Most salaried employees know they should have an emergency fund — but very few can name the exact rupee amount they need. An emergency fund calculator gives you a practical way to arrive at a specific target based on your actual essential monthly expenses, not your salary. Job loss, a sudden medical bill, a delayed salary, or a family emergency can drain your account fast. If your backup plan is a credit card limit or a call to a relative, you are exposed. This article gives you a step-by-step calculation method, realistic Indian examples across three household types, and a clear guide to where to keep your emergency money so it is safe, accessible, and actually useful when you need it.

Quick Answer: Emergency Fund Calculator

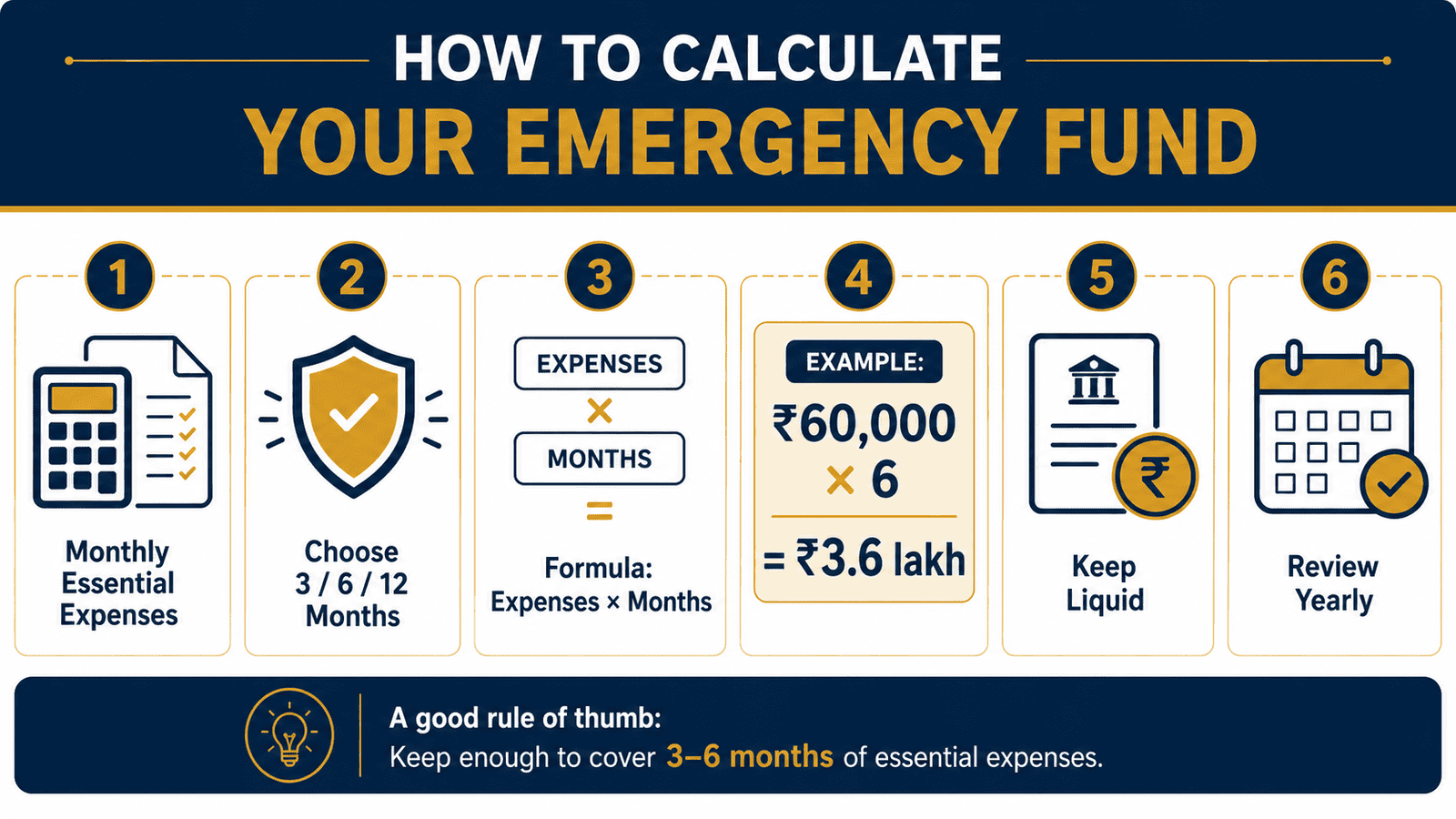

An emergency fund calculator helps you estimate backup money by multiplying monthly essential expenses by 3, 6, 9 or 12 months. For example, if your rent, EMI, groceries, insurance and bills total ₹60,000 per month, a 6-month emergency fund target is ₹3.6 lakh.

