You started your SIP at ₹5,000 or ₹10,000 a few years ago. Your salary has gone up since then — but your SIP amount has not moved. That gap is exactly what a step-up SIP calculator is built to show you. Instead of modelling a flat monthly investment forever, it lets you estimate what happens when you raise your SIP every year alongside your income — the way most salaried investors actually plan to invest.

This article explains how the step-up SIP calculator works, what inputs it needs, how to read its output honestly, and what the numbers genuinely cannot tell you. Mutual fund investments are subject to market risks, and every figure this calculator produces is an estimate, not a guarantee.

Quick Answer: Step Up SIP Calculator

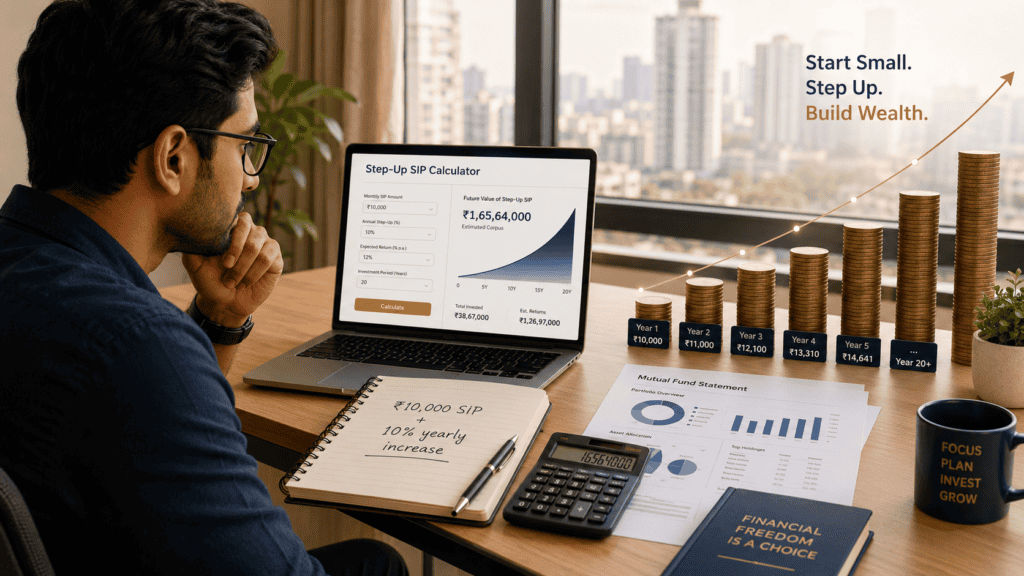

A step up SIP calculator estimates how your corpus may grow when you raise your SIP every year. For example, ₹10,000 monthly SIP with a 10% yearly step-up over 15 years can show a much larger estimated corpus than a fixed SIP, depending on assumed return and market performance.

How to Calculate Step-Up SIP Returns

The step-up SIP calculator works on four inputs and produces three outputs. The core formula works year by year:

Monthly SIP in Year N = Starting Monthly SIP × (1 + Annual Step-Up %)^(N − 1)

The calculator applies this to every month across your full tenure and compounds each instalment forward at your assumed annual return. Here are the four inputs:

| Input | Example Value | What It Means |

|---|---|---|

| Starting monthly SIP | ₹10,000 | Your SIP amount in Year 1 |

| Annual step-up percentage | 10% | How much you raise the SIP each year |

| Expected annual return | 12% | Assumed return rate — not guaranteed |

| Investment tenure | 15 years | Total years of investing |

The three outputs are: total amount invested, estimated wealth gain, and estimated maturity corpus. Here is how your monthly commitment grows with a 10% annual step-up starting at ₹10,000:

