You get a job offer. It says ₹12,00,000 CTC. Quick mental math: ₹1,00,000 a month. You plan your rent, set a SIP target, tell your family the number. Then the first salary arrives: around ₹86,500 in a no-TDS month. That missing ₹13,500 is not a payroll error. It is exactly how CTC vs in-hand salary works in India — and most employees never get a straight explanation of where it goes.

This article breaks down every component hiding inside your CTC, names every deduction between your offer letter and your bank account, and walks through the calculation with real ₹ figures. Whether you are evaluating a new offer or simply trying to understand your payslip, you will know precisely what each number means by the time you finish reading.

Quick Answer: CTC vs In-Hand Salary

CTC vs in-hand salary: your CTC is the total annual cost your employer spends on you, including EPF, gratuity, and insurance. Your in-hand salary is what reaches your bank account after deductions. For most Indian salaried employees, in-hand salary is 65–87% of their CTC, depending on tax bracket, EPF structure, professional tax state, variable pay, and tax regime.

How to Calculate In-Hand Salary from CTC

Monthly In-Hand Salary = Monthly Gross Salary − Employee EPF − Professional Tax − TDS (Income Tax)

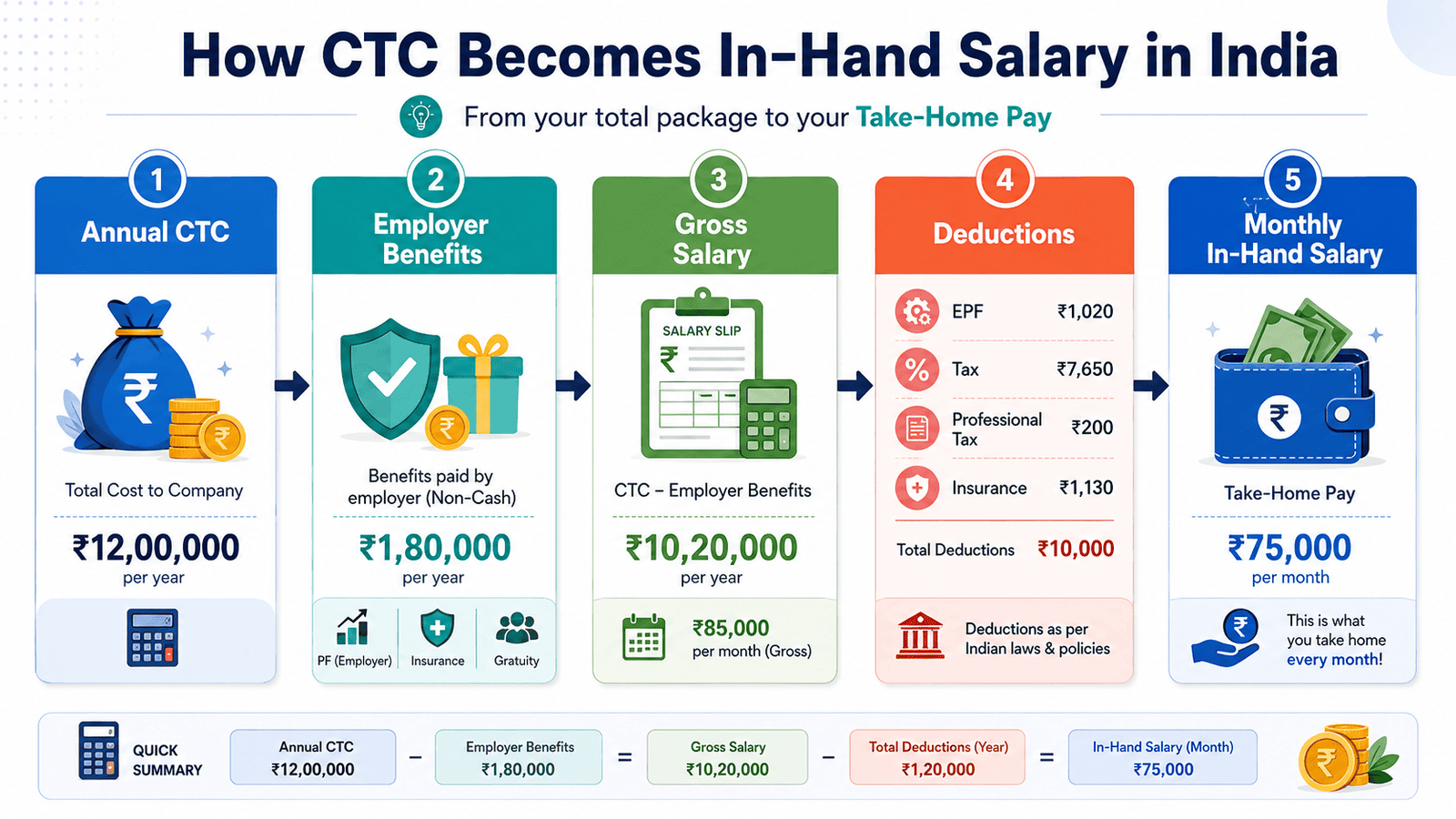

There are four steps between your CTC and your bank account. Each one removes a layer.

Step 1 — Find Your Gross Salary

Gross salary is the total cash your employer pays you before any deductions — basic salary, HRA, special allowance, LTA, and variable pay. To arrive here from CTC, subtract all employer-side costs: employer EPF, gratuity provision, and health insurance premium. These costs are inside your CTC but never appear as income on your payslip.

Gross Salary = CTC − Employer EPF − Employer Gratuity − Employer Insurance

For a typical ₹12L CTC structure, gross salary works out to approximately ₹10,98,000/year — ₹91,500/month.

Step 2 — Deduct Employee EPF