How to Calculate Your Emergency Fund: Step-by-Step

The calculation itself is simple. The part most readers get wrong is the base figure — what counts as an essential monthly expense. Work through these five steps before setting your target.

- Step 1: List your essential monthly expenses. Include rent or home loan EMI, groceries, utilities (electricity, water, gas, broadband), health and term insurance premiums, school or tuition fees, regular medicines, basic transport, and all loan EMIs. These are costs that continue even when your income stops.

- Step 2: Remove avoidable lifestyle expenses. Eating out, OTT subscriptions, gym memberships, vacations, and discretionary shopping can all be paused during an emergency. Do not include these in your base figure.

- Step 3: Choose your target months. Use 3 months for stable, low-risk households. Use 6 months as the standard benchmark for most salaried earners. Use 9–12 months if your income is variable, your sector is volatile, or you have dependants with significant medical needs.

- Step 4: Multiply to get your target. Apply the formula below to your essential expense total.

- Step 5: Split into two layers. Keep 1 month’s worth in a savings account for instant access. Park the remaining amount in a sweep-in FD or short-term FD (3–6 months) for better returns without sacrificing quick access.

Emergency Fund Target = Monthly Essential Expenses × Number of Months

Here is how the target changes at three common essential expense levels:

| Monthly Essential Expenses | 3-Month Target | 6-Month Target |

|---|---|---|

| ₹40,000 | ₹1,20,000 | ₹2,40,000 |

| ₹60,000 | ₹1,80,000 | ₹3,60,000 |

| ₹1,00,000 | ₹3,00,000 | ₹6,00,000 |

A household with ₹1,00,000 in essential monthly expenses targeting a 12-month buffer would need to keep ₹12,00,000 in liquid form. That is a significant opportunity cost — which is why matching your target months to your actual risk level is important, rather than defaulting to the highest number.

Key Takeaways

- Base your emergency fund on essential monthly expenses — not your full salary or total lifestyle spending. Two people earning ₹90,000 can have very different emergency fund targets depending on their EMI, dependants, and fixed costs.

- 6 months is a useful benchmark but not a universal rule. A dual-income couple with no EMI may manage on 3–4 months; a sole earner with a home loan and two children likely needs 9 months or more.

- EMIs must be included in your calculation. Missing a home loan or personal loan EMI during a job loss creates credit score damage and late charges on top of income stress.

- Emergency money must stay liquid and low-risk. Equity funds, long-term FDs with premature withdrawal penalties, or locked PPF cannot serve as your primary safety net.

- Split the fund into layers: 1 month in a regular savings account for instant access, the remainder in a sweep-in FD or short-term FD.

- Review your emergency fund every time your salary, EMI load, or family responsibilities change significantly — not just once a year.

Key Facts at a Glance

| Parameter | Detail | Notes |

|---|---|---|

| Formula | Monthly essential expenses × 3, 6, 9, or 12 | Based on expenses, not salary |

| Low-risk households | 3–4 months | Stable job, no EMI, dual income, no dependants |

| Moderate-risk households | 6 months | Single income, 1–2 dependants, home loan EMI |

| High-risk households | 9–12 months | Sole earner, volatile industry, variable income, health dependants |

| Where to keep it | Savings account + sweep-in FD or short-term FD | RBI-regulated bank deposits; check current rates at rbi.org.in |

| What not to use it for | Vacations, gadgets, SIP top-ups, planned upgrades | Replenish immediately after any withdrawal |

| Review frequency | Annually, or after any major life event | Salary change, new EMI, marriage, child, relocation |

Emergency money kept in a savings account earns modest but accessible interest. For a full explanation of how banks calculate this, see our guide on bank savings basics.

What Is an Emergency Fund and What Should It Cover?

An emergency fund is money kept in a separate, accessible account specifically for unexpected financial shocks — not for planned purchases, not for investments, and not for routine bills. Think of it as your financial firewall: it absorbs a sudden hit so the rest of your financial life does not collapse around it.

The phrase gets used loosely, but what qualifies as an emergency is specific. Job loss. A medical procedure not covered by insurance. A sudden car or appliance repair. A family member needing urgent financial support. An unexpected relocation. These events disrupt income or create an unavoidable large expense without warning.