| Year | Monthly SIP (₹) | Annual Contribution (₹) |

|---|---|---|

| Year 1 | 10,000 | 1,20,000 |

| Year 3 | 12,100 | 1,45,200 |

| Year 5 | 14,641 | 1,75,692 |

| Year 10 | 23,579 | 2,82,948 |

| Year 15 | 37,975 | 4,55,700 |

At a 12% assumed annual return, this step-up approach results in approximately ₹38,12,000 in total invested capital over 15 years, with an estimated maturity corpus of approximately ₹1,02,00,000. A fixed ₹10,000 SIP over the same period at the same assumed return would invest ₹18,00,000 and produce an estimated corpus of approximately ₹50,46,000. These are illustrative estimates only — actual results depend entirely on market performance. Try our step-up SIP calculator to model your own inputs, and compare with a plain monthly investment projection using the monthly SIP estimate tool before deciding.

Past performance does not guarantee future returns. The 12% figure above is used only for illustration.

Key Takeaways

- A step-up SIP raises your monthly investment by a fixed percentage each year — for example, ₹10,000 in Year 1 becomes ₹11,000 in Year 2 at a 10% step-up.

- At a 10% annual step-up over 15 years starting at ₹10,000, your total invested capital reaches approximately ₹38,12,000 — more than double the ₹18,00,000 in a fixed SIP scenario.

- Calculator results depend entirely on the return assumption you enter. Switching from 12% to 10% to 8% produces very different estimated corpus figures — always model multiple scenarios.

- A higher step-up percentage is not automatically better. Choosing an amount that strains future cash flow often leads to SIP cancellations, which defeats the entire purpose of long-term investing.

- The step-up SIP calculator is a planning and comparison tool, not a return predictor. Mutual fund investments are subject to market risks and past performance does not guarantee future returns.

Key Facts at a Glance

| Parameter | Detail | Notes |

|---|---|---|

| What is a step-up SIP | SIP where monthly investment increases annually | Also called top-up SIP or annual SIP escalation |

| Required calculator inputs | Starting SIP, step-up %, assumed return %, tenure | Return assumption is entered by user — not guaranteed |

| Calculator outputs | Total invested, estimated gains, maturity value | All figures are illustrative estimates |

| Best suited for | Salaried investors with predictable income growth | Align step-up with annual salary increment |

| Main risks | Market-linked returns and over-commitment | Mutual funds regulated by SEBI — sebi.gov.in |