You generally contribute 12% of your basic salary plus dearness allowance to your EPF account every month in covered establishments. On a basic of ₹40,000, that is ₹4,800/month. This money goes to your EPFO account — not the government, and not lost. It earns interest each year and can be withdrawn at retirement or resignation under specific conditions.

Step 3 — Deduct Professional Tax

Professional tax is a small state-level deduction that many first-time employees miss entirely when planning their budget. Rates vary significantly: Maharashtra and Karnataka can go up to ₹2,500/year, Karnataka typically deducts ₹200 per month and ₹300 in February above the applicable salary threshold, while Delhi, Haryana, and Rajasthan generally do not levy professional tax on salaried employees. Many employees in PT-applicable states see around ₹150–₹250 deducted in a normal month depending on their state and salary slab.

Step 4 — Deduct TDS

Your employer estimates your full-year tax liability at the start of April, divides by 12, and deducts that amount monthly as TDS. The figure depends on which tax regime you choose and what investments or deductions you declare. Under the new tax regime for salaried individuals, the standard deduction is ₹75,000 for AY 2026-27. This directly reduces your taxable salary before the slab calculation and Section 87A rebate are applied. Use our CTC to in-hand salary calculator to compute your exact take-home.

Approximate In-Hand at Common CTC Levels

| Annual CTC | Approx Monthly Gross | Approx Monthly In-Hand |

|---|---|---|

| ₹5,00,000 | ₹38,000 | ₹35,500–₹36,500 |

| ₹8,00,000 | ₹61,000 | ₹57,000–₹58,500 |

| ₹12,00,000 | ₹91,500 | ₹86,000–₹87,000 |

| ₹18,00,000 | ₹1,37,000 | ₹1,17,000–₹1,22,000 |

| ₹25,00,000 | ₹1,88,000 | ₹1,55,000–₹1,60,000 |

Key Takeaways

- Your CTC commonly includes employer EPF (generally 12% of basic plus dearness allowance in covered establishments, with the employer share split as per EPFO rules) and gratuity provisioning (commonly shown around 4.81% of basic) — employer costs that go to separate accounts, never your bank. On a ₹12L CTC, these account for approximately ₹6,700/month that never reaches you as spending money.

