Every year, HR teams across India quietly add an NPS option to the annual tax declaration portal. Most employees stare at it for a few seconds and click past it — because nobody ever explained what NPS actually means.

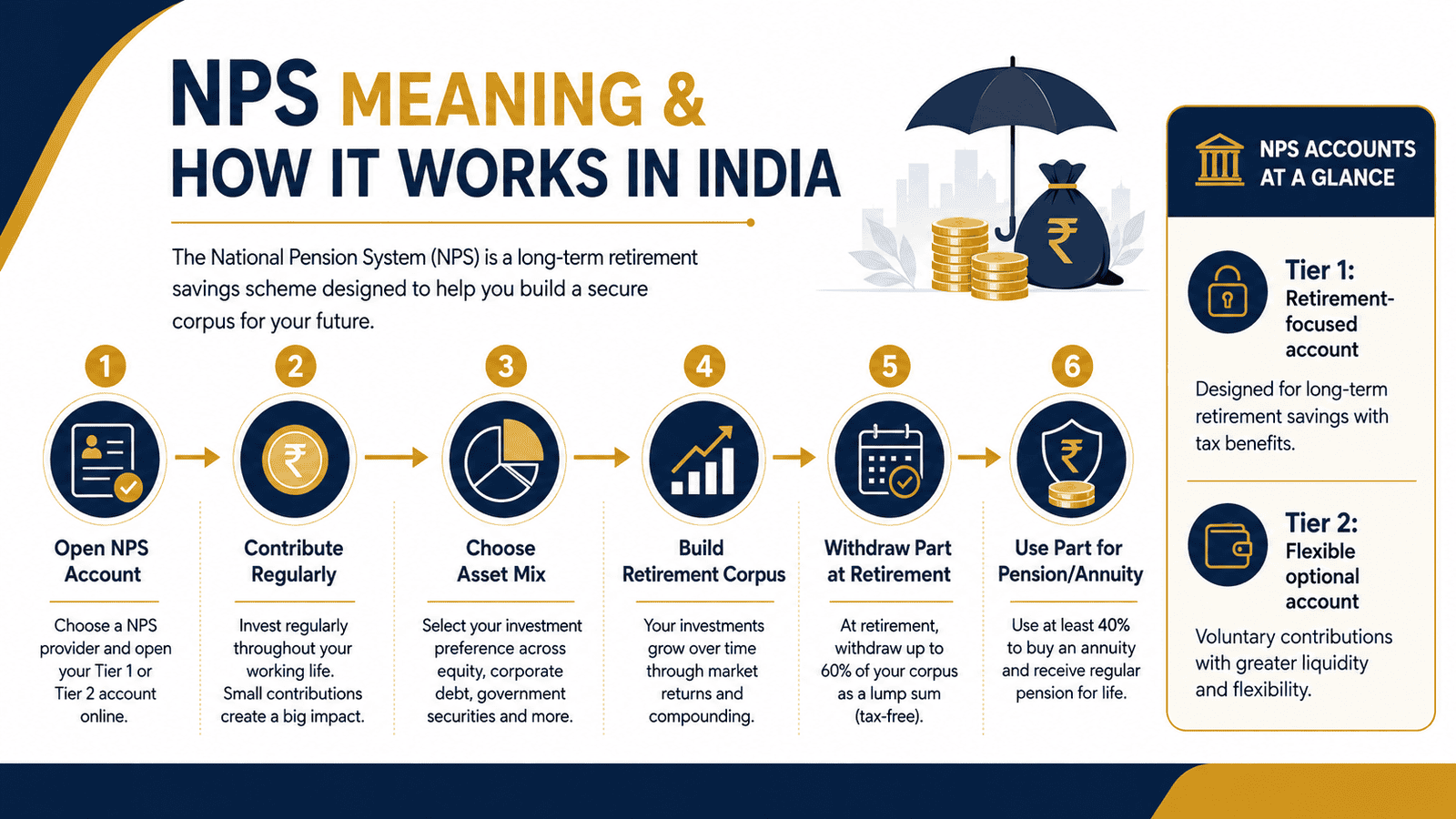

NPS meaning is not complicated. It stands for National Pension System, a government-regulated scheme built specifically for retirement savings. But the confusion is real: NPS is part retirement account, part market-linked investment, and part pension product — all in one structure.

