You receive the offer letter, spot the headline CTC, divide by 12 — and feel good about the number. Then the first salary arrives in your bank account and it is nowhere near that figure. That gap is not a calculation error. It is how Indian salary structures work, and using a take-home salary calculator India tool without understanding those deductions means you will get the same unpleasant surprise every month.

The culprit is a chain of deductions: employer PF tucked inside your CTC, employee PF taken from your gross pay, professional tax levied by your state, and income tax deducted at source every month. For someone on a ₹12,00,000 CTC in Pune, the actual monthly bank credit can be ₹10,000 to ₹20,000 lower than a simple divide-by-12 estimate. This guide walks through the formula step by step, a realistic Indian salary example, and exactly what to verify before relying on any calculator output.

Quick Answer: Take-Home Salary Calculator India

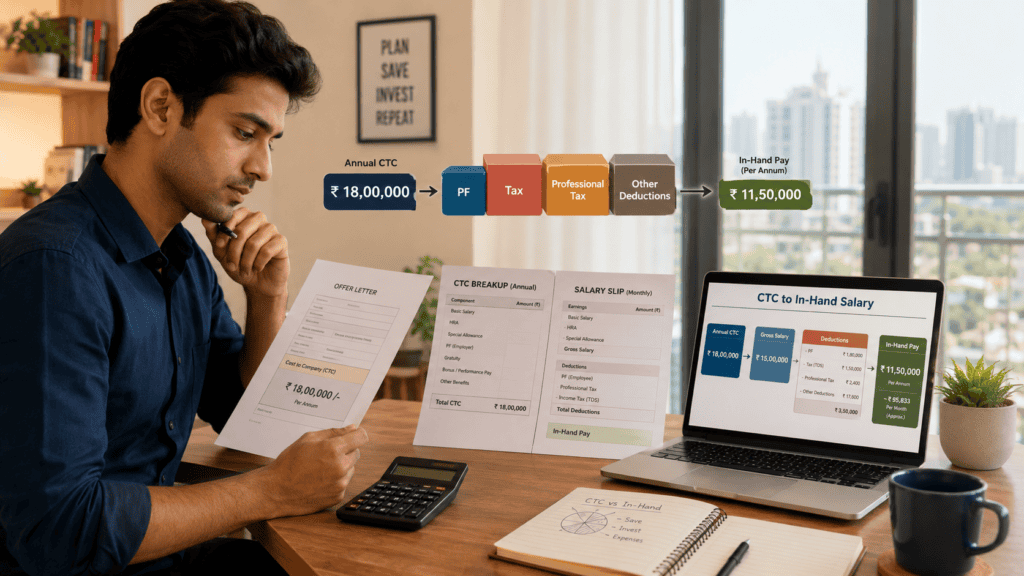

A take-home salary calculator India helps you estimate monthly in-hand pay from CTC after salary components such as basic pay, HRA, employee PF, professional tax, income tax/TDS and other deductions. For example, a ₹12,00,000 CTC may not mean ₹1,00,000 monthly credit because employer PF and taxes reduce cash salary.

How to Calculate Monthly In-Hand Salary from CTC

Most take-home salary calculators in India follow the same four-step formula. Understanding each step tells you exactly where the money goes — and which assumptions the calculator is making on your behalf. Use Ridhi’s take-home salary calculator to estimate your monthly in-hand pay with your own inputs.

