Your credit card statement arrives every month — and most people glance at the total payable number, transfer the money, and move on. That one habit costs more than it should.

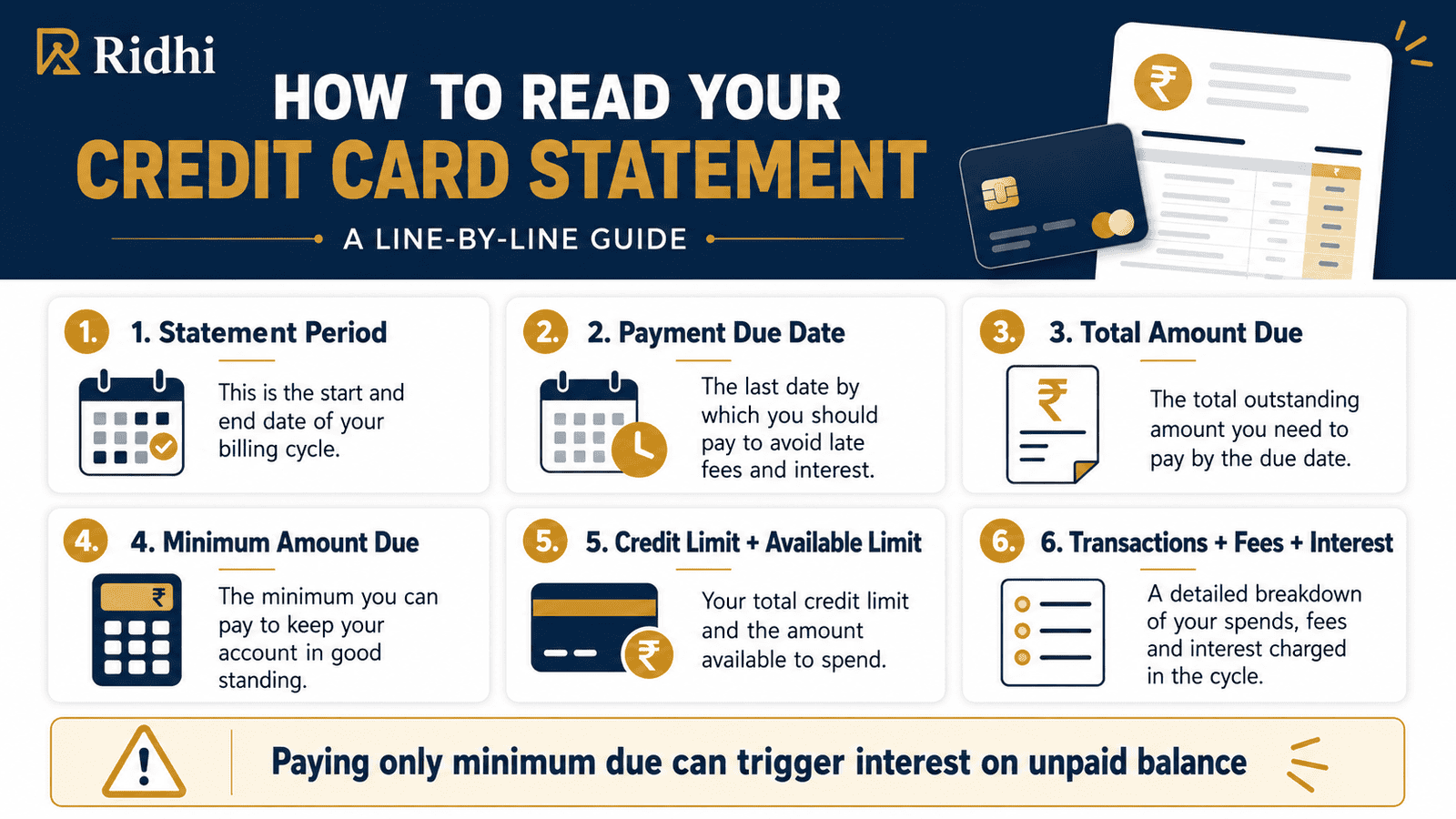

A credit card statement contains far more than a single amount. It shows your billing cycle, payment due date, transactions, fees, interest charges, reward points, and your remaining credit limit — all on the same document. Miss one line and you could pay interest you never expected, lose reward points you legitimately earned, or let an unauthorised charge sit unnoticed for weeks.

