Estimated maturity value | P = Monthly SIP amount | r = Monthly rate of return (annual rate ÷ 12) | n = Total months (years × 12)

Step-by-Step: ₹10,000 Monthly SIP, 15 Years, 12% Annual Return

Monthly rate (r) = 12% ÷ 12 = 1% = 0.01

Total months (n) = 15 × 12 = 180

Estimated maturity value ≈ ₹50,45,740

Amount you actually invest: ₹10,000 × 180 months = ₹18,00,000

Estimated gains from compounding: ₹50,45,740 − ₹18,00,000 = ₹32,45,740

This is where the power of long compounding becomes visible — your estimated returns (₹32.5 lakh) are nearly 1.8 times the amount you actually put in (₹18 lakh). The longer the tenure, the wider that gap becomes.

SIP Projections at Different Amounts, Tenures, and Return Assumptions

| Monthly SIP / Tenure / Assumed Return | Total Invested | Estimated Corpus |

|---|---|---|

| ₹5,000 / 10 years / 12% | ₹6,00,000 | ₹11,61,695 |

| ₹10,000 / 15 years / 12% | ₹18,00,000 | ₹50,45,740 |

| ₹10,000 / 15 years / 8% | ₹18,00,000 | ₹34,60,435 |

| ₹20,000 / 20 years / 12% | ₹48,00,000 | ₹1,99,82,734 |

Notice the third and second rows: dropping the assumed return from 12% to 8% for the same ₹10,000 SIP over 15 years cuts the estimated corpus by approximately ₹16 lakh — from ₹50.5 lakh to ₹34.6 lakh. The return assumption is the single most important input in any SIP calculation. Get it wrong and your entire plan is built on shaky ground.

Key Takeaways

- A ₹10,000 monthly SIP for 15 years at an assumed 12% annual return estimates a corpus of ₹50,45,740 — against ₹18,00,000 actually invested.

- Changing the assumed return from 12% to 8% on the same SIP reduces the estimated corpus by approximately ₹16 lakh — use 10%–12% as your base planning range for equity funds, not 15%+.

- Every SIP calculator India uses a fixed return assumption. Actual mutual fund returns fluctuate year to year and are never guaranteed. Mutual fund investments are subject to market risks.

- The calculator does not factor in a fund’s expense ratio — typically 0.5%–1% for direct plans and 1%–2.5% for regular plans — which reduces your effective annual return.

- ₹50 lakh in 15 years does not buy what ₹50 lakh buys today. At 6% inflation, that corpus’s real purchasing power is approximately ₹20–22 lakh in today’s terms. Always plan with inflation in mind.

- ELSS-based SIPs offer a Section 80C deduction on contributions up to ₹1,50,000 per year under the old tax regime, but carry a 3-year lock-in per SIP instalment.

- A step-up SIP — increasing the monthly amount by 10% each year — can nearly double the estimated corpus over 15–20 years compared to a flat SIP at the same starting amount.

Key Facts at a Glance

| Parameter | Detail | Note |

|---|---|---|

| Minimum SIP amount | ₹100 per month (most AMCs) | Varies by fund and AMC |

| Lock-in period | None for open-ended equity funds; 3 years per instalment for ELSS | ELSS lock-in applies per SIP instalment, not the whole portfolio |

| Return assumption range | 10%–12% for equity; 6%–8% for debt or hybrid funds | Historical reference only — not guaranteed |

| LTCG tax (equity MF) | 12.5% on gains above ₹1,25,000/year | Verify current rate at incometax.gov.in before redemption |

| STCG tax (equity MF) | 20% if units held under 1 year | Verify current rate at incometax.gov.in |