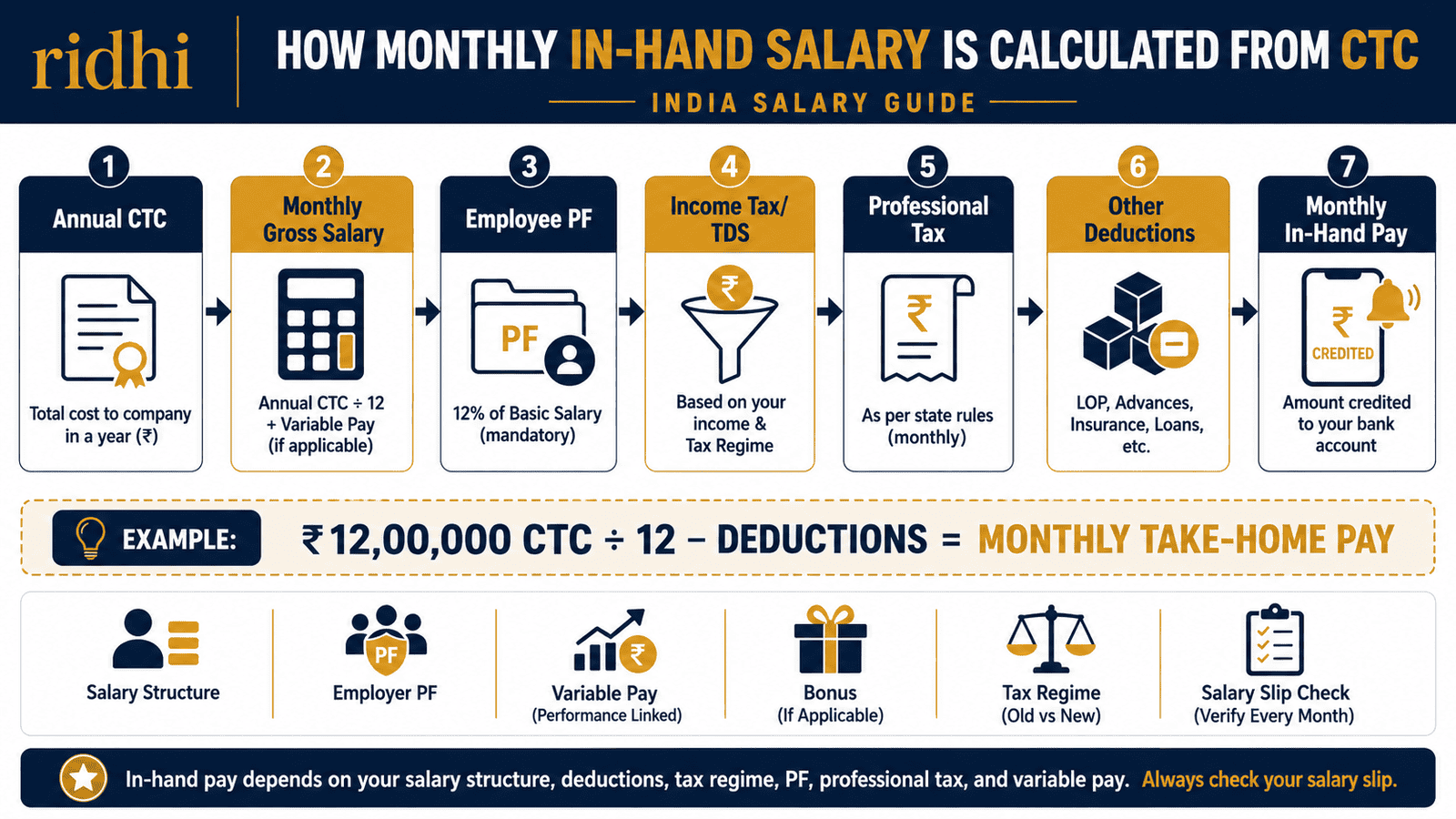

Monthly In-Hand = [(Annual CTC − Employer-Side Non-Cash Items) ÷ 12] − Monthly Deductions

Step 1 — Start with Annual CTC

Your Cost to Company is the total annual amount your employer spends on employing you. It includes items that never reach your bank account — employer PF contribution, gratuity provision, group insurance, and similar benefits. Always start your calculation from annual CTC, not from any “monthly salary” shortcut.

Step 2 — Remove Employer-Side Non-Cash Items

Employer PF contribution (typically 12% of basic salary) is usually the largest employer-side item inside CTC. Gratuity provision, group health insurance premium, and meal or transport benefits may also be included. Removing these gives you your annual gross salary — the total cash portion of your CTC.

Step 3 — Divide by 12 for Monthly Gross Salary

Monthly gross salary is what your payslip shows before any deductions. It covers basic pay, HRA, special allowances, and fixed monthly components. This is the starting figure on your salary slip every month.

Step 4 — Subtract Monthly Deductions

Three main deductions convert monthly gross to in-hand pay: employee PF contribution (typically 12% of basic salary, credited to your EPF account), professional tax (a state-level deduction, usually ₹200 per month in states that levy it), and TDS on salary under Section 192 (income tax deducted monthly by your employer based on your estimated annual tax liability and the regime you have chosen).

