You want a credit card that never charges an annual fee. That is a reasonable place to start — but lifetime free credit cards India is a phrase that carries a very specific meaning in banking, and it is narrower than most first-time applicants expect. Zero joining fee and zero annual fee sound like pure upside. The problem is that these are just two of the fifteen-odd charges a credit card can carry.

The moment you carry an unpaid balance, withdraw cash from an ATM, or spend abroad, your “free” card begins generating real costs. A single month of unpaid interest on a ₹20,000 bill can cost more than the annual fee on a standard paid card.

This article does not simply list card names. It explains what lifetime free actually covers, compares card profiles by use case and hidden-cost risk, and gives you a practical framework to evaluate any no-annual-fee card before applying. Issuer terms and card features can change without notice — every figure here should be verified from the official card MITC before you decide.

Quick Answer: Lifetime Free Credit Cards India

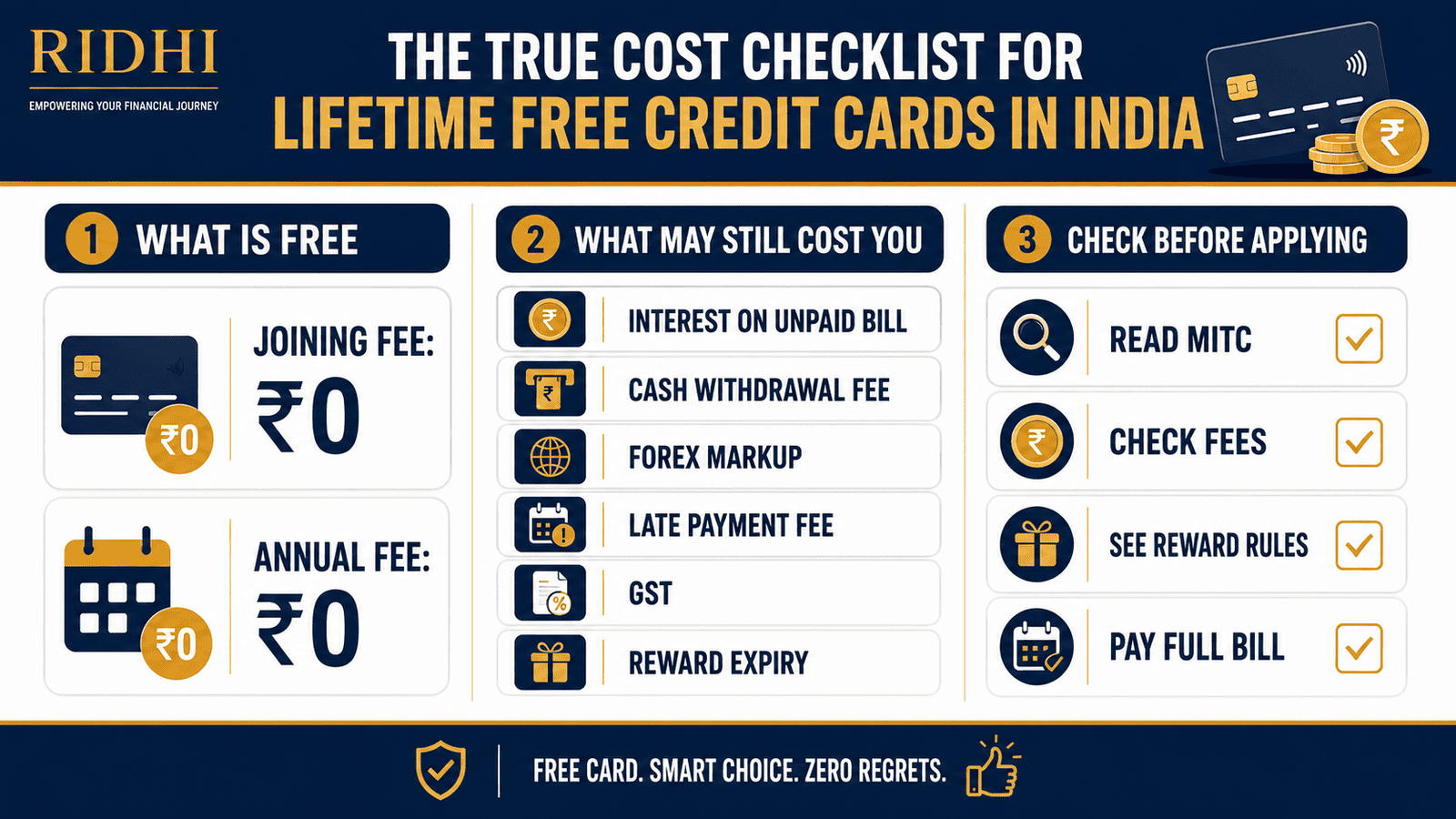

Lifetime free credit cards India usually mean ₹0 joining fee and ₹0 annual fee, not zero charges forever. You may still pay interest, GST, late fees, cash withdrawal charges, forex markup, EMI charges, or reward-related costs. Always read the card MITC before applying.

Key Takeaways

- A ₹0 annual fee typically saves ₹500–₹1,500 per year — but one month of unpaid interest at 3% per month on a ₹20,000 bill adds ₹600 in interest charges alone, before GST.

- Repayment discipline is the only variable that determines whether your lifetime free card is actually free to use — not the fee waiver itself.

- Cash withdrawals on any credit card, including lifetime free ones, attract a cash advance fee of typically around 2.5% of the amount and interest from day one, with no grace period.

- Reward points on no-fee cards often carry lower earn rates, higher redemption minimums, or expiry timelines — check these details in the MITC, not the marketing page.

- Banks can change reward structures, earn rates, and partner benefits on existing cards — re-read your MITC at least once a year to know what your card still offers.

- Using a lifetime free card and paying the full outstanding balance every month can build your CIBIL score at zero annual cost.

