If you are a freelancer in India — whether you design for clients, write code, consult for startups, or take on project-based work — your tax situation is fundamentally different from a salaried employee. No employer calculates your tax. No Form 16 lands in your inbox. You are responsible for tracking receipts, claiming expenses, paying advance tax, reconciling TDS, and filing the correct ITR form. The good news: income tax for freelancers in India follows a clear, repeatable workflow once you understand the structure. This guide walks you through every step, from classifying your income correctly to choosing between normal books and presumptive taxation under Section 44ADA.

Quick Answer: Income Tax for Freelancers in India

Income tax for freelancers in India applies to freelance receipts treated as business or professional income. Freelancers must calculate net taxable income, choose normal books or eligible presumptive taxation, adjust TDS, pay advance tax if liability exceeds ₹10,000, and file the correct ITR form.

Key Takeaways

- Freelance income is usually reported under “Profits and Gains from Business or Profession” — not under the salary head — which changes how you calculate and file tax.

- You will file either ITR-3 or ITR-4 Sugam depending on whether you maintain full books or opt for the presumptive taxation route under Section 44ADA.

- Under Section 44ADA, eligible professionals can declare a fixed percentage of gross receipts as taxable income instead of maintaining detailed expense records — subject to receipt limits and profession eligibility.

- TDS deducted by your clients under Section 194J is not the end of your tax obligation — you must still reconcile it in your ITR and pay any remaining tax liability.

- If your estimated annual tax liability after TDS credit exceeds ₹10,000, advance tax instalments are required across four due dates during the financial year.

- GST registration and filing are entirely separate from income tax — your GST turnover threshold and service type determine whether GST applies to your practice.

- Business expenses such as laptop depreciation, internet costs, software subscriptions, and coworking fees may be deductible under the normal taxation route — but only if they are genuinely incurred for your freelance work and properly documented.

Key Facts at a Glance

| Parameter | What Applies to Freelancers | Where to Verify |

|---|---|---|

| Income head | Profits and Gains from Business or Profession | incometax.gov.in |

| ITR form | ITR-3 (full books) or ITR-4 Sugam (presumptive, if eligible) | eportal.incometax.gov.in |

| Presumptive scheme | Section 44ADA — eligible professionals, subject to receipt limit | incometax.gov.in |

| TDS deducted by clients | Section 194J — check Form 26AS and AIS for credits | eportal.incometax.gov.in |

| Advance tax trigger | Tax liability after TDS credit exceeds ₹10,000 in the year | incometax.gov.in |

| GST registration | Separate check based on turnover and service type — see GST registration rules | gst.gov.in |

| Filing due date | Typically 31 July for non-audit cases (verify each assessment year) | incometax.gov.in |

How Income Tax for Freelancers in India Actually Works

What Counts as Freelance Income

Freelance income covers client payments, retainer fees, project-based consulting, platform payouts (Upwork, Toptal, Fiverr), professional service charges, and overseas receipts credited to your Indian bank account. It also includes income from domestic companies that hire you on contract.

The critical point: this is almost never “salary income” in the tax sense. You have no employer-employee relationship, no Form 16, and no TDS deducted at source under Section 192. Instead, clients typically deduct TDS under Section 194J — the section that covers professional and technical fees.

The Correct Income Head: Profits and Gains from Business or Profession

Under the Income Tax Act, your freelance receipts fall under the head “Profits and Gains from Business or Profession” (PGBP). This matters because the PGBP head has its own rules for deductions, ITR form selection, and tax computation — rules that are more flexible than the salary head in some ways, and more demanding in others.

As a freelancer, you are not an employee receiving a fixed salary. You earn variable receipts from multiple payers. The tax law recognises this and provides specific provisions — including the presumptive taxation scheme — to make compliance manageable for individual professionals. Learn more about how the 44ADA freelancer rules apply to eligible professions before deciding your route.

Normal Taxation: Gross Receipts Minus Eligible Expenses

Under the normal route, your taxable professional income equals gross receipts minus eligible business expenses. Eligible expenses include: laptop depreciation, internet and mobile bills (the professional use proportion), software subscriptions, coworking space fees, domain and hosting costs, professional development courses, and any other expense genuinely incurred to earn your freelance income.