What to Include in Your Monthly Essential Expenses

These are the costs that cannot reasonably be paused, renegotiated, or reduced during a financial crisis:

- Rent or home loan EMI

- Groceries and household staples

- Electricity, water, gas, and broadband

- Health insurance and term life insurance premiums

- School fees or tuition fees for dependants

- Regular medicines and medical costs for dependants

- Essential transport — fuel, metro pass, or auto commute

- All active loan EMIs (vehicle loan, personal loan)

What to Leave Out

These expenses can be reduced or cut entirely during a difficult stretch, so they should not inflate your emergency fund target:

- Eating out and food delivery orders

- OTT and streaming subscriptions

- Gym, spa, and personal care services

- Vacations and weekend travel

- Shopping for clothes, gadgets, or home decor

- Vehicle upgrades and discretionary servicing

This distinction matters more than most readers realise. A salaried employee earning ₹95,000 per month after tax might spend ₹72,000 in total. But if their essential-only costs come to ₹52,000, the emergency fund target is built on ₹52,000 — not ₹72,000 or ₹95,000. The difference between a 6-month target of ₹3,12,000 versus ₹4,32,000 is ₹1,20,000: real money that could be invested instead.

Why Salary Is the Wrong Base

Two people earning ₹80,000 per month can have entirely different emergency fund needs. A single person renting in Bengaluru with no EMI and no dependants has a fundamentally lower risk profile than a sole earner in Nagpur supporting a spouse, two school-going children, and an elderly parent with regular medical costs. Basing the emergency fund on salary misses this completely — and leads most people to either over-save (keeping too much idle) or under-save (leaving themselves exposed).

Why an Emergency Fund Is Not the Same as Savings

Regular savings accounts, equity investments, and long-term deposits serve different purposes. An emergency fund has one priority: immediate access without penalty or volatility. A 5-year FD or an equity mutual fund that fell 25% during a market downturn cannot serve as your safety net in the same month you lost your job.

According to RBI guidelines, deposits at scheduled commercial banks are covered by DICGC insurance up to a specified limit per depositor per bank — making bank deposits a comparatively safer choice for emergency money than market-linked instruments. Always verify the current coverage limit directly at rbi.org.in before making decisions.

The Opportunity Cost Trade-off

A common objection: “Why keep ₹4 lakh idle in a low-yield account?” The answer is that opportunity cost here is a deliberate, conscious choice — you are purchasing access, safety, and stability. If a ₹3,60,000 emergency fund earns 3.5% in a savings account instead of 12% in equity, the approximate annual difference is around ₹30,600. That is the annual cost of financial security for your household. In any year when your income actually stops, that trade-off is clearly worth it.

The first step in any emergency fund calculation is accurately estimating your essential monthly expenses. For a practical breakdown of how to separate essential from discretionary spending using Indian household numbers, see the monthly budget rule guide.

Real Example: Three Indian Households

The emergency fund target changes significantly across different household profiles. Here are three realistic examples.

Profile 1 — Rohit, 31, Pune, IT employee, ₹95,000/month after tax (single, no EMI)

Rohit’s essential expenses: rent ₹18,000, groceries ₹8,000, utilities ₹3,500, health insurance ₹2,500, transport ₹4,500. Monthly essential total: ₹36,500. At 6 months, his target is ₹2,19,000. His sector is stable and he has no dependants. A 3–4 month fund of ₹1,09,500–₹1,46,000 may be adequate, freeing up the rest for long-term investments.

Profile 2 — Priya and Sandeep, 35 and 37, Chennai, dual income with home loan EMI

Combined essential expenses: home loan EMI ₹32,000, groceries ₹13,000, school fees ₹8,000, utilities ₹5,000, insurance premiums ₹5,500, transport ₹5,000. Monthly essential total: ₹68,500. With two incomes, a 4–5 month target of ₹2,74,000–₹3,42,500 is reasonable. However, the home loan EMI means going below 4 months creates real risk if either income is interrupted.

Profile 3 — Kavya, 34, Hyderabad, freelance content consultant, variable income

Essential expenses total ₹44,000 per month. Income fluctuates between ₹40,000 and ₹1,20,000 depending on client work. A 9–12 month buffer is appropriate. Minimum target: ₹3,96,000. Preferred target: ₹5,28,000. Variable income earners face the highest probability of an income gap — and the least ability to time it.