- If you are likely to carry a balance even occasionally, a lifetime free card is not automatically cheaper than a paid card — the revolving interest will far exceed any annual fee waiver.

Comparing Lifetime Free Card Profiles: Benefits and Hidden Costs by Use Case

The right no-annual-fee card depends on your spending pattern, not just the headline fee. The table below compares six common card profiles by typical reward model and the specific hidden costs to verify before applying. Any card-specific rate, reward value, or eligibility figure must be confirmed from the issuer’s current MITC and official product page — these details change frequently. For a detailed comparison of reward models across card types, see card reward choices.

| Card Profile / Use Case | Typical Reward Model on LF Cards | Key Hidden Costs to Verify Before Applying |

|---|---|---|

| Beginner / First Credit Card | Basic reward points on all spends; low earn rate (1 point per ₹100–₹150 typically); limited redemption catalogue | Revolving interest rate; late payment fee slabs; minimum credit limit offered; GST on all applicable charges |

| Low-Spend Salaried User (₹25,000–₹50,000/month) | Flat cashback on select categories (1–1.5% typically); monthly cashback cap likely applies | Monthly cashback cap; minimum spend for cashback eligibility; forex markup if used abroad; reward exclusions on fuel or wallet loads |

| Online Shopper | Accelerated rewards or cashback on e-commerce platforms; typically 2–5% on partner sites, lower on others | Lower or no reward on offline spends; reward expiry timeline; redemption minimum; GST on reward adjustments |

| Cashback Seeker | Direct cashback credited to statement; no redemption step; typically 1–2% flat with category exclusions | Cashback exclusions (fuel, EMI, wallet top-ups, government payments); monthly earning cap; revolving interest rate if balance is ever carried |

| Fuel / Daily Commuter | Fuel surcharge waiver at specific petrol stations (typically 1% surcharge waived); may offer fuel points on select networks | Minimum and maximum transaction limits for surcharge waiver; fuel excluded from reward earn on some cards; confirm partner petrol station list |

| Occasional International Traveller | Basic rewards on international spends; a small number of LF cards offer reduced or no forex markup — Verify current forex terms | Forex markup fee (typically 1–3.5% plus GST); dynamic currency conversion charge; cash withdrawal abroad adds a further cash advance fee and interest |

