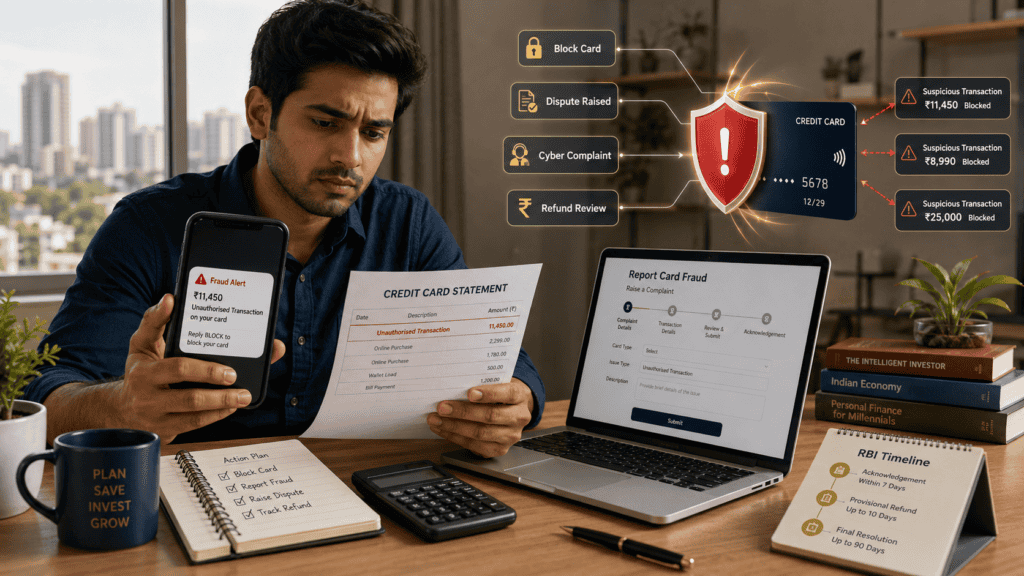

You check your phone at 2 a.m. and see an SMS: ₹38,500 debited from your credit card at GLOBALSTORE-NYC. You were asleep. You never made this transaction.

Credit card fraud in India is more common than most people expect — and the first few minutes after you spot it matter more than anything that follows. A delayed response, a deleted SMS, or a missed complaint number can seriously complicate your dispute later.

This guide gives you a clear India-specific action plan: what to do right now, how RBI rules and bank policies shape your refund position, what evidence to save, and where to escalate if your bank goes quiet. Refund is not automatic in every case — but fast, documented action gives you the strongest possible position under the framework that governs your claim.

Quick Answer: Credit Card Fraud

Credit card fraud should be reported immediately by blocking the card, informing the bank, saving the complaint number, and disputing the unauthorised transaction. Under RBI customer liability rules, refund responsibility can depend on reporting time, negligence, and transaction type. Acting within the first few hours gives you the strongest case — delays can reduce your protection under the bank’s dispute framework.

Key Takeaways

- Blocking your card within minutes of spotting fraud stops further misuse — use your bank app, net banking, or customer care IVR immediately, before you do anything else.

- Under RBI’s customer liability framework, reporting speed affects your refund position; customers who report promptly and demonstrate no negligence have a stronger claim — verify current thresholds at rbi.org.in before assuming any specific timeline applies.

- Never delete fraud SMS or email alerts — these are your primary time-stamped evidence when the bank and RBI investigate the dispute.

- Sharing OTP, CVV, or card details — even under pressure or deception — may be treated as customer negligence and can increase your liability under the RBI framework.

- Never ignore a ₹1 or ₹5 unknown debit — fraudsters routinely make a small test charge to verify the card before hitting it for a large amount.

- A verbal complaint to customer care is not enough: always insist on and save a written complaint reference number with the exact date and time it was logged.

- If your bank does not resolve the complaint within its stated timeline, you can escalate to the RBI Integrated Ombudsman Scheme at rbi.org.in.