Comparison: 3-Month vs 6-Month vs 9-Month vs 12-Month Emergency Fund

For a household with ₹60,000 in monthly essential expenses, here is how the four most common targets compare. For more on using FDs as a second storage layer, see our detailed guide on fixed deposit safety.

| Fund Target | Best For / Risk Level | Amount at ₹60,000/Month |

|---|---|---|

| 3 Months | Low Risk Stable government or large-company job, dual income, no EMI, no dependants | ₹1,80,000 |

| 6 Months | Moderate Risk Single income, home loan EMI, 1–2 dependants, private sector employment | ₹3,60,000 |

| 9 Months | Higher Risk Sole earner, volatile industry, family medical dependants, sector facing layoffs | ₹5,40,000 |

| 12 Months | High Risk Freelancer or self-employed, highly variable income, large family responsibility | ₹7,20,000 |

According to RBI guidelines, DICGC deposit insurance covers deposits at regulated banks up to a specified limit per depositor per institution. A household whose 12-month emergency fund exceeds this limit may want to consider spreading the amount across two separate banks to stay within the insured threshold. Verify the current limit at rbi.org.in before deciding.

How to Decide What’s Right for You

Use this risk framework to find the right target for your household. Once you have set your target, a sweep-in FD can help you earn FD-like interest while keeping your emergency money accessible without a full premature withdrawal process.

| Risk Profile | Key Characteristics | Suggested Target |

|---|---|---|

| Low Risk | Stable employer, dual income, no EMI, no dependants | 3–4 months |

| Moderate Risk | Single income, home loan EMI, 1–2 dependants, private sector | 6 months |

| High Risk | Sole earner, variable income, volatile sector, health dependants | 9–12 months |

You have a stable government or large-company job, a working partner, and no outstanding EMI — THEN a 3-month emergency fund is likely sufficient as a starting point, and you can prioritise investing beyond that.

You are a sole earner with a home loan EMI and one or two dependants — THEN build to at least 6 months of essential expenses before meaningfully increasing long-term investments.

You work in a startup, contract role, or a sector where layoffs have happened recently — THEN 9 months is a safer floor, even if it takes 18–24 months of systematic saving to get there.

You or a close dependant has a chronic health condition generating unpredictable medical costs — THEN add a separate buffer of 3–6 months of estimated medical expenses on top of your regular emergency fund target.

You have no health insurance at all — THEN treat your emergency fund as partially covering potential medical costs too, and do not go below 9 months until adequate coverage is in place.

Your income is stable, your essential expenses are low relative to income, and you have a partner earning independently — THEN do not over-build your emergency fund at the cost of long-term wealth creation. A 3-month buffer may free up meaningful capital for SIPs each month.

Common Mistakes to Avoid

Treating Your Credit Card Limit as an Emergency Fund

A credit card limit is not your money — it is borrowed money at very high interest if not repaid in full within the cycle.

Relying on a ₹1.5 lakh credit limit during a job loss means immediately taking on high-interest debt at a time when income has already stopped. That compounds the problem significantly rather than solving it.

Build a separate cash emergency fund that does not depend on repayment capacity.

Investing Emergency Money in Equity or Equity Mutual Funds

Equity markets can fall sharply during economic downturns — precisely when emergencies like job losses are most likely to occur.

A ₹3,60,000 emergency fund invested in equity could drop to ₹2,52,000 or less during a market fall, exactly when you need to redeem it. SEBI consistently categorises equity as a long-term wealth tool, not a safety vehicle. Refer to SEBI’s investor awareness materials at sebi.gov.in for more on risk classification.

Keep emergency money in savings accounts or short-term FDs only.

Locking All Emergency Money in Long-Term FDs

A 3-year or 5-year FD offers higher interest — but premature withdrawal typically attracts a penalty and can involve a processing delay of 1–2 business days.

During a real emergency, the last thing you need is a penalty calculation, a branch visit, and a waiting period before funds are available.

Use short-term FDs of 3–6 months or sweep-in FDs that allow partial withdrawals quickly and without significant penalty.

Forgetting Annual Lump-Sum Expenses in Your Monthly Base

Health insurance renewals, school annual fees, and vehicle insurance premiums often arrive as annual one-time payments.

If your health insurance renewal costs ₹18,000 per year, that adds ₹1,500 per month to your essential expense base for emergency fund calculation purposes. Divide all annual fixed costs by 12 and include them in your monthly figure. Ignoring this creates a gap exactly when you can least afford it.

Run a quick annual expense audit and add the monthly equivalent to your base.