This article walks you through every line of a credit card statement in plain language, with a realistic Indian example, so you can check yours in under five minutes — and never be caught off guard by a charge again.

Quick Answer: How to Read a Credit Card Statement

To read a credit card statement, check the statement period, payment due date, total amount due, minimum amount due, credit limit, transactions, fees, interest, rewards and previous payments. If ₹25,000 is outstanding, paying only the minimum can keep interest running on the unpaid balance. Statement formats vary by bank — always refer to your card issuer’s official app, website, or MITC document for exact terms applicable to your card.

Key Takeaways

- The payment due date is not the same as the statement generation date — confusing the two is one of the most common reasons cardholders pay late and incur fees.

- Total amount due and minimum amount due are two very different numbers: paying only the minimum does not clear your bill and interest continues on the unpaid balance.

- Finance charges on Indian credit cards can be significant — and at many issuers, they apply on the full outstanding balance if even a small amount is left unpaid, depending on your card’s MITC terms.

- Review every transaction line — not just the final payable amount. Unauthorised charges, missing refunds, and hidden fee entries are only visible here.

- Your statement also shows your available credit limit, reward points earned and redeemed, active EMI schedules, and any annual or late payment fee entries that are easy to overlook.

- According to RBI guidelines, credit card issuers must provide a clear statement of all applicable charges. Always verify rates and fees against your specific card’s MITC document before assuming any figure applies to you.

- Checking your statement within 24–48 hours of generation gives you the full dispute window — most issuers have a strict deadline for reporting errors.

Key Facts at a Glance

| Statement Term | What It Means | Why It Matters |

|---|---|---|

| Statement Period | The date range covered by this bill (e.g. 5 April to 4 May) | Transactions outside this window appear in the next statement |

| Payment Due Date | Last date to pay without late charges | Missing it can trigger late fees and a CIBIL impact |

| Total Amount Due | Complete balance payable for this cycle | Pay this in full to avoid finance charges on retail purchases |

| Minimum Amount Due | Smallest amount to avoid immediate late-payment classification | Paying this does not stop interest on the remaining unpaid balance |

| Credit Limit | Maximum borrowing capacity approved by the issuer | High usage relative to limit affects your CIBIL score |

| Available Credit Limit | Remaining credit after subtracting outstanding balance | Track this before making large new purchases |

| Finance Charges | Interest applied on any unpaid balance per issuer terms | Rates vary — verify in your card’s MITC document |

| Late Payment Fee | Fee charged if payment is not received by due date | Amount varies by issuer and outstanding balance slab |

How to Read Every Line of Your Credit Card Statement

Opening a credit card statement for the first time can feel overwhelming. It is not, once you know the layout. Most Indian issuers — whether it is HDFC, SBI Card, ICICI, Axis, or a co-branded issuer — follow a broadly similar structure, though the exact labelling and order may differ. Here is what each section contains and why it matters.

Cardholder Details and Card Number

The top of the statement shows your registered name, a masked card number (usually only the last four digits), your registered mailing address, and the statement generation date. Confirm these details match your current information. If your registered address is outdated, bank communications and physical statements may not reach you — a common reason people miss payment due dates.

Statement Period and Billing Cycle

The statement period defines exactly which transactions are included in this bill — for example, from 5 March to 4 April. This is your billing cycle. All purchases, payments, fees, and interest entries within this window appear on this statement. Anything that happens after the closing date appears on the following month’s statement. Understanding your billing cycle basics helps you plan purchases strategically and avoid inadvertently crossing into a new cycle when timing large spends.

