If you have ever looked at your monthly payslip and spotted a small deduction labelled “Professional Tax” — and wondered why yet another amount is being cut besides TDS — you are not alone. Professional tax in India confuses millions of salaried employees, partly because it is not income tax and partly because the rules are completely different from state to state.

Some states charge it. Others do not. The amount varies. And the deduction sits quietly in your payslip every month, reducing your actual in-hand credit. This article explains exactly what professional tax is, why your employer deducts it, how it differs from income tax and TDS, how it affects your monthly take-home salary, and how to verify what applies to you — based on where you actually work.

Quick Answer: Professional Tax in India

Professional tax in India is a state-level tax deducted from salary by employers in applicable states. It reduces monthly in-hand pay, usually as a small payslip deduction, and is separate from income tax/TDS. The maximum annual limit is ₹2,500, but slabs and exemptions vary by state.

Key Takeaways

- Professional tax is a state-level levy — not a central government tax like income tax. Not every state in India charges it, so whether it appears in your payslip depends entirely on where your employer’s payroll is registered.

- The Constitution caps professional tax at ₹2,500 per year per person under Article 276, but each state sets its own slabs and thresholds within this limit.

- For salaried employees, the employer deducts professional tax from monthly salary and remits it to the state authority — it appears as a separate deduction line in your payslip, distinct from TDS and PF.

- Even if TDS is already being deducted, professional tax is a completely separate, additional deduction — both will appear in the same payslip in applicable states.

- Professional tax paid during the year is deductible from your gross salary under Section 16(iii) of the Income Tax Act, which slightly reduces your taxable income at filing time.

- State slabs, thresholds, and exemptions vary and can change — always verify the current slab with your employer’s payroll team or your state’s official commercial tax department before relying on any published figure.

Key Facts at a Glance

| Parameter | Detail | Note |

|---|---|---|

| Who levies it | State governments (where applicable) | Not all Indian states charge it |

| Constitutional maximum | ₹2,500 per year | Article 276, Constitution of India |

| Who deducts it | Employer, via monthly payroll | Employee sees it as a payslip line item |

| Where it appears | Deductions section of monthly payslip | Separate from TDS and PF lines |

| Income Tax benefit | Deductible under Section 16(iii) of IT Act | Reduces gross salary before tax is computed |

| Same as income tax? | No — completely separate levy | Different authority, different legal basis |

| Frequency | Monthly deduction in most states | Some states vary the amount across specific months |

salary slip deductions explained — see how professional tax fits alongside PF, TDS, and other monthly deductions in a complete payslip breakdown.

What Is Professional Tax in India — And Why Is It on Your Payslip?

The name is misleading. “Professional tax” sounds like something charged only on professionals — doctors, lawyers, chartered accountants. In reality, it applies to anyone earning an income through a profession, trade, or employment in a state that has enacted professional tax laws. That includes salaried employees in software companies, banks, factories, hospitals — anyone drawing a monthly salary in an applicable state.

A State Tax, Not a Central Tax

Income tax is collected by the Government of India and governed by the Income Tax Act, 1961. Professional tax is different: it is levied by individual state governments under the authority of Article 276 of the Constitution of India. This constitutional provision allows state legislatures to impose taxes on professions, trades, callings, and employment, subject to a maximum annual cap per person.

Because each state enacts its own professional tax legislation independently, the rules are not uniform across India. Some states charge professional tax on all employees above a salary threshold. Others apply it across graduated income slabs. A handful of states and Union Territories do not levy it at all. Where you work — not where you live — determines whether you pay it and how much.

Why Your Employer Deducts It From Salary

For salaried employees, the professional tax collection mechanism is entirely managed by the employer. The employer — registered with the state’s professional tax authority — deducts the applicable amount from each employee’s monthly salary and remits it to the state government via a professional tax challan. The employee does not need to file a separate professional tax return or make a separate payment. It is fully handled through payroll.