You must maintain books of account for this route. Receipts, invoices, and payment records are not optional — they are your evidence if the tax department questions a deduction.

Presumptive Taxation: Section 44ADA

Section 44ADA was introduced to reduce compliance burden for individual professionals in specified fields — which include legal, medical, engineering, architecture, accountancy, technical consultancy, and interior decoration, among others. Freelance designers, writers, developers, and consultants may also fall within the “other notified profession” category, but eligibility must be confirmed for your specific profession.

Under Section 44ADA, if your gross receipts are within the prescribed limit, you can declare a fixed percentage of your gross receipts as your taxable income — without needing to document individual expenses. You are not required to maintain detailed books of account under this route, which significantly simplifies annual compliance.

However, Section 44ADA is not universally better. If your actual expenses are high — say your coworking, software, and equipment costs represent a large share of receipts — the normal route with actual books may result in lower taxable income than the presumptive percentage. Run a comparison before you commit each year.

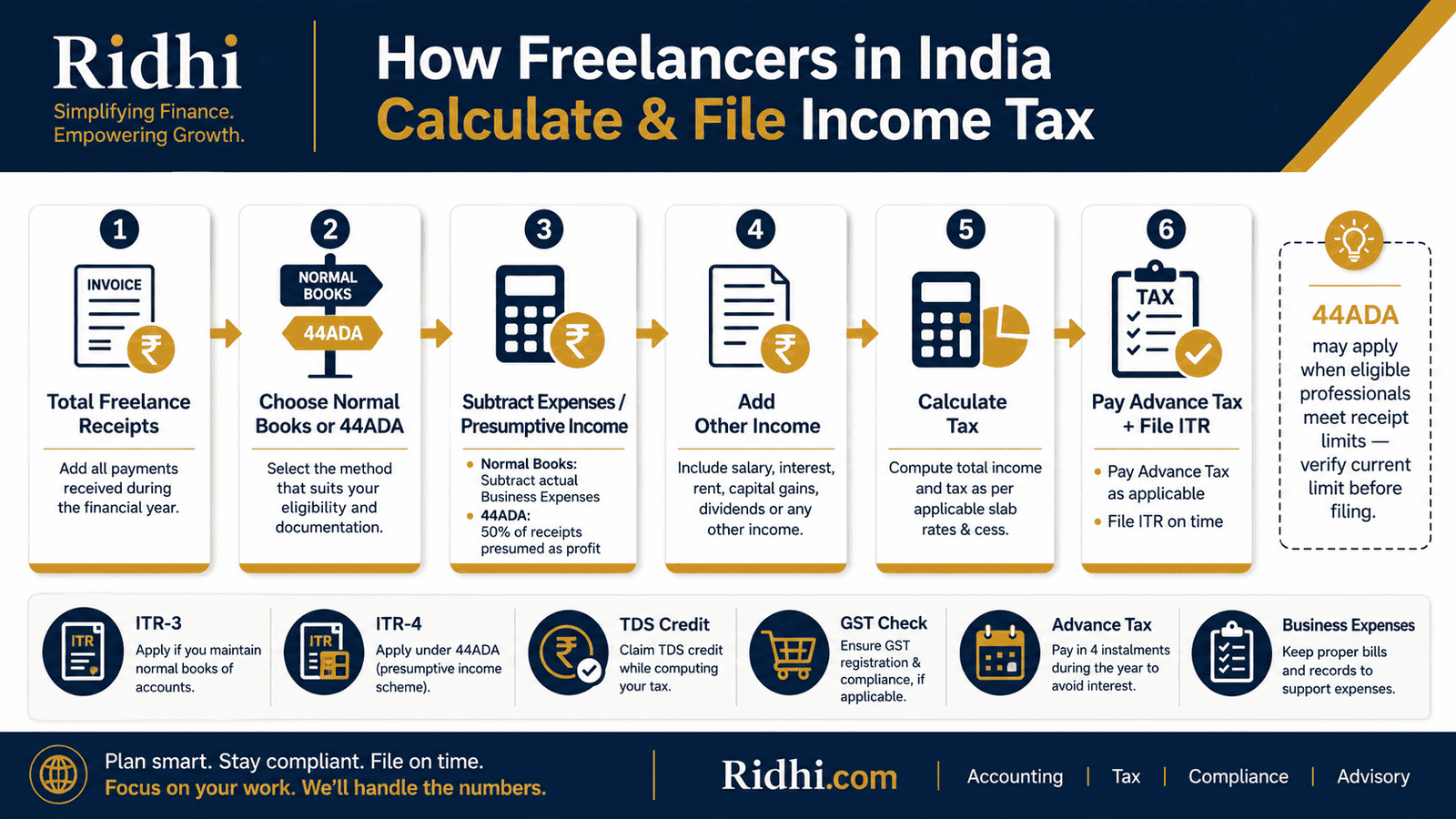

ITR Form Selection

Freelancers file either ITR-3 or ITR-4 Sugam. ITR-4 Sugam is available to individuals who opt for the presumptive taxation scheme under Section 44ADA and meet the eligibility conditions — including the receipt limit. ITR-3 is for freelancers who maintain regular books of account, have income from multiple heads, or are not eligible for the presumptive route. Filing the wrong form is a common mistake — verify which form applies to your situation on the Income Tax e-filing portal before each assessment year.

Real Example: Riya’s Freelance Tax Workflow

Riya, 29, Bengaluru, freelance UI designer, collected ₹12,00,000 in total receipts during the financial year from four Indian clients and two overseas clients. Her Indian clients deducted ₹72,000 as TDS under Section 194J across the year. Her overseas clients paid directly to her bank account — no TDS deducted at source.

Normal books route: Riya adds up all receipts — ₹12,00,000. She documents ₹2,40,000 in eligible business expenses: ₹60,000 laptop depreciation, ₹36,000 coworking fees, ₹24,000 software subscriptions, ₹48,000 internet and phone (professional proportion), ₹72,000 in other project-related costs. Net professional income: ₹9,60,000.

