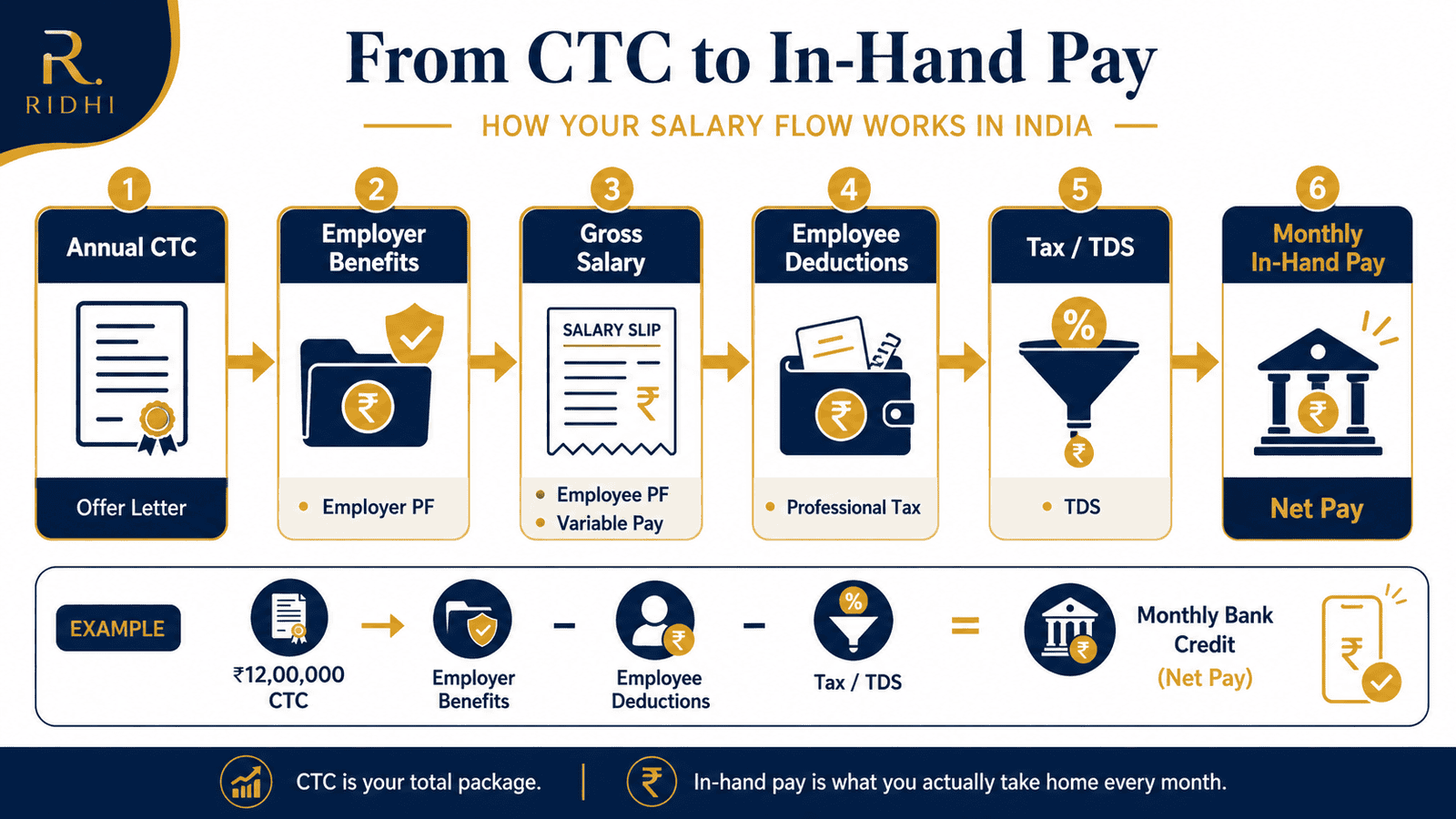

CTC vs In-Hand Salary: How to Calculate What You Actually Earn in India

You receive an offer letter showing ₹12 lakh per year and mentally picture ₹1 lakh arriving in your bank account every month. Then the first salary credit appears: ₹68,000. That gap is not an error — and it is completely explainable once you understand the difference between CTC vs in-hand salary.