This is why professional tax appears in your payslip’s deductions section — alongside TDS, Provident Fund, and other statutory deductions. It is not a voluntary deduction. If your employer is in a state that levies professional tax and your salary crosses the applicable threshold, the deduction will appear automatically. Understanding CTC and take-home salary differences is essential — professional tax is one of the deductions that quietly creates the gap between what your offer letter shows and what you actually receive each month.

State of Employment, Not Residence, Determines Applicability

Suppose you live in Gurugram (Haryana) but work for a company whose payroll is registered in Mumbai (Maharashtra). Your employer will apply Maharashtra’s professional tax rules to your salary — because your employment is on the Maharashtra payroll entity. This can create confusion when employees switch between companies in different states, change their reporting location, or work in remote arrangements where physical location and payroll state differ.

If you recently joined a new company, changed office locations, or shifted to a remote arrangement with a different entity, it is worth checking with your payroll or HR team which state’s professional tax rules apply to your salary. The answer is usually reflected in your payslip — but understanding the logic helps you verify it independently.

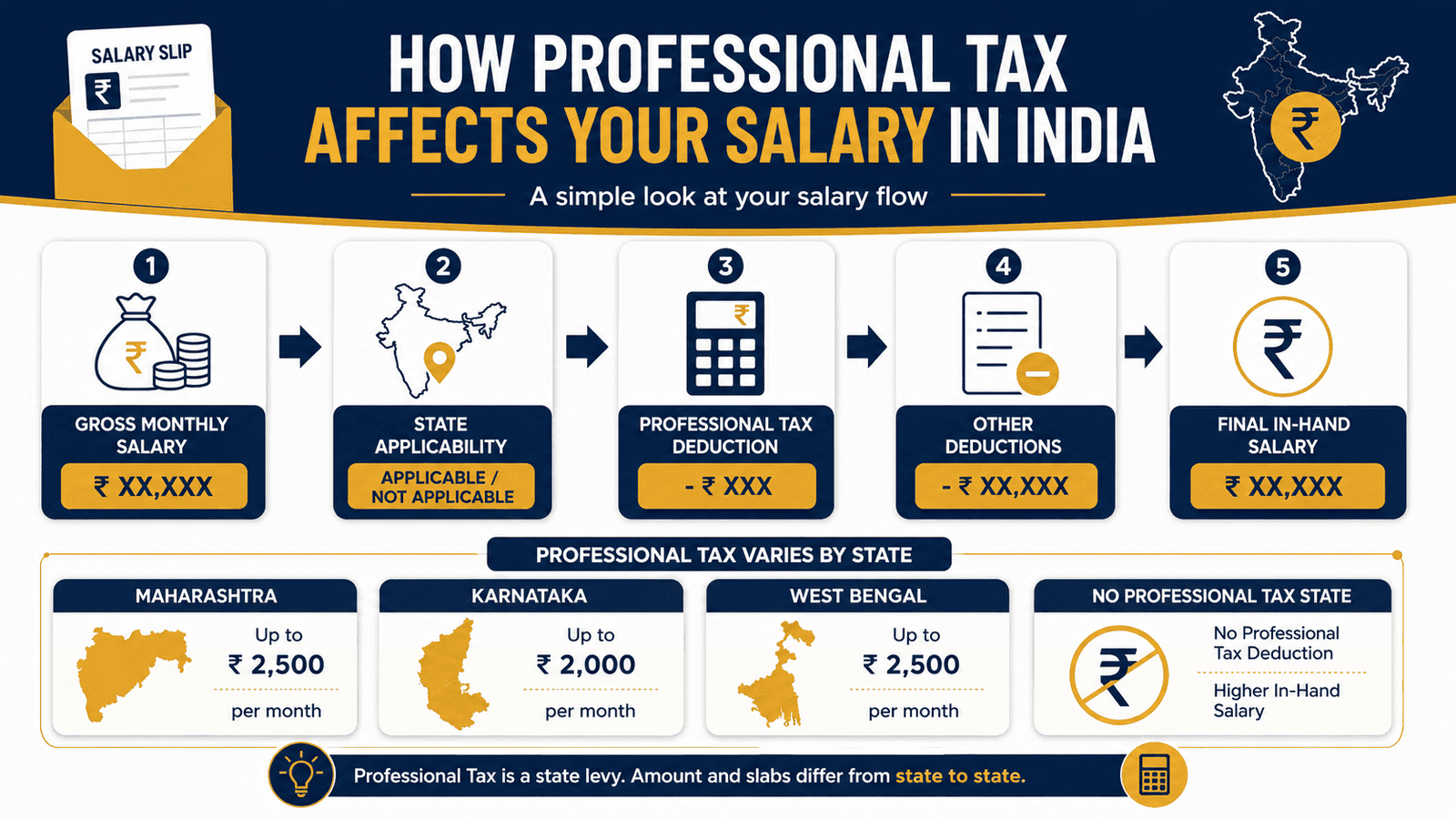

How Professional Tax Fits Into Your Salary Structure

Here is a simplified gross-to-net salary flow that shows exactly where professional tax sits:

Net In-Hand Salary = Gross Salary − TDS − PF (Employee Share) − Professional Tax − Other Deductions

Professional tax reduces your net monthly credit — the amount that actually lands in your bank account. Whether it is visible in your CTC depends on how your employer structures the compensation offer. Some employers include it explicitly in the CTC breakdown; others treat it as an external statutory deduction outside the CTC figure. Either way, it reduces take-home pay by the applicable amount each month.

Because it is a statutory deduction, you cannot opt out of professional tax if your employer’s payroll is in an applicable state and your salary crosses the threshold. There is, however, a small benefit at tax time: professional tax paid during the financial year is deductible from your gross salary under Section 16(iii) of the Income Tax Act. This means if you paid ₹2,400 in professional tax during the year, your gross salary is reduced by that amount before income tax is computed — a modest but legitimate reduction in taxable income.

