Most couples in India spend months planning the guest list, the venue, and the menu — and less than a week on what happens financially once the wedding is over. That gap between the last vendor invoice and the first shared monthly budget is where many new marriages hit their first real money problem. Marriage financial planning covers the full picture: estimating wedding costs, building a joint emergency fund, buying the right insurance, updating nominees, managing debt, and setting shared goals. Done before the wedding, this checklist can prevent the most common — and most expensive — mistakes Indian couples make in their first year together.

Quick Answer: Marriage Financial Planning

Marriage financial planning means preparing for wedding costs, shared monthly expenses, emergency fund, insurance, debt, and future goals before and after marriage. A couple may start by estimating a sample ₹10 lakh wedding budget, then separately planning cash reserves, health insurance, term cover, and monthly savings.

Key Takeaways

- A typical mid-range Indian wedding costs ₹10–₹25 lakh depending on city, guest count, and venue — build an itemised budget per category before approaching a single vendor.

- Newly married couples in Tier-1 cities should target an emergency fund of ₹2.5–₹4 lakh — equivalent to 6 months of combined household expenses.

- After marriage, your term insurance cover should be at least 10 times your annual income — for someone earning ₹95,000/month, that means a minimum of ₹1.14 crore of life cover.

- A ₹10 lakh personal wedding loan at 15% over 3 years adds approximately ₹1.24 lakh in interest — money that could instead fund 12 months of goal-based SIP investments.

- Update nominees on all bank accounts, EPF, PPF, mutual fund folios, and insurance policies within 30 days of receiving your marriage certificate.

- A ₹10 lakh family floater health insurance plan for a couple aged 25–30 typically costs ₹12,000–₹18,000 per year — and is entirely separate from your employer group cover.

Key Facts at a Glance

| Financial Pillar | Target or Rule | When to Act |

|---|---|---|

| Wedding budget | Set itemised cap before booking any vendor | 12+ months before the wedding |

| Emergency fund | 6 months of combined household expenses | Build before the wedding |

| Term insurance | Minimum 10× annual income per earner | Within 3 months of marriage |

| Health insurance | ₹10 lakh family floater (add spouse) | Before or at the time of marriage |

| Nominee update | All accounts, EPF, PPF, and policies | Within 30 days of marriage |