Key Facts at a Glance

| Term | What It Usually Means | What to Check in the MITC |

|---|---|---|

| Lifetime Free | No joining fee and no annual or renewal fee for the life of the card, unconditionally | Whether any condition, spend milestone, or account-type change can trigger a fee later |

| Joining Fee | One-time fee charged when the card is issued; ₹0 on lifetime free cards | Whether a welcome bonus requires minimum spend within 30–60 days to activate |

| Annual / Renewal Fee | Yearly charge for continuing to hold the card; ₹0 on lifetime free cards | Confirm the MITC states no fee — not a waiver conditional on annual spend |

| Interest (Finance Charge) | Charged on any balance not paid in full by due date; typically 3% per month / 36–42% p.a. on many entry-level cards | Exact monthly rate; whether interest compounds; GST applicability; date from which interest accrues |

| Late Payment Fee | Fixed charge if minimum amount due is missed; structured in slabs by outstanding balance | Current slab amounts and GST on the fee — see Schedule of Charges, not the marketing page |

| Cash Advance Fee | Fee for ATM withdrawals using the card; typically 2.5% of the amount (minimum ₹300–₹500) | Minimum fee amount; whether interest also applies from day one with no grace period |

| Forex Markup | Surcharge on international transactions; typically 1.5–3.5% of transaction value plus 18% GST | Exact markup percentage; GST calculation on the markup; dynamic currency conversion risk |

| MITC | Most Important Terms and Conditions — the official document with every charge, limit, and rule | Available on the issuer’s website; read before applying and re-read after any communication from the bank |

What “Lifetime Free” Actually Means — and What It Does Not Cover

The phrase “lifetime free” comes from the credit card marketing playbook. It refers to two specific charges only: the joining fee charged when you receive the card, and the annual or renewal fee charged each year. Both are ₹0 on a lifetime free card. Every other charge the card carries is completely independent of this waiver.

Joining Fee, Annual Fee, and Renewal Fee Are Not the Same Thing

A joining fee is a one-time charge when the card is first issued. An annual fee is charged every year on the card anniversary. A renewal fee is what some issuers call the annual fee in the second year onwards — the terminology differs by bank, but the mechanism is the same.

On a genuine lifetime free card, all three are permanently ₹0 — not waived on a minimum spend condition, not reversed if you cross ₹1 lakh in annual spend, but structurally absent from the card’s fee schedule. This is the meaningful distinction between a “fee waiver” card and a truly lifetime free card. If a card’s annual fee is waived only when you spend a minimum amount per year, that card is not lifetime free — it has a conditional waiver.

If you are applying for your first card and trying to understand which type suits your situation, see our complete beginner framework: first credit card. And before you assume the grace period makes a free card entirely cost-free, understand how that grace period actually works: billing cycle basics — the grace period eliminates interest only if you pay the entire outstanding balance by the due date, not a partial amount.

Why Banks Offer Lifetime Free Cards

Banks do not offer no-fee cards out of generosity. The economics work in other ways. Every card transaction earns the issuer an interchange fee — typically 1–2% paid by the merchant at the point of sale. A card used frequently, even with no annual fee attached, generates consistent revenue through interchange alone.

Banks also use entry-level free cards to build long-term customer relationships. A first-time cardholder who uses the account responsibly for two years becomes a viable candidate for a premium card upgrade, a personal loan, or a home loan pre-approval. The free card is the starting point in a multi-product relationship — not the end goal for the bank.

As a cardholder, this means the lifetime free card is typically designed for lower spend profiles and limited benefit tiers. Premium features — airport lounge access, higher reward earn rates, concierge services, comprehensive travel insurance, and higher credit limits — are generally reserved for paid cards where the annual fee directly funds those benefits.

The Charges That the Fee Waiver Does Not Cover

This is the section most competitor articles skip past. These are the charges that apply on a lifetime free card in exactly the same way they apply on any paid card:

Interest on revolving balance: If you do not pay the full outstanding amount by the due date, interest applies — typically from the individual transaction dates, not from the due date. According to RBI credit card directions, issuers must disclose this rate clearly in the MITC. The annual rate on many entry-level cards ranges from 36% to 42%, though this varies by issuer and must be verified.