Profession Tax Registration: What Your Employer Holds

Most employees never interact with professional tax registration directly — but it is useful to know the structure. Employers in applicable states are required to obtain a Profession Tax Registration Certificate (PTRC) from the state authority. This allows them to deduct and remit tax on behalf of their employees. A self-employed person or business owner, by contrast, may need a separate Profession Tax Enrolment Certificate (PTEC) and handle their own payment. As a salaried employee, you are covered under your employer’s PTRC registration — you have no separate registration obligation in most states.

Which States Charge Professional Tax?

States that have enacted professional tax legislation include Karnataka, Maharashtra, West Bengal, Andhra Pradesh, Telangana, Tamil Nadu, Gujarat, Odisha, Kerala, Madhya Pradesh, Assam, Chhattisgarh, Bihar, Jharkhand, Meghalaya, Tripura, and Sikkim. States that currently do not levy professional tax include Delhi, Uttar Pradesh, Rajasthan, Haryana, Punjab, Himachal Pradesh, and Uttarakhand, among others. This list is subject to change with state legislation and notifications — always confirm with your employer’s payroll team or the relevant state commercial tax department directly.

Real Example: Rohan’s Payslip in Bengaluru

Rohan, 29, is a software engineer at a Bengaluru-based tech company, earning ₹85,000 per month in gross salary. Every month, his payslip shows three deduction lines: TDS (deducted at source for income tax), PF (his 12% employee Provident Fund contribution), and Professional Tax.

Karnataka is one of the states that levies professional tax. For salaries above a minimum monthly threshold, Karnataka’s professional tax applies at a fixed monthly amount in most months, with the structure designed to stay within the ₹2,500 annual constitutional cap. Rohan’s monthly take-home salary is reduced by this deduction — a small but real difference in his bank credit.

When Rohan’s colleague moved to the same company’s Delhi office at an identical salary, the Professional Tax line disappeared from his payslip entirely. Delhi does not levy professional tax. Rohan’s colleague now takes home slightly more each month, not because his CTC is different, but simply because his payroll state changed.

