If you spotted NPS on your CTC letter or offer document and wondered what it actually does to your salary — you are not alone. Most salaried employees see “employer NPS contribution” in their pay structure without knowing whether it saves tax, cuts their take-home pay, or simply locks money away until retirement. The confusion is understandable: NPS in salary works differently from EPF, and the tax treatment changes depending on who contributes, which tax regime you are in, and what your employer’s payroll policy says.

This article breaks down exactly how NPS in salary works — the employer contribution angle, the Section 80CCD(2) deduction, the impact on your CTC and monthly in-hand pay, and what withdrawal restrictions mean for your money in practice. By the end, you will know whether the NPS in your salary structure is genuinely working in your favour.

Quick Answer: What Is NPS in Salary?

NPS in salary means your employer contributes to your National Pension System account as part of your CTC. It can reduce taxable salary through Section 80CCD(2), subject to employer type and percentage limits, while withdrawal rules usually split retirement corpus into lump sum and annuity portions. The tax benefit available to you differs depending on whether you are in the old or new tax regime.

Key Takeaways

- Employer NPS contribution is usually part of your CTC — it may reduce your monthly in-hand salary rather than add to it.

- Section 80CCD(2) allows a deduction on employer NPS contribution — up to 10% of basic salary for private sector employees and up to 14% for central government employees.

- Unlike most salary deductions, the Section 80CCD(2) benefit is available even under the new tax regime — making it one of the few deductions that crosses both regimes.

- Employee-side NPS deductions under Section 80CCD(1) and 80CCD(1B) are available only under the old tax regime.

- At retirement, a minimum of 40% of your corpus must be used to purchase an annuity — you cannot withdraw the full amount as a lump sum.

- NPS is market-linked and regulated by PFRDA — it is not the same as EPF and carries different risks and restrictions.

Key Facts at a Glance

| Parameter | Detail |

|---|---|

| Full form | National Pension System |

| Regulatory authority | PFRDA — Pension Fund Regulatory and Development Authority |

| Account identifier | PRAN — Permanent Retirement Account Number |

| Who contributes (employer-linked) | Employer (defined percentage), employee (optional additional contribution) |

| Where it appears | CTC letter, salary slip, Form 16 Part B, tax declaration portal |

| Employer contribution deduction | Section 80CCD(2) — available in both old and new tax regime |

| Employer limit — private sector | Up to 10% of basic salary |

| Employer limit — central government | Up to 14% of basic salary |

| Employee contribution deduction | Section 80CCD(1) — within ₹1.5L overall 80C ceiling; old regime only |

| Additional employee deduction | Section 80CCD(1B) — up to ₹50,000 over 80C limit; old regime only |

| Retirement withdrawal (at age 60) | Up to 60% lump sum tax-free; minimum 40% must purchase annuity |

| Account types | Tier 1 (mandatory, retirement lock-in) and Tier 2 (voluntary, no lock-in, no tax benefit for private sector) |

To understand how NPS fits into your complete pay structure, see our guide on salary slip components and deductions.