Payment Due Date and Grace Period

The payment due date is the last date by which your payment must reach the bank — not the date you initiate the transfer. Most issuers provide 18–25 days after the statement closing date as the payment window, and this is your grace period. Pay the total amount due within this window and no interest is charged on standard retail purchases, subject to your issuer’s terms. A payment initiated on the due date itself may not clear in time if your bank’s NEFT or RTGS processing runs late — always pay 2–3 days early.

Total Amount Due

This is the complete amount you owe for the current billing cycle. It includes all purchases made during the statement period, outstanding balance carried from previous months (if any), applicable fees such as annual fee or late payment fee, and GST on those fees and interest. Paying this figure in full by the due date is the only way to completely avoid finance charges on retail transactions.

Minimum Amount Due

This is a small fraction of your total — typically calculated as a percentage of the outstanding balance or a fixed minimum floor, whichever is higher, as per your card issuer’s policy. Paying only this amount avoids an immediate overdue classification, but interest continues to accrue on every rupee of the remaining unpaid balance. This is the most misunderstood number on the statement, and it costs Indian cardholders significant money every year.

Credit Limit and Available Credit Limit

Your credit limit is the maximum the issuer will allow you to borrow at any point. The available credit limit is what remains after subtracting your current outstanding. If your credit limit is ₹3,00,000 and your outstanding balance is ₹90,000, your available limit is ₹2,10,000. This figure matters beyond just knowing your remaining purchasing power — high credit utilisation relative to your limit is a key factor in CIBIL scoring.

Cash Limit

Many credit cards show a separate cash withdrawal limit — the amount you can withdraw from an ATM or a bank branch using the card. This is usually a percentage of your total credit limit. Cash advances attract a one-time transaction fee plus daily interest from the date of withdrawal, with no grace period — unlike regular retail purchases. The interest rate on cash advances is often higher than the standard purchase rate.

Transaction Section — Read This Line by Line

This is the most important part of the statement. It lists every purchase, payment, refund, reversal, EMI debit, fee entry, and interest charge during the statement period. Go through this section against your SMS and email transaction alerts. Pay specific attention to:

- Transactions you do not recognise — any unfamiliar merchant name or amount

- Refunds for returned items that should have appeared but have not

- EMI conversion entries — some issuers auto-convert large purchases to EMI

- Fee entries such as annual fees, overlimit fees, or late payment charges from the previous month

- GST applied on fees and finance charges, which appears as a separate line on many statements

Finance Charges

If you carried an unpaid balance from the previous month, finance charges appear as a separate entry. Most Indian credit card issuers calculate interest on the daily average outstanding balance, dating back to the original transaction date — not from the due date. This means even a partial payment from the previous cycle may not eliminate interest completely. The applicable rate varies by issuer and card type; refer to your card’s MITC document for the exact rate that applies to your account.

Reward Points Summary

Toward the end of the statement, most issuers show a reward points or cashback summary — points earned this cycle, points redeemed, points expired (if any), and the closing balance. If your card earns accelerated points on specific categories such as fuel, dining, or travel, check that the correct earn rate was applied to those transactions. Reward reversals do happen and are easy to miss.

Previous Balance and Payment Received

The statement also shows the opening balance (carried forward from last month) and the payment amount received from you. Verify that your previous payment is correctly credited and that the opening balance used in this statement is accurate. An error here — particularly a payment credited after the cut-off — can result in incorrect finance charge calculations for the current cycle.

Real Example: Rohan’s April Statement

Rohan is 27, a software engineer in Bengaluru earning ₹85,000 per month. He has been using his first credit card for six months — mostly for groceries, OTT subscriptions, and Swiggy orders. His April statement arrives and he opens it properly for the first time.

Statement period: 5 March to 4 April. Total amount due: ₹25,000. Minimum amount due: ₹1,250. Due date: 25 April.

Breaking it down: ₹18,500 in retail purchases this month, a ₹500 cashback reversal pending from a cancelled order, a ₹750 annual fee entry, and ₹5,250 carried forward from last month’s unpaid balance with finance charges applied on that amount.