For Rohan, the annual professional tax paid is deductible under Section 16(iii) — so it reduces his gross salary before income tax is computed. Use our monthly in-hand salary calculator to estimate how state-level deductions affect your actual salary credit each month.

How to Calculate Your Professional Tax Impact

The calculation logic is straightforward once you know your state’s applicable slab. The core formula:

Annual Professional Tax = Monthly Deduction Amount × Number of Applicable Months

In most applicable states, the deduction is a fixed monthly amount once your salary crosses a threshold. In some states, the amount may differ in a specific month to reach the annual total within the constitutional cap.

| Scenario | Monthly PT Deduction | Annual PT Impact |

|---|---|---|

| Karnataka — salary above applicable threshold | ₹200 (illustrative — verify with state authority) | Up to ₹2,500 (constitutional cap) |

| Maharashtra — salary above applicable threshold | Varies by income slab (verify with state authority) | Up to ₹2,500 |

| Delhi or other non-PT state | ₹0 | ₹0 |

Because slabs, thresholds, and month-specific deduction structures vary by state and are updated by state budget notifications, every figure in this table is illustrative only. Verify the exact slab applicable to your payroll state directly with your employer’s HR or payroll team, or from your state’s official commercial tax department, before using any amount in your salary planning.

Comparison: Professional Tax vs Income Tax vs TDS vs PF

Salaried employees often see multiple deduction lines in their payslip and assume they are all forms of the same tax. They are not. Here is a clear side-by-side comparison of the most common deductions that cause confusion:

| Feature | Professional Tax | Income Tax / TDS |

|---|---|---|

| Levied by | State government | Central government |

| Legal basis | Article 276, Constitution; State PT Act | Income Tax Act, 1961 |

| Annual maximum | ₹2,500 per year | Based on total taxable income and applicable slab |

| Applies in | Only states that have enacted PT legislation | All of India — no state exemption |

| Who remits to authority | Employer remits via professional tax challan | Employer remits TDS to central government |

| Employee action needed | None — employer handles deduction and remittance | File ITR annually; employer deducts TDS monthly |

| Reduces taxable income? | Yes — deductible under Section 16(iii) of IT Act | No — tax paid does not generate further deduction |

| Shown in Form 16 | Yes — as a deduction from gross salary | Yes — as TDS amount deducted and remitted |

Understanding this distinction is one of the first steps to reading your payslip accurately and planning your take-home salary correctly. See our complete guide on gross vs net salary for a full breakdown of how all these deductions flow from your offer letter to your bank account.

How to Decide What’s Right for You

Professional tax is not a product you choose — it is a statutory levy that either applies to you or does not, based on your payroll state. But there are clear practical decisions and actions to take once you understand the rule.

Your payslip shows a Professional Tax deduction and you are in an applicable state — verify that the deducted amount matches your state’s current official slab. Ask payroll for the specific notification or slab reference they are using.

You recently transferred to a different state or a different payroll entity — check with HR whether your payroll has been updated to reflect the new state’s professional tax rules. The change should appear within one to two payroll cycles.

You work remotely for a company registered in a PT state but live in a non-PT state — ask payroll which state’s rules apply to your salary. The answer depends on your employment agreement and your employer’s payroll registration, not your physical location.

You are filing your ITR and see professional tax in Form 16 — the deduction under Section 16(iii) should already be factored into the gross salary figure shown. Cross-check the Form 16 amount against your payslip total before filing.

Your payslip shows a sudden change in the professional tax amount without any HR communication — raise it immediately. Payroll errors in professional tax can persist for months if unreported, creating a small but compounding overpayment.

You are an employee on the payroll of a state that does not levy professional tax — this deduction should not appear in your payslip at all. If it does, do not assume the employer is correct. Raise a formal payroll query with HR and request a correction and refund for any months already deducted.

Common Mistakes to Avoid

Assuming Professional Tax Is the Same as Income Tax

Professional tax and income tax are governed by completely different laws, collected by different authorities, and serve different purposes.