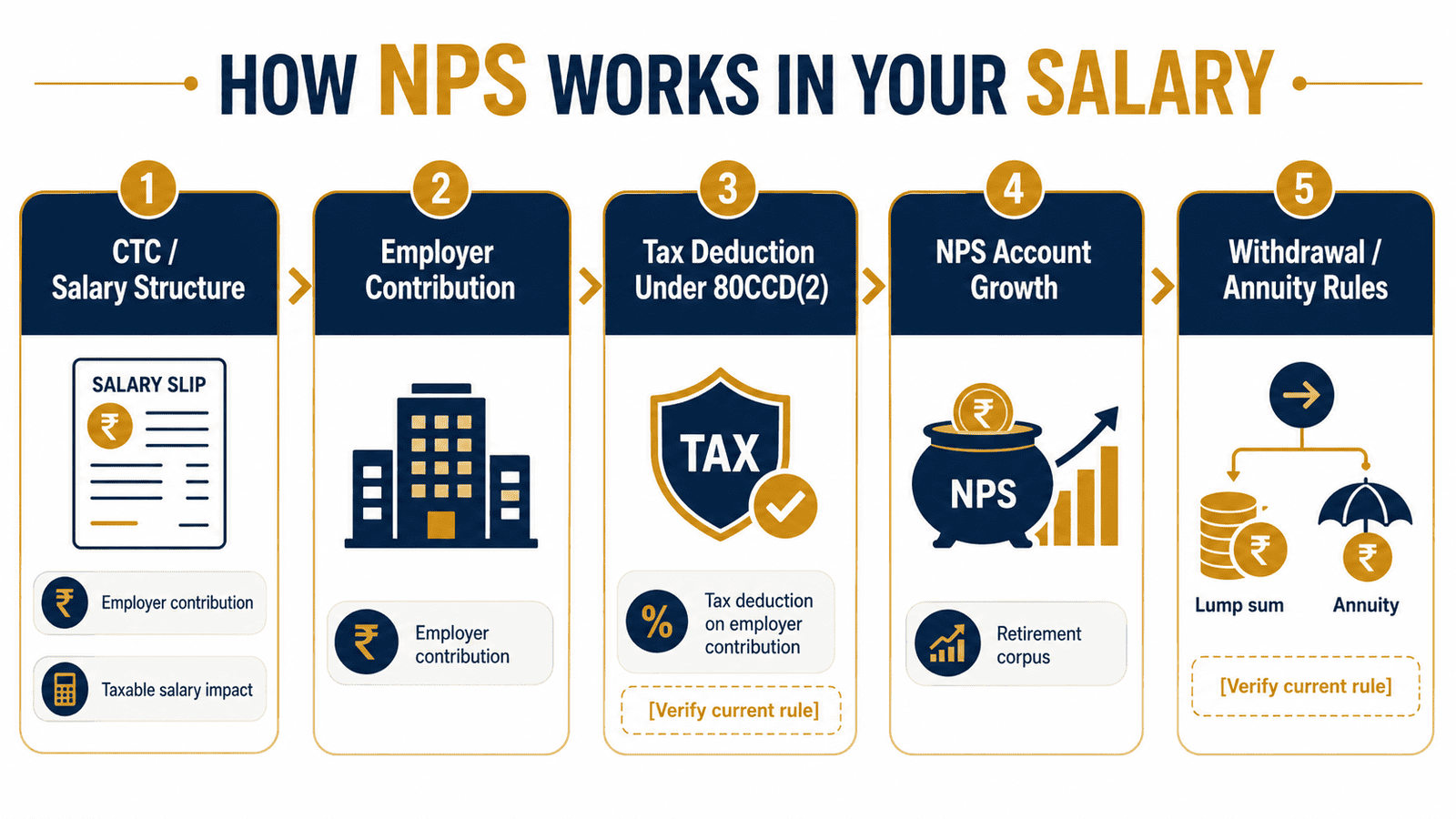

How NPS in Salary Actually Works for Salaried Employees

What the National Pension System Is — and Who Regulates It

The National Pension System is a government-backed, market-linked retirement scheme regulated by PFRDA under the PFRDA Act, 2013. Every subscriber gets a Permanent Retirement Account Number — a unique identifier that stays with you throughout your working life, regardless of how many times you change jobs.

The scheme has two account types. Tier 1 is the primary retirement account with a defined lock-in — it is the account that appears in employer-linked salary structures. Tier 2 is a voluntary savings account with no lock-in, but it carries no tax benefit for most private sector employees. When NPS appears on your payslip or CTC breakup, it almost always refers to Tier 1 contributions.

Employer-Linked NPS vs Opening NPS on Your Own

You can open an NPS account independently through a Point of Presence (any registered bank or financial institution). But employer-linked NPS is different in a meaningful way. Your company registers a corporate NPS account and routes contributions directly through payroll. The employer contributes a percentage of your basic salary into your Tier 1 account before the money ever reaches you.