CTC is what your employer spends to employ you. In-hand salary is what you actually receive. Between those two numbers sit employer PF contributions, gratuity provisioning, variable pay, employee PF deductions, income tax, and state professional tax. This article breaks the conversion down step by step — with a real ₹12 lakh example, a practical calculation method, and a checklist for reading any offer letter.

Quick Answer: CTC vs In-Hand Salary

CTC vs in-hand salary means your annual company cost is not the same as your monthly bank credit. For a ₹12 lakh CTC, subtract employer PF, employee PF, tax/TDS, professional tax, insurance, variable pay, and other deductions to estimate monthly take-home salary. The actual monthly in-hand amount depends on your salary structure, state, tax regime, and employer — always verify with HR before budgeting.

How to Calculate Monthly In-Hand Salary from CTC

Follow these five steps to convert any CTC figure into an estimated monthly in-hand salary. Each step removes a layer that your offer letter includes but your bank account never sees.

Monthly In-Hand = (Annual Fixed Gross ÷ 12) − Employee PF − Monthly TDS − Professional Tax − Other Deductions

Step 1 — Read Your Annual CTC from the Offer Letter

CTC is the total cost your employer incurs to employ you for one year. It includes salary, employer PF, gratuity provisioning, insurance premiums, variable pay, and the monetary value of any other benefit. Do not divide this number by 12 and call it your monthly pay.

Step 2 — Remove Employer-Side Costs

Employer PF is 12% of your basic salary, paid by your employer — not deducted from your pay. Gratuity provisioning (approximately 4.81% of basic) is another employer-side cost. Group health insurance premiums, if included in CTC, fall into the same category. These are inside your CTC but never arrive as cash.

Step 3 — Separate Fixed Pay from Variable Pay

Performance bonus, annual incentive, and retention pay are part of CTC but are not guaranteed monthly. Use only your fixed annual gross — basic + HRA + allowances — for monthly budgeting. Treat variable pay as potential upside, not a baseline.

Step 4 — Convert to Monthly Gross

Divide your annual fixed gross (after removing employer-side costs and variable pay) by 12. This is your monthly gross salary — the figure before employee-side deductions.

Step 5 — Deduct Employee-Side Items

Three deductions reduce monthly gross to in-hand:

- Employee PF: 12% of your monthly basic salary, sent to your EPF account. Per EPFO guidelines, this is mandatory for covered establishments.

- TDS (Section 192): Your employer deducts income tax monthly based on your projected annual taxable income and your declared tax regime.

- Professional Tax: A state-level levy applicable in Maharashtra, Karnataka, West Bengal, Tamil Nadu, and several other states. In Maharashtra, the standard rate is ₹200 per month for salaries above ₹10,000 per month.

Use the monthly take-home salary calculator

| Annual CTC | Est. Monthly Gross (Fixed) | Est. Monthly In-Hand Range |

|---|---|---|

| ₹6 lakh | ₹43,000–₹46,000 | ₹37,000–₹41,000 |

| ₹12 lakh | ₹74,000–₹78,000 | ₹63,000–₹69,000 |

| ₹18 lakh | ₹1,10,000–₹1,15,000 | ₹88,000–₹96,000 |

These ranges are illustrative only. Actual in-hand salary depends on your specific salary breakup, state of employment, tax regime, and employer structure.

Key Takeaways

- CTC is your employer’s total annual cost — it includes employer PF, gratuity, insurance, and benefits that never appear as monthly bank credits.

- For a ₹12 lakh CTC, monthly in-hand salary is typically in the range of ₹63,000–₹69,000 — not ₹1 lakh — after PF, TDS, and professional tax deductions.

- Variable pay (performance bonus, incentive) is part of CTC but is not guaranteed monthly cash — never count it as part of your regular monthly budget.