Treating them as the same leads to confusion when reading Form 16, comparing salaries across states, or estimating take-home pay. A Bengaluru employee and a Delhi employee on identical gross salaries will have different net credits each month — simply because of professional tax applicability.

Check your payslip: TDS and Professional Tax will always appear as separate deduction lines. They are never combined.

Thinking Every State Charges the Same Slab

Professional tax slabs are state-specific and are updated independently through state budget notifications — there is no single national slab.

An employee who assumes Karnataka’s slab applies in Maharashtra, or vice versa, may miscalculate their take-home salary by ₹100–₹300 per month. Over a financial year, that is a ₹1,200–₹3,600 error in salary planning — a meaningful difference for any household budget.

Always verify the exact slab with your employer or the state’s official commercial tax department before using any figure in your calculations.

Missing the Section 16(iii) Deduction When Filing ITR

Many first-time ITR filers are unaware that professional tax paid is deductible from gross salary under Section 16(iii) of the Income Tax Act.

If your employer has correctly reflected this in Form 16, the deduction is already captured. But if you are filing your ITR without carefully cross-referencing Form 16, you may miss this — leaving a small but legitimate tax reduction unclaimed. On ₹2,400 paid in professional tax, the income tax saving depends on your slab but is real regardless of bracket.

Always check that Form 16 reflects the correct Section 16(iii) professional tax deduction before filing.

Comparing Job Offers Across States Without Accounting for State Deductions

Two candidates receiving ₹70,000 gross monthly — one in Pune (Maharashtra) and one in Gurugram (Haryana) — will have different net salaries because Maharashtra levies professional tax and Haryana does not.

A ₹300–₹500 difference in gross salary between two offers may effectively disappear — or even reverse — once professional tax and other state-specific deductions are factored in. This catches many mid-career employees off guard when evaluating lateral moves.

Always calculate net in-hand salary, not just gross or CTC, before accepting or declining an offer. See our guide on basic salary and its payroll impact for the broader picture of how salary structures affect your actual credit.

Treating CTC as Monthly Take-Home Salary

Your Cost to Company is an annual figure that includes employer contributions, benefits, and components that never reach your bank account directly. Dividing CTC by 12 gives you gross monthly salary — not your in-hand credit.

Professional tax is one of several statutory deductions — alongside TDS, employee PF, and any other applicable levies — that reduce your monthly credit below what a simple CTC ÷ 12 calculation suggests. This misunderstanding is especially common among first-job candidates budgeting against an offer letter number.

Account for all applicable deductions, including professional tax where relevant, to arrive at a realistic monthly take-home estimate before you start spending against it.

Not Raising a Payroll Query When the Deducted Amount Looks Inconsistent

Professional tax deductions are determined by state slabs — the amount should be predictable and consistent month to month. If your payslip shows a different amount without explanation, that is a flag worth investigating.

Payroll errors in professional tax are not unheard of, particularly after salary revisions, mid-year state transfers, or system migrations. A recurring ₹100–₹200 monthly error adds up to ₹1,200–₹2,400 over a year — and most employers will correct and refund payroll errors once raised formally.

Contact your payroll or HR team with the specific month and amount. Most corrections are processed in the following payroll cycle.

When This May Not Be the Right Choice

Professional tax is a statutory levy, not a product you choose. However, there are specific situations where it may not apply to you — or where the deduction in your payslip deserves a closer look:

- You are employed in a state that does not levy professional tax — such as Delhi, Haryana, or Uttar Pradesh. If professional tax appears in your payslip and your payroll is registered in a non-PT state, this may be a payroll error that needs correcting.

- You fall into an exemption category — several states provide professional tax exemptions for individuals above a certain age, persons with disabilities, or those below a minimum income threshold. Exemption rules are state-specific and are subject to change through notifications, so verify directly with your state’s official authority.

- You are a remote employee whose payroll state differs from your work location — if your physical work location and your employer’s payroll registration are in different states, the professional tax applicability depends on the employment agreement and registration, not your home address. Clarify this directly with HR before assuming the deduction is correct or incorrect.