This pre-salary routing matters because the employer’s contribution is handled under Section 80CCD(2) — which gives it different tax treatment compared to anything you invest personally. Personal NPS requires you to invest yourself and claim the deduction at ITR time. Employer NPS happens automatically and shows up in Form 16.

How the Three NPS Deduction Sections Work — and Where They Differ

Section 80CCD(1) — Your Own NPS Contribution

If you contribute to NPS from your salary, Section 80CCD(1) allows a deduction of up to 10% of your basic salary. The catch: this deduction falls inside the overall ₹1.5 lakh ceiling shared by Section 80C and 80CCC. If your EPF, life insurance, and ELSS already fill that space, your own NPS contribution adds no additional deduction. This section is available only under the old tax regime.

Section 80CCD(1B) — The ₹50,000 Bonus Deduction

Section 80CCD(1B) is separate from 80C entirely. It allows an additional deduction of up to ₹50,000 for your own NPS contributions — on top of the ₹1.5 lakh 80C limit. If you are in the 30% tax bracket, this alone can save up to ₹15,600 per year. However, this benefit is available only under the old tax regime.

For a full breakdown of this section, see our guide on the Section 80CCD(1B) extra NPS deduction.

Section 80CCD(2) — The Employer Contribution Advantage

This is the most valuable part of employer-linked NPS — and it works in both tax regimes. When your employer contributes to your NPS account, that contribution is deductible from your gross taxable salary under Section 80CCD(2). According to the Income Tax Department (incometax.gov.in), this employer contribution is not treated as a taxable perquisite — you do not pay income tax on it in the year it is contributed.

For private sector employees, the deduction is available up to 10% of basic salary. For central government employees, the limit is 14% of basic salary. This deduction is over and above the ₹1.5 lakh 80C limit — and unlike almost every other salary deduction, it is available under the new tax regime as well.

That combination — tax efficiency in both regimes, no 80C ceiling impact, and retirement accumulation — is why employer NPS is often the more strategically important part of the NPS-in-salary conversation.

For a broader overview of NPS as a product, see our guide on the National Pension System meaning and benefits.

Real Example: Rohan’s NPS and CTC Breakup

Rohan is 32, a software engineer at a Bengaluru tech firm, earning ₹18 lakh total CTC. His basic salary is ₹7,20,000 per year (₹60,000 per month) — 40% of CTC, which is typical in Indian IT payroll structures.

His employer’s NPS contribution is 10% of basic: ₹72,000 per year, or ₹6,000 per month. This ₹72,000 is inside the ₹18 lakh CTC — it is not extra salary on top. The remaining cash components total ₹16,08,000 after accounting for NPS and EPF. So Rohan’s monthly in-hand pay is lower than a colleague earning ₹18 lakh with no NPS component.

The tax benefit: Rohan’s taxable salary reduces by ₹72,000 under Section 80CCD(2). If he is in the 20% slab, he saves ₹14,400 in income tax per year. If he falls in the 30% slab, the saving is ₹21,600. The ₹6,000 per month is simultaneously building a retirement corpus — not disappearing.

The key insight: NPS inside CTC reduces take-home pay today but builds a retirement asset that the tax system partly subsidises through the Section 80CCD(2) deduction.

See our complete guide on CTC vs in-hand salary differences to understand how components like NPS shift the pay structure.

How to Calculate Employer NPS Contribution and Tax Impact

Annual Employer NPS Contribution = Basic Salary × Employer Contribution Rate

Using Rohan’s numbers: ₹7,20,000 × 10% = ₹72,000 per year

Annual Tax Saving = Employer NPS Contribution × Your Tax Slab Rate

At 20% slab: ₹72,000 × 20% = ₹14,400 saved per year. At 30% slab: ₹72,000 × 30% = ₹21,600 saved per year.