Presumptive route (if eligible): If Riya qualifies under Section 44ADA and her receipts are within the prescribed limit, she could declare the prescribed percentage of ₹12,00,000 as taxable income — which in this case would be higher than her actual net income of ₹9,60,000. That means the normal route saves her more tax in this scenario.

She checks her freelance TDS credit on Form 26AS and AIS to confirm ₹72,000 appears against her PAN. This TDS is deducted from her final tax payable — but she still needs to file an ITR, and she must separately verify whether her overseas receipts crossed the GST registration threshold.

Key insight: TDS deducted by clients reduces the cash you owe at filing time — it does not mean your tax obligation is complete or that filing can be skipped.

How to Calculate Your Freelancer Tax

Normal route: Taxable professional income = Gross receipts − Eligible business expenses

Presumptive route (if eligible under 44ADA): Taxable income = Gross receipts × Prescribed percentage

Here is a simplified five-step framework:

Step 1 — Add all receipts. Sum every rupee received from all clients and platforms during the financial year, including overseas credits. Use your bank statements and invoices, not just TDS certificates.

Step 2 — Choose your computation route. Either subtract eligible documented business expenses (normal route) or apply the presumptive percentage if you qualify under Section 44ADA.

Step 3 — Add other income. Include savings account interest, fixed deposit interest, capital gains from mutual funds or shares, and any rental income. These are added to your professional income to arrive at total taxable income.

Step 4 — Apply deductions and regime rules. Under the old tax regime, deductions such as Section 80C (up to ₹1.5 lakh) and 80D (health insurance) can reduce taxable income further. The new tax regime offers lower slab rates but removes most deductions. Choose the regime that produces lower tax — and verify current slab rates for the applicable assessment year. For a deeper look at allowable costs, see deductible business expenses before finalising your numbers.

Step 5 — Subtract TDS and advance tax paid. Your gross tax liability minus TDS already deducted by clients and advance tax already deposited gives you the net amount payable or refundable.

| Scenario | Key Inputs | Indicative Taxable Income |

|---|---|---|

| Normal books, high expenses | ₹12,00,000 receipts, ₹2,40,000 expenses | ₹9,60,000 (before deductions) |

| Presumptive 44ADA (if eligible) | ₹12,00,000 receipts, prescribed % applied | Verify current % at incometax.gov.in |

| Normal books, low expenses | ₹12,00,000 receipts, ₹80,000 expenses | ₹11,20,000 (before deductions) |