- Employee PF is 12% of your basic monthly salary, deducted from your gross pay; employer PF is also 12% of basic but comes from the employer’s side and is embedded inside your CTC.

- Your tax regime choice affects monthly TDS — selecting the right regime can add ₹2,000–₹5,000 or more to monthly in-hand on a ₹12 lakh salary.

- Always ask HR for a written month-wise salary breakup — fixed pay, variable pay, and estimated monthly deductions — before signing any offer letter.

Key Facts at a Glance

| Term | What It Means | Where It Appears |

|---|---|---|

| CTC (Cost to Company) | Total employer annual cost: salary + employer PF + gratuity + insurance + variable pay + benefits | Offer letter, employment contract |

| Gross Salary | Basic + HRA + all allowances — before employee PF and TDS are deducted | Salary slip (earnings column) |

| Net Salary / In-Hand Pay | Monthly amount credited to your bank after all employee-side deductions | Salary slip (net pay line), bank statement |

| Employee PF | 12% of basic salary deducted from your gross and credited to your EPF account | Salary slip (deductions side) |

| Employer PF | 12% of basic salary paid by your employer — inside CTC, not deducted from your gross pay | CTC breakup sheet, Form 16 |

| Variable Pay | Performance bonus, incentive, or retention pay — part of CTC, paid periodically, not guaranteed monthly | Offer letter, variable pay policy |

| Professional Tax | State-level deduction — up to ₹2,500 per year; not applicable in all states | Salary slip (deductions side) |

| TDS on Salary | Monthly income tax withheld by employer under Section 192 — varies by income, regime, and declarations | Salary slip, Form 16, Form 26AS |

For how each of these lines appears on your payslip: salary slip components explained

Understanding CTC vs In-Hand Salary: The Full Picture

When a recruiter quotes “₹12 lakh package,” they mean the employer’s total annual expenditure to keep you on payroll. That is CTC — Cost to Company. It is a cost figure, not a salary figure. And those two things are different in ways that matter every month.

What CTC Actually Contains

A typical Indian CTC bundles four types of components. Some arrive as monthly cash. Others build long-term benefits. And some are perquisites that hold monetary value for the employer but never land in your account.

- Fixed cash earnings: Basic salary, House Rent Allowance, Special allowance, Leave Travel Allowance, other fixed monthly allowances — these credit to your bank each month.

- Employer statutory contributions: Employer PF (12% of basic) and gratuity provisioning (approximately 4.81% of basic) — employer costs included in CTC but never paid to you as cash.

- Variable pay: Performance bonus, annual incentive, sales commission — part of CTC, paid periodically and conditionally.

- Benefits and perquisites: Group health insurance premiums, meal vouchers, club memberships — their monetary value appears in your CTC but they are not cash-in-hand.

On a ₹12 lakh CTC with ₹4.8 lakh basic, employer PF alone accounts for ₹57,600 and gratuity provisioning adds approximately ₹23,088 — that is over ₹80,000 removed from the headline number before a single rupee of employee deduction.

For a deeper explanation of why annual CTC looks so much larger than your monthly credit: why your CTC looks bigger than in-hand pay

The Flow from CTC to Gross Salary

Gross salary is what remains after removing employer-side costs from CTC. It is the amount your employer pays you directly — before your share of PF and income tax are deducted.

Gross Salary = CTC − Employer PF − Gratuity Provisioning − Insurance Premium − Other Employer-Side Benefits

For a ₹12 lakh CTC, removing employer PF (₹57,600) and gratuity provisioning (approx. ₹23,088) brings the annual cash component down to roughly ₹11.2 lakh before any employee deduction is applied.

The Flow from Gross Salary to Net (In-Hand) Pay

Three main deductions convert monthly gross to monthly in-hand:

- Employee PF: 12% of basic monthly salary, sent to your EPF account. On a ₹40,000 monthly basic, that is ₹4,800 per month — ₹57,600 per year. According to EPFO guidelines, this is mandatory for employees in covered establishments.