Key Facts at a Glance

| Situation | First Action | Refund / Dispute Note |

|---|---|---|

| Unauthorised online transaction | Block card via app or customer care; raise written dispute immediately | Refund depends on reporting speed, investigation outcome, and current RBI rules — verify timelines at rbi.org.in |

| Card physically lost or stolen | Block card; report to bank and nearest police station | Transactions after a reported block are generally not your liability; confirm with your bank’s policy |

| OTP scam or phishing | Report to bank and cybercrime.gov.in; block card; save all scammer messages | Voluntary OTP sharing may increase customer liability — facts, bank policy, and RBI rules apply |

| International charge not made by you | Raise dispute; disable international usage immediately via app | Card-not-present fraud; chargeback route applicable — verify bank’s chargeback policy and timeline |

| Duplicate or incorrect merchant charge | Contact merchant first; if unresolved in 48 hours, raise bank dispute | Chargeback applicable; original transaction receipt or bank statement needed as proof |

| Add-on card misuse | Block add-on card; report to bank; confirm whether usage was authorised | Primary cardholder is liable unless fraud is clearly established — check bank policy |

Understanding Credit Card Fraud and the Dispute Process

Credit card fraud occurs when someone uses your card or card details without your knowledge or consent. In India, this happens in several distinct ways — and each type affects how your bank classifies the dispute and what your refund position looks like.

Types of Credit Card Fraud in India

OTP fraud and phishing is the most common type. A fraudster impersonates a bank official, TRAI representative, or delivery agent and tricks you into sharing your OTP, CVV, or card number. They then make a card-not-present transaction within seconds. If you shared any detail — even under pressure — the bank’s investigation will focus on whether the sharing was your negligence.

Lost or stolen card fraud occurs when your physical card is used by someone else. If you reported the card lost before the transaction took place, liability typically does not fall on you. If the card was used before you reported it, timing and your notification speed become central to the dispute outcome.

International card-not-present fraud happens when your card number and CVV are used for a foreign transaction — typically through data breaches on merchant sites or dark web card trading. You did not share anything; the data was stolen without your knowledge. This type generally supports a stronger liability argument in your favour.

Duplicate or incorrect merchant charge is not technically fraud but is handled through the same dispute channel. If a merchant charged you twice or charged the wrong amount, you raise a chargeback request with your bank.

Add-on card misuse occurs when a supplementary cardholder makes a transaction the primary holder was unaware of. Whether this qualifies as fraud depends entirely on whether the transaction was genuinely unauthorised.

Fraud vs. Dispute vs. Chargeback — What Is the Difference?

Fraud is a criminal act — someone used your card without consent. A dispute is the formal process you raise with your bank to contest a transaction. A chargeback is the mechanism banks use to reverse a payment from the merchant’s side when a dispute is found valid. Not every dispute results in a chargeback, and not every chargeback succeeds — but this is your primary financial remedy when a transaction is genuinely fraudulent.

Understanding which route applies to your situation helps you give the bank the right evidence from the start. Begin by reviewing your credit card statement carefully to identify every suspicious entry — Card statement lines explains how to read every line on your statement, including how reversals and dispute credits appear once a case is under investigation.

How Banks Investigate a Fraud Dispute

When you raise a dispute, the bank logs a complaint reference number, conducts an internal investigation, and may contact the merchant or the payment network. For international card-not-present fraud, the bank typically raises a chargeback through Visa, Mastercard, or RuPay. For domestic fraud, NPCI may be involved depending on the card network used.

According to RBI guidelines on unauthorised electronic banking transactions, banks are required to acknowledge your complaint and resolve it within a defined period — verify the current resolution timeline directly with your bank’s MITC or at rbi.org.in before using any specific number in your planning.