For a retirement corpus estimate: if ₹6,000 per month is contributed from age 32 to retirement at 60 (28 years) and earns an assumed 8% annual return, the accumulated amount from the employer’s contribution alone could reach approximately ₹75 lakh. This is an illustrative number only — NPS returns are market-linked and not guaranteed.

| Scenario | Key Inputs | Estimated Annual Tax Saving |

|---|---|---|

| 20% tax slab | Basic ₹7.2L, employer NPS 10% = ₹72,000/year | ₹14,400 |

| 30% tax slab | Basic ₹7.2L, employer NPS 10% = ₹72,000/year | ₹21,600 |

| Higher basic salary | Basic ₹10L, employer NPS 10% = ₹1,00,000/year | ₹20,000–₹31,200 |

To estimate your own retirement corpus from monthly NPS contributions, use our NPS retirement corpus calculator. NPS investments are subject to market risks. Corpus figures are illustrative and not guaranteed.

Comparison: Old Regime vs New Regime — NPS Tax Benefits

| NPS Deduction Type | Old Tax Regime | New Tax Regime |

|---|---|---|

| Employee contribution — Section 80CCD(1) | Available — up to 10% of basic, within ₹1.5L 80C ceiling | Not Available |

| Extra employee deduction — Section 80CCD(1B) | Available — up to ₹50,000 above 80C limit | Not Available |

| Employer contribution — Section 80CCD(2) | Available — up to 10% of basic (private) / 14% (central govt) | Available — same limits apply |

| Lump sum withdrawal at retirement (up to 60%) | Tax-free | Tax-free |

| Annuity income after retirement | Taxable at slab rate at time of receipt | Taxable at slab rate at time of receipt |

| Maximum combined NPS benefit | ₹1.5L (80C) + ₹50,000 (80CCD 1B) + employer contribution | Employer contribution under 80CCD(2) only |

For a full breakdown of which deductions apply to your salary under each regime, see our old vs new tax regime comparison.

How to Decide What’s Right for You

Your employer contributes to NPS above and beyond your existing CTC — not by reallocating existing salary components — THEN it is almost certainly a net benefit: you receive retirement allocation plus a Section 80CCD(2) deduction at no cost to your current in-hand pay.

Your employer NPS contribution is carved from your fixed salary components such as basic or special allowance — THEN your monthly in-hand pay will be lower. Compare the take-home reduction against the actual tax saving at your slab rate before deciding whether to accept or restructure.

You are under the new tax regime — THEN only the employer’s Section 80CCD(2) deduction gives you a tax advantage through NPS. Your own additional contributions will not reduce taxable income. Check whether the employer deduction alone justifies staying enrolled.

You are under the old tax regime and have not filled your ₹1.5 lakh 80C limit — THEN your own NPS contribution under 80CCD(1) can fill that space first, before you consider the additional ₹50,000 under 80CCD(1B).

You already have substantial EPF, PPF, and equity SIPs for retirement — THEN additional NPS may be redundant unless the employer’s Section 80CCD(2) deduction gives you a tax advantage you are currently not capturing.

You are comfortable locking money until age 60 and accepting that at least 40% of the corpus must be used for annuity purchase — THEN NPS Tier 1 may not suit your liquidity needs. A combination of EPF and equity mutual funds may offer retirement growth with more flexibility.

If you want to understand how additional employee-side NPS contributions can stack on top of employer NPS, see our guide on the Section 80CCD(1B) deduction.

Common Mistakes to Avoid

Assuming Employer NPS Is Free Extra Salary

Many employees assume the employer NPS contribution is an add-on above their total pay.

In most corporate payroll structures it is allocated inside the CTC. An ₹18 lakh CTC with ₹72,000 employer NPS means your cash components total ₹17.28 lakh — not ₹18 lakh plus NPS. Accepting this without checking can leave you short on monthly cash flow by ₹6,000 every month without realising why.

Ask HR directly and in writing whether the NPS contribution is above CTC or within it before accepting the offer.

Confusing Section 80CCD(1B) with Section 80CCD(2)

Section 80CCD(1B) is the employee’s own ₹50,000 additional deduction. Section 80CCD(2) is the employer’s contribution deduction. They are different sections that must be shown in different columns on your tax declaration form.

If your employer’s contribution is incorrectly clubbed into 80C or 80CCD(1B) in your Form 16, the deduction may be applied against the wrong ceiling — and you may lose part of the benefit. This is a common payroll system error that goes unnoticed until ITR filing.