Illustrative estimates (new tax regime, basic at 40% of CTC, employer PF included in CTC):

| Annual CTC | Approx. Monthly Gross | Est. Monthly In-Hand (New Regime) |

|---|---|---|

| ₹6,00,000 | ₹47,600 | ₹44,000–₹47,000 |

| ₹12,00,000 | ₹95,200 | ₹88,000–₹92,000 |

| ₹20,00,000 | ₹1,64,500 | ₹1,40,000–₹1,50,000 |

These are illustrative estimates only. Actual in-hand salary depends on your employer’s salary structure, PF deduction policy, state professional tax, variable pay, current tax slabs, standard deduction amount, and the tax regime you have chosen. Always use your actual salary breakup for accurate figures.

Key Takeaways

- CTC is the employer’s total annual cost — not the monthly amount credited to your bank. Dividing CTC by 12 overstates your in-hand salary by ₹8,000 to ₹20,000 in most mid-range salary packages.

- Employer PF contribution (12% of basic salary) is often included inside CTC, reducing your annual gross cash salary before any deductions even touch your payslip.

- Employee PF (12% of basic) is deducted from your monthly gross — reducing take-home by ₹2,400 on a ₹20,000 basic or ₹4,800 on a ₹40,000 basic each month.

- Professional tax is a state-level deduction — typically ₹200 per month in states such as Maharashtra, Karnataka and West Bengal. Several states do not levy it at all.

- The tax regime you choose (old or new) can change your monthly TDS by ₹5,000–₹15,000 at mid-level CTCs. Current income tax slab rates and standard deduction amounts must be verified at incometax.gov.in before relying on any estimate.

- Two employees with identical CTCs can receive meaningfully different monthly in-hand salaries depending on their basic pay ratio, PF treatment, variable pay, and tax declarations.

- Calculator output is always an estimate. Your actual salary slip and HR payroll system are the only reliable sources of your exact monthly bank credit.

Key Facts at a Glance

| Salary Term | What It Means | Reaches Your Bank? |

|---|---|---|

| CTC (Cost to Company) | Total annual employer cost — includes employer PF, gratuity, insurance, benefits | No — employer-side items are not paid to you in cash |

| Gross Salary | Annual cash salary after removing employer-side non-cash items from CTC | No — employee deductions still apply |

| Monthly Gross | Gross salary ÷ 12 — payslip total before employee-side deductions | No — PF, PT, and TDS are deducted first |

| Net / In-Hand Salary | Monthly gross minus employee PF, professional tax, and income tax TDS | Yes — this is the actual bank credit |

| Employee PF | 12% of basic salary deducted monthly and deposited to EPF account under EPFO rules | No — goes to PF account, not current account |

| Professional Tax | State employment tax, typically up to ₹2,400 per year where applicable | No — remitted to state government |

| TDS (Section 192) | Monthly income tax deducted by employer based on annual tax estimate and regime chosen | No — remitted to Income Tax Department |

How Take-Home Salary Is Calculated in India

The distance between your headline CTC and the actual monthly bank credit is not random. It follows a defined structure — one that your payslip traces every month, even if it has never been explained to you clearly.

CTC Is What You Cost, Not What You Earn

Your Cost to Company is the total employer spend on your employment. It bundles items that benefit you indirectly — employer PF going into your retirement corpus, a gratuity provision building up year by year, group health insurance covering hospitalisation — but none of these reach your bank account as monthly cash. For a thorough explanation of this gap, read the guide on CTC versus in-hand pay.

Subtracting employer-side items from CTC leaves annual gross salary — the total cash available for monthly pay. This is the figure payroll actually works with. For a component-by-component breakdown of what appears on your payslip, see the salary slip components guide.

The Three Deductions That Reduce Monthly Gross

Employee Provident Fund: Under EPFO rules, you contribute 12% of your basic salary every month to your EPF account. This is a compulsory saving — it builds a retirement corpus — but it immediately reduces the cash you receive. The matching employer contribution is usually already inside your CTC and does not reduce your take-home additionally. Current PF contribution rates and the wage ceiling for mandatory contribution should be verified at epfindia.gov.in.

Professional Tax: States such as Maharashtra, Karnataka, West Bengal and Andhra Pradesh levy professional tax on salaried employees, usually ₹200 per month for most income brackets. Some states do not charge it at all. Because it varies by state and income slab, any calculator that does not ask for your state of employment may apply the wrong figure — or miss it entirely.