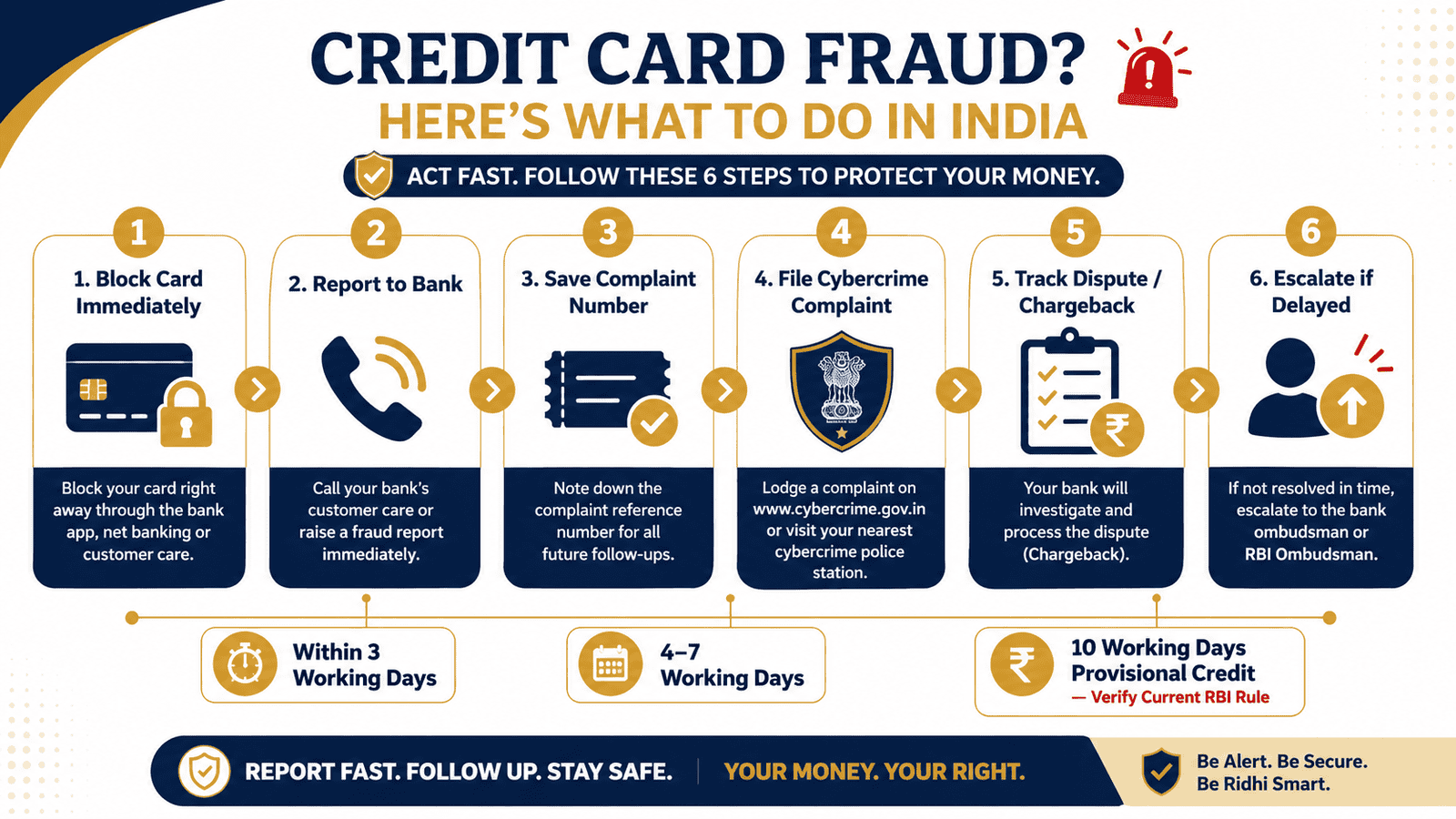

The Emergency Checklist

The moment you spot an unauthorised transaction, these five steps — in order — protect your position: block the card, call customer care and log a complaint, screenshot and save every SMS and email alert, file a cybercrime complaint at cybercrime.gov.in, and send a written dispute email to the bank’s fraud team with your complaint reference number. Do not skip the written step. It timestamps your claim.

Real Example: Rohit’s ₹38,500 International Fraud

Rohit, 31, is a software engineer in Pune earning ₹1.4 lakh per month. At 2:13 a.m. on a Wednesday, an SMS arrives: “INR 38,500 debited from credit card ending 4821 at GLOBALSTORE-NYC. If not you, call [number].” Rohit was asleep. He never made this transaction.

Within 10 minutes: He opens the bank app, taps “Block Card,” and screenshots the fraud SMS with the timestamp visible.

Within 30 minutes: He calls the 24×7 credit card helpline, reports the unauthorised transaction, and writes down the complaint reference number the agent provides.

Next morning: He emails the bank’s fraud dispute address with the complaint number, transaction details, and a written statement confirming he did not make the transaction. He also files a complaint at cybercrime.gov.in and saves the acknowledgement number.

Before the due date: Rohit notices the ₹38,500 is still showing in his outstanding balance. He calls the bank to confirm in writing how the disputed amount affects his minimum due and whether interest will accrue during the investigation. Because due date confusion is common in fraud situations — Billing cycle basics explains how fraud reversals interact with outstanding balances and payment deadlines.