Late payment fee: If the minimum amount due is not paid, a late fee is charged in addition to interest — not instead of it. The fee is typically structured in slabs based on the outstanding balance amount.

GST on all charges: Goods and Services Tax at 18% applies to interest charges, late fees, cash advance fees, forex markup fees, and most other applicable charges. Add 18% mentally to any fee figure you see in the Schedule of Charges to estimate the true debit to your account.

Cash advance fee: Withdrawing cash from an ATM using a credit card is not a debit transaction — it is a loan from the bank. A cash advance fee applies immediately, and interest begins from the transaction date with no grace period.

Forex markup: Spending in a foreign currency — whether travelling abroad or shopping on international websites — carries a markup fee of typically 1.5% to 3.5% of the transaction value, plus GST on that markup.

EMI-related charges: Converting a purchase to EMI on a credit card typically carries its own interest rate and sometimes a one-time processing fee per transaction. This applies even on lifetime free cards.

Repayment Behaviour Is the Only Variable That Actually Matters

Every charge listed above — except forex markup — is avoidable with a single habit: pay the full outstanding balance before the due date, every month. Not the minimum amount due. The entire statement balance.

If you do this consistently, your lifetime free card costs ₹0 annually, generates reward value on top, and helps build your credit file. The annual fee waiver is meaningful in this scenario — the card is genuinely free.

If you pay only the minimum, or miss the due date entirely, the interest and fee structure of a credit card will cost significantly more than any annual fee on a standard paid card. The fee waiver offers no protection from these charges — they are identical in mechanism to a paid card.

Real Example: Two Ways Ankit Uses the Same Lifetime Free Card

Ankit Sharma is 28, lives in Bengaluru, and earns ₹85,000 per month as a software engineer. He was approved for a lifetime free credit card with a ₹60,000 credit limit.

Scenario A — Disciplined repayment: Ankit uses the card for groceries, subscriptions, and an online electronics purchase. Monthly spend: ₹22,000. His billing cycle closes and the full amount due is ₹22,000. He pays it in full before the due date. Interest charged: ₹0. Late fee: ₹0. Annual card cost after 12 months: ₹0. He also earned reward points on every transaction.

Scenario B — Partial payment and ATM use: The following month, Ankit pays only ₹5,000 of a ₹20,000 bill and withdraws ₹5,000 in cash from an ATM. The remaining ₹15,000 revolves at the card’s monthly interest rate. The ATM withdrawal generates a cash advance fee on ₹5,000, plus interest from the withdrawal date — no grace period. Add 18% GST on both. In this one month, Ankit has paid more in charges than the annual fee on a standard entry-level paid card.

The ₹0 annual fee is identical in both scenarios. What changes entirely is the cost of Ankit’s repayment behaviour — not the card.

How to Calculate the Real Cost of a “Free” Credit Card

The most significant hidden cost on any lifetime free card is revolving interest on an unpaid balance. The formula is straightforward. Use the credit card interest calculator to run your own scenario, or work through the example below. For a deeper explanation of how this interest is actually calculated on your statement, see: card interest calculation.

Monthly Extra Cost = (Outstanding Balance × Monthly Interest Rate) + GST on Interest + Late Payment Fee + GST on Late Fee

Worked example — illustrative rates only; verify current figures with your issuer before applying:

Outstanding balance: ₹20,000. Example monthly rate: 3% per month (36% p.a.). Month 1 interest: ₹600. GST on interest at 18%: ₹108. Example late payment fee for this balance slab: ₹500. GST on late fee: ₹90. Total extra cost in month 1: ₹1,298.

| Scenario | Key Figures | Month 1 Extra Cost |

|---|---|---|

| Full payment before due date | ₹20,000 paid; zero revolving balance | ₹0 |

| Minimum payment only (no late fee) | ₹19,500 revolving at 3%/month + 18% GST on interest | ≈ ₹690 |

| No payment made (interest + late fee) | ₹20,000 revolving; interest ₹600 + late fee ₹500 + GST on both | ≈ ₹1,298 |

The annual fee waiver on a lifetime free card saves ₹500–₹1,500 per year. A single missed payment on a ₹20,000 bill can generate more than that in one month. The card’s free status is not the variable that determines your cost — your repayment behaviour is.