Cross-check Form 16 Part B to confirm each NPS deduction is in the correct section before filing your ITR.

Ignoring Old Regime vs New Regime Impact on NPS Benefits

Switching to the new tax regime removes 80C and 80CCD(1B) entirely. If you had been counting on personal NPS contributions to save ₹50,000 extra tax under 80CCD(1B), that saving disappears the moment you switch regimes — even if your contribution continues.

Recalculate your effective NPS-linked tax benefit every time you evaluate a regime switch. What made sense in the old regime may not hold in the new one.

Focusing Only on the Tax Saving and Ignoring the Lock-In

NPS Tier 1 money cannot be freely accessed before age 60. Partial withdrawals are allowed for specific purposes after 3 years, but only up to 25% of your own contributions — not the total corpus including employer contributions. If your emergency fund is thin, routing significant savings into NPS creates a cash-lock risk during a financial emergency.

Build at least 3–6 months of expenses in liquid instruments before committing large amounts to NPS Tier 1.

Not Verifying Whether Employer NPS Appears Correctly in Form 16

Some payroll systems do not automatically populate the Section 80CCD(2) deduction in Form 16 Part B. If the employer contribution is missing from your Form 16, you may miss the deduction entirely when filing ITR — leaving ₹14,000–₹22,000 in unnecessary tax paid.

Check Form 16 Part B before filing. If the deduction is absent, request a corrected certificate from payroll before the ITR deadline.

When This May Not Be the Right Choice

Employer-linked NPS in salary may be less suitable in a few specific situations.

If your monthly cash flow is already tight and the NPS contribution is carved from your fixed pay, reducing take-home pay further can create real pressure — especially with EMIs, rent, or school fees to manage.

If your employer simply relabels an existing salary component as NPS without increasing total pay, the tax saving may not justify the reduction in liquidity. You are essentially prepaying yourself into a locked retirement account.

If you are in the early stages of your career and expect to change employers frequently, managing NPS portability and ensuring each new employer maps contributions correctly is an additional administrative responsibility that many employees underestimate.

If the annuity requirement — where at least 40% of corpus must be used to buy a pension product at retirement — does not align with your retirement income plan, NPS may not be the right core vehicle for you.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

NPS rules, tax treatment, and withdrawal guidelines are governed by multiple official bodies. Before making any salary structuring or tax decision involving NPS, verify current figures from these sources:

- Income Tax Department — incometax.gov.in: Section 80CCD deduction limits, regime-specific applicability, and ITR filing rules for NPS.

- PFRDA — pfrda.org.in: NPS scheme rules, withdrawal eligibility, annuity purchase requirements, partial withdrawal conditions, and fund manager options.

- Your employer’s HR or payroll team: Confirmation of whether employer NPS is above or inside CTC, and how it is reported in Form 16 Part B.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before signing an offer letter that includes NPS, ask HR one direct question: “Is the employer NPS contribution inside my CTC or above it?” That single answer determines whether NPS is a genuine benefit or a salary reallocation with a retirement tag on it.

- If you are under the new tax regime, confirm that your employer’s NPS contribution is correctly appearing under Section 80CCD(2) in your tax declaration portal — this is the only NPS deduction that works for you under the new regime. Do not let it be reported under the wrong section.

- If you are in the 30% tax bracket under the old regime, contributing an additional ₹50,000 personally under Section 80CCD(1B) — on top of employer NPS — can save ₹15,600 extra per year. Do this before the March 31 deadline if you have unused capacity.

- Check your NPS fund allocation and nominee details at least once a year. Employer contributions flow in automatically, but many employees have never selected their preferred asset class mix and sit in the default option indefinitely.

- If you change jobs, provide your PRAN to the new employer immediately. Gaps in employer contribution mapping are common and can result in months of missed contributions — with no automatic alert from the payroll system.

- Do not assume Tier 2 NPS has the same tax benefit as Tier 1. If your employer sets up a Tier 2 account for flexibility, contributions there do not qualify for Section 80CCD(2) and function like an ordinary savings account for private sector employees.