- TDS under Section 192: Your employer estimates your total annual taxable income, calculates the annual tax, and divides it into 12 monthly deductions. The amount changes based on your investment declarations, HRA exemption, tax regime choice, and Form 16 data.

- Professional Tax: Applicable in Karnataka, Maharashtra, West Bengal, Tamil Nadu, Andhra Pradesh, and several other states. In Maharashtra, the standard rate is ₹200 per month for most salaried employees earning above ₹10,000 per month.

Why Variable Pay Complicates the Picture

If ₹72,000 of your ₹12 lakh CTC is annual performance bonus, it may be paid once a year — only if you meet targets. Counting it as ₹6,000 per month in your budget is a planning error that compounds every month. Some employers pay variable quarterly; others annually; others link it to company-level profitability. Always read the variable pay policy document before building any financial plan on the full CTC number.

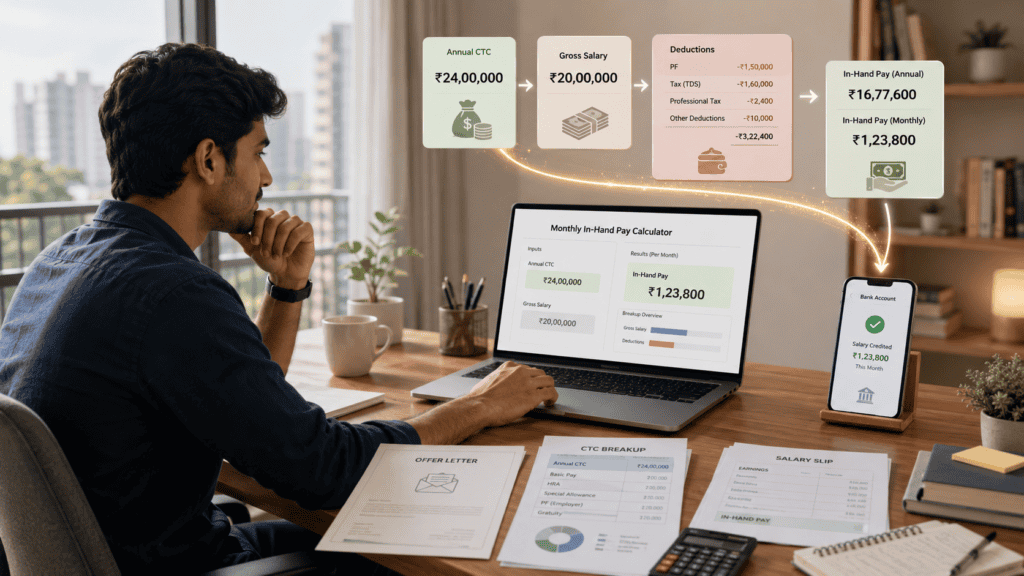

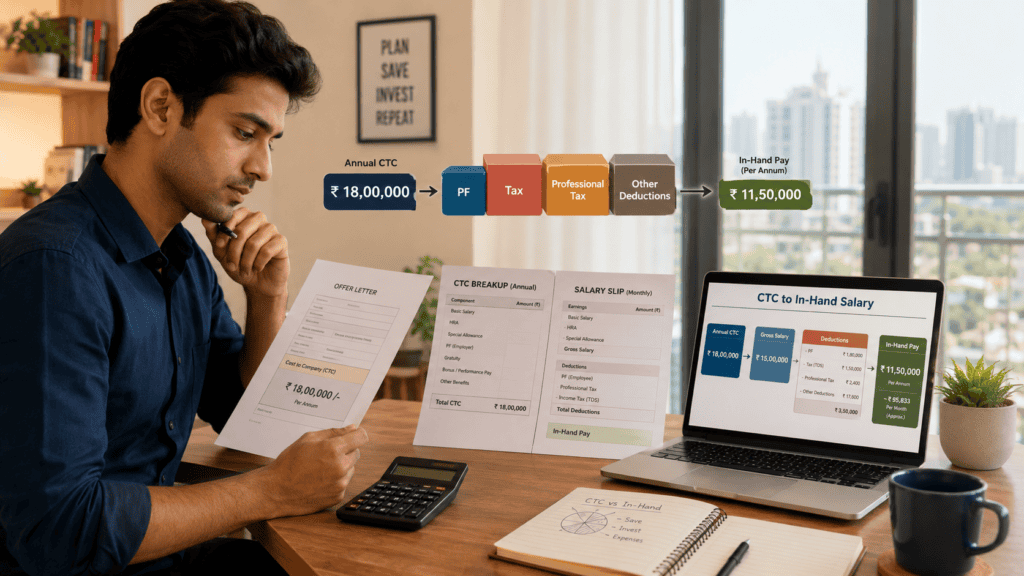

Real Example: Rohit’s ₹12 Lakh Offer Letter

Rohit, 28, is a software engineer at a mid-size IT company in Pune. His offer letter says ₹12,00,000 CTC. He expected roughly ₹1 lakh per month. Here is the actual breakup.

| Component | Annual (₹) | Monthly (₹) |

|---|---|---|

| Basic Salary | 4,80,000 | 40,000 |

| House Rent Allowance | 2,40,000 | 20,000 |

| Special Allowance | 2,04,912 | 17,076 |

| Variable Pay (performance bonus) | 72,000 | — |

| Employer PF (12% of basic) | 57,600 | — |

| Gratuity Provisioning (~4.81% of basic) | 23,077 | — |

| Group Health Insurance | 22,411 | — |

| Total CTC | 12,00,000 | — |

Rohit’s fixed monthly gross = ₹40,000 + ₹20,000 + ₹17,076 = ₹77,076. Now apply employee-side deductions:

| Deduction | Monthly (₹) | Basis |

|---|---|---|

| Employee PF | 4,800 | 12% of ₹40,000 basic |

| TDS (estimated, new regime) | ~3,650 | Taxable income after standard deduction |