How a Step-Up SIP Works — and What the Calculator Is Actually Estimating

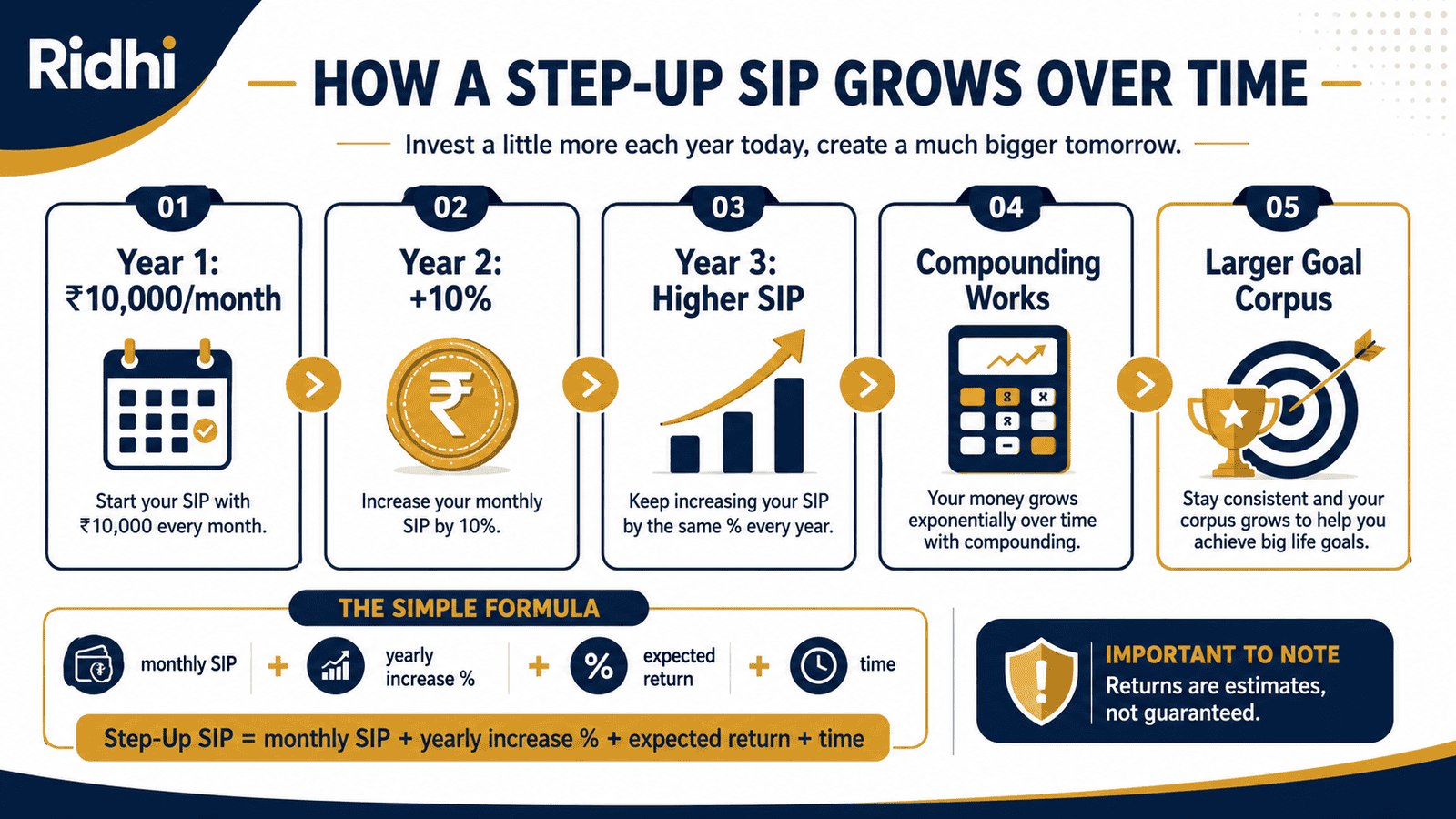

A normal SIP keeps your monthly investment constant for the full tenure. You invest ₹10,000 every month in Year 1 and in Year 15. A step-up SIP — sometimes called a SIP top-up or annual SIP escalation — increases that amount by a fixed percentage at the start of each new investment year. You set this instruction once with your fund house or platform, and the monthly debit from your bank account rises automatically each year by the percentage you chose.

The Return Assumption Is Your Input, Not a Forecast

This is the most important thing to understand about any step-up SIP calculator. The expected annual return field is not a projection from a fund house, from SEBI, or from historical performance. It is simply a number you enter. The calculator applies that number uniformly across every month of your tenure — which is not how markets actually behave. Equity markets deliver uneven returns year by year, with some years sharply negative.