This article explains NPS in plain language. What the scheme is, how Tier 1 and Tier 2 accounts work, what tax benefits are available, how and when you can withdraw, and whether it actually suits your financial situation. All rules and limits mentioned here must be verified from official sources before you take any action.

Quick Answer: NPS Meaning

NPS meaning refers to the National Pension System, a government-regulated retirement savings scheme where you contribute regularly, invest through approved pension funds, and build a retirement corpus. At retirement, part of the corpus may be withdrawn and part may be used for pension or annuity as per current PFRDA rules.

Key Takeaways

- NPS full form is National Pension System, regulated by the Pension Fund Regulatory and Development Authority (PFRDA) — not a bank, mutual fund house, or insurance company.

- It has two account types: Tier 1 is the primary retirement account with restricted withdrawal rules; Tier 2 is a voluntary savings account with fewer restrictions for most investors.

- Returns are market-linked — your NPS corpus grows or falls with equity and debt market performance, not at a government-fixed guaranteed rate.

- At exit, a portion of the corpus must be used to purchase an annuity for a regular pension; the rest may be taken as a lump sum — verify the current mandatory split at pfrda.org.in before investing.

- Section 80CCD(1B) may allow an additional tax deduction beyond the standard ₹1.5 lakh Section 80C ceiling — verify the current limit and applicable tax regime at incometax.gov.in.

- Tier 1 has a long lock-in period until approximately age 60 — it is not suitable as an emergency fund or for any financial goal shorter than two decades.

Key Facts at a Glance

| Parameter | Detail |

|---|---|

| Full Form | National Pension System |

| Regulator | Pension Fund Regulatory and Development Authority (PFRDA) |

| Primary Purpose | Building a retirement corpus and generating pension income at retirement |

| Account Types | Tier 1 (mandatory retirement account) and Tier 2 (optional savings) |

| Return Type | Market-linked — equity, corporate bonds, government securities |

| Unique Identifier | Permanent Retirement Account Number (PRAN) |

| Corpus at Exit | Partial lump sum allowed; balance used for annuity — verify current percentage at pfrda.org.in |

| Tax Sections | Section 80CCD(1), 80CCD(1B), 80CCD(2) — verify current limits at incometax.gov.in |

| Minimum Contribution | Verify current minimum at pfrda.org.in before account activation |

What NPS Meaning Tells You About How the Scheme Actually Works

Your PRAN — One Retirement Account for Life

When you open an NPS account, you receive a Permanent Retirement Account Number — PRAN. This 12-digit number is yours permanently. Whether you switch jobs, move cities, or change your pension fund manager, your PRAN stays the same. It is one of NPS’s most practical design features: a single account that follows you across employers and states without requiring transfer paperwork every time you change roles.

You can open a Tier 1 NPS account through your employer if they offer a corporate NPS facility, through a bank registered as a Point of Presence (PoP), or online via the eNPS portal at enps.nsdl.com. The process requires your Aadhaar, PAN, and a bank account for contributions and future withdrawals.

How Contributions Work

After account opening, you contribute money — monthly, quarterly, or as a lump sum — into your NPS account. There is a minimum annual contribution required to keep a Tier 1 account active; verify the current figure at pfrda.org.in before you begin.

If your employer offers NPS as a salary benefit, they may also contribute on your behalf. That employer NPS contribution is treated separately from your own contribution and may qualify for a tax deduction under Section 80CCD(2) — verify the applicable limit and rules at incometax.gov.in, as these differ depending on whether you work in the government or private sector.

Pension Fund Managers — Who Invests Your Money

Your NPS contributions are not managed by the government directly. PFRDA authorises a set of registered pension fund managers — professional investment managers who allocate your money across asset classes. Each manager offers their own performance track record across equity and debt categories.

You choose one pension fund manager at account opening. PFRDA allows you to switch managers periodically — verify the current switching rules and frequency at pfrda.org.in. Choosing a manager is not permanent, but it is worth comparing publicly available fund performance before your first decision.

Asset Classes and Investment Choice

NPS invests across four main asset classes: equity (E), corporate bonds (C), government securities (G), and alternative investment funds (A). Each carries a different risk and return profile. You manage your allocation in one of two ways.