Comparison: Normal Taxation vs Section 44ADA Presumptive Taxation

| Parameter | Normal Books Route | Section 44ADA Presumptive Route |

|---|---|---|

| Eligible for | All freelancers and professionals | Eligible professions only |

| Taxable income basis | Gross receipts minus actual expenses | Fixed % of gross receipts |

| Books of account | Required | Not required |

| Expense documentation | Required for each claim | Not required |

| ITR form | ITR-3 | ITR-4 Sugam (if eligible) |

| Receipt limit | No limit under this route | Subject to prescribed annual limit |

| Tax audit risk | If receipts cross audit threshold | Lower risk within receipt limit |

| Best when | Expenses are genuinely high and documented | Expenses are low or documentation is incomplete |

Do not assume one route is always better. Verify current presumptive percentages and receipt limits at incometax.gov.in, and consider consulting a tax professional if your income is high, international, or involves multiple income heads.

How to Decide What’s Right for You

Your profession is explicitly listed as eligible under Section 44ADA and your gross receipts are within the prescribed limit — THEN the presumptive route under ITR-4 Sugam is worth evaluating for its simplicity.

Your documented business expenses (equipment, software, coworking, internet) are high relative to receipts — THEN the normal books route via ITR-3 may produce lower taxable income than the presumptive percentage.

You earn from overseas clients and your receipts cross the GST registration threshold — THEN GST registration and LUT (Letter of Undertaking) filing become a separate compliance task alongside income tax. Read the freelancer ITR filing guide after sorting your GST status.

TDS has been deducted by your clients — THEN always reconcile Form 26AS and your Annual Information Statement before filing, because a mismatch can trigger a notice or delay your refund.

Your estimated net tax liability after TDS credit is likely to exceed ₹10,000 in the financial year — THEN advance tax instalments are required and missing them attracts interest under Sections 234B and 234C.

Your profession is not in the eligible list under Section 44ADA — THEN you cannot file ITR-4 using this scheme, and ITR-3 with normal books is the applicable route.

Common Mistakes to Avoid

Treating Freelance Income as Salary Income

Some freelancers declare payments from clients under the salary head because the money came via a formal contract.

This leads to the wrong ITR form, incorrect deduction claims, and possible notices from the Income Tax Department — since no Form 16 will be issued and no employer TAN matches your PAN.

Classify all project-based and professional receipts under PGBP unless an actual employer-employee relationship exists.

Ignoring TDS Because Money Already Came Net of Deduction

When a client deducts ₹12,000 from your ₹1,20,000 invoice and pays you ₹1,08,000, some freelancers assume the tax obligation is finished.

TDS is only a credit against your final tax liability. You are still required to file an ITR, declare the gross receipt of ₹1,20,000 (not ₹1,08,000), and reconcile the TDS credit. Understating gross receipts is a common audit trigger.

Always check Form 26AS and your AIS to confirm TDS entries match your records before filing.

Claiming Personal Expenses as Business Expenses

Your home internet connection, personal laptop, or phone used partly for personal browsing is not 100% deductible as a business expense.

Overclaiming personal costs inflates your expense deduction, understates taxable income, and can attract scrutiny during assessment. Only the professionally used proportion of mixed-use assets and utilities is deductible — and you need evidence to support that proportion.

Keep separate bills or logbooks where possible.

Forgetting Advance Tax Instalments

Freelancers with irregular income often wait until March or filing season to calculate their tax, then pay everything at once. If your net tax liability exceeds ₹10,000 for the year, advance tax was due in quarterly instalments.

Missing instalments results in interest under Sections 234B and 234C — which can add up to thousands of rupees even when the underlying tax amount is modest. See the full schedule and payment process in the advance tax payments guide.

Start estimating tax after each quarter, not at year-end.

Mixing GST and Income Tax Rules

GST turnover and income tax turnover are calculated differently. GST applies to the value of taxable supplies; income tax applies to net taxable income after expenses and deductions.

Confusing the two leads to incorrect GST registration decisions and wrong income disclosures. Treat them as two parallel but separate compliance tracks.

Check your GST obligation independently each year — it does not automatically follow from your income tax filing status.

Choosing ITR-4 When Not Eligible

ITR-4 Sugam is only available to individuals who are eligible for presumptive taxation under Section 44ADA or Section 44AD and meet all conditions, including the receipt limit.