Rohan spots a ₹349 transaction from a merchant he does not recognise — he raises a dispute before making any payment. He also notices that his minimum payment last month caused the minimum due trap — the ₹5,250 carried forward includes both the unpaid principal and the finance charges applied to it.

The key insight: paying the minimum last month did not just defer the balance — it made it more expensive. Paying the total amount due this month is the only way to stop the cycle.

How to Calculate the Cost of Paying Only the Minimum

Using Rohan’s example to show the actual rupee impact:

Finance Charge = Unpaid Balance × Monthly Interest Rate

Starting figures from the statement:

- Total amount due: ₹25,000

- Minimum payment made: ₹1,250

- Unpaid balance carried forward: ₹23,750

Finance charges depend on the rate in your card’s MITC. Indian credit cards commonly apply monthly rates that, for illustration purposes using a rate of 3.5% per month (verify with your issuer — rates vary and this is for illustration only):

Finance charge = ₹23,750 × 3.5% = ₹831.25 for one month

That ₹831.25 appears as an additional charge in next month’s statement. If Rohan pays only the minimum again, the balance grows further. Over three months, interest alone on a ₹25,000 bill can comfortably exceed ₹2,500 — for purchases already fully consumed.

| Scenario | Unpaid Balance | Approx. Monthly Finance Charge |

|---|---|---|

| Pay minimum (₹1,250 of ₹25,000) | ₹23,750 | ₹831 (at 3.5% illustrative rate) |

| Pay half the bill (₹12,500) | ₹12,500 | ₹438 (at 3.5% illustrative rate) |

| Pay total amount due (₹25,000) | ₹0 | ₹0 |

For the exact method Indian card issuers use — including how daily average balance is calculated — refer to the interest calculation method explained in detail.

Comparison: Full Payment vs Minimum vs No Payment

| Payment Choice | What Happens to Your Account | Key Risk |

|---|---|---|

| Full payment by due date | No interest on retail purchases (subject to issuer terms); no late fee; CIBIL unaffected by payment behaviour this cycle | Requires sufficient funds available on or before due date |

| Minimum amount due only | Account stays technically current; late-payment status avoided; interest applies on entire remaining balance | Finance charges compound month over month; total cost grows significantly |

| No payment at all | Late payment fee charged; finance charges applied from transaction dates; potential negative CIBIL entry | Credit score damage; recovery and negotiation become difficult |

| Part payment above minimum | Outstanding reduced; interest still applies on the remaining unpaid portion | Still incurs finance charges — better than minimum, not as good as full payment |

| Auto-debit set up | Payment made automatically; missed-due-date risk eliminated | If auto-debit is set for minimum only, balance grows with interest; bank account must have sufficient funds |

How to Decide What’s Right for You

all transactions in the statement are correct and you have the funds available — pay the total amount due before the due date. This is the only payment that eliminates finance charges on retail purchases.

you spot a transaction you did not make — raise a dispute with your issuer immediately. Do not delay payment on the undisputed portion of the bill while the investigation is ongoing.

your statement balance is consistently above 40%–50% of your credit limit — that high utilisation figure is visible on your CIBIL report. Consider making a part-payment before the statement generation date to reduce the reported balance. See how credit usage affects your CIBIL score and what threshold to target.

you have paid only the minimum for two or more consecutive months — treat this as a debt warning sign. The interest compounding will make your total outstanding significantly higher than your original purchases within a few months.

your statement shows an EMI entry you do not recall approving — contact the card issuer’s helpdesk. Some banks convert large purchases to EMI automatically under certain conditions; you may be able to reverse it within a window.

you can pay the full amount this month — pay as much above the minimum as you can manage. Every extra rupee reduces the balance on which finance charges are calculated, even if you cannot eliminate them entirely.

you have set up auto-debit yet — ensure your linked account has sufficient balance at least two days before the due date. An auto-debit failure is treated by the bank as a missed payment, with the same fee and CIBIL consequences.