How to Decide What’s Right for You

You are applying for your first credit card and plan to use it for small monthly purchases under ₹15,000 — a lifetime free card is a practical, zero annual cost way to build a CIBIL score, as long as you pay the full balance every month without exception.

You spend primarily on one category — online shopping, fuel, or groceries — choose the lifetime free card whose reward or cashback model is optimised for that specific category rather than a generic card with broad but shallow rewards across all categories.

Your monthly card spend is under ₹15,000 and you earn under ₹6 lakh per year — a lifetime free cashback card is very likely your most cost-efficient option, since the annual fee on a premium card will not be recovered through benefits at this spend level.

You travel internationally twice or more per year — check the forex markup percentage on any card before selecting it. Some lifetime free cards carry a 3.5% forex markup; a paid card with zero forex markup may cost less in total if international spend is significant.

You spend ₹2 lakh or more per month on your card — a paid premium card may return substantially more in reward value, lounge access, and insurance coverage than its ₹2,000–₹5,000 annual fee. Calculate the net benefit on your actual spend pattern before defaulting to a free card.

You are confident you can pay the full balance every single month — a lifetime free card is not the low-cost choice if you tend to carry balances. Revolving interest will cost you significantly more than any annual fee on a comparable paid card.

You need airport lounge access, travel insurance, or high cashback rates above 2% as regular features — a paid card where the annual fee is justified by these specific benefits will deliver more net value than any lifetime free card currently available as of recent data.

Common Mistakes to Avoid

Assuming Lifetime Free Means All Charges Are Zero

The most common misreading of “lifetime free” is treating it as a blanket cost waiver for everything.

It covers only the joining fee and the annual fee. Interest, GST, cash advance charges, late fees, and forex markup apply on a lifetime free card in exactly the same way as on any paid card — none of these are reduced or waived.

Before applying, download the card’s Schedule of Charges from the issuer’s website and read every line — not just the annual fee row.

Paying Only the Minimum Amount Due

The minimum amount due is typically 5% of the outstanding balance or a fixed floor amount — whichever is higher. It is not a repayment plan.

Paying only the minimum keeps the account current and avoids a late fee, but full revolving interest accumulates on the remaining balance from the individual transaction dates. Over six months on a ₹20,000 unpaid balance, interest charges at 36% p.a. compound to several thousand rupees — far more than any annual fee. Read your statement line by line: card statement lines explains exactly what each entry means.

Set up an auto-payment for the full statement balance where your bank allows it. This eliminates revolving interest risk entirely.

Withdrawing Cash From an ATM Using Your Credit Card

A credit card ATM withdrawal is a cash advance loan, not a debit transaction — even on a lifetime free card.

A cash advance fee of typically 2.5% of the amount withdrawn applies immediately, plus interest begins from the date of withdrawal with no grace period at all. Add 18% GST on the fee. For a full breakdown of why this is one of the most expensive short-term borrowing options available: cash withdrawal charges.

Avoid using any credit card for ATM cash withdrawals except in a genuine emergency with no alternative.

Ignoring GST on Every Applicable Fee

GST at 18% is levied on credit card interest charges, late fees, cash advance fees, and forex markup charges.

If your interest for the month is ₹600, the actual debit to your account is ₹708. If your late fee is ₹500, the debit is ₹590. These amounts appear as separate line items on your credit card statement and are frequently overlooked as small administrative charges.

When estimating any fee from the Schedule of Charges, add 18% to get the true cost.

Choosing a Card Based Entirely on the Welcome Bonus

Welcome bonuses — gift vouchers, cashback on first purchase, reward points credited in the first month — are one-time benefits that expire after 30–90 days.