Frequently Asked Questions

Is NPS employer contribution taxable in the year it is contributed?

No. The employer’s NPS contribution is not taxed in the year it is deposited into your account. It is deductible from your gross taxable salary under Section 80CCD(2). However, the annuity income you receive post-retirement is taxable at your slab rate at that time. The lump sum portion withdrawn at maturity (up to 60% of the corpus) is tax-free.

Is employer NPS contribution part of CTC?

This depends on your employer’s policy. Many companies include it inside the total CTC figure — meaning your cash salary is lower because a portion is routed to NPS. Some employers offer NPS as an additional benefit above CTC. Always get written confirmation from HR before accepting an offer that includes an NPS component.

Is NPS tax benefit available under the new tax regime?

The employer’s contribution deduction under Section 80CCD(2) is available under both the old and new tax regime. However, the employee-side deductions — Section 80CCD(1) and Section 80CCD(1B) — are not available under the new regime. Under the new regime, only the employer’s contribution gives you a tax advantage through NPS.

What is Section 80CCD(2) and how does it work?

Section 80CCD(2) allows salaried employees to claim a deduction for the employer’s NPS contribution from their gross taxable salary. For private sector employees, the limit is up to 10% of basic salary. For central government employees, it is up to 14% of basic salary. This deduction is in addition to the ₹1.5 lakh 80C ceiling and is available in both tax regimes.

Can I withdraw NPS before retirement?

Tier 1 NPS has limited pre-retirement withdrawal options. After completing 3 years as a subscriber, you can withdraw up to 25% of your own contributions for specific purposes — higher education or marriage of children, medical treatment of specific conditions, or purchase or construction of a home. For a premature full exit before age 60, at least 80% of the corpus must be used to purchase an annuity; only 20% can be taken as a lump sum.

What happens to NPS if I resign or change jobs?

Your PRAN is fully portable. When you move to a new employer, the same NPS account continues. You provide your PRAN to the new employer and contributions resume under the new payroll. The accumulated corpus from your previous employer’s contributions stays in your account and continues to be invested per your fund allocation. There is no need to open a new account.

Is NPS better than EPF for retirement savings?

Neither is universally better. EPF offers a fixed, government-declared interest rate and fully liquid withdrawal at retirement. NPS is market-linked, with potentially higher long-run returns, but it requires annuity purchase at exit and has stricter partial withdrawal rules. Most planners suggest treating EPF as the stable base and NPS as the growth layer — using both rather than replacing one with the other.

Can I opt out of employer NPS contribution?

This depends on your employer’s policy. Some companies make NPS mandatory as a pay component. Others allow employees to decline. If declining means the NPS amount is redistributed to your basic or allowances, be aware: you may lose the Section 80CCD(2) deduction in the process, which can increase your taxable income and cost you more in tax than you gain in take-home pay.

What is the difference between Tier 1 and Tier 2 NPS?

Tier 1 is the core retirement account — it has the lock-in, the annuity requirement at exit, and the tax benefits. Tier 2 is a voluntary savings account with no lock-in and no mandatory annuity, but it also carries no tax benefit for private sector employees. Employer-linked NPS in salary structures almost always refers to Tier 1. Tier 2 can be opened separately for flexible savings but does not appear in standard CTC arrangements.

Final Verdict

NPS in salary can be a genuinely valuable retirement planning tool — but only if you understand what it is actually doing to your pay and tax. If your employer contributes to NPS under Section 80CCD(2) and that contribution is a real benefit and not just a salary reallocation, you receive a tax-efficient retirement accumulation that works in both the old and new tax regime. That is rare in Indian salary planning.

The trade-off is real. The lock-in, the annuity purchase requirement, and the market-linked nature of returns mean NPS in salary is a retirement product, not a short-term savings vehicle. It requires a long-horizon mindset and comfort with the withdrawal rules before it makes sense to embrace it fully.

Evaluate your own salary structure, chosen tax regime, and monthly liquidity needs carefully before deciding. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.