| Goal-based SIP | Start the month after the wedding | Month 1 post-wedding |

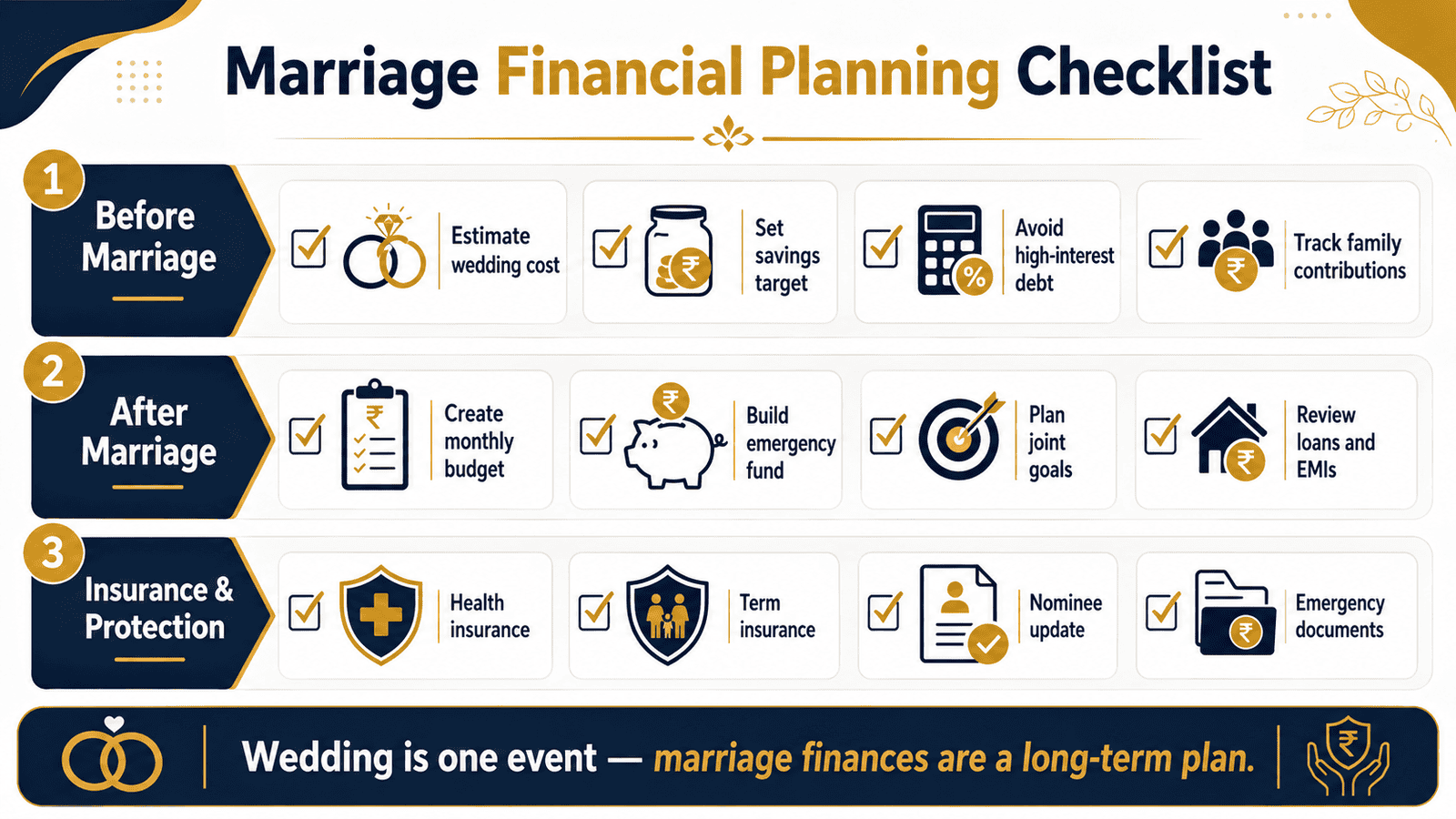

How to Approach Marriage Financial Planning in India

There are five pillars every Indian couple should address — ideally in the 12 months before the wedding and the 3 months immediately after. Skipping even one creates a gap that tends to become more expensive to fix over time.

Pillar 1: Wedding Cost Planning

Start with the number you can fund entirely from savings — without borrowing a single rupee. Then build backwards to an itemised breakdown. Most couples underestimate wedding costs by 20–30% because they forget smaller line items: travel for outstation guests, last-minute alterations, tips, and post-wedding hospitality.

A mid-range wedding in a Tier-1 Indian city typically spans these categories:

| Wedding Expense Category | Typical Range (₹) | Common Underestimation |

|---|---|---|

| Venue and decoration | 2,50,000–6,00,000 | Décor add-ons agreed late |

| Catering | 1,50,000–4,00,000 | Guest count revised upwards |

| Photography and videography | 60,000–2,00,000 | Pre-wedding shoot not budgeted |

| Clothes, jewellery, and grooming | 1,00,000–4,00,000 | Jewellery almost always doubles the estimate |

| Travel, return gifts, miscellaneous | 50,000–1,50,000 | Return gifts always cost more than planned |

Every rupee borrowed for the wedding carries 12–18% annual interest on a standard personal loan. Decide your ceiling first, build a savings plan to reach it, and treat that ceiling as non-negotiable before your first vendor meeting.

Pillar 2: Post-Marriage Household Budget

Shared rent, groceries, utilities, insurance premiums, and EMIs all need a single, transparent plan after marriage. A practical starting framework is the 50-30-20 rule: 50% of take-home income to needs, 30% to wants, 20% to savings. Apply it to your combined income, then adjust for your actual cost structure in your city. Read the full monthly budget rule guide to build your first joint household budget from scratch.

Pillar 3: Emergency Fund

An emergency fund for a married couple covers 6 months of combined household expenses — not individual expenses. For a Pune couple spending ₹50,000/month on rent, groceries, utilities, and transport, that target is ₹3,00,000. Keep it in a savings account or overnight liquid mutual fund, never in equity. Build this before the wedding, not after. Use the emergency fund amount calculator to find the right target for your specific household costs.

Pillar 4: Insurance Checklist After Marriage

Term insurance: Marriage increases your financial dependents. At minimum, hold life cover equal to 10 times your annual income — the amount that can replace your income for roughly a decade, allowing your spouse to sustain their lifestyle and clear shared debt. Use the term cover estimate guide to calculate the right figure for your income and liabilities.

Health insurance: Add your spouse to your individual plan where the insurer permits it, or buy a dedicated family floater covering both of you at a minimum ₹10 lakh sum insured. Do not rely solely on employer group cover — it terminates the day you leave that job.

Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing. Premiums vary by age, health status, insurer, and sum insured. Always compare options from IRDAI-registered insurers at irdai.gov.in before deciding.