| Professional Tax (Maharashtra) | 200 | State levy for salary above ₹10,000/month |

| Total Deductions | ~8,650 | — |

Rohit’s estimated monthly in-hand: ₹77,076 − ₹8,650 = approximately ₹68,426.

That is roughly ₹68,000 — not ₹1 lakh. The gap of over ₹31,000 per month is real: employer-side costs, variable pay not counted monthly, employee PF, TDS, and professional tax all take their share. Understanding your basic salary specifically is critical — it drives your PF amount, gratuity entitlement, HRA exemption, and tax calculation. See: how basic salary affects PF, HRA, and tax

Comparison: CTC vs Gross Salary vs Net Salary vs In-Hand Pay

These four terms describe the same salary at four different stages of calculation. Using them interchangeably when reading an offer letter — or comparing two jobs — leads to real financial mistakes.

| Term | What It Includes / Excludes | Key Document |

|---|---|---|

| CTC | Everything the employer spends: salary + employer PF + gratuity + insurance + variable pay + benefits | Offer letter |

| Gross Salary | Fixed cash earnings (basic + HRA + allowances) before employee PF and TDS are deducted | Salary slip — earnings column |

| Net Salary | Gross salary minus employee PF, TDS, professional tax, and any other employee-side deductions | Salary slip — net pay line |

| In-Hand / Take-Home | Same as net salary in most standard payrolls — the amount actually credited to your bank | Bank statement |

| Taxable Salary | Gross salary minus applicable exemptions (HRA, LTA) minus standard deduction — the base for income tax | Form 16, ITR |

| Fixed Pay | The portion paid every month regardless of performance — excludes variable pay and one-time components | Offer letter — fixed component line |

How to Decide What’s Right for You

You are comparing two job offers — compare fixed monthly in-hand salary first, not total CTC. A ₹15 lakh offer with 30% variable pay may deliver lower monthly cash than a ₹13 lakh offer with 10% variable pay, depending on the salary structure.