| Regulated by | SEBI — sebi.gov.in | All mutual funds must be SEBI-registered |

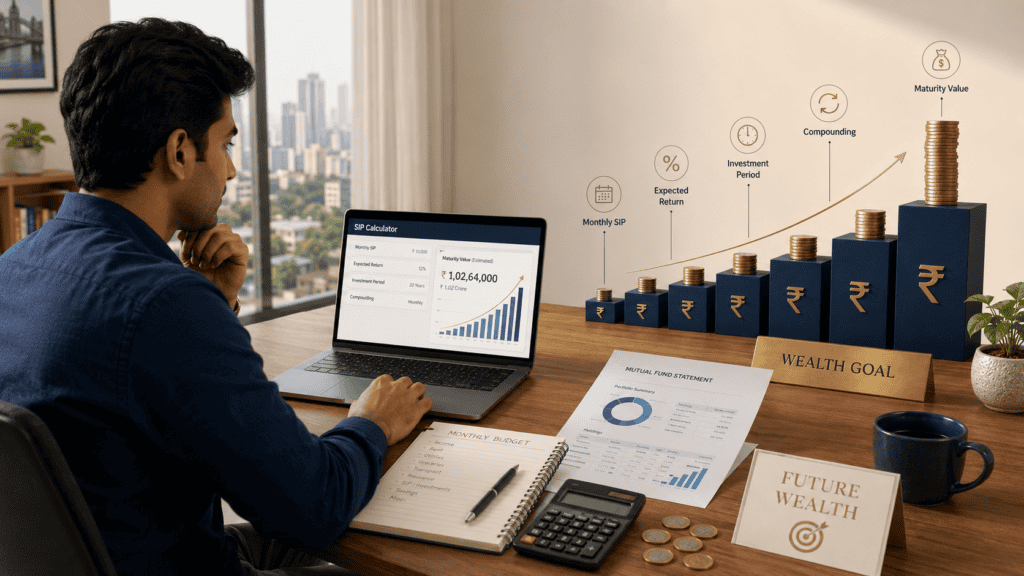

What a SIP Calculator India Actually Does — and What It Does Not

A SIP calculator India is a projection tool. It takes three inputs — monthly amount, tenure, and an assumed annual return — and runs them through a compound interest formula. The result is an estimated maturity value if the assumed return held constant every single month for the entire tenure. Markets do not work that way. Returns in any given year can swing between −40% and +60% for an equity fund. The calculator smooths all of that into one tidy number.

If you are completely new to this product category, read the guide to mutual fund basics first. Once you understand how a mutual fund is managed, pooled, and priced, the SIP mechanics will fall into place naturally.

How Rupee Cost Averaging Works in Practice

A SIP works by purchasing mutual fund units at the prevailing NAV on a fixed date every month. When the market falls, your ₹10,000 buys more units. When the market rises, your ₹10,000 buys fewer. Over time, this rupee cost averaging reduces the impact of short-term volatility on your average purchase price. It does not eliminate risk — but it removes the pressure of timing your entry. For a full breakdown of how monthly investing works — including how NAVs are calculated and how SIP dates affect unit allotment — the dedicated mechanics guide covers it in detail.

The Input That Matters Most: Your Return Assumption

Of the three calculator inputs, the return assumption is where most beginners go wrong. Using 15% or 18% as a base case produces impressive numbers — but almost no diversified equity fund has sustained those rates over 15–20 years after costs and market cycles. A more grounded planning assumption sits between 10% and 12% for equity SIPs, and 6%–8% for hybrid or debt-oriented SIPs.

The other input beginners underestimate is tenure. A ₹10,000 SIP at 12% for 10 years estimates approximately ₹23.2 lakh. Extend to 20 years and the same monthly amount estimates approximately ₹98.9 lakh. Extend to 25 years and it crosses ₹1.89 crore. The compounding effect becomes exponential only in the later years — which is why starting earlier matters more than starting with more.

The Cost the Calculator Ignores: Expense Ratio

Every mutual fund charges an annual expense ratio — a fee expressed as a percentage of your invested corpus. Regular plans typically carry 1%–2.5%; direct plans often sit at 0.5%–1%. A fund that delivers 12% gross may net you 10.5% after a 1.5% expense ratio. Over 15 years, that gap on a ₹10,000 SIP reduces an estimated ₹50.5 lakh corpus to approximately ₹43 lakh. The SIP calculator India never asks for this input. Always check the expense ratio of the fund you choose before committing.

Real Example: Rohit’s SIP Plan in Bengaluru

Rohit, 29, is a software engineer in Bengaluru earning ₹95,000 per month. He wants to start a SIP of ₹15,000 per month in a diversified equity mutual fund for 20 years, planning for financial independence at 49.

He opens a SIP calculator India and enters ₹15,000 monthly, 20 years, 12% assumed return. The result: Estimated corpus — ₹1,49,87,050 (approximately ₹1.50 crore). Total invested: ₹15,000 × 240 months = ₹36,00,000. Estimated gains: ₹1,49,87,050 − ₹36,00,000 = ₹1,13,87,050.