Using the Emergency Fund for Lifestyle Purchases

A holiday, a new phone upgrade, or a home renovation is not a financial emergency — even if it feels urgent in the moment.

Using ₹80,000 from a ₹3,60,000 emergency fund for a vacation reduces your 6-month buffer to 4.7 months overnight. If an actual emergency follows within a few months, you are exposed.

Set a separate short-term savings goal for large planned expenses instead of touching the emergency fund.

Not Replenishing After a Genuine Emergency

The most commonly overlooked mistake: spending from the fund when needed — which is correct — and then never rebuilding it.

If a ₹3,60,000 fund drops to ₹1,20,000 after a medical emergency, the urgency to replenish it is equal to the urgency that originally built it. Set up an automatic monthly transfer to rebuild before resuming any increase in other investments.

When This May Not Be the Right Choice

A standard 3–6 month emergency fund target is not the right starting point for every household. Consider adjusting your approach if any of these scenarios apply:

You are carrying high-interest debt. Personal loans at 18–24% or credit card revolving balances at high interest rates can cost more per month than the safety value of a large emergency fund. In this case, maintaining a smaller 1–2 month buffer while aggressively clearing high-interest debt may be more effective than building a full 6-month fund first. Read more at fund before investing.

Your income is extremely variable. Freelancers or consultants whose income fluctuates by more than 50% month to month may need to blend the emergency fund concept with a working capital buffer rather than treating them as separate buckets.

You already hold large liquid assets. If you have a substantial amount in a savings account or short-term deposits already, building a formal emergency fund separately may be redundant. The key is ensuring the money is accessible, not duplicated.

A voluntary job change is planned within 6 months. The income gap of a planned transition requires its own separate planning beyond a standard emergency fund, especially if there will be a notice period or onboarding delay.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Emergency fund planning involves banking products, interest income taxation, and sometimes investment instruments — all governed by official regulatory bodies. Do not rely on articles, aggregator sites, or informal sources for current rates and rules. Verify directly:

- RBI (rbi.org.in) — savings account interest rate regulations, FD rules, DICGC deposit insurance coverage limits, and guidelines for regulated banking institutions.

- SEBI (sebi.gov.in) — investor education resources, mutual fund risk classification, and guidance on short-term debt instruments for retail investors.

- Income Tax Department (incometax.gov.in) — interest income from savings accounts and FDs is taxable under applicable Indian income tax slabs. TDS may be deducted at source by banks on FD interest above a threshold. Check current slab rates, TDS rules, and Section 80TTA deduction details here.

- Your bank’s official website — current savings account rates, FD rates, premature withdrawal penalty terms, and sweep-in FD features vary by institution and can change at any time.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Build in two layers from day one. Open a dedicated savings account at a separate bank for your emergency fund. As soon as the balance crosses 1 month’s essential expenses, move the excess into a sweep-in FD or a 3–6 month FD. This gives you instant access to the first layer while the second layer earns more.

- Keep it in a separate account, ideally at a separate bank. Mixing emergency money with your salary account makes it mentally easy to spend on non-emergencies. A separate account — particularly at a different bank — adds enough friction to protect the fund from casual withdrawal.

- Automate the build-up, then redirect. Set a standing instruction to transfer a fixed amount — even ₹5,000 or ₹8,000 per month — to the emergency account every salary credit. Once the target is met, redirect that same amount to a SIP or recurring deposit. Do not just stop the transfer; redirect it with intention.

- Review after every major life change. A salary hike, a new EMI, marriage, a new child, relocation to a higher-cost city, or loss of a second income all affect your essential expense base. A ₹3,60,000 fund built for ₹60,000 in monthly expenses becomes insufficient if expenses grow to ₹78,000 after a home loan starts.

- Do not count EPF as your emergency fund. EPF withdrawal involves eligibility conditions, application processing time, and tax implications depending on your years of contribution. It is not a reliable instant-access tool for a job loss situation in month one.

- Include annual expenses in your monthly base. Divide all annual fixed costs — insurance renewals, school fees, vehicle insurance — by 12 and add to your essential expense figure before calculating your target. For practical steps to use alongside your emergency fund if you do face a job loss, read our guide on job loss planning.

Frequently Asked Questions

How much emergency fund is enough in India?

For most salaried employees, 3–6 months of essential monthly expenses is a practical starting range. The right figure depends on your job stability, number of dependants, EMI obligations, whether you have a second household income, and your industry’s layoff risk. There is no universal amount — a person with ₹40,000 in monthly essential costs needs a fundamentally different fund than someone with ₹1,00,000 in essential obligations.