Filing ITR-4 when you are ineligible — because your receipts exceed the limit, your profession is not covered, or you have income from capital gains — results in a defective return notice.

Verify eligibility on the Income Tax e-filing portal before selecting your ITR form for each assessment year.

When This May Not Be the Right Choice

A general freelancer tax guide covers the standard workflow. But certain situations go beyond what a self-service approach can safely handle:

Foreign income and foreign bank accounts: If you earn from overseas clients, hold a foreign currency account, or need to claim foreign tax credits under a DTAA (Double Taxation Avoidance Agreement), the filing becomes significantly more complex — additional schedules, FEMA compliance, and potentially Schedule FA (Foreign Assets) requirements may apply.

High receipts crossing audit thresholds: If your gross receipts exceed the tax audit threshold under Section 44AB, a Chartered Accountant must conduct and certify your audit before you file. This is not optional.

Mixed income — salary plus freelancing plus capital gains: Multiple income heads with different rules, different TDS sections, and potentially different tax regimes interact in ways that are easy to miscalculate without professional help.

Registered business structure: If you have already incorporated an LLP or Pvt Ltd, the company — not you as an individual — is the taxable entity, and this guide does not apply.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Freelancer tax rules in India change with each Budget and CBDT circular. The figures used in this guide reflect rules as understood at the time of writing — but income tax slabs, Section 44ADA receipt limits, advance tax thresholds, TDS rates, and ITR form eligibility must be verified for the current assessment year before you file.

Use these official sources:

- Income Tax Department — incometax.gov.in (rules, circulars, slab rates, Section 44ADA text)

- Income Tax e-Filing Portal — eportal.incometax.gov.in (ITR forms, AIS, Form 26AS, advance tax payment)

- GST Portal — gst.gov.in (registration, return filing, LUT for exports)

- CBIC — cbic.gov.in (GST notifications, legal context for service classification)

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Open a dedicated bank account for freelance receipts. Mixing personal and professional inflows makes it nearly impossible to reconstruct annual receipts accurately come filing season — and a clean account statement is your first line of defence if questioned.

- Raise numbered invoices for every payment. Even if a client does not ask for one, your invoice is proof of the receipt date, the amount, and the nature of the service. This directly supports your PGBP computation and GST records if applicable.

- Track TDS client-by-client. Download your Form 26AS and Annual Information Statement from the e-filing portal every quarter — not just before filing. TDS mismatches are far easier to resolve when flagged early, rather than on 30 July.

- Save expense proofs monthly, not annually. A software subscription charged on your card in May is easy to document in May. Reconstructing 12 months of costs in July is error-prone and stressful. A simple monthly folder (physical or cloud) works.

- Estimate your advance tax liability after each quarter. Add up receipts received, deduct documented expenses or apply the presumptive percentage, apply the current slab, subtract TDS already credited. If the number exceeds ₹10,000, a quarterly instalment is due. Do this in June, September, and December — not in March.

- Reconcile AIS and Form 26AS before filing. Your Annual Information Statement now shows income reported by banks, platforms, and clients. If a receipt appears in AIS but not in your ITR, expect a notice. Fix mismatches before you submit.

- Do not wait for the last week of July to file. The e-filing portal slows significantly in the final days before the deadline. Filing in the first two weeks of July gives you time to fix errors without late fees.

Frequently Asked Questions

Do freelancers need to file an ITR in India?

Yes. If your gross total income exceeds the basic exemption limit for the assessment year, or if TDS has been deducted on your payments, filing an ITR is required. Even if your income is below the exemption limit, filing is advisable to claim any TDS refund. Verify the current exemption limits for your chosen tax regime at incometax.gov.in.

Which ITR form should a freelancer use?

Most freelancers use either ITR-3 or ITR-4 Sugam. ITR-4 is available if you opt for presumptive taxation under Section 44ADA and meet all eligibility conditions including the receipt limit. If you maintain full books, have income from capital gains, or are not eligible for presumptive taxation, ITR-3 applies. Verify form eligibility on the e-filing portal before filing each year.

Can freelancers claim laptop and internet expenses as tax deductions?