Income Tax Deducted at Source: Your employer deducts TDS every month under Section 192 of the Income Tax Act, based on your projected annual taxable income. The monthly deduction depends on the tax regime you have declared, investment and exemption proofs you have submitted, and the current standard deduction applicable for salaried employees. According to the Income Tax Department (incometax.gov.in), employees must inform their employer of their regime choice at the start of each financial year — and can change it only at the time of filing their ITR.

Variable Pay and Why It Distorts Calculator Output

Many Indian salary structures include a variable pay component — performance bonus, sales incentive, or project allowance — paid quarterly or annually, not monthly. This component is part of your CTC but is not guaranteed cash every month. If your salary breakup shows a high variable component, your fixed monthly in-hand will always be lower than a CTC ÷ 12 estimate suggests. Any salary calculator that uses total CTC without separating fixed and variable pay will overstate your monthly bank credit.

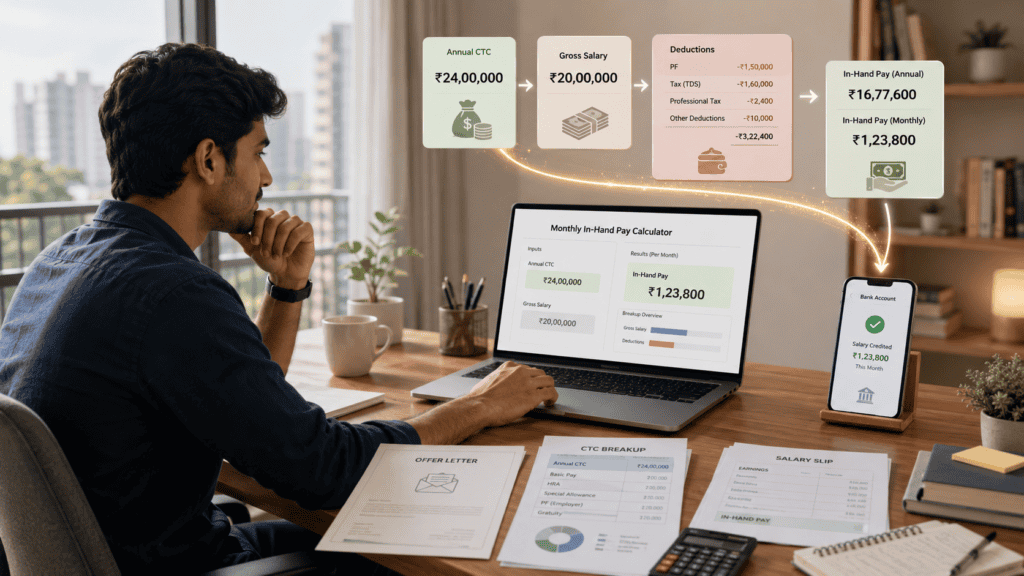

Real Example: Rohan’s ₹12,00,000 CTC in Pune

Rohan, 27, is a software analyst at a mid-size IT company in Pune. His offer letter quotes an annual CTC of ₹12,00,000. Here is an illustrative salary breakdown using standard Indian payroll assumptions.

Step 1 — Annual CTC: ₹12,00,000

Step 2 — Employer-side items inside CTC: Employer PF on basic salary of ₹40,000/month = ₹4,800/month → ₹57,600/year. Annual gross salary = ₹12,00,000 − ₹57,600 = ₹11,42,400.

Step 3 — Monthly gross: ₹11,42,400 ÷ 12 = ₹95,200.

Step 4 — Monthly deductions from Rohan’s payslip:

- Employee PF (12% of ₹40,000 basic): ₹4,800

- Professional tax (Maharashtra): ₹200

- TDS: varies significantly by regime and current tax rules — under the new regime with standard deduction applied, Rohan’s annual taxable income in this illustration falls within a range where TDS may be low or nil; under the old regime without any deduction claims, monthly TDS could reach ₹10,000–₹13,000

Estimated monthly in-hand (new regime): approximately ₹88,000–₹91,000

Estimated monthly in-hand (old regime, no deductions claimed): approximately ₹78,000–₹82,000

The regime choice alone creates a ₹8,000–₹12,000 difference in monthly bank credit in this example — without any change to Rohan’s actual CTC. Understanding how Basic salary impact on PF, HRA and tax works is essential before evaluating any offer.