Pillar 5: Shared Financial Goals

Once the checklist above is complete, sit down together and list your goals: home down payment, children’s education, international travel, retirement. Assign each goal a rupee target and a timeline, then work backwards to a monthly savings figure. Goal-based SIP investing through mutual funds is one of the most practical tools for Indian couples to build towards large future targets with consistent small contributions over time.

Real Example: Ankit and Priya’s 12-Month Marriage Plan

Ankit, 29, is a software engineer in Pune earning ₹95,000 per month. His fiancée, Priya, 27, earns ₹65,000 per month at an IT company in the same city. They plan to marry in 12 months. Combined savings: ₹4 lakh. Estimated wedding budget: ₹12 lakh, with ₹4.5 lakh expected from both families.

Their couple’s share: ₹12,00,000 − ₹4,50,000 = ₹7,50,000. From their ₹4 lakh savings, they allocate ₹2.5 lakh to the emergency fund and ₹1.5 lakh to the wedding corpus. Balance to save over 12 months: ₹6,00,000 at ₹50,000/month jointly.

On insurance: Ankit holds ₹75 lakh of term cover — insufficient post-marriage. He upgrades to ₹1.14 crore (12 times his annual income). Priya has no standalone health insurance. She buys a ₹10 lakh family floater at approximately ₹15,000/year before the wedding date.

Both update nominees on EPF, PPF, savings accounts, and mutual fund folios within 30 days of the marriage certificate being issued.

Key insight: By ring-fencing the emergency fund first and treating it as untouchable, Ankit and Priya protect themselves against any financial shock during the wedding planning period — exactly when most couples are most financially exposed.

How to Calculate Your Monthly Wedding Savings Target

Monthly Savings Required = (Wedding Goal − Existing Savings Earmarked − Family Contribution) ÷ Months to Wedding

Using Ankit and Priya’s numbers step by step:

Step 1: Wedding budget = ₹12,00,000

Step 2: Less family contribution = ₹4,50,000

Step 3: Less earmarked savings = ₹1,50,000

Step 4: Balance to save = ₹6,00,000

Step 5: Monthly savings required = ₹6,00,000 ÷ 12 = ₹50,000/month

Park this in a recurring deposit or liquid mutual fund — not a regular savings account. Use the goal SIP estimate calculator to model different timelines and return scenarios, and the goal-based SIP planner to map each post-marriage financial goal to a specific monthly investment amount.

| Scenario | Monthly Savings | Corpus at 12 Months |

|---|---|---|

| ₹50,000/month, no returns (savings account) | ₹50,000 | ₹6,00,000 |

| ₹45,000/month at 6% p.a. (liquid fund) | ₹45,000 | ≈₹5,57,000 |

| ₹50,000/month at 6% p.a. (liquid fund) | ₹50,000 | ≈₹6,19,000 |

A 6% return on a liquid fund adds approximately ₹19,000 over 12 months on a ₹50,000/month saving rate. Small gain — but it costs nothing extra to choose a liquid fund over a savings account for a 12-month wedding corpus.

Comparison: Wedding Loan vs Wedding Fund (Savings-First)

| Parameter | Wedding Loan | Wedding Fund |

|---|---|---|

| Interest cost | 12–18% p.a. | Nil |

| Monthly EMI (₹10L over 3 years) | ≈₹33,000–₹36,000/month | None after the wedding |

| Total interest paid on ₹10L | ≈₹1.2L–₹1.9L | ₹0 |

| Starting marriage with debt | Yes | No |

| CIBIL score impact | High if EMI is missed | No impact |

| Budget discipline required | Low upfront, high for 3 years after | High upfront, free after the wedding |

| Best suited for | Genuine emergency — no other option | Anyone who plans 12+ months ahead |

| Risk level | High | Low |

A wedding loan is not categorically wrong — but every rupee of EMI over the next 3 years is a rupee that cannot go towards your emergency fund, insurance premium, or first home down payment.

How to Decide What’s Right for You

you are the sole earner in the new household or have ageing parents as dependents — THEN buy or increase your term insurance cover before the wedding date, not after.

your combined take-home is above ₹1.5 lakh/month and the wedding is 12 or more months away — THEN pursue a savings-first approach with zero borrowing for the wedding.

your existing EMIs already exceed 30% of your take-home pay — THEN do not add a wedding loan. Scale down the wedding before adding more debt to your monthly obligations.

your spouse currently has no standalone health insurance outside employer cover — THEN buy a family floater before the wedding date, not at the next annual policy renewal.

you have not yet had a full financial conversation with your partner — covering salary, savings, existing debts, credit score, and investments — THEN do a combined net worth review before making any joint financial commitment.

you have a 3–6 month emergency fund already in place — THEN build that before increasing your wedding budget. A medical emergency in your first year of marriage should not leave you with credit card debt at 36–42% annual interest.