Rohit also runs the same figures at 10% to set a conservative floor. The estimated corpus drops to approximately ₹1,13,00,000 — still above ₹1 crore. He decides to plan around ₹1 crore as his target and treat the 12% scenario as upside, not a base case.

The insight from Rohit’s calculation: even if equity markets deliver only 10% annualised over 20 years, his estimated corpus still exceeds ₹1 crore from just ₹36 lakh invested. That is the argument for staying invested through down cycles rather than pausing SIPs when markets fall.

Comparison: SIP vs Lumpsum Investment

Before deciding how to deploy your savings, it helps to understand how monthly investing stacks up against a one-time investment. The full SIP and lumpsum choice guide covers the detailed decision framework — here is the core comparison across key parameters.

| Parameter | SIP (Monthly) | Lumpsum (One-Time) |

|---|---|---|

| Capital needed upfront | Low — ₹100–₹1,000/month minimum | High — full amount at once |

| Market timing risk | Low — rupee cost averaging applies | High — returns depend on entry point |

| Compounding benefit | Strong over long tenures; builds gradually | Strongest if invested early in a rising market |

| Suitable for | Salaried investors, beginners, regular savers | Investors with a bonus, inheritance, or windfall |

| ELSS tax benefit | Per-instalment 3-year lock-in; staggered release | Entire amount locked for 3 years from investment date |

| Behavioural discipline | Auto-debit builds habit automatically | Requires discipline to stay fully invested |

How to Decide What’s Right for You

These if/then decisions help you move from a calculator result to an actual plan. Connect your estimate to specific planning future money goals so the number has a purpose rather than sitting as an abstract figure.

You are salaried with a steady income and can commit a fixed amount monthly — THEN SIP is your most practical starting point. Begin at ₹1,000–₹5,000 and increase by ₹500–₹1,000 each year as your income grows.

Your SIP calculator estimate falls short of your goal even at 12% — THEN increase the monthly SIP amount now rather than assuming higher future returns will make up the gap. Returns cannot be controlled; contribution amounts can.

You want an 80C deduction and can stay invested for 3 years per instalment under the old tax regime — THEN an ELSS fund SIP combines tax saving and equity growth in one product with the shortest lock-in of all 80C options.

Your goal is within 3 years — a car down payment, a wedding, a vacation fund — THEN equity SIPs are not suitable. Debt mutual funds or bank recurring deposits carry far less short-term volatility for near-term goals.

You receive an annual bonus — THEN consider making a lumpsum addition to your existing SIP folio in the same fund. This top-up can significantly improve the estimated corpus without changing your monthly budget.

You do not yet have a 3–6 month emergency fund — THEN do not start a long-tenure equity SIP until that buffer exists. Stopping a SIP mid-way during a financial emergency forces redemption — often at a market low — destroying the compounding benefit you built.

Common Mistakes to Avoid

Treating the Calculator Output as a Guaranteed Amount

The estimated corpus is a projection based on a fixed assumed return. Mutual fund investments are subject to market risks — actual returns fluctuate every year.

Treating ₹50 lakh as a locked-in outcome can lead to under-saving or premature spending in anticipation. A bear market in the final 2–3 years of a 15-year SIP can materially reduce the actual corpus below the calculator’s estimate.

Run your calculation at both 10% and 12% and plan your goal around the conservative figure.

Using an Unrealistically High Return Assumption

Entering 18% or 20% produces large, exciting numbers — but very few diversified equity funds have sustained those rates for 15–20 years after costs and market cycles.

The real cost: you commit to a smaller monthly SIP, assuming high returns will compensate. When they do not, your corpus lands materially short of your goal with no time to correct.

Use 10%–12% for equity and 6%–8% for debt or hybrid SIPs as your standard planning assumption.

Ignoring the Expense Ratio

The SIP calculator does not ask for the fund’s expense ratio — but every fund charges one. A 1.5% annual expense ratio on a ₹10,000 SIP over 15 years can reduce the effective corpus by ₹7–8 lakh compared to a direct plan at 0.5%.

Always compare the direct plan and regular plan expense ratios before selecting a fund.

Stopping SIPs During a Market Dip

A falling market feels alarming — but stopping your SIP when NAVs are low means you miss buying more units at lower prices, which is exactly when rupee cost averaging delivers the most benefit.