- Active Choice: You set the percentage split across asset classes yourself. This suits someone who understands market risk and wants direct control over their retirement portfolio allocation.

- Auto Choice: Your equity allocation reduces automatically as you approach retirement. PFRDA offers multiple lifecycle fund options under Auto Choice — conservative, moderate, and aggressive — each reducing equity at a different pace as you age.

Neither approach guarantees a return. Equity can fall in bad market years and recover over time. This market-linked nature is the central difference between NPS and fixed-return products like PPF or bank fixed deposits.

Tier 1 — The Retirement Account

Tier 1 is the core NPS account — and the one most people mean when they hear “NPS account.” It is built as a long-term retirement savings vehicle with restricted withdrawal rules. Partial withdrawals before the standard exit age are permitted only in specific conditions after a defined lock-in period; verify exact partial withdrawal conditions and applicable purposes at pfrda.org.in.

At exit — on or after the standard retirement age — you can take a portion of the corpus as a lump sum and must use the remaining balance to purchase an annuity from a registered annuity service provider. The annuity generates a monthly pension for life. The exact lump sum versus annuity split is governed by current PFRDA regulations and must be verified before you plan your retirement income.

For a complete side-by-side breakdown of Tier 1 rules, tax treatment, and exit conditions, read our detailed guide on Tier account differences.

Tier 2 — The Optional Savings Account

Tier 2 is a voluntary account that you can open alongside Tier 1. It allows more frequent deposits and withdrawals than Tier 1 and does not carry the same long lock-in restriction for most subscribers.

However, Tier 2 does not automatically provide the same tax deductions as Tier 1. For government employees, specific rules may apply — verify the current tax treatment of your Tier 2 contributions at incometax.gov.in before contributing for tax purposes. For most private-sector investors, Tier 2 functions more as a flexible investment account than a retirement savings vehicle.

Real Example: Rohan’s NPS Decision in Pune

Rohan, 31, is a software professional in Pune earning ₹95,000 per month. When his HR portal added an NPS option last October, he had two questions: “Is this actually a retirement plan or just another tax trick?” and “What happens if I need the money before 60?”

Rohan decides to contribute ₹5,000 per month to NPS Tier 1. Over 29 years until age 60, his contributions alone total ₹17.4 lakh in principal. The actual corpus at retirement will be higher or lower depending on how equity and debt markets perform year after year — not a figure anyone can guarantee today.

At exit, a portion of whatever corpus Rohan has built can be taken as a lump sum. The remaining mandatory portion must be used to buy an annuity from a registered provider — giving him a monthly pension whose size depends on annuity market rates at the time he retires.

The key insight for Rohan: NPS Tier 1 is not a savings account he can access before 60. It is a 29-year retirement commitment. Use our retirement corpus estimate tool to model how different contribution levels and return assumptions change his projected outcome before he decides his monthly amount.

How to Calculate Your NPS Retirement Corpus

Estimated NPS Corpus = Monthly Contribution × Future Value Annuity Factor (derived from assumed annual return rate and number of years)

Using Rohan’s ₹5,000 monthly contribution and a 25-year horizon, here is how the estimated corpus changes across three different assumed annual return scenarios. These figures are illustrative — they use standard future value of annuity mathematics and are not projections or guarantees.

| Scenario | Assumed Annual Return | Estimated Corpus (25 Years) |

|---|---|---|

| Conservative | 8% per annum | Approximately ₹48 lakh |

| Moderate | 10% per annum | Approximately ₹66 lakh |

| Aggressive | 12% per annum | Approximately ₹94 lakh |

At exit, a mandatory portion of this corpus must be used to purchase an annuity. The monthly pension that annuity generates depends on annuity rates at the time of retirement — rates that are market-driven and cannot be locked in today. Plan for a range of outcomes, not just the moderate-return scenario.

Use the NPS corpus calculator alongside these numbers to test your own contribution level and time horizon before deciding how much to allocate each month.

Comparison: NPS vs PPF and NPS vs EPF

For most salaried employees, NPS sits alongside PPF and EPF as a retirement tool. Understanding how they compare helps you decide whether NPS deserves a separate allocation in your retirement plan. For a full three-way analysis, read our guide: PPF and EPF comparison.