Rohit’s outcome depends on the bank’s investigation findings and the applicable RBI rules at the time — but documented, same-day reporting gives him the strongest possible position.

How to Calculate Your Liability and Cash-Flow Exposure

There is no fixed formula for calculating a guaranteed refund. However, modelling three scenarios helps you understand your financial exposure while the dispute is pending.

Fraud Exposure = Disputed Amount + Interest Accrued (if unpaid) − Provisional Credit (if granted by bank)

| Scenario | Key Conditions | Practical Outcome |

|---|---|---|

| A — Reported same day, no negligence | Card-not-present breach; customer not at fault; reported within bank’s liability threshold period | Strongest zero-liability claim; bank may grant provisional credit — verify current RBI threshold and provisional credit rules at rbi.org.in |

| B — Reported after significant delay | Transaction noticed weeks later; not reported promptly | Liability position weakens with delay; outcome depends on bank policy and current RBI rules — verify before assuming any specific outcome |

| C — Dispute pending, due date approaching | ₹38,500 still in bill; no provisional credit yet; due date in 5 days | Interest or late fee may apply on unpaid disputed amount depending on bank policy — ask bank explicitly in writing how disputed amounts are treated |

To estimate how interest charges may build on an unpaid balance during a pending dispute, use our credit card interest calculator. All liability thresholds and provisional credit timelines must be verified directly at rbi.org.in before making any payment decision.

Comparison: Fraud Scenarios and Dispute Complexity

| Scenario | Likely Classification | Key Dispute Challenge |

|---|---|---|

| Lost card used before reporting | Third-party breach with timing dispute | Gap between physical loss and reporting weakens claim — timing of your complaint is critical |

| OTP shared in phishing scam | Possible customer negligence finding | Voluntary OTP sharing increases your liability exposure — save all scammer messages as supporting evidence regardless |

| International transaction not made by you | Card-not-present fraud or data breach | Stronger chargeback route; no fault evidence helps — disable international usage immediately after reporting |

| Duplicate merchant charge | Merchant billing error | Not fraud — chargeback route; original receipt or bank statement required as proof of the original valid transaction |

| Add-on card misuse | Depends on authorisation facts | Primary cardholder is liable unless fraud is established — informal family authorisation complicates the claim |

| Small test charge followed by large fraud | Third-party breach with prior signal | Ignored test transaction weakens the vigilance argument — always report both transactions together |

How to Decide What’s Right for You

The transaction is clearly not yours and no OTP, CVV, or card detail was shared — block the card immediately and raise a written fraud dispute with the bank the same day. Do not wait for the next billing cycle.

The charge appears to be a merchant error or duplicate billing — contact the merchant first with your transaction proof. If unresolved within 48 hours, raise a chargeback dispute with your bank; this is not a fraud complaint but the outcome is the same.

Your bill due date is approaching and the disputed amount is still showing as outstanding — call your bank and ask in writing how the disputed amount should be treated for payment purposes. Do not simply ignore the bill.

Interest charges have appeared on the disputed amount — request a written reversal once the dispute is resolved in your favour. Learn exactly how interest accrues on unpaid card balances: Card interest charges.

Your bank has not responded or resolved the complaint within its own stated timeline — escalate in writing to the bank’s nodal officer first, then file a grievance with the RBI Integrated Ombudsman Scheme at rbi.org.in.

You have not yet blocked the card — do not spend time on complaint calls before blocking. Every minute the card is active, further fraudulent charges are possible. Block first via app or IVR, then call customer care.

Common Mistakes to Avoid

Waiting for the Monthly Statement Before Reporting

Many cardholders only discover fraud when the full bill arrives at month-end.

This delay can significantly weaken your dispute position. Under RBI’s customer liability framework, faster reporting generally offers stronger protection — a three-week delay may be treated very differently from a same-day complaint. The investigation window, provisional credit eligibility, and your liability exposure are all affected by how quickly you acted.

Enable SMS and email alerts for every transaction, including amounts as small as ₹1, so you catch fraud within minutes rather than weeks.

Sharing OTP, CVV, or Card Number Under Any Pretext

No bank, RBI official, TRAI representative, or delivery partner will ever ask for your OTP or CVV. Ever.

If you shared these details — even under pressure, fear, or deception — your liability in the dispute may increase substantially. Banks may classify this as customer negligence. Save every message, call recording, or screenshot involving the scammer; they can still support your case even when OTP was shared, depending on the circumstances and current rules.