All PF rates, tax slabs, standard deduction amounts, and professional tax figures used above are illustrative. Verify current rates at epfindia.gov.in and incometax.gov.in before relying on any of these numbers.

Comparison: CTC vs Gross Salary vs Net Salary vs In-Hand Pay

| Parameter | CTC / Gross Salary | Net / In-Hand Salary |

|---|---|---|

| What it represents | Employer’s total annual cost (CTC) or total cash before deductions (gross) | Cash actually credited to your bank account each month |

| Includes employer PF | Yes (CTC) / No (Gross) | No |

| Shown in offer letter | Yes | Rarely |

| Shown in salary slip | Yes (Gross) | Yes |

| Employee deductions applied | None — pre-deduction figure | Employee PF, professional tax, TDS |

| Best used for | Comparing offers, salary negotiation | Monthly budgeting, EMI planning, SIP sizing |

| Typical % of CTC | Gross: 85–95% of CTC | 70–85% of CTC (varies by structure and tax) |

How to Decide What’s Right for You

You are comparing two job offers — compare fixed monthly in-hand pay, not headline CTC. Two ₹15,00,000 CTC offers can produce different monthly bank credits by ₹10,000 or more depending on basic pay ratio, variable pay structure and PF treatment.

Your taxable income is likely under ₹12,75,000 annually after standard deduction — the new tax regime may result in very low or zero monthly TDS, significantly boosting your in-hand pay. Use the Income tax comparison tool to verify this against current rules before declaring your regime to HR.

You have significant 80C investments, active HRA claims or home loan interest deductions — the old tax regime may reduce your total tax more than the new regime’s lower slab rates. The monthly take-home difference at ₹12,00,000–₹20,00,000 CTC can be ₹5,000–₹15,000 depending on your deduction amounts.

A large portion of your CTC is variable pay, joining bonus or performance incentive — your fixed monthly in-hand will be lower than any calculator assumes. Do not set up recurring EMIs or SIPs based on variable components you have not yet received.

Your employer deducts employee PF on actual basic salary rather than on the ₹15,000 PF wage ceiling — your monthly PF deduction will be higher than many generic calculators assume, and your in-hand salary lower.

You have not received your actual salary breakup from HR — do not use a generic calculator output as the basis for financial commitments such as rent, loan EMIs or SIPs. The calculator’s structural assumptions may not match your employer’s payroll design.

Common Mistakes to Avoid

Dividing CTC by 12 and Assuming That Is Your Monthly Salary

This is the most common mistake salaried employees make when reading an offer letter.

CTC includes employer PF, gratuity, insurance and other non-cash items. Dividing by 12 can overstate your monthly in-hand by ₹10,000–₹25,000. Someone on ₹12,00,000 CTC often receives ₹88,000–₹92,000, not ₹1,00,000. Read more about Annual package difference before accepting any offer based on headline CTC alone.

Always ask HR for the monthly gross and fixed in-hand figures separately.

Missing Employer PF Inside the CTC

Many offer letters show employer PF as a line item within the CTC total.

On a ₹40,000 basic salary, employer PF = ₹4,800/month = ₹57,600/year — sitting inside your ₹12,00,000 CTC but never landing in your bank account. Miss it, and your cash salary calculation is off by nearly ₹58,000 annually. Check the CTC breakup sheet for a line labelled “Employer PF” or “Employer Contribution.”

Treating Variable Pay as Guaranteed Monthly Income

Variable pay — performance bonus, incentive, quarterly allowance — is part of CTC but is conditional and typically not monthly.

If your CTC includes 20% variable pay on a ₹12,00,000 package, your fixed monthly salary is based on only ₹9,60,000 — a ₹24,000/month difference from treating the full CTC as fixed. Build your monthly budget using fixed pay only.

Forgetting State Professional Tax

Professional tax of ₹200/month in states like Maharashtra and Karnataka reduces take-home by ₹2,400 per year. Forgetting it means your monthly calculation is consistently off.

Check your state’s professional tax applicability before finalising any in-hand estimate.

Not Checking Which Tax Regime the Calculator Uses

The old and new income tax regimes can produce monthly TDS differences of ₹5,000–₹15,000 at mid-range CTCs. Many online calculators default to one regime without making it explicit.

Always confirm which regime the calculator uses and check that it matches the regime you have declared to your employer’s payroll team.