Set your SIP on auto-debit and treat the monthly deduction as a fixed expense, not a discretionary one.

Not Accounting for Inflation

₹50 lakh in 15 years does not buy what ₹50 lakh buys today. At 6% annual inflation, that corpus’s real purchasing power is approximately ₹20–22 lakh in today’s terms.

For retirement or large future goals, always calculate the inflation-adjusted target corpus — then use the SIP calculator to find the monthly amount needed to reach it.

Never Increasing the Monthly SIP Amount

Starting at ₹5,000/month and keeping it flat for 15 years means your investment rate as a share of your income shrinks as your salary grows.

A step-up SIP that increases by 10% each year can grow an estimated corpus by 60%–80% over 15 years compared to a flat SIP starting at the same amount.

When This May Not Be the Right Choice

An equity mutual fund SIP is not the right tool in every situation. If you carry high-interest debt — a personal loan above 14% or an outstanding credit card balance — the interest you are paying will likely exceed what your SIP can earn. Clear that debt first before directing surplus income into equity investments.

If your investment horizon is under 3 years, equity SIPs carry real risk of an absolute loss. Short-term goals are far better served by debt mutual funds, liquid funds, or bank recurring deposits.

If your income is irregular — seasonal freelance work, commission-heavy sales — a fixed monthly SIP commitment can create cash flow pressure in lean months. A flexible SIP or disciplined lumpsum approach on strong earning months may suit your income pattern better.

If you have not yet built a 3–6 month emergency fund, starting an equity SIP before that safety net exists exposes you to the risk of forced premature redemption during an unexpected financial shock — often at the worst possible time in the market.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Mutual fund regulations, tax treatment, and investment limits governing SIPs are maintained by these official bodies. Always verify current figures before acting on any number in this article:

- SEBI (Securities and Exchange Board of India) — sebi.gov.in — Regulates all mutual funds, mandates risk disclosures, and publishes fund categorisation and expense ratio norms.

- Income Tax Department — incometax.gov.in — Governs LTCG and STCG tax rates on mutual fund gains, Section 80C deduction limits for ELSS, and TDS applicability on redemptions.

For a complete guide to tax on fund gains — including exactly how LTCG and STCG apply to different fund types, holding periods, and redemption scenarios — refer to the dedicated taxation guide before planning any withdrawal.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Start a step-up SIP from day one: A ₹5,000 SIP increasing by 10% annually for 15 years at 12% estimates a corpus of approximately ₹75–80 lakh — versus ₹43 lakh for a flat ₹5,000 SIP over the same period. The step-up does most of the heavy lifting.

- Always run two return scenarios: Calculate at 10% and at 12%. Plan your goal around the 10% figure. If actual returns beat that, treat it as a bonus — not a right.

- Check the direct plan option before investing: Direct mutual fund plans eliminate distributor commissions, reducing expense ratios by 0.5%–1.5% annually. Over 15–20 years, that saving alone can add ₹5–10 lakh to the estimated corpus on a ₹10,000 SIP.

- Work backwards from your goal: If you need ₹1 crore in 15 years at 12%, the required monthly SIP is approximately ₹19,819. Start from the goal amount, not from what feels comfortable to invest.

- Name every SIP after a goal: A SIP labelled “daughter’s education — 2038” is psychologically much harder to cancel during market volatility than a generic SIP. Naming the purpose also prevents premature redemption for non-emergency spending.

- Do not run more than 3–4 equity SIPs simultaneously: More SIPs rarely mean more diversification if the underlying funds hold similar large-cap stocks. One broad index fund SIP plus one mid-cap SIP covers most diversification needs for a new investor — without the complexity of tracking eight different portfolios.

Frequently Asked Questions

Is the SIP calculator India result a guaranteed return?

No. The result is an estimate based on a fixed assumed return you enter. Mutual fund investments are subject to market risks, and actual returns vary year to year. Use the output as a planning guide — not as a commitment from the fund or the AMC.

What return rate should I use when running a SIP calculation?

For equity mutual funds, 10%–12% is a commonly used conservative-to-moderate range for long-term planning. Using 15% or 18% produces large numbers but rarely reflects 15–20 year real-world outcomes after fund costs, market corrections, and varying performance cycles.