File a complaint at cybercrime.gov.in regardless — honest reporting of all facts gives you a cleaner case.

Not Taking a Written Complaint Reference Number

A phone call without a complaint reference number is nearly impossible to trace or prove later.

Always insist on a written complaint number — via app, email, or branch acknowledgement. Without it, there is no documented proof of the exact date and time you raised the dispute, which is central to how the RBI liability framework assesses your claim.

Deleting Fraud SMS or Email Alerts

That fraud alert SMS is your primary time-stamped evidence. It shows the transaction amount, time, merchant name, and card used.

Deleting it removes all of this. Screenshot every alert immediately and save it in at least two places — phone gallery and a forwarded email to yourself. Do this before anything else, even before calling the bank.

Paying Only the Minimum Due While a Dispute Is Pending

If the disputed amount remains in your outstanding balance and you pay only the minimum due, interest continues to accrue on the full balance — including the fraudulent charge you did not make.

This compounds your financial exposure. Understand the full danger: Minimum amount trap. Always ask your bank in writing how a disputed amount affects your minimum due calculation and whether interest will be reversed if the dispute is accepted.

Ignoring Small Unknown Transactions

A ₹1, ₹2, or ₹5 charge from an unfamiliar merchant name is often a card validation test — a fraudster checking whether the card is active before running a large transaction.

If you dismiss it as a negligible amount and take no action, you may miss the window to block the card before the large fraud charge hits. Every unknown debit, regardless of size, warrants immediate investigation.

When This May Not Be the Right Choice

The fraud dispute route is not the correct path in every situation. Recognise these cases before filing:

Merchant delivery or service failure: If you made the transaction but goods were not delivered or the service was deficient, this is a consumer dispute — not fraud. Raise a chargeback using the correct merchant dispute reason, not a fraud complaint; conflating the two can weaken both claims.

Family or add-on card usage you forgot you authorised: If a family member used a supplementary card and the transaction was informally authorised — even verbally — filing a fraud complaint can create legal complications for all parties. Clarify the facts within the household before contacting the bank.

Forgotten subscription renewal: A recurring charge from a streaming service, gym, or app store may look unfamiliar but was authorised by you in the past. Search your email for the original subscription confirmation before raising a dispute.

Ignoring disputed dues to avoid payment: If you stop paying a disputed balance entirely and the dispute is not accepted, late payment marks and interest damage can reach your credit bureau file — review what unpaid dues can do to your standing: Credit profile impact.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- RBI customer liability framework for unauthorised electronic banking transactions — rbi.org.in. This is the primary document governing how banks must handle fraud liability, refund timelines, and provisional credit obligations for Indian cardholders.

- Bank credit card MITC (Most Important Terms and Conditions) — your issuing bank’s official website. Dispute filing windows, chargeback procedures, provisional credit policies, and internal escalation timelines vary by bank and must be read directly.

- National Cyber Crime Reporting Portal — cybercrime.gov.in. File a complaint here for all online fraud, phishing, OTP scams, and digital identity misuse — in addition to your bank complaint, not instead of it.

- RBI Complaint Management System and Integrated Ombudsman Scheme — rbi.org.in. If your bank does not resolve the complaint within its stated timeframe, file a formal grievance through the RBI Ombudsman portal after exhausting the bank’s internal complaint process.

- NPCI — npci.org.in. Relevant for disputes involving RuPay credit cards or UPI-linked credit card transactions.

Expert Tips

- Turn off international transaction permissions on your credit card when you are not travelling abroad — most bank apps allow you to toggle this in under 30 seconds. A card blocked for international use cannot be hit by international card-not-present fraud, no matter who has the card number.

- Set your credit card limit as close to your genuine monthly usage as possible. A ₹50,000 limit caps your maximum fraud exposure at ₹50,000 — not your savings account balance.

- Enable instant SMS and email alerts for every single transaction, including amounts below ₹10. Fraud test charges are designed to be invisible — low-value threshold alerts miss them entirely.

- Use virtual card numbers or single-use card features where your bank offers them for online shopping, particularly on unfamiliar websites. A virtual number cannot be reused after one transaction, making it worthless to anyone who intercepts it.

- Review your credit card statement at least once per billing cycle — not just when the due date arrives. One unknown entry caught early is far simpler to dispute than several months of accumulated fraud charges.