Common Mistakes to Avoid

Treating Minimum Due as the Full Bill

Many first-time cardholders believe that paying the minimum amount clears that month’s charges cleanly.

It does not. Finance charges apply on the remaining ₹23,000-plus of unpaid balance and appear in next month’s statement, often without a clear explanation linking them to the previous month’s partial payment. A ₹25,000 bill left at the minimum can generate ₹800–₹900 in additional interest charges within a single month.

Pay the total amount due wherever your cash flow allows — and treat the minimum as an emergency floor, not a routine choice.

Confusing Statement Date with Payment Due Date

The statement is generated on one date; the payment is due several days later.

Readers who see “Statement Date: 5 April” and assume payment is needed by 5 April will consistently pay before they need to — or, worse, assume a due date that has already passed. Always locate the “Payment Due Date” line explicitly.

Set a phone reminder with the actual due date as soon as the statement arrives.

Ignoring Cash Advance Entries

Cash withdrawals on a credit card appear as a separate entry in the transaction section.

They attract a one-time transaction fee and daily interest from the date of withdrawal — with no grace period. If someone used your card or you withdrew cash in an emergency, the interest charges can appear unexpectedly high. Learn exactly what cash withdrawal charges cost and why they are best avoided.

Always verify whether any cash advance entries in the statement are yours before assuming the balance is correct.

Not Checking Refunds and Reversals

If you returned a purchase or a merchant issued a refund, it should appear as a credit entry in the statement.

If it does not appear and you paid the statement balance in full, you have effectively paid for a purchase that no longer exists. Refunds from merchants can take 7–21 working days to reflect, and they do not always land before the next statement closes. Follow up with the merchant and the bank if a pending refund is missing from two consecutive statements.

Keep all merchant refund confirmation references until the credit appears on your statement.

Missing Annual Fee or Late Payment Fee Lines

Annual fees and late payment fees can appear buried in the middle of the transaction list without a separate alert.

Annual fees may appear without a prior SMS on some cards, especially on renewal year. Late payment fees from the previous cycle appear in the current statement’s transaction section, not as a separate summary line. Always scroll through the full transaction list — not just the balance summary at the top.

If an annual fee appears and you believe you are eligible for a fee waiver, contact the issuer within the statement period.

Not Verifying the Opening Balance

If your previous month’s payment is not reflected correctly in the opening balance, you may be charged finance charges that should not apply.

This can happen when a payment is credited after the statement cut-off date. Always check the “Previous Balance” and “Payment Received” lines and confirm they match your payment records — including the date on which the payment cleared.

Keep your payment transaction reference numbers for at least two statement cycles.

Overlooking the Reward Points Section

If you made a ₹12,000 purchase in a bonus category that earns 5x points but only see base-rate points credited, you are losing reward value you earned.

Reward reversals are common — for merchant category mismatches, failed milestone criteria, or processing errors. Check the points earned this cycle against the expected earn rate, especially after large purchases or during promotional periods.

Discrepancies must be raised with the issuer within the statement cycle to have the best chance of correction.

When This May Not Be the Right Choice

Reading the statement on your own is useful for routine monthly checks. But certain situations require you to go further than just reviewing the document.