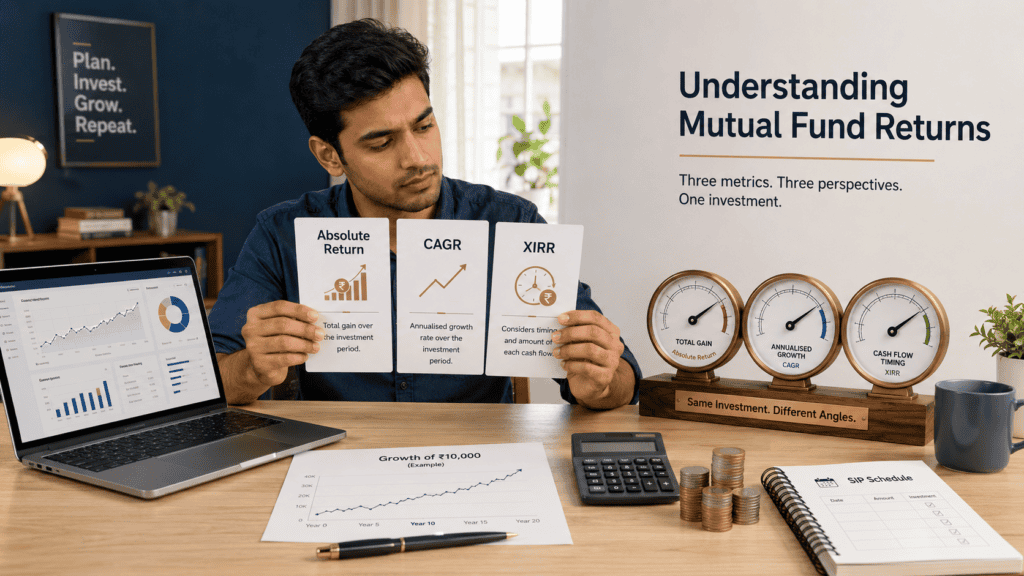

Before relying on a single return assumption, understand how mutual fund returns are actually measured. Our guide on returns measurement methods explains the difference between CAGR, absolute return, and XIRR — all of which you will encounter when evaluating fund performance.

If you are new to systematic investing altogether, read our explainer on SIP basics explained before modelling step-up scenarios.

Why Step-Up Investing Is Linked to Income Growth

The logic behind a step-up SIP is straightforward. Most salaried employees in India receive annual salary increments. A software engineer earning ₹1.6 lakh per month today may earn ₹1.75 lakh next year. If their SIP stays fixed at ₹10,000, the share of income going toward long-term investing actually shrinks over time.

A step-up SIP corrects for this drift. It keeps investment amounts roughly proportional to income — the principle behind salary hike linked investing. The step-up is not about chasing a higher corpus number; it is about ensuring that higher income translates into meaningfully higher investing, not just higher spending.

Using the Calculator for Goal-Based SIP Planning

For goal-based SIP planning — say, building a ₹1 crore corpus for a child’s education in 18 years — the step-up SIP calculator lets you work backwards. You can test whether a manageable starting SIP with consistent annual escalation reaches your target, rather than locking into a large fixed SIP from Day 1. This makes it a genuinely useful planning tool, as long as the return assumptions you use are realistic and documented.

According to SEBI’s investor education guidelines, investors should assess the risk profile of any scheme before investing. The risk-o-meter disclosed in every Scheme Information Document reflects the risk level of that specific fund — not the calculator’s assumed return.

Real Example: Rohan’s Salary-Linked Step-Up in Bengaluru

Rohan, 31, is a software engineer in Bengaluru earning ₹1.6 lakh per month. He has been investing ₹10,000 per month in a diversified equity mutual fund through SIP. Every April, after his salary increment arrives, he increases his SIP by 10%.

In Year 1, Rohan invests ₹10,000/month — totalling ₹1,20,000 for the year. After his first increment, Year 2 becomes ₹11,000/month. By Year 5, his monthly SIP is ₹14,641 — roughly 8.4% of his expected salary at that point, assuming modest income growth. By Year 10, his monthly commitment has grown to ₹23,579.

Two forces are working together here: Rohan’s total invested capital is growing much faster than in a fixed SIP scenario, and each rupee invested in Year 1 has had the most time to compound. The power of compounding amplifies early contributions the most — which is why starting with even a modest SIP and increasing it consistently tends to outperform waiting to start at a higher amount.

Key insight: Rohan’s step-up decisions are always tied to a confirmed increment — not to what the calculator shows as an ideal. If a promotion is delayed, the step-up simply waits until cash flow is certain.