What is the minimum SIP amount I can start with?

Most AMCs allow SIPs starting at ₹100 per month, though some funds set a minimum of ₹500 or ₹1,000. Consistency matters far more than the starting amount. A ₹1,000 SIP maintained for 20 years at 12% estimates a corpus of approximately ₹9.99 lakh from just ₹2.4 lakh invested.

Can I pause or stop a SIP after starting?

Yes. Open-ended mutual fund SIPs (other than ELSS) can be paused or stopped at any time without penalty. Units already purchased remain in your folio. However, stopping during a market dip means you miss buying more units at lower prices — precisely when rupee cost averaging is working hardest for you.

Is a SIP the same as a bank recurring deposit?

No. A recurring deposit (RD) gives a fixed, predetermined interest rate with capital protection. An equity mutual fund SIP carries market risk — returns are not fixed, capital is not guaranteed, and you may receive less than you invested if you redeem during a falling market. The potential for higher long-term returns comes with this variability.

Does the SIP calculator account for taxes on redemption?

No. Standard SIP calculators show a pre-tax estimated corpus. When you redeem equity mutual fund units held over 1 year, LTCG above ₹1,25,000 in a financial year is taxed. Units held under 1 year attract STCG. Both rates can change with each Budget — always verify current rates at incometax.gov.in before planning a large redemption.

What is an inflation-adjusted corpus and why does it matter?

An inflation-adjusted corpus is the estimated maturity value expressed in today’s purchasing power. If the calculator shows ₹50 lakh in 15 years and inflation runs at 6% annually, the real purchasing power of that amount is approximately ₹20–22 lakh in today’s terms. For retirement or large future goals, always target the inflation-adjusted number — not the nominal figure.

What happens if I miss a SIP instalment?

A missed instalment is typically skipped — most AMCs do not charge a penalty for occasional missed payments. However, repeated failures may trigger cancellation of the SIP mandate by your bank. The simplest fix is to maintain a dedicated savings account with a standing balance for SIP auto-debits, separate from your day-to-day spending account.

Can I use a SIP calculator to plan a specific goal like buying a house?

Yes — and it works best when you work backwards. If you need ₹30 lakh in 10 years, enter that as the target, select 10 years, and use a 10%–12% assumed return. The calculator will show the required monthly SIP (approximately ₹14,500–₹16,000 for this example). Equity SIPs work best for goals 7 or more years away — shorter timelines carry too much market-timing risk.

Is SIP only for equity mutual funds?

No. SIPs can be set up in debt mutual funds, hybrid funds, liquid funds, index funds, and ELSS funds. For goals under 5 years or for investors with low risk tolerance, a debt fund SIP at an assumed 6%–8% return is more appropriate than an equity fund SIP.

Final Verdict

A SIP calculator India is one of the most practical first steps for any new investor — it makes the abstract logic of compound growth concrete and actionable. The key is to use it honestly: run the numbers at 10% and 12%, plan for the conservative scenario, and treat any upside as a welcome surprise rather than an expectation. A ₹10,000 monthly SIP started at 29 and held for 20 years at a realistic 12% assumption estimates a corpus of approximately ₹98.9 lakh — from just ₹24 lakh invested. Mutual fund investments are subject to market risks. Past performance does not guarantee future returns. The calculator is a planning tool, not a promise.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Arjun Kapoor writes about mutual funds, SIPs, ELSS, fund categories, investment returns, and beginner investing concepts for Indian readers. His focus is on education, not product promotion or fund recommendations. He helps readers understand how mutual funds work before they start investing or comparing schemes.

He covers topics such as mutual fund meaning, SIP meaning, SIP calculator, direct mutual funds vs regular plans, NAV, ELSS tax-saving funds, CAGR, absolute returns, XIRR, expense ratio, large cap vs mid cap vs small cap funds, flexi cap funds, index funds vs active funds, liquid funds, debt mutual funds, SIP pause vs SIP stop, lumpsum vs SIP, and how to start SIP in India.

Arjun’s writing is simple, risk-aware, and long-term oriented. He avoids guaranteed-return language and explains investment concepts using examples, timelines, and comparison tables. His articles remind readers that mutual fund investments are subject to market risks, and past performance does not guarantee future returns. Readers should verify scheme details from SEBI, AMFI, fund houses, and official scheme documents.