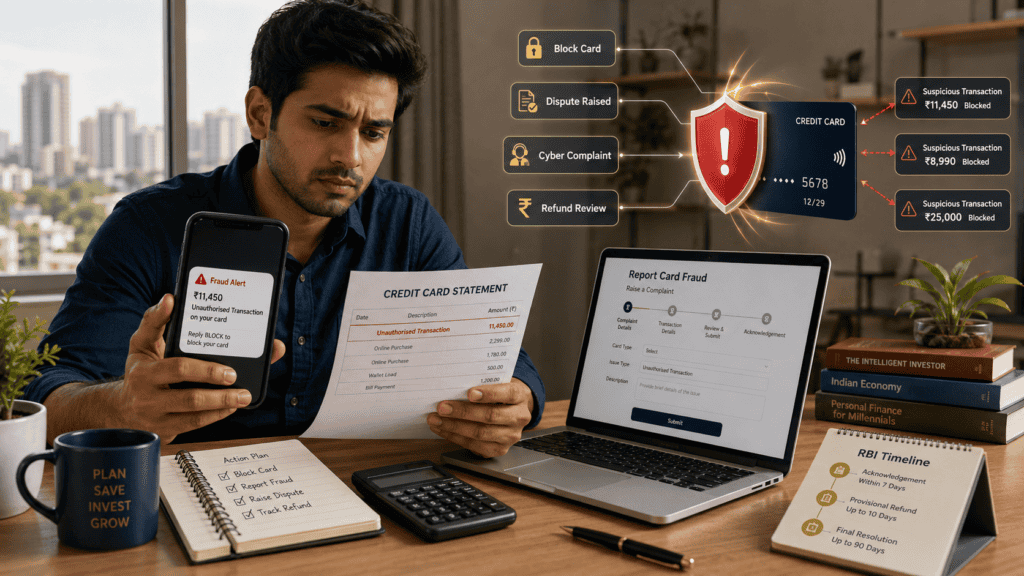

If you find an unauthorised or fraudulent transaction, reviewing the statement is only the first step — you must report it immediately through your bank’s official dispute channel, not just make a note of it. Dispute filing windows can be as short as 30 days from the statement date, and delays can affect your ability to get a refund.

If your statement contains a legal or recovery notice, do not attempt to handle it by reading the statement alone. Contact the issuer’s customer service and, if amounts are significant, consider speaking with a qualified financial or legal advisor.

If you are revolving a large balance month after month and the finance charges are growing, the statement alone cannot resolve the underlying problem. A structured repayment plan or a balance transfer option discussed directly with your bank may be necessary.

If the statement includes complex entries — EMI foreclosure charges, co-branded reward adjustments, insurance premiums, or chargeback reversals — and the figures are unclear, raise a service request with the card issuer’s helpdesk rather than trying to reconcile them manually.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit card rules in India are governed primarily by RBI directions, which all card issuers must follow. Your card’s Most Important Terms and Conditions (MITC) document is the single most important reference for your specific card — it lists the exact fees, interest rates, late payment charge slabs, cash advance rates, and GST treatment applicable to your account.

- RBI — rbi.org.in (credit card directions, customer protection guidelines, grievance framework)

- Your card issuer’s official website — MITC document, schedule of charges, cardholder agreement, and updated fee tables

- Bank’s official app or net banking portal — live account information, statement download, and dispute submission portal

If you find an unauthorised transaction, follow your bank’s official dispute process without delay. For step-by-step guidance, see how to report credit card fraud and claim a refund in India.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Check your statement within 24–48 hours of receiving the generation notification. Dispute windows are time-limited — early review gives you the full window to raise any issue before the deadline.

- Set a calendar reminder 4–5 days before the payment due date, not just the day before. NEFT and RTGS transfers can take up to one working day to reflect on the card account; a buffer protects you from technical delays.

- Always aim to pay the total amount due rather than the minimum. Even paying ₹1 less than the total outstanding can attract finance charges at some issuers — check your MITC for the exact rule on partial payments.

- Match every transaction in the statement against your SMS and email transaction alerts from the bank. Any transaction in the statement that has no corresponding alert is worth investigating promptly.

- Download and save your last 12 monthly statements. They are useful for income tax filing support, reimbursement claims with employers, visa applications requiring bank statements, and dispute evidence if a refund does not appear.

- Check your credit utilisation on the statement — not just your outstanding balance. If your outstanding is ₹75,000 on a ₹1,00,000 limit, your utilisation is 75%, which is likely weighing on your CIBIL score without your realising it.

- If you hold a supplementary or add-on card issued to a family member, those transactions also appear in your primary statement. Review them separately to ensure no charges have slipped through unnoticed.

Frequently Asked Questions

What is a credit card statement?