- Your salary is below your state’s minimum professional tax threshold — most states exempt low-income earners from professional tax entirely. If your gross salary is below the state’s floor slab, no deduction should appear.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Professional tax is governed by individual state laws, not a single central act. The following official sources are the only reliable places to verify current rules, slabs, thresholds, and exemptions:

- Your state’s Commercial Tax Department or Professional Tax Department — each applicable state publishes its official professional tax notifications, current slabs, and registration requirements on its state government website. Look for the “Commercial Taxes” or “Professional Tax” section on your state’s official government portal.

- Income Tax Department — incometax.gov.in — for understanding how professional tax is treated under Section 16(iii) of the Income Tax Act and how it is reflected in Form 16 during ITR filing.

- Your employer’s payroll or HR team — for the specific state, current slab, and registration basis used for your salary deductions. Ask for the official notification reference if the deduction amount is unclear.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Understanding where professional tax fits within your broader salary tax picture becomes clearer once you know your total taxable income. Our guide on taxable income from salary explains the full flow from gross salary to the income figure that income tax is actually applied to.

Expert Tips

- Download your payslip every month — not just at tax filing time. Professional tax errors, if left unchecked for six months, can mean ₹1,200–₹3,000 in excess deductions that are difficult to trace and recover retrospectively.

- When evaluating job offers across different states, always request an illustrative in-hand salary breakdown — not just the CTC figure. Professional tax differences can create a ₹200–₹300 monthly gap between two offers that look identical on paper.

- If your company restructures, changes payroll entities, or is acquired, verify within two to three pay cycles that your professional tax deduction reflects the correct new payroll state. System migrations frequently introduce payroll errors that persist silently for months.

- Check Form 16 every financial year to confirm the professional tax amount appears correctly under Section 16(iii). If it is missing despite monthly payslip deductions, raise this with your employer’s accounts or payroll team before filing your ITR — an understated deduction means paying slightly more income tax than necessary.

- Ask your payroll team for the specific state notification number they are using to calculate your professional tax deduction. Employers are required to follow the officially notified slab — if the deduction does not match, you have grounds to request a formal correction.

- If you are self-employed or a freelancer in an applicable state, your professional tax obligation is different from a salaried employee’s. You may need to obtain a Profession Tax Enrolment Certificate (PTEC) and remit the tax yourself via a professional tax challan to the state authority. Do not assume your salaried-employee experience covers self-employment obligations — verify with your state’s commercial tax department.

Frequently Asked Questions

What is professional tax in India for salaried employees?

Professional tax in India is a state-level tax charged on income earned through employment, trade, or profession in states that have enacted their own professional tax legislation. For salaried employees, the employer deducts the applicable amount from monthly salary and remits it to the state government. The employee sees it as a separate line in the payslip’s deductions section. The maximum annual amount any individual can be charged is ₹2,500, but the actual slab and monthly deduction depend entirely on which state’s payroll your employment falls under.

Is professional tax the same as income tax?

No — professional tax and income tax are entirely separate levies with different legal bases, governing authorities, and purposes. Income tax is a central government tax under the Income Tax Act, 1961, and applies uniformly across all of India based on your annual taxable income. Professional tax is a state government tax that applies only where state legislation has been enacted, and has a fixed annual maximum of ₹2,500. Both can appear in the same payslip as separate deduction lines — they do not replace or reduce each other, except that professional tax paid is deductible from gross salary for income tax computation purposes under Section 16(iii).

Is professional tax deducted every month?

In most applicable states, yes — professional tax is deducted monthly from salary once your income crosses the state’s minimum threshold. However, some states structure their slab so that a slightly different amount is deducted in a specific month of the year, such that the total across twelve months does not exceed the ₹2,500 annual cap. The exact monthly pattern depends on your state’s current professional tax notification. Check with your payroll team for the specific structure applied to your salary.

Which states in India have professional tax?