Under the normal taxation route (not the presumptive route), yes — but only the proportion used for professional work. A laptop used exclusively for client projects can be claimed as a depreciating asset. Internet bills are deductible to the extent used professionally. Keep bills and usage records. Under the presumptive route (Section 44ADA), individual expense claims are not made — the presumptive percentage already accounts for them.

What is Section 44ADA and who qualifies?

Section 44ADA is a presumptive taxation scheme for specified individual professionals — including those in legal, medical, engineering, architecture, accountancy, technical consultancy, interior decoration, and certain other notified professions. If eligible, you can declare a fixed percentage of gross receipts as taxable income without maintaining detailed books, provided receipts are within the prescribed annual limit. Verify current limits and the list of eligible professions at incometax.gov.in.

Is GST mandatory for all freelancers in India?

Not automatically. GST registration is required if your taxable turnover exceeds the prescribed threshold in a financial year, or if you supply services to overseas clients (export of services) — even if turnover is lower, in some cases. The threshold and applicable categories depend on your state and service type. Check your obligation separately at gst.gov.in. GST is a completely separate compliance track from income tax.

What if a client has already deducted TDS from my payment?

TDS deducted under Section 194J by your client appears in your Form 26AS and Annual Information Statement. This amount is a credit against your final income tax liability — it is not extra tax paid. You must still file an ITR, declare the full gross receipt (before TDS deduction), and claim the TDS credit. If TDS exceeds your total tax liability, the difference is your refund.

Do freelancers have to pay advance tax?

Yes, if your estimated net tax liability (after TDS credit) for the financial year exceeds ₹10,000. Advance tax is payable in four instalments across the year — typically by 15 June, 15 September, 15 December, and 15 March. Missing instalments attracts interest under Sections 234B and 234C. Verify current due dates and instalment percentages at incometax.gov.in before each financial year.

Is income earned from foreign freelance clients taxable in India?

Yes. If you are a resident of India for tax purposes, your global income — including payments from overseas clients — is taxable in India. The fact that the money was received in foreign currency or into an Indian bank account does not change your tax obligation. You may be able to claim relief under a Double Taxation Avoidance Agreement if tax was also deducted in the client’s country, but this requires specific documentation and schedule filings in your ITR.

Can I switch between normal taxation and Section 44ADA every year?

There are restrictions on opting out of the presumptive scheme once opted in — specific rules apply under Section 44ADA regarding how many years you must continue after opting out. Verify current switch-out rules at incometax.gov.in or consult a tax professional before changing your route mid-stream.

What happens if I file the wrong ITR form?

The Income Tax Department may issue a defective return notice, requiring you to file a revised or fresh return in the correct form. Filing in the wrong form can also lead to mismatch issues with TDS credits and deductions. Always verify which form applies to your situation for the specific assessment year before submitting.

Final Verdict

Income tax for freelancers in India becomes manageable once you separate the workflow into its components: classify your income correctly under PGBP, decide between normal books and the Section 44ADA presumptive route based on your actual expenses and profession eligibility, reconcile TDS credits from Form 26AS, pay advance tax if your net liability crosses the threshold, and file the correct ITR form by the due date. None of these steps is inherently complex — but each one must be done in the right order and based on verified current rules.

Section 44ADA can meaningfully simplify compliance for eligible professionals, but it is not universally the better option — especially if your documented expenses are high. GST is a parallel obligation that must be assessed separately. Use the freelancer ITR filing guide as your next step once you have worked through the calculation. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Amit Verma writes about money management for Indian freelancers, consultants, creators, professionals, and self-employed workers. His content focuses on income planning, tax basics, GST awareness, cash flow, invoicing, business expenses, and financial stability for people who do not receive a fixed monthly salary.

He covers topics such as Section 44ADA, presumptive taxation, professional income, advance tax, GST basics, TDS for freelancers, invoice planning, business expense tracking, ITR filing for self-employed professionals, emergency funds, health insurance, retirement planning, and irregular income management.

Amit’s writing is practical, relatable, and built around the realities of independent work. He understands that freelancers often deal with delayed payments, uneven income, unclear tax deductions, missing employer benefits, and uncertainty around compliance. His guides help readers organise their financial life better, but they are educational and not a substitute for professional advice. Since tax rules, GST limits, filing requirements, and deduction treatment can change, readers should verify current rules from official sources or consult a qualified professional.