Common Mistakes to Avoid

Budgeting Only for the Wedding, Not the Year After

Most couples plan for the wedding day but ignore the first-year setup spike: new home, furniture, appliances, and a possible income drop if one partner takes a career break.

This can cost ₹3–₹5 lakh before any regular investing begins. Build a post-wedding budget covering at least 3 months of new household expenses before the wedding date.

Raiding the Emergency Fund for a Bigger Wedding

Spending emergency reserves on a larger venue or extra guests is a costly shortcut. A ₹1 lakh medical bill in month two of marriage with no cash reserve forces a credit card loan at 36–42% interest annually.

Reduce the wedding budget before touching the emergency fund. Never the other way around.

Not Updating Nominee Details

Bank accounts, PPF, EPF, mutual fund folios, and insurance policies all carry nominee records. Without updating them after marriage, legal delays of 12–24 months are common before assets reach your spouse in a worst-case scenario.

Set a calendar reminder: complete all nominee updates within 30 days of receiving your marriage certificate.

Carrying an Undersized Term Cover Into Marriage

A ₹25–₹50 lakh term plan bought in your early twenties is almost always insufficient after marriage. At a 12% assumption, ₹50 lakh replaces fewer than 5 years of ₹95,000/month income — far short of what a dependent spouse would need.

Review your cover amount at every major life milestone. Marriage always qualifies.

Mixing Wedding Savings With the Emergency Fund

Keeping both in one account makes it trivially easy to fund a vendor advance from your emergency reserves without realising it.

Use two separate accounts from day one — or one savings account and one liquid mutual fund.

Taking a Wedding Loan Without Modelling the EMI

A ₹10 lakh personal loan at 15% over 3 years carries a monthly EMI of approximately ₹34,665 and a total interest outgo of ₹1.24 lakh. On a ₹95,000 monthly salary, that leaves very little room for savings, insurance, or any unplanned expense for the next 36 months.

Calculate the exact EMI before you sign — then decide if that is the wedding worth starting your financial life with.

When This May Not Be the Right Choice

The planning framework in this article assumes a baseline of financial stability. It may not apply cleanly if:

- You or your partner currently carry high-interest debt totalling over ₹3 lakh — clear that before adding new insurance premiums, wedding savings, and investment obligations.

- Your combined monthly take-home is below ₹40,000 — a ₹10 lakh wedding budget creates disproportionate financial pressure at this income level. A simpler ceremony and a strong financial foundation is the more practical starting point.

- You are planning marriage within 3 months with no existing savings — the 12-month planning framework cannot be compressed into 90 days without taking on avoidable debt.

- One partner is unwilling to share income, savings, or debt information openly — joint financial planning without full transparency does not work.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Marriage-related financial decisions span insurance, investments, and tax — all regulated domains. The key official sources to consult before acting:

- IRDAI (irdai.gov.in) — Insurance regulations, registered insurer verification, and policyholder guidelines. Before buying any health or term plan, verify the insurer’s registration here. Review the health cover basics guide to understand what standard plans do and do not cover.

- SEBI (sebi.gov.in) — Mutual fund and SIP regulations, fund performance data, and registered investment advisor verification.

- Income Tax Department (incometax.gov.in) — Section 80C and 80D deduction limits and rules applicable to individuals and married couples.

- RBI (rbi.org.in) — Personal loan regulations, interest rate benchmarks, and banking consumer rights.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Pay wedding vendors in staged instalments — not lump sums upfront: Most venues and photographers accept a 20–30% advance to hold the date. Spreading payments preserves your monthly cash flow across the 12-month planning window rather than locking it up in advance.

- Open a dedicated joint savings account purely for wedding expenses: Separate from your emergency fund and individual accounts. Visibility into one shared number prevents last-minute overspending when vendor add-ons arrive.

- Buy term insurance before you turn 30: A ₹1 crore term plan at age 28 costs approximately ₹10,000–₹12,000 per year with most IRDAI-registered insurers. The same plan at 35 typically costs ₹15,000–₹20,000. Every year of delay is a permanent cost increase.

- Compare family floater premiums across at least 3 IRDAI-registered insurers: Premiums for an identical ₹10 lakh family floater can vary by ₹4,000–₹6,000 per year for the same couple profile. Do not buy the first quote you see.

- Start your first goal-based SIP the month after the wedding — not when you feel ready: ₹5,000/month in an equity mutual fund held for 10 years at a 10% average return grows to approximately ₹10.3 lakh. Waiting 12 months to start costs you roughly ₹1.5–₹2 lakh in lost compounding.