Your offer letter shows a high CTC but HR cannot provide a written month-wise salary breakup — ask for a written structure showing fixed pay, variable pay, and estimated monthly deductions before you sign anything.

Employer PF is inside your CTC — as is common in most mid-size and large Indian companies — your real cash component is ₹57,600 lower per year on a ₹4.8 lakh basic before any employee deduction. Factor this into your offer comparison.

You have limited 80C investments, no home loan, and moderate HRA — the new tax regime is likely to improve your monthly in-hand because of the ₹75,000 standard deduction and lower slab rates for incomes under ₹12–15 lakh. Verify your specific case. Compare old vs new tax regime

You are planning monthly EMIs, rent, SIPs, or any recurring commitment — use only fixed monthly in-hand as your planning figure. Variable pay, joining bonuses, and annual bonuses should be treated as upside until they arrive.

You do not have a written salary breakup showing each component separately — do not accept, sign, or budget based on the CTC headline alone. Request a breakup in writing. Most HR teams provide this on request before the date of joining.

Common Mistakes to Avoid

Dividing CTC by 12 and Treating It as Monthly Pay

This is the most common and most expensive budgeting error for salaried employees in India.

On a ₹12 lakh CTC, the actual monthly in-hand is typically ₹63,000–₹69,000 — not ₹1 lakh — after removing employer-side costs, variable pay, employee PF, TDS, and professional tax. Assuming ₹1 lakh leads to overestimated EMI capacity and a savings shortfall from month one.

Use the five-step method above or the take-home calculator to get an accurate estimate before committing to any recurring expense.

Counting Variable Pay as Guaranteed Monthly Income

Variable pay in your CTC is conditional — it depends on your performance rating, team targets, and your employer’s profitability cycle.

A ₹72,000 annual performance bonus looks like ₹6,000 per month — but if it arrives once a year (or not at all in a poor year), including it in your monthly budget means you are consistently over-counting monthly income by ₹6,000 every single month.

Exclude variable pay from monthly cash flow planning until it has been credited to your account.

Confusing Employee PF with Employer PF

These are two separate deductions with very different effects on your salary. Employee PF reduces your gross monthly pay and therefore your in-hand salary. Employer PF is part of CTC and reduces the cash value of your total package — but it does not appear as a deduction on your salary slip.

Confusing them causes you to either overestimate in-hand (if you forget the employee deduction) or underestimate gross salary (if you confuse their placement). See: employee PF vs employer PF full breakdown

Ignoring State-Wise Professional Tax

Professional tax is not a national deduction — it applies in specific states only. If you work in Maharashtra, Karnataka, Tamil Nadu, or West Bengal, it is deducted monthly.

In Maharashtra, the standard rate is ₹200 per month for most salary levels above ₹10,000 per month — ₹2,400 per year that many online CTC calculators omit entirely. Forgetting it means your calculated in-hand is slightly higher than your actual bank credit.

Always check whether professional tax applies in your state before finalising your budget.

Not Submitting Investment Declarations Early Enough

TDS under Section 192 is recalculated by your employer during the year based on declarations you submit. If you do not declare investments at the start of the financial year, your employer may deduct higher TDS from April onward — and a large catch-up deduction typically hits in January–March.

Submit your tax regime choice and investment declarations to HR in April and submit investment proofs by December to keep monthly TDS stable and predictable.

Using Gross Salary for EMI Eligibility Estimates

Banks assess loan eligibility on net monthly income, not gross. If your gross is ₹77,000 but in-hand is ₹68,000, your actual EMI capacity is lower than the bank’s initial estimate based on your gross figure.

Always use net in-hand salary when calculating how much EMI you can comfortably afford each month.

When This May Not Be the Right Choice

The five-step CTC-to-in-hand calculation works reliably for standard salaried roles with a simple fixed and variable structure. It may not give you an accurate picture in these situations:

- Your CTC includes ESOPs or stock grants: Equity compensation adds notional value that does not translate to cash until shares vest and are sold. A ₹5 lakh ESOP component inside a ₹20 lakh CTC is not guaranteed monthly income.