A welcome bonus worth ₹1,000 is irrelevant to the three-year cost of holding and using a card. Evaluate the ongoing reward rate, category exclusions, redemption conditions, and interest rate before applying — not the launch offer.

Not Re-Reading the MITC After Any Bank Communication

Banks can modify reward programmes, earn rates, partner cashback arrangements, and interest rates — within RBI guidelines — by notifying you by email or SMS in advance.

If you receive any communication about changes to your card’s terms, download the updated MITC immediately and compare it with the version you reviewed at application. Ignoring a reward devaluation notice can mean months of earning at a reduced rate without realising it.

When This May Not Be the Right Choice

A lifetime free credit card is not the optimal choice for every salaried employee, even if the ₹0 annual fee headline is appealing.

If you spend ₹2 lakh or more per month on your card — a premium paid card may return substantially more in reward value, lounge access, and insurance coverage than its annual fee costs. Calculate your net benefit before assuming free is always better.

If you travel internationally frequently — a lifetime free card with a 3% forex markup costs ₹3,000 on every ₹1 lakh of foreign spend, plus GST. A paid card with zero forex markup can be cheaper overall if your international spend is significant.

If you know you will carry a balance in some months — the revolving interest rate on credit cards is high regardless of the annual fee structure. If balance-carrying is likely, explore alternatives: a low-interest personal loan, a salary overdraft facility, or a secured credit card may cost less over time.

If you are likely to overspend simply because “the card is free” — a credit limit that feels costless to access can lead to spending beyond your repayment capacity. If this is a concern, a debit card or a credit card with a lower limit and an annual fee you actively want to justify may work better as a spending discipline.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

The rules governing credit card charges, billing cycles, interest rate disclosure, and consumer protections in India are set and monitored by the Reserve Bank of India. The primary reference is the Master Direction — Credit Card and Debit Card Issuance and Conduct Directions, available at rbi.org.in.

- RBI (rbi.org.in): Consumer protection rules, billing dispute resolution procedures, maximum interest rate disclosure requirements, and credit card conduct guidelines for all regulated issuers.

- Issuer’s official website: The card MITC (Most Important Terms and Conditions) and Schedule of Charges for your specific card variant. These are the only reliable source for current rates, limits, and reward terms.

- Your monthly statement: Every charge, GST line, interest calculation, and reward adjustment is itemised here. Read it in full every month — not just the minimum due line and the payment instruction.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Set up auto-pay for the full statement balance where your bank allows it — this single step eliminates revolving interest risk entirely and keeps your free card genuinely free every month without requiring manual action each billing cycle.

- Keep credit utilisation below 30% of your credit limit — if your lifetime free card has a ₹60,000 limit, try to keep your monthly balance under ₹18,000. High utilisation hurts your CIBIL score even if you pay the full balance on time.

- Redeem reward points before they expire — check the expiry policy in your card’s reward programme terms specifically. Many points lapse after 12–24 months of account inactivity or at a fixed calendar date, often without a prominent reminder.

- Calculate your effective reward rate on your actual monthly spend before applying — if 60% of your spend falls in excluded categories like fuel, rent, EMI, or government payments, your real earn rate may be below 0.5%. A card with a modest annual fee but better category rewards may return more in practice.

- Download and re-read your MITC once a year — banks can and do adjust reward earn rates, partner cashback deals, and redemption thresholds on existing cards. An annual MITC review takes fifteen minutes and can reveal changes that have been affecting your rewards without your knowledge.

- Never treat a ₹0 annual fee as a reason to hold an unused card indefinitely — an inactive card with zero annual fee still affects your credit profile and may be downgraded or closed by the issuer. If you are not using a card, review whether to keep it or close it intentionally.

Frequently Asked Questions

Are lifetime free credit cards in India really free to use?

The joining fee and annual fee are ₹0 — that much is genuinely free. But the card is not free to use if you pay interest, incur a late fee, withdraw cash from an ATM, or spend in a foreign currency. The full Schedule of Charges still applies to every other cost. Always read the MITC before applying, not just the marketing page.