Ignoring the Impact of Declarations Not Yet Submitted

If you have not submitted investment proofs, HRA rent receipts or home loan interest certificates to your employer, TDS will be calculated on your full income without those deductions. The monthly in-hand hit is immediate — you recover the excess only when you file your ITR and claim a refund. Submit your proofs early in the financial year to smooth out monthly cash flow.

When This May Not Be the Right Choice

A standard take-home salary calculator India tool may give unreliable or insufficient output in these situations:

Complex salary structures: If your CTC includes ESOPs, restricted stock units, car lease, LTA varying year to year, or reimbursements in lieu of allowances, a basic calculator will miss or incorrectly count them.

Multiple employers in one financial year: If you switched jobs mid-year, your combined taxable income spans both employers’ payrolls. A single-employer calculator will underestimate annual tax — and your monthly TDS with the new employer may be too low, creating a shortfall at ITR filing.

No investment declarations submitted to employer: If proofs for HRA, 80C, or home loan interest are not submitted, actual monthly TDS will be higher than any calculator assuming full deductions. The in-hand figure will differ until ITR is filed and a refund is processed.

Freelance, consulting or business income alongside salary: Salary calculators are designed for pure salaried employees. If you also earn from freelancing or rental income, your total tax liability will differ significantly from any salary-only estimate.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Salary deductions in India are governed by rules that change with each Budget and regulatory update. Before making any financial decisions based on calculator output or the illustrative figures in this article, verify the following directly from official sources:

- Income Tax Department (incometax.gov.in): Current income tax slabs for salaried employees, standard deduction applicable for the financial year, Section 192 TDS rules for employer deduction, new vs old tax regime thresholds, and rebate under Section 87A.

- EPFO (epfindia.gov.in): Current employee and employer PF contribution rates, the PF wage ceiling for mandatory contributions, and EPS contribution rules.

- State government professional tax portals: Professional tax slabs and income thresholds vary by state and can change. For state-by-state details, use the Professional tax impact guide as a starting reference, then verify directly with your state authority.

- Your employer’s HR or payroll team: Your exact salary breakup, PF deduction policy, variable pay structure, and any employer-specific deductions that no generic calculator can capture.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before accepting any offer, ask HR for two documents in writing: the detailed monthly salary breakup showing fixed and variable components separately, and the expected monthly in-hand figure. These two documents eliminate all ambiguity around the headline CTC.

- If your basic salary is above ₹15,000 per month, confirm whether your employer deducts employee PF on your actual basic or on the statutory PF wage ceiling. The difference can be ₹3,000–₹5,000 per month in take-home at mid-level packages — and most generic calculators assume the ceiling, not actual basic.

- Run your expected salary through both the old and new tax regime before the financial year starts. Submit your regime declaration to HR early — you can only switch regimes at ITR filing, not mid-year through payroll. Getting this decision right at the start avoids over-deduction for the entire year.

- If you are joining a new employer mid-year and have received income from a previous employer, submit the previous employer’s Form 16 Part A or TDS certificate to your new HR/payroll team. Without it, your new employer calculates TDS as if you earned nothing before joining — leading to a large underpayment that you will owe when filing your ITR.

- When negotiating a salary hike, ask for the revised fixed monthly gross, not the CTC percentage increase. A 15% CTC hike concentrated in variable pay, insurance premium top-ups or gratuity accrual may produce a negligible increase in your actual monthly bank credit.

- Save your salary slips from each month — either download PDFs from your HR portal or forward payslip emails to a dedicated folder. Banks, landlords and loan providers frequently ask for the last three months of salary slips, and HR portals do not always archive them indefinitely.

Frequently Asked Questions

Is CTC divided by 12 the same as my monthly salary?

No. CTC divided by 12 gives your monthly CTC equivalent, not your in-hand salary. Employer PF, gratuity provision, and other non-cash benefits are inside CTC but are not credited to your bank account. After removing these employer-side items and deducting employee PF, professional tax, and income tax TDS, the actual monthly bank credit is typically 70–85% of the monthly CTC equivalent — often ₹10,000–₹25,000 lower in mid-range packages.

What is the difference between gross salary and net salary in India?

Gross salary is your monthly pay before any employee-side deductions — it appears at the top of your payslip as the total earnings figure. Net salary (also called in-hand or take-home salary) is what remains after deducting employee PF, professional tax, and income tax TDS. Net salary is the amount credited to your bank account each month.