- Your role is heavily commission- or incentive-driven: If 40%–60% of your CTC is variable, the fixed in-hand estimate represents a floor — not a reliable average — and your actual monthly pay will vary significantly.

- You work with multiple employers in the same financial year: Each employer calculates TDS only on income paid by them. Without informing your new employer of prior-year income, TDS may be under-deducted and a tax demand may arise at ITR filing.

- Your employer uses a Flexible Benefit Plan (FBP): Components like LTA, meal coupons, and medical allowance may be flexed in and out of the CTC, meaning the same headline CTC produces different monthly cash depending on how you allocate benefits.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Salary structures, income tax slabs, EPF contribution rates, and professional tax slabs are all subject to change after a Union Budget or regulatory notification. Verify current figures from these official sources before making any decision based on numbers quoted in this article:

- Income Tax Department (incometax.gov.in) — for current income tax slabs, standard deduction amounts, Section 192 TDS rules, old and new tax regime comparison, and Form 16 guidance.

- EPFO (epfindia.gov.in) — for current EPF contribution rates, PF wage ceiling, and employee and employer PF rules for covered establishments.

- Your state government’s commercial taxes or finance department website — for current professional tax slabs applicable in your state of employment.

- Your employer’s HR or payroll portal — for the actual CTC breakup, salary slip format, and variable pay policy specific to your role and company.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before signing any offer, ask HR three specific questions in writing: What is my fixed monthly gross? What is my estimated monthly in-hand after PF, TDS, and professional tax? When and exactly how is variable pay calculated and paid? These three answers tell you far more than the CTC headline.

- Compare job offers on fixed monthly in-hand — not CTC. A ₹14 lakh CTC with 25% variable and employer PF embedded inside CTC may deliver less monthly cash than a ₹12 lakh CTC with 10% variable and employer PF outside CTC.

- Submit your tax regime declaration to HR in the first week of April. Employers use this to calibrate TDS for the full financial year. Delaying submission often results in higher TDS in the early months and unpredictable deductions later.

- Check whether your employer caps PF calculation at ₹15,000 per month basic. Some employers calculate PF on a capped ₹15,000 wage even if your actual basic is higher. This reduces monthly employee PF deduction and slightly increases in-hand — but also reduces your long-term EPF corpus. Know the trade-off.

- Never use gross salary when calculating EMI affordability. A standard thumb rule is that total EMIs should not exceed 40%–50% of net monthly in-hand — not gross. Using gross overstates your repayment capacity.

- Factor in professional tax when comparing offers across cities. Moving from Delhi (no professional tax) to Bengaluru or Mumbai (professional tax applicable) reduces monthly in-hand by ₹150–₹200 per month. Small, but worth knowing when budgeting a relocation.

Frequently Asked Questions

Is CTC the same as my salary?

No. CTC is your employer’s total annual cost to employ you — it includes salary components plus employer PF, gratuity provisioning, insurance premiums, variable pay, and other benefits. Your actual salary — gross or net — is a subset of CTC. You will never receive the full CTC as cash.

Why is my in-hand salary so much lower than my CTC?

Because CTC includes employer-side costs (employer PF, gratuity, insurance) that never come to you as cash, variable pay that is paid periodically and conditionally, and employee-side deductions (employee PF, TDS, professional tax) that reduce your gross pay before it is credited. All of these gaps together explain the difference.

Is employer PF deducted from my salary?

No. Employer PF is paid by your employer and comes out of the CTC budget — not your gross salary. However, because employer PF is included inside your CTC, it reduces the cash component of your total package. Employee PF — 12% of your monthly basic — is what is actually deducted from your gross salary and reduces your in-hand pay.

Does variable pay come every month?

Typically, no. Performance bonus, annual incentive, and sales commission are usually paid quarterly or annually and are linked to your performance rating and company targets. Some employers in sales or customer-facing roles pay monthly incentives. Always read the variable pay policy in your offer letter before treating any variable component as regular monthly cash.