Can a bank add an annual fee to a lifetime free card later?

A genuine lifetime free card should not have an annual fee added mid-tenure. However, issuer terms can change, and some “lifetime free” offers are conditional on account type or product category. If you receive any communication about a fee change, contact the bank’s customer service immediately and retain a copy of the MITC you agreed to at application. Verify the card’s fee-free status directly with the issuer before applying.

Do lifetime free credit cards charge interest?

Yes. The annual fee and the interest rate are entirely separate. If you do not pay the full outstanding balance by the due date, interest applies to the remaining balance at the card’s revolving rate — typically 36–42% p.a. on many entry-level cards, though this varies by issuer and must be confirmed from the MITC. The annual fee waiver does not reduce or delay this interest charge in any way.

Is a no annual fee credit card good for building a CIBIL score?

Yes, when used correctly. Making regular purchases and paying the full balance on time each month demonstrates responsible credit behaviour and builds your credit history with bureaus including CIBIL. The annual fee waiver does not affect how the account is scored — the key requirement is consistent, on-time full payment every billing cycle.

What hidden charges should I check on a lifetime free card?

The main charges to look up in the Schedule of Charges are: revolving interest rate (monthly and annual), late payment fee by outstanding balance slab, cash advance fee and applicable interest rate, forex markup percentage, GST at 18% on all applicable charges, EMI processing fee, and reward redemption fee. These are the charges the marketing headline almost never highlights.

Should I choose cashback or reward points on a lifetime free card?

Cashback is simpler for most beginners — it credits directly to your statement with no redemption step, no minimum threshold, and no expiry concern. Reward points offer more flexibility in principle but require you to track point balances, meet redemption minimums, and choose from a catalogue that may not match your actual needs. If you prefer clarity and zero effort on redemption, cashback is the easier choice for a first or second credit card.

What happens if I miss the payment due date on a free credit card?

Two costs apply simultaneously: a late payment fee is charged based on your outstanding balance slab, and interest begins accruing on the full outstanding amount from the individual transaction dates — not just from the due date you missed. GST at 18% applies on both the late fee and the interest charge. Missing even one due date on a ₹20,000 balance can cost ₹1,000 or more in a single month when all charges are combined.

Can I get a lifetime free credit card with a monthly salary of ₹25,000?

Minimum income eligibility varies by issuer and specific card variant. Many banks offer entry-level lifetime free cards for salaried applicants with income from ₹15,000–₹25,000 per month, but requirements change. Verify directly with the issuer — do not rely only on third-party aggregator sites for income eligibility, as these may not reflect the most current criteria or the bank’s internal underwriting practices.

Is the revolving interest rate on a lifetime free card higher than on a paid card?

Not necessarily. Some paid cards have comparable or even higher interest rates than lifetime free cards. The annual fee and the interest rate are set independently by the issuer. Always compare both figures from each card’s MITC before applying — a card that charges no annual fee but a higher revolving rate is not cheaper if you ever carry a balance.

Can I use a lifetime free card to build a credit limit upgrade over time?

Consistent, on-time full repayment and responsible credit utilisation are the main drivers of credit limit increases over time, regardless of whether your card has an annual fee. However, some lifetime free cards have lower credit limit ceilings than premium cards. If a high credit limit is an explicit goal, check whether the card type you are considering has a limit ceiling that would meet your future requirement — verify with the issuer directly.

Final Verdict

Lifetime free credit cards India are a genuinely useful product for disciplined, low-to-moderate spenders who pay their full bill each month. For a first-time cardholder, a salaried employee building credit history, or anyone who wants cashback on everyday purchases at zero annual cost — these cards make complete sense as of recent data.

The real risk is not the annual fee. It is revolving interest on unpaid balances, cash advance charges, and the assumption that “free” extends beyond the two fees it actually covers. A lifetime free card used with full monthly repayment costs nothing and builds credit. The same card used with partial payments can cost more in a single month than a standard paid card’s entire annual fee.

Compare cards based on your actual spending pattern and repayment discipline — not the headline. Read the MITC from end to end before you apply. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.