NPS vs PPF

| Parameter | NPS Tier 1 | PPF |

|---|---|---|

| Return Type | Market-linked — equity and debt mix | Government-fixed rate — verify current rate from official notifications |

| Lock-in | Until approximately age 60; limited partial exit in specific conditions | 15-year maturity; partial withdrawal permitted from year 7 |

| Pension or Annuity at Exit | Yes — annuity purchase required on exit | No — full lump sum on maturity |

| Equity Exposure | Yes — up to allowed limit per asset class | No — debt instruments only |

| Tax Deduction | 80CCD sections — possible additional benefit beyond ₹1.5L limit | Within ₹1.5L Section 80C ceiling |

| Best For | Long-term growth with built-in retirement income | Conservative savers wanting government-backed certainty |

NPS vs EPF

| Parameter | NPS Tier 1 | EPF |

|---|---|---|

| Who Contributes | Employee (and optionally employer) | Employee and employer — mandatory for eligible salaried employees |

| Return Type | Market-linked — equity and debt | Government-fixed rate — verify current rate at epfindia.gov.in |

| Pension Component | Yes — annuity converts corpus to monthly pension | No — lump sum on exit; EPS is a separate, smaller pension scheme |

| Voluntary or Mandatory | Voluntary — you must actively choose to open it | Mandatory for most salaried employees above income threshold (verify at epfindia.gov.in) |

| Account Portability | PRAN stays unchanged across all employers and locations | UAN stays; EPF balance must be transferred on job change |

| Tax on Lump Sum at Exit | Verify current tax treatment at incometax.gov.in | Tax-free after 5 continuous years of service — verify at incometax.gov.in |

How to Decide What’s Right for You

retirement is your primary financial goal and you can leave this money untouched for 20 or more years — THEN NPS Tier 1 may be a useful addition to your retirement portfolio alongside mandatory EPF contributions.

you want fixed, government-backed returns with no market risk and no annuity requirement at exit — THEN understanding public provident fund basics may help you identify a better fit before committing to a market-linked product.

you are a salaried employee trying to understand whether NPS complements or overlaps your existing PF deductions — THEN reading about employee provident fund rules will give you the structural comparison you need before adding NPS to your salary declaration.

you are in a higher tax bracket and have already exhausted the ₹1.5 lakh Section 80C ceiling — THEN the additional deduction potentially available under Section 80CCD(1B) may make NPS worth considering, subject to current verified limits and your applicable tax regime.

your emergency fund is not yet fully built to cover 3–6 months of expenses — THEN NPS Tier 1 is not the right destination for your surplus right now, because that money cannot be accessed if a financial emergency arises.

comfortable with the possibility that your retirement corpus could be meaningfully lower than your estimates due to poor market years — THEN NPS may not be the right primary retirement vehicle, and a fixed-return product may suit your risk tolerance better.

Common Mistakes to Avoid

Treating NPS Like a Fixed-Return Product

NPS is not a fixed deposit or a PPF. Returns depend entirely on equity and debt market performance across your investment years.

Many first-time investors assume they will receive a predictable monthly pension at a fixed amount. They will not. Both the final corpus and the pension generated from the annuity can vary based on market conditions and annuity rates at the time of retirement.

Set realistic expectations before you begin contributing — use conservative return assumptions in any calculation.

Ignoring the Tier 1 Lock-in

Tier 1 contributions cannot be freely withdrawn before the standard exit age. Partial withdrawals are only permitted in specific circumstances after a minimum lock-in period — verify exact rules at pfrda.org.in.

Putting money you may need in the next 5–10 years into NPS Tier 1 is a planning error. Keep emergency savings and near-term goals funded through liquid instruments, not retirement accounts.

Confusing Tier 1 and Tier 2

Tier 2 offers more accessible withdrawals, but it does not carry the same tax benefits as Tier 1 for most private-sector investors. Assuming both accounts work the same way leads to incorrect tax claims and wrong liquidity expectations.

Understand the difference before contributing to either account — or before declaring NPS contributions in your tax filing.

Investing Only for the Tax Benefit

NPS Tier 1 locks your money away for decades. Choosing it only to reduce your tax outgo for the current financial year — without a genuine retirement plan behind the decision — often leaves investors frustrated when they want access to that money years later and cannot get it.