Is a 3-month emergency fund enough?

It can be, for the right household. If you are in a stable government or large-company role, have a dual-income household, carry no EMI, and have no dependants with significant medical needs, 3 months may be sufficient. For most single-income households with a home loan and school-going children, 3 months is a starting point, not a destination. Build to 6 months as soon as your income allows.

Should the emergency fund be kept in an FD or a savings account?

Both have a role, and the optimal approach uses both. Keep roughly 1 month’s essential expenses in a regular savings account for immediate same-day or next-day access. Keep the remaining amount in a sweep-in FD or a short-term (3–6 month) FD at a regulated bank. This earns more than a savings account while still allowing access within 1–2 business days. Avoid long-term FDs for this purpose because premature withdrawal penalties and processing delays can slow access at the worst possible moment. Verify current rates and terms with your specific bank.

Can I use mutual funds for my emergency fund?

Liquid mutual funds are sometimes suggested because they earn more than savings accounts. However, they carry NAV risk, redemptions typically take 1–2 business days, and short-term market stress can affect their value at the exact time you need to withdraw. SEBI classifies liquid funds as low-risk, not no-risk. If you use them at all, restrict them to the second layer of your emergency fund — never the first. Keep at least 1–2 months in a savings account or sweep-in FD for true instant access.

Should EMI be included when calculating the emergency fund?

Yes, absolutely. Your home loan EMI, personal loan EMI, and vehicle loan EMI must continue even if your income stops. Missing EMIs creates late payment charges, credit score damage, and in some cases legal escalation from the lender. Include every active EMI obligation in your monthly essential expense base before calculating your target.

Should I build an emergency fund before starting SIPs?

In most cases, yes — at least a basic 1–3 month buffer should be in place before you begin aggressive SIP investing. Without it, a sudden large expense may force you to redeem equity investments at a loss or take a high-interest personal loan. Once a basic buffer exists, you can run SIP contributions and emergency fund contributions simultaneously each month until both targets are met.

What happens to emergency fund interest in terms of taxation?

Interest earned from savings accounts and FDs is taxable as income in India. For non-senior citizens, savings account interest up to ₹10,000 per year is currently deductible under Section 80TTA. FD interest is fully taxable at your applicable slab rate, and banks may deduct TDS above a threshold. Verify the current limits, TDS rules, and deduction eligibility at incometax.gov.in before filing.

What should I do if I have to use my emergency fund?

Use it — that is exactly what it is for. The priority immediately after is to replenish it as quickly as possible. Once the emergency is resolved and income is stable again, restart your automatic monthly transfer and rebuild the fund before resuming or increasing other investments. Treat rebuilding the emergency fund with the same urgency as building it in the first place.

Final Verdict

The emergency fund calculator is straightforward: multiply your monthly essential expenses by 3, 6, 9, or 12, depending on your actual risk profile. If the full target feels overwhelming, start with a 1-month goal — then build steadily through an automatic monthly transfer. Most stable salaried readers should aim for a 3–6 month emergency fund before scaling up long-term investments. Single earners with EMIs, dependants, or variable income should target 9–12 months. Keep the money in a savings account plus sweep-in FD combination: safe, liquid, and earning reasonable interest. Never mix it with daily spending, never use it for planned purchases, and revisit the target every time your expenses or income change meaningfully. Use an emergency fund calculator to revisit your specific rupee target annually. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Meera Iyer writes about banking, fixed deposits, recurring deposits, savings accounts, emergency funds, senior citizen deposits, and safe cash management for Indian readers. Her work is especially useful for families, retirees, conservative savers, and beginners who want to understand where to keep short-term or low-risk money.

She covers topics such as FD meaning, FD calculator, RD calculator, FD vs RD, simple interest vs compound interest, savings account interest, sweep-in FD, premature FD withdrawal, senior citizen FD rules, TDS on FD interest, Form 15G, Form 15H, joint account rules, zero balance accounts, minimum balance charges, small finance bank FDs, post office FD vs bank FD, and emergency fund planning.

Meera’s content focuses on safety, liquidity, taxation, and practical decision-making. She avoids hype and explains both benefits and limitations of banking products. Since deposit interest rates, TDS rules, penalty charges, DICGC coverage, and bank policies can change, readers should always confirm the latest details from their bank, RBI, DICGC, India Post, or relevant official sources before making decisions.