How do I calculate monthly in-hand salary from CTC?

Remove employer-side costs (employer PF, gratuity provisioning, insurance) from CTC. Separate variable pay. Divide remaining fixed annual gross by 12 to get monthly gross. Subtract employee PF (12% of basic), estimated monthly TDS, and professional tax if applicable in your state. The result is your estimated monthly in-hand. Use the take-home calculator on this page for a quicker estimate.

Which is better: high CTC or high fixed pay?

For monthly budgeting, EMI planning, and financial security — high fixed pay is more reliable. High CTC with a large variable component gives you a big headline number but uncertain monthly cash. If you are comparing two offers at a similar CTC, the one with a higher fixed monthly in-hand salary is almost always more stable financially, all else being equal.

Can I negotiate my salary structure — not just the amount?

Yes, and it is worth doing. In many mid-size and large companies across IT, BFSI, and FMCG sectors, you can request a restructured breakup — more fixed pay, lower variable — or ask whether employer PF can be placed outside CTC. This does not change the employer’s total cost but changes how much of your package arrives as monthly cash. Ask before you join.

What is Form 16 and how does it relate to my CTC?

Form 16 is a TDS certificate issued by your employer at the end of each financial year. Part A shows total TDS deducted and deposited. Part B shows a detailed salary breakup including gross salary, exemptions, standard deduction, and taxable income as per the Income Tax Department. It is your primary salary document for ITR filing and will clearly show which components of your CTC were treated as taxable pay.

What happens if I switch jobs mid-year — how does TDS change?

Your new employer calculates TDS based only on salary paid by them — they will not automatically account for income received from your previous employer. To avoid under-deduction and a tax demand at ITR time, submit your previous employer’s salary details (via Form 12B or salary slip) to your new HR team as soon as you join. This allows your new employer to account for your full-year income when calculating TDS.

Is professional tax the same across all Indian states?

No. Professional tax is levied by state governments and applies only in states that have enacted professional tax legislation — including Maharashtra, Karnataka, Tamil Nadu, West Bengal, Andhra Pradesh, and Telangana. It does not apply in Delhi, Haryana, Rajasthan, or Uttar Pradesh, among others. Rates and slabs vary by state and salary level. Your salary slip will show the deduction if it applies to your state of employment.

Final Verdict

CTC vs in-hand salary is one of the most practically important differences a salaried employee in India needs to understand — whether you are evaluating your first offer letter, comparing two jobs, or planning your monthly household budget.

CTC is a useful figure for comparing employer costs across companies. In-hand salary is what you actually live on. For most employees on a ₹12 lakh CTC structure, monthly in-hand lands in the ₹63,000–₹69,000 range after employer-side costs, employee PF, TDS, and professional tax. The exact number depends on your salary breakup, state of employment, employer structure, and your tax regime choice.

Before accepting any offer: request a month-wise salary breakup in writing, estimate your in-hand using the five-step method or calculator, and verify current tax and PF rules from official sources. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Vikram Sethi writes about loans, EMI planning, credit score impact, borrowing costs, and repayment decisions for Indian borrowers. His content helps readers look beyond the monthly EMI and understand the full cost of borrowing, including principal, interest, processing fees, GST, insurance, prepayment charges, foreclosure fees, late payment penalties, and credit score impact.

He covers topics such as EMI calculators, home loan eligibility, personal loan eligibility, debt-to-income ratio, flat interest rate vs reducing balance, missed EMI consequences, loan prepayment vs part payment, home loan balance transfer, processing fees, gold loan vs personal loan, car loan vs cash purchase, top-up home loans, loan against PPF, and credit score basics.

Vikram’s writing style is practical, cautionary, and calculation-driven. He uses Indian examples, ₹ amounts, comparison tables, and decision frameworks to help borrowers compare options more carefully. His articles are educational and do not guarantee loan approval, interest rates, or savings. Readers should verify current rates, charges, eligibility, and terms directly with lenders before applying or refinancing.