Comparison: Fixed SIP vs Step-Up SIP

| Parameter | Fixed SIP | Step-Up SIP |

|---|---|---|

| Contribution pattern | Same amount every month throughout tenure | Increases by fixed % at start of each year |

| Total invested (₹10K start, 15 yrs) | ~₹18,00,000 | ~₹38,12,000 (at 10% annual step-up) |

| Estimated corpus (12% assumed return) | ~₹50,46,000 | ~₹1,02,00,000 |

| Best suited for | Fixed or unpredictable income | Rising income with predictable increments |

| Affordability risk | Low — debit never changes | Medium — future debits increase each year |

| Flexibility | Easy to pause or cancel | Step-up instruction can be paused separately |

| Market risk | Market-linked | Market-linked |

The corpus estimates above assume a 12% annual return applied uniformly throughout 15 years. This is an illustrative assumption — not a projected or guaranteed outcome. Both options carry equity market risk. A step-up SIP is not automatically superior; it performs better than a fixed SIP only when it is sustained for the full tenure.

How to Decide What’s Right for You

Your salary grows by 8–12% annually and your job is stable — a 10% annual step-up is a practical starting point. It tracks income growth without requiring a significant stretch in your monthly budget.

You are early in your career and unsure about income consistency — start with a fixed SIP and move to a 5% step-up only after two consecutive annual increments have confirmed a clear earnings trend.

Your income arrives in irregular lumps — bonuses, project billing, freelance payments — consider making lump sum additions to existing funds after each bonus rather than setting an automatic step-up that triggers a recurring higher debit.

Your goal deadline is under 7 years and you are investing in equity mutual funds — use conservative return assumptions of 8–10% in the calculator, not historical peaks. Shorter horizons leave less time to recover from a market downturn before you need the funds.

You want to compare how much difference a 5%, 10%, or 15% step-up actually makes — run the calculator for all three and look at what the monthly SIP amount becomes in Year 10 and Year 15, not just the final corpus. Affordability in the later years matters as much as the headline number.

You have high-interest debt, no emergency fund, or irregular income — a step-up SIP is not the right next step. Prioritise clearing high-cost debt and building 3–6 months of liquid emergency savings before scaling up any market-linked investment commitment.

Common Mistakes to Avoid

1. Entering an Unrealistically High Return Assumption

Setting 15% or 18% as the expected return produces a dramatically large corpus estimate in the calculator.

Equity mutual funds in India have delivered varying long-term returns across categories — some categories averaging 10–13% CAGR over long periods, others considerably less. No fund guarantees future performance. An inflated input creates an estimated outcome that may never materialise, leading to under-preparation for actual financial goals.

Use 10–12% as a working assumption for diversified equity funds and always run an 8% conservative scenario alongside it.

2. Choosing a Step-Up Percentage That Strains Future Cash Flow

A 20% step-up starting at ₹10,000 means your monthly SIP reaches approximately ₹61,917 by Year 10.

If that amount becomes unaffordable — due to EMIs, family expenses, or a slower increment year — you will pause or cancel the SIP. A cancelled SIP in Year 7 of a 15-year plan delivers worse outcomes than a lower fixed SIP run consistently. The cost is not just missing returns; it is disrupting the compounding sequence entirely.

Always model what your required SIP will be in Year 10 before committing to a step-up percentage.

3. Ignoring Fund Costs and the Expense Ratio

The calculator shows a gross estimated corpus. It does not deduct annual fund management costs.

Understanding the fund cost impact matters over long tenures — a 1% annual expense ratio difference on a large corpus compounds into a meaningful reduction in net returns over 15 years. Direct plans carry lower expense ratios than regular plans and are worth comparing specifically for long-tenure SIPs.

Always check the expense ratio of the specific scheme in its Scheme Information Document before investing.

4. Increasing SIP Without an Emergency Fund

Scaling up a SIP aggressively without a liquid emergency fund means a medical bill or job disruption could force you to redeem units during a market downturn — at the worst possible time.

Build and maintain 3–6 months of expenses in a liquid instrument before committing to increasing equity SIP amounts. Step-up increases should come from genuine surplus, not from stretching the budget.