States that have enacted professional tax legislation include Karnataka, Maharashtra, West Bengal, Andhra Pradesh, Telangana, Tamil Nadu, Gujarat, Odisha, Kerala, Madhya Pradesh, Assam, Chhattisgarh, Bihar, Jharkhand, Meghalaya, Tripura, and Sikkim, among others. States that currently do not levy professional tax include Delhi, Haryana, Uttar Pradesh, Punjab, Rajasthan, and Himachal Pradesh. This list is not exhaustive and can change with state legislation or notifications. Always confirm with your employer’s payroll team or directly with the relevant state’s commercial tax department for the current position.

Can I get a professional tax refund?

In most cases, professional tax is not refundable — it is a statutory levy paid for the privilege of exercising a profession or employment in a state during that period. Unlike income tax, there is no annual return-filing process for employees to claim back professional tax. However, if your employer has incorrectly deducted professional tax for months when it should not have applied — for example, in a state where the tax is not levied, or in a month when your salary was below the exemption threshold — you can raise a payroll correction request with HR for a refund through the next payroll cycle.

Does professional tax reduce my taxable income?

Yes. Under Section 16(iii) of the Income Tax Act, professional tax paid during the financial year is deductible from your gross salary before taxable income is computed. Your employer reflects this in Part B of Form 16 as a deduction from gross salary. So if you paid ₹2,400 in professional tax during the year, your taxable gross salary is lower by ₹2,400 — the income tax saving depends on your applicable slab. If this deduction does not appear in your Form 16 despite monthly payslip deductions, raise it with your employer before filing your ITR.

Why is professional tax different in different states?

Because each state enacts its own professional tax law independently, as permitted under Article 276 of the Constitution of India. The Constitution only sets a ceiling of ₹2,500 per year per person — it does not standardise slabs, thresholds, exemption categories, or the occupations covered. Each state legislature decides its own slab structure, updates it through budget notifications, and administers it through its own state commercial tax department. This is why an employee in Karnataka, Maharashtra, and West Bengal on identical salaries can have meaningfully different monthly professional tax deductions.

What happens if I transfer from a PT state to a non-PT state mid-year?

Once your employment and payroll move to a non-PT state, your employer should stop deducting professional tax from the month the new state payroll applies. The professional tax already deducted for earlier months under the PT state is generally not refundable — those months were legitimately covered under that state’s rules. The months after the transfer should show zero professional tax deduction. Confirm the change with your HR team and check your payslip within two to three cycles to ensure the deduction has correctly stopped.

Is professional tax applicable if I work from home?

It depends on your employer’s payroll registration, not your physical home location. Most employers register their payroll in the state where their principal office or registered entity is located. If that state levies professional tax, it will typically be applied to your salary regardless of where you physically work from. If your employer’s payroll is registered in a non-PT state, no professional tax should be deducted even if you happen to live in a PT state. Clarify with your payroll team which state’s rules apply to your specific employment arrangement.

Can I see professional tax in my Form 16?

Yes. Your employer is required to reflect professional tax paid under Section 16(iii) in Part B of your Form 16, as a deduction from gross salary before taxable income is computed. If you received a professional tax deduction every month in your payslip but it does not appear in Form 16, this is a discrepancy worth raising with your employer’s payroll or accounts team before you file your ITR. An incorrectly prepared Form 16 can result in a slightly higher income tax computation than what is actually owed.

Final Verdict

Professional tax in India is a small but real deduction that reduces monthly in-hand salary for employees in applicable states. At a constitutional maximum of ₹2,500 per year, the absolute rupee impact is modest — but it is separate from income tax and TDS, governed entirely by your state’s own rules, and something every salaried employee in an applicable state should understand and verify.

Check your payslip for the deduction line. Confirm the amount matches your state’s current official slab. Verify your Form 16 reflects the Section 16(iii) deduction correctly each year. And if you are comparing salaries across states or evaluating a new job offer, always account for state-level deductions in your net salary calculation. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.