Use NPS when the retirement goal and the tax benefit align. Not when only one does.

Forgetting the Annuity Requirement at Exit

A mandatory portion of your NPS corpus must be used to buy an annuity from a registered annuity provider when you exit. You cannot take the full corpus as a lump sum. The exact percentage must be verified at pfrda.org.in.

Annuity rates at retirement depend on market conditions at that time — not on any rate available today. Plan for a range of monthly pension outcomes rather than a single number.

Not Reviewing Asset Allocation as You Get Older

In Active Choice, your equity allocation stays constant unless you manually adjust it. Remaining at high equity allocation as you near retirement increases the risk of a large corpus drop in the final years — exactly when you can least afford it.

Review your NPS asset allocation every three to five years and reduce equity exposure progressively as retirement approaches, or use Auto Choice so the rebalancing happens automatically.

When This May Not Be the Right Choice

NPS Tier 1 is not the right savings vehicle if your goal has a timeline shorter than 15–20 years. The lock-in structure is designed for retirement, not for mid-term financial goals like a home renovation, a child’s education in 8 years, or an emergency reserve.

If you need predictable, fixed returns without any dependence on market performance, NPS will not meet that expectation. Unlike PPF or bank FDs, the corpus is not guaranteed — it can be lower than expected in adverse market conditions.

If you are within 5 years of retirement and have not started NPS yet, a short contribution period limits the compounding benefit and may make the annuity component less meaningful relative to alternatives.

If you have not yet secured adequate life insurance and health insurance, those gaps deserve priority over NPS contributions — retirement savings built without protection underneath can unravel quickly.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

NPS account rules — including contribution minimums, partial withdrawal conditions, exit age, annuity requirements, and pension fund manager options — are governed by PFRDA. Always verify current rules directly at pfrda.org.in before opening an account or making any contribution decision.

Tax benefits under Section 80CCD — including the additional deduction potentially available beyond the standard Section 80C ceiling and the treatment of employer contributions — are governed by the Income Tax Act. Verify current limits and applicable tax regime rules at incometax.gov.in. You can use our income tax calculator to model how NPS deductions interact with your total tax liability under both old and new regimes before committing to a contribution amount.

Employer-linked retirement options including EPF are governed by EPFO at epfindia.gov.in.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Treat NPS Tier 1 as capital that does not exist until retirement. The moment you mentally earmark it for any purpose before age 60, the lock-in will become a source of frustration. Set it up, automate the contribution, and leave it alone for decades.

- Verify your tax regime before maximising NPS for tax reasons. The additional deduction under Section 80CCD(1B) may not apply under the new tax regime — confirm the current position at incometax.gov.in before increasing your monthly contribution purely for tax saving.

- Do not choose a pension fund manager at random. PFRDA-registered managers publish publicly available performance data across equity, corporate bond, and government securities categories. Spend 20 minutes comparing 5-year returns before selecting one.

- Review your asset allocation every 3–5 years. What made sense at 31 years old will not make sense at 52. Shift progressively from equity toward lower-risk asset classes as you approach your exit age — rather than making a sudden, large move close to retirement.

- Use conservative return assumptions when planning. Run your retirement corpus estimate at 8% as well as 10% or 12%. Markets do not consistently deliver the best-case scenario, and planning on the moderate number avoids a retirement shortfall surprise.

- Understand annuity rates before committing large sums to NPS. A significant portion of your corpus converts to an annuity at retirement. Annuity rates vary by provider and change with market conditions. Research what current annuity payout rates look like so the math at exit does not come as a surprise.

Frequently Asked Questions

What is NPS full form?

NPS full form is National Pension System. It is a government-regulated retirement savings scheme supervised by the Pension Fund Regulatory and Development Authority (PFRDA), a statutory authority under the Ministry of Finance.

Is NPS a government scheme?

Yes. NPS is a government-established retirement savings scheme. It was originally launched for central government employees and later extended to all Indian citizens. PFRDA, a statutory regulator, oversees all NPS operations, fund managers, and exit rules.

Does NPS give a guaranteed pension?

No. NPS does not guarantee a fixed pension amount. Your retirement corpus depends on your contributions, how equity and debt markets perform over your investment years, and your time horizon — all of which can vary significantly. The monthly pension generated from the annuity portion also depends on annuity rates at the time of retirement, which are market-driven and cannot be locked in today.