5. Stopping SIPs During Market Falls

The calculator’s estimated returns assume consistent investing throughout the full tenure. Stopping a SIP after a 20–30% market fall breaks the investment sequence and causes you to miss the recovery period — historically when equity markets have delivered significant gains.

Review your goals and tenure before making any SIP change during a downturn. Market movements are not a valid reason to interrupt a long-term plan.

6. Treating Calculator Output as a Guaranteed Outcome

As SEBI regulations require all mutual fund houses to disclose: past performance is not indicative of future results, and investments in mutual funds are subject to market risks. A calculator output is a projection built on your assumed inputs — it is not a promise from any fund house, regulator, or platform.

Use the step-up SIP calculator to compare scenarios and test affordability — not to decide a retirement income at a precise rupee figure.

When This May Not Be the Right Choice

A step-up SIP may not suit you if your income is irregular or project-based. Freelancers, consultants, and commission-driven earners often see wide month-to-month variation — automated annual escalation increases financial risk when the income floor is unpredictable.

If you have outstanding high-interest loans — personal loans above 14–18% annual interest or credit card revolving debt — directing more money toward a market-linked investment before clearing that debt is unlikely to work in your financial favour. High-cost debt repayment delivers a near-certain return; equity markets do not.

Short-term goals under 3–5 years are generally not suited to equity mutual fund SIPs with or without a step-up. Market volatility over short periods can result in a maturity corpus below your total invested amount at exactly the time you need the money.

If you are already committed to multiple SIPs and EMIs that collectively exceed 50–60% of take-home salary, adding a step-up layer before reviewing and rationalising existing commitments creates financial strain without proportionate benefit.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Mutual funds in India are regulated by the Securities and Exchange Board of India (SEBI). All scheme-level disclosures, risk ratings, and performance data are governed by SEBI regulations. Before investing in any scheme, verify information from official sources:

- SEBI — sebi.gov.in (regulatory framework, investor education, registered adviser database)

- AMFI India — amfiindia.com (registered mutual fund advisers, NAVs, risk-o-meter disclosures)

- Fund house websites — Scheme Information Documents (SIDs) and factsheets for each specific scheme

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Calculator outputs — including on this site — are estimates based on user inputs and are not official return projections from any fund house, SEBI, or AMFI.

Expert Tips

- Increase your SIP only after the revised salary has landed in your account for at least one full month — not when the increment letter arrives. Cash flow confirmation matters more than the offer date.

- Run three return scenarios every time you use the step-up SIP calculator: 8%, 10%, and 12%. The range between these scenarios is more useful information than any single corpus figure.

- Match your step-up percentage to your actual salary increment — not to a round number that looks good in the calculator. A 9% increment supports a 9–10% step-up. A 20% step-up with a 9% increment is a cash flow risk in the making.

- Review your SIP amounts once a year — ideally in April after the financial year closes — against your goals, not just your income. Corpus targets shift as life circumstances change.

- If you receive an annual performance bonus, consider making a lump sum addition to an existing fund rather than raising the monthly SIP. This preserves flexibility — a lump sum is a one-time decision, while a higher SIP debit recurs for years.

- Ready to set up your investment structure before adding a step-up layer? Our start investing monthly guide walks through the entire process step by step.

Frequently Asked Questions

What is a step-up SIP calculator?

A step-up SIP calculator estimates your potential mutual fund corpus when you increase your monthly SIP by a fixed percentage each year. You enter four values — starting monthly amount, annual step-up percentage, expected return, and tenure — and the calculator outputs an estimated total invested amount, estimated wealth gain, and estimated maturity corpus. The output depends entirely on your assumed return, not on any guaranteed rate. For context on how mutual fund returns are actually measured, read our guide on returns measurement methods.

Is step-up SIP better than a normal SIP?

It depends on your income pattern and financial discipline. If your salary grows predictably each year and your emergency fund is in place, a step-up SIP helps your investment grow alongside your income. If your income is variable or you are already managing stretched cash flow, a fixed SIP is more sustainable. A step-up SIP is better in practice only if you follow through — a cancelled step-up SIP in Year 8 typically delivers a worse outcome than a consistent fixed SIP over the same period.