A credit card statement is a monthly summary issued by your card issuer showing all transactions, fees, interest, reward points, payment due dates, and your outstanding balance for that billing cycle. It is generated automatically at the end of each billing period and sent to your registered email or mailing address.

What is the difference between total amount due and minimum amount due?

The total amount due is the complete balance you owe for the billing period — purchases, fees, interest, and any carried-forward balance. The minimum amount due is a much smaller fraction — typically calculated as a percentage of the outstanding or a fixed floor, whichever is higher — that keeps the account from being classified as overdue. Paying only the minimum does not prevent interest from running on the remaining unpaid balance; it only avoids an immediate late-payment status.

What is a credit card billing cycle?

The billing cycle is the period between two consecutive statement generation dates — for example, 5 March to 4 April. All purchases, payments, fees, and interest entries within this window appear on that month’s statement. Transactions made after the cycle closes appear on the following month’s statement.

Will paying only the minimum amount due affect my CIBIL score?

Paying the minimum keeps your account technically current, so it may not trigger an immediate negative payment record on your CIBIL report. However, maintaining a high outstanding balance relative to your credit limit raises your credit utilisation ratio, which is a key factor in CIBIL scoring. Revolving a high balance over multiple months can gradually lower your credit score even without a missed payment.

Why is interest charged even after I made a payment?

If you paid only the minimum or a partial amount last month, finance charges apply on the unpaid balance from the original transaction dates. At many Indian issuers, if any balance is carried forward, new purchases in the current cycle also lose their grace period and attract interest from the purchase date — this is called the loss of interest-free period. The exact rule depends on your card’s MITC, so verify with your issuer.

Where can I find reward points in the statement?

Reward points or cashback summary are usually listed toward the end of the statement, in a separate section showing points earned this cycle, points redeemed, points expired or forfeited, and the closing balance. Some issuers also display the approximate rupee value of the point balance. If you made purchases in bonus-earn categories, cross-check that the accelerated earn rate was correctly applied.

Can I dispute a transaction I see in my statement?

Yes. If you see a transaction you did not authorise or do not recognise, contact your card issuer immediately through the official customer support number, app, or net banking portal. Most issuers require disputes to be raised within 30–60 days from the transaction date or statement date — confirm the exact window from your issuer’s MITC. Acting quickly significantly improves the likelihood of a successful resolution.

What is the MITC document and where do I find it?

MITC stands for Most Important Terms and Conditions. It is the official document from your card issuer listing all fees, interest rates, late payment charges, cash advance rates, grace period rules, and other key terms applicable to your specific card. It is typically available on your card issuer’s official website under the credit cards section, in your welcome kit, or by requesting it through customer support or the bank app.

What happens if I miss the payment due date entirely?

Missing the due date typically triggers a late payment fee, which varies by issuer and by the outstanding balance slab — cards with higher balances generally attract a higher absolute fee. Finance charges also apply on the full outstanding from the transaction dates. Repeated missed payments can result in a negative entry on your CIBIL report, affecting your eligibility for future loans, home loans, and even new credit card applications.

Is setting up auto-debit on the minimum amount due a good idea?

Auto-debit protects you from missing the due date and incurring late fees, which makes it a useful safety net. However, if it is set only for the minimum amount due, the remaining large balance continues to attract finance charges every month. A better approach is to set auto-debit for the total outstanding amount — but only if your linked bank account reliably has sufficient funds. An auto-debit failure due to insufficient balance is treated as a missed payment.

Final Verdict

Your credit card statement is not just a bill — it is a complete monthly health record of your account. Make it a habit to read it before you pay, not after. Start with the payment due date, total amount due, and minimum amount due. Then go through every transaction line, check that refunds have appeared, confirm fees are what you expect, review finance charges if any, and note your reward points balance. If anything does not match your records, raise it before making payment.

For beginners working through their first few statements, one rule covers most situations: understanding how to read a credit card statement correctly means paying the total amount due in full before the due date, every month. That single habit eliminates finance charges, protects your CIBIL score, and ensures rewards are not offset by avoidable interest.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.