Does employer PF contribution reduce my in-hand salary?

Not directly on your payslip — employer PF is deposited to your EPF account on your behalf, not deducted from your monthly gross. However, if employer PF is included inside your CTC (which is common), it reduces the cash gross available for your monthly pay. The indirect effect is a lower annual gross salary than your CTC headline suggests. Employee PF, by contrast, is directly deducted from your monthly gross salary.

Can a take-home salary calculator India tool give me my exact monthly salary?

No — it gives an estimate, not an exact figure. The precise number depends on your employer’s specific salary structure, PF deduction policy, your state’s professional tax, the tax declarations you have submitted, which tax regime your employer is computing TDS under, and any mid-year changes. Your payslip or HR payroll system is the only source of your exact monthly bank credit.

Why is professional tax deducted from my salary?

Professional tax is a state-level employment tax levied under each state’s own legislation. States such as Maharashtra, Karnataka, West Bengal and Andhra Pradesh charge it on salaried employees — typically ₹200 per month in most income brackets, up to a maximum of ₹2,400 per year. States such as Delhi, Rajasthan and Haryana do not levy professional tax. Where it applies, deduction is mandatory and the employer remits it to the state government.

What happens if I do not submit investment declarations to my employer?

If you do not submit proofs for HRA, 80C investments, home loan interest, or other deductions, your employer computes TDS on your full taxable income without those deductions. Monthly TDS is higher, and your in-hand pay lower. You can claim a refund when filing your ITR, but the monthly cash impact is immediate throughout the year. Submitting declarations and proofs early avoids systematic over-deduction.

Is variable pay included in monthly in-hand salary calculations?

Variable pay is part of your CTC but is typically not paid monthly. It may be disbursed quarterly, half-yearly, or annually — and usually only on meeting performance targets. If your CTC has a significant variable component, your fixed monthly in-hand will be materially lower than CTC ÷ 12. For budgeting, recurring expenses and EMI planning, use only your fixed monthly in-hand figure.

What is Section 192 TDS on salary?

Section 192 of the Income Tax Act requires your employer to deduct income tax at source from your salary each month. The monthly TDS amount is calculated by estimating your total annual taxable income based on your salary and declarations, computing the annual tax liability using the applicable slabs and regime, and spreading it evenly across 12 months. The current slab rates, standard deduction amount, and rebate thresholds for Section 192 must be verified at incometax.gov.in for the relevant financial year before relying on any estimate.

Why do two colleagues with the same CTC receive different in-hand salaries?

Several factors create this difference: different basic pay percentages (higher basic means higher PF deduction), different tax regimes declared, different investment proof submissions, different HRA exemption eligibility based on city of residence, and different variable pay realisation timing. Even within the same company and grade, salary breakup design can produce meaningfully different monthly bank credits from identical CTC figures.

Final Verdict

A take-home salary calculator India tool is one of the most practically useful resources a salaried employee has — especially at offer evaluation, appraisal time, or before committing to a large EMI. But it is an estimate, not a guarantee. Your actual monthly bank credit depends on your employer’s salary structure, your state’s professional tax, the PF deduction policy, your tax declarations, and the current financial year’s regime rules.

Use the calculator to understand the broad range of your in-hand pay. Then verify every component — basic pay, employer PF, variable pay, HRA — with your actual salary breakup from HR. Comparing offers? Ignore CTC headlines and compare fixed monthly gross instead. Your financial planning deserves the real number, not the headline.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Sanya Malhotra writes about everyday personal finance for Indian individuals and families. Her content focuses on budgeting, saving, emergency funds, debt control, net worth tracking, family money decisions, and practical habits that help readers manage money with more confidence.

She covers topics such as monthly budgeting, expense planning, saving habits, emergency fund behaviour, debt repayment, household financial planning, family discussions about money, financial mistakes, net worth tracking, short-term vs long-term goals, and beginner personal finance concepts.

Sanya’s writing style is warm, simple, and realistic. She avoids making personal finance feel intimidating and instead explains money decisions through relatable Indian examples, ₹ budgets, checklists, and step-by-step frameworks. Her articles are useful for students, freshers, couples, parents, and families who want to improve daily money habits. Her content is educational and does not provide personalised financial advice. Readers should adapt examples to their own income, family responsibilities, city, debt level, risk comfort, and financial goals.