What is an NPS Tier 1 account?

Tier 1 is the primary NPS retirement account. It carries restricted withdrawal rules — you generally cannot access this money freely before the standard exit age. At retirement, a portion must be used for an annuity purchase. Tier 1 is designed exclusively for long-term retirement savings and is not suitable for short-term or emergency use.

What is an NPS Tier 2 account?

Tier 2 is a voluntary savings account available to those who already hold an active Tier 1 NPS account. It offers more flexible withdrawal rules for most private-sector investors. However, the tax treatment of Tier 2 contributions differs from Tier 1 and must be verified at incometax.gov.in before contributing for tax purposes.

Is NPS better than PPF?

It depends on what you are optimising for. NPS offers market-linked growth potential and a built-in pension income component at retirement. PPF offers government-fixed, guaranteed returns with no equity risk. NPS may suit an investor focused on long-term corpus growth with retirement income. PPF may suit a conservative saver who prioritises predictability over growth potential. Neither is universally better — your risk tolerance and timeline determine the right fit.

Can I withdraw money from NPS Tier 1 before retirement?

Partial withdrawal from NPS Tier 1 is permitted only under specific conditions — such as higher education, medical emergencies, home purchase, or certain other defined purposes — after a minimum lock-in period. The exact conditions, eligible purposes, and withdrawal limits must be verified directly at pfrda.org.in. NPS Tier 1 is not designed to function as a liquid or accessible savings account.

What is PRAN in NPS?

PRAN stands for Permanent Retirement Account Number. It is a unique 12-digit number assigned to every NPS subscriber at account opening. It remains unchanged across employer changes, location changes, and pension fund manager switches throughout your working career.

Is NPS useful for salaried employees?

NPS can be useful for salaried employees who want to build retirement savings beyond their mandatory EPF, particularly those in higher tax brackets who wish to use the additional deduction available under Section 80CCD(1B). However, NPS is voluntary — meaning you must actively choose it, understand the lock-in, and verify current tax benefits at incometax.gov.in before starting contributions.

What tax deductions are available under NPS?

NPS offers deductions under Section 80CCD(1) on your own contributions, Section 80CCD(1B) for an additional amount potentially above the ₹1.5 lakh Section 80C ceiling, and Section 80CCD(2) on employer NPS contributions. The exact deduction limits, caps, and which deductions apply under the old versus new tax regime must be verified at incometax.gov.in — these rules can change with each Budget.

Final Verdict

NPS meaning goes well beyond a tax-saving tool. It is a structured, government-regulated retirement savings scheme that builds a corpus over decades and converts part of it into a regular pension at retirement — through annuity purchase.

For a salaried professional with a long working horizon, NPS may be a useful complement to mandatory EPF contributions — particularly if you want equity-linked growth and an additional tax deduction beyond the Section 80C ceiling. It is not a savings account, a fixed deposit substitute, or an emergency fund. Tier 1 money is retirement money.

Before activating NPS through your HR portal or opening an account online, verify current contribution rules, exit rules, tax deduction limits, and annuity requirements directly at pfrda.org.in and incometax.gov.in.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Suresh Nair writes about Indian government savings schemes, post office schemes, and conservative long-term savings options. His content is especially useful for families, parents, senior citizens, and low-risk savers who want to understand scheme rules before depositing money.

He covers topics such as Public Provident Fund, Sukanya Samriddhi Yojana, Senior Citizens’ Savings Scheme, National Savings Certificate, Kisan Vikas Patra, Post Office Monthly Income Scheme, National Pension System, post office fixed deposits, post office recurring deposits, child savings schemes, senior citizen savings options, maturity rules, withdrawal rules, lock-in periods, and tax treatment.

Suresh’s writing is mature, rule-focused, and cautious. He explains eligibility, deposit limits, tenure, interest calculation, tax benefits, withdrawal conditions, and practical use cases in simple language. His articles are useful for readers who prefer safety and predictable rules over high-risk investments. Since government scheme interest rates, deposit limits, lock-in rules, and tax treatment may change through official notifications, readers should verify current details from India Post, PFRDA, Income Tax Department, or relevant government sources before investing.