What is a good yearly SIP increase percentage?

Align it with your realistic salary increment. A 5% step-up is conservative and sustainable for most salaried employees in stable roles. A 10% step-up matches typical mid-level salary growth in sectors like technology, banking, and consulting. Anything above 15% should only be chosen if income growth is clearly established, your emergency fund is healthy, and you have modelled what the monthly SIP amount will be in Year 10 and Year 15.

Can I reduce or stop a step-up SIP later?

Yes. Most fund houses and investment platforms allow you to pause, reduce, or cancel the step-up instruction without affecting the underlying SIP. The base SIP continues at the last active amount; only future escalation stops. Check the specific process with your fund house or distributor — some require advance notice before the escalation date.

Are step-up SIP returns guaranteed?

No. Mutual fund investments are subject to market risks. Past performance does not guarantee future returns. The calculator uses a return assumption you enter — it does not predict what any fund will actually deliver. As SEBI mandates in all mutual fund communications, scheme returns are not guaranteed and investors may receive less than the amount invested.

Is step-up SIP good for salaried employees?

It can be a well-suited approach for salaried employees with predictable annual increments, a long investment horizon (10 years or more), and an established emergency fund. It is less suitable for employees with irregular income patterns, significant existing debt, or financial goals within the next 3–5 years.

What happens if my bank account balance is insufficient when the increased SIP debit runs?

The instalment will be returned unpaid, similar to a regular SIP dishonour. Most fund houses allow a small number of dishonours before the SIP is automatically cancelled. Consistent dishonours also attract banking charges. Before your step-up activates each year, confirm your standing instruction account will have sufficient balance on the scheduled debit date.

Can I link the step-up to a fixed rupee increase instead of a percentage?

Many fund houses and platforms offer both options — fixed percentage step-up and fixed rupee step-up. A fixed rupee increase (for example, ₹1,000 more per year) is simpler to plan for but may not keep pace with inflation or salary growth over time. A fixed percentage increase maintains proportionality to your growing income. Check the options available on your specific platform or with your distributor before setting up the instruction.

Final Verdict

The step-up SIP calculator is a practical goal-planning tool for Indian salaried investors who expect their income to grow over time. It shows clearly how modest annual increases in monthly investment — tied to real salary growth — can result in a significantly larger estimated long-term corpus compared to a fixed SIP. The math is straightforward: more capital invested over more years, compounding consistently, produces a meaningfully different estimated outcome.

Use the step-up SIP calculator to compare scenarios, stress-test your assumptions at 8%, 10%, and 12%, and choose a step-up percentage you can sustain through a slower increment year. A step-up SIP that gets cancelled in Year 8 because it became unaffordable will underperform a fixed SIP that ran all 15 years without interruption. The corpus difference that matters is the one you actually receive — not the one the calculator showed at a 15% assumed return.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Arjun Kapoor writes about mutual funds, SIPs, ELSS, fund categories, investment returns, and beginner investing concepts for Indian readers. His focus is on education, not product promotion or fund recommendations. He helps readers understand how mutual funds work before they start investing or comparing schemes.

He covers topics such as mutual fund meaning, SIP meaning, SIP calculator, direct mutual funds vs regular plans, NAV, ELSS tax-saving funds, CAGR, absolute returns, XIRR, expense ratio, large cap vs mid cap vs small cap funds, flexi cap funds, index funds vs active funds, liquid funds, debt mutual funds, SIP pause vs SIP stop, lumpsum vs SIP, and how to start SIP in India.

Arjun’s writing is simple, risk-aware, and long-term oriented. He avoids guaranteed-return language and explains investment concepts using examples, timelines, and comparison tables. His articles remind readers that mutual fund investments are subject to market risks, and past performance does not guarantee future returns. Readers should verify scheme details from SEBI, AMFI, fund houses, and official scheme documents.