- Save your bank’s 24×7 credit card helpline under a name you will instantly recognise during panic — “BLOCK HDFC CARD” is more useful than “HDFC Customer Care” when adrenaline is running. When choosing your next card, prioritise fraud controls: Safe first card covers the features to look for, including instant app blocking, virtual card support, and transaction controls.

- After any fraud case is resolved, apply for a replacement card with a new number immediately — even if no further fraud has appeared. A compromised card number remains a risk on dark web trading platforms long after you block the physical card.

Frequently Asked Questions

Will the bank definitely refund my credit card fraud amount?

Refund is not automatic or guaranteed in all cases. It depends on the type of fraud, how quickly you reported it, whether any customer negligence is found, and the outcome of the bank’s investigation. Under RBI’s customer liability framework, customers who report promptly and are not found negligent have a stronger claim — but verify the current rules directly at rbi.org.in before assuming a specific outcome.

What if I reported the fraud three or more days after it happened?

Delayed reporting generally weakens your position under the RBI customer liability framework. The rules distinguish between transactions reported within different time windows — faster reporting is linked to stronger liability protection. The exact current thresholds should be verified at rbi.org.in, as these can change with regulatory updates.

I shared my OTP with a fraudster. Can I still dispute the transaction?

Yes — file the dispute and the cybercrime complaint regardless. However, sharing OTP may be treated as customer negligence, which can increase your liability significantly under the RBI framework. Save every message, screenshot, and call log involving the scammer; these may help establish the deception involved. Be honest with the bank about what happened — the investigation outcome depends on the facts and current rules.

Should I pay the disputed amount while my complaint is still pending?

This depends entirely on your bank’s policy. Some banks issue provisional credit during an active investigation; others continue to show the disputed amount as due. If you do not pay and the dispute is later rejected, you may incur interest and late charges on the full amount. Ask your bank explicitly in writing how the disputed balance affects your minimum due and whether interest will be reversed if the dispute is accepted — do not assume either way.

How long does a credit card chargeback take in India?

Chargeback timelines vary by bank, card network (Visa, Mastercard, or RuPay), and transaction type. International chargebacks typically take longer than domestic disputes. Verify the current resolution timeline with your specific bank’s MITC or credit card terms before building any cash-flow expectation around a chargeback completion date.

Can I file a cybercrime complaint and an RBI Ombudsman complaint at the same time?

The cybercrime complaint at cybercrime.gov.in and your bank dispute can run simultaneously — these are separate processes. However, the RBI Ombudsman complaint should only be filed after you have first raised the grievance formally with your bank and not received a satisfactory response within the bank’s own complaint resolution timeline. The Ombudsman is a second-tier escalation, not a first step.

What is a dispute reference number and why does it matter so much?

A dispute reference number is the bank’s formal written acknowledgement that your complaint was logged on a specific date and time. It is your primary proof of timely reporting. Without it, establishing exactly when you raised the dispute becomes very difficult — and timing is directly relevant to how the RBI customer liability framework assesses your claim.

Can credit card fraud affect my CIBIL score?

The fraud itself does not affect your CIBIL score. However, if the disputed amount remains unpaid while the investigation continues — and the dispute is ultimately not accepted — the unpaid balance and any resulting late payments can be reported to credit bureaus by your bank. This is why understanding your payment obligations during a pending dispute matters more than simply ignoring the bill while waiting for the outcome.

Is a police FIR required to dispute credit card fraud?

An FIR is not mandatory for all bank disputes. For significant fraud amounts, identity theft, or phishing scams, however, an FIR strengthens your formal complaint record and may be requested by your bank as supporting documentation. A cybercrime complaint at cybercrime.gov.in serves as a formal registered complaint and is recommended for all online fraud cases regardless of whether you also file an FIR at the local police station.

Final Verdict

Credit card fraud is a time-sensitive emergency — and how you respond in the first hour shapes everything that follows. Block the card first. Log a written complaint second. Document every step third. A calm, documented response beats a panicked verbal complaint every time.

Your refund position depends on reporting speed, the type of fraud, your documentation quality, and the current RBI rules that apply to your case — not on how loudly or persistently you complain. If your bank delays, the RBI Integrated Ombudsman Scheme at rbi.org.in is your formal escalation route. For large fraud amounts or identity theft, professional or legal advice may also be worth considering.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.