- Check both CIBIL scores 6 months before marriage: A score below 700 for either partner will reduce your joint home loan eligibility. Address errors or defaults well in advance — not after you have submitted a loan application.

Frequently Asked Questions

How much should a couple budget for a wedding in India?

There is no standard figure — it depends on city, guest count, and family expectations. A mid-range wedding in a Tier-1 city typically costs ₹10–₹25 lakh. Build an itemised budget per category and set a firm ceiling before approaching any vendor. Working backwards from a round total almost always leads to overspending.

Should I take a wedding loan or save up in advance?

Saving is almost always preferable. A ₹10 lakh personal loan at 15% over 3 years adds approximately ₹1.24 lakh in interest and a monthly EMI of ₹34,665 for 36 months. That EMI directly competes with savings, insurance premiums, and investments for your entire first 3 years of marriage. If borrowing is unavoidable, keep the amount as small as possible and the tenure as short as your EMI capacity allows.

What insurance should a couple buy immediately after marriage?

Two at minimum: a term insurance plan covering at least 10 times the annual income of each earning partner, and a ₹10 lakh family floater health insurance plan. Employer group health cover is not a substitute — it ends the day you change jobs. Insurance is a subject matter of solicitation; read the policy document carefully before purchasing.

Can I add my spouse to my existing health insurance policy?

In most cases, yes. Marriage is a standard trigger event for mid-term endorsement. Contact your insurer within 30–90 days of marriage — the exact window varies by insurer and plan. If that window has passed, port to a family floater plan at the next renewal. Always verify the specific terms in your policy document.

What is a reasonable emergency fund for a newly married couple?

Six months of combined household expenses. For a couple in Pune spending ₹50,000/month on rent, groceries, utilities, and transport, the target is ₹3,00,000. Keep it in a savings account or overnight liquid mutual fund — not in equity or fixed deposits with lock-in periods.

What happens if I do not update nominees after marriage?

Your existing nominee — typically a parent — stays on record. In the event of your death, your spouse may need to go through a lengthy legal process to claim those assets, which can take 12–24 months. Update nominees on all bank accounts, EPF, PPF, mutual fund folios, and insurance policies within 30 days of receiving your marriage certificate.

Should newly married couples maintain joint or separate bank accounts?

Both work — what matters is transparency. Many couples maintain individual accounts for personal spending and a shared joint account for rent, EMIs, groceries, and savings goals. The non-negotiable requirement is that both partners have full visibility into the combined financial position at all times.

Is term insurance necessary even when both partners earn?

Yes. Even in a dual-income household, the loss of one earner changes the entire financial plan — especially with a home loan, planned children, or ageing parents in the picture. Both earning partners should hold individual term covers sized to their respective incomes and shared liabilities.

When should a couple start investing together?

The month after the wedding — not after settling in or feeling financially comfortable. Every month of delay on a goal-based SIP has a measurable cost. ₹10,000/month started 12 months later reduces a 10-year corpus by approximately ₹2 lakh at a 10% annualised return.

Final Verdict

Marriage financial planning is not just about affording a wedding — it is about starting your shared financial life without gaps in insurance, without avoidable debt, and with a clear plan for what comes next. Couples who address all five pillars — wedding budget, household budget, emergency fund, insurance, and shared goals — before the wedding day are in a significantly stronger financial position one year in compared to those who plan it afterwards.

Start with the most urgent gap in your current situation: no emergency fund, insufficient term cover, or no joint budget. Fix one thing at a time, in order of priority. Use the tools and guides on Ridhi.com to model your monthly savings target and insurance needs before your next major financial commitment.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Ishita Sharma writes about goal-based financial planning for Indian families and individuals. Her content connects saving, budgeting, investing, insurance, and debt decisions to real-life goals such as child education, marriage, retirement, home buying, emergency funds, family protection, and long-term wealth building.

She covers topics such as child education planning, marriage goal planning, retirement planning, home-buying goals, inflation-based goal estimation, monthly investment planning, savings timelines, emergency buffers, asset allocation basics, family financial milestones, and goal calculators.

Ishita’s writing is structured, thoughtful, and decision-oriented. She helps readers move from vague goals like “save more” to clearer questions such as how much may be needed, by when, what assumptions matter, and what trade-offs exist. Her articles use Indian examples, timelines, ₹ amounts, and simple planning frameworks. Her content is educational and should not be treated as personalised investment, tax, loan, or insurance advice. Since future costs, inflation, returns, product rules, and tax treatment can change, readers should verify current information before acting.