- Three deductions reduce your gross salary to in-hand: employee EPF, professional tax, and TDS. For employees in the ₹8L–₹15L CTC range, TDS is typically the largest of the three.

- Employees in Delhi, Haryana, and Rajasthan pay ₹0 professional tax. Employees in Maharashtra and Karnataka can lose up to ₹2,500/year to it, depending on the applicable salary slab and month.

- If your annual salary income is up to ₹12.75 lakh under the new regime, the ₹75,000 standard deduction can reduce taxable income to ₹12 lakh and the Section 87A rebate can make tax nil, except for special-rate income such as certain capital gains.

- Variable pay (performance bonus) is usually part of your annual CTC but paid quarterly or annually — it does not appear in your regular monthly in-hand figure.

- For regular employees, gratuity is generally payable after 5 continuous years of service, except in cases such as death or disablement where the 5-year condition does not apply. It is part of CTC but is not accessible as monthly income.

Key Facts at a Glance

| Salary Component | Part of CTC? | Reaches Your Bank? |

|---|---|---|

| Basic Salary | Yes | Yes — fully taxable |

| HRA | Yes | Yes — HRA exemption may apply under the old regime if rent conditions are met |

| Special Allowance | Yes | Yes — fully taxable |

| Leave Travel Allowance | Yes | Yes — LTA exemption may apply under the old regime when valid travel conditions and proof are met |

| Employer EPF (12% of basic) | Yes | No — your EPFO account, not bank |

| Gratuity (4.81% of basic) | Yes | No — lump sum after qualifying service, usually 5 years for regular employees |

| Group Health Insurance | Some | No — covers hospitalisation costs |

| Employee EPF (deduction) | N/A | No — deposited to your EPFO account |

| Professional Tax (deduction) | N/A | No — remitted to the applicable state government where PT applies |

| TDS / Income Tax (deduction) | N/A | No — excess TDS can be claimed as refund through ITR if eligible |

Understanding CTC vs In-Hand Salary in India

What CTC Actually Means

CTC — Cost to Company — is the total amount your employer spends to keep you employed each year. It is not your salary. It is your salary plus all employer-side costs: EPF contribution, gratuity provision, health insurance premium, and any other benefit the company funds on your behalf. When a company quotes “₹12 lakh CTC,” their payroll budget for you is ₹12 lakh annually. That number is useful for comparing offers. It is a poor number to use when planning your monthly budget or EMI.

Gross Salary: The Cash You Are Paid Before Deductions

Gross salary is the cash portion of your CTC — every component that appears as income on your payslip. Basic salary, HRA, special allowance, LTA, variable pay. Employer EPF, gratuity, and insurance are not part of gross salary; they are employer costs layered on top of your gross salary to arrive at CTC. To fully understand your salary slip, remember: gross salary — not CTC — is the starting point for all deductions. Your payslip deductions come out of gross, not CTC.

Why Basic Salary Is the Anchor Number

Basic salary is typically 40–50% of gross salary and is the single most important figure in your pay structure. Both your employee EPF deduction and your employer’s EPF contribution are generally calculated at 12% of basic wages plus dearness allowance in covered establishments. Your gratuity is 4.81% of basic. Your HRA exemption is calculated as a percentage of basic. A lower basic salary means lower EPF deductions and a higher monthly in-hand — but a smaller EPF corpus at retirement. To understand exactly how EPF is calculated and how your corpus compounds over a career, see our dedicated guide.

HRA and Its Tax Effect on Take-Home

HRA is typically 40–50% of basic and appears as income on your payslip. If you live in rented accommodation and choose the old tax regime, a portion of your HRA may be exempt from income tax if you meet the rent-payment conditions and keep proof. If you own your home or live in company housing, the full HRA is taxable. Checking HRA exemption rules before submitting your investment declaration to HR can change your monthly TDS by ₹1,000–₹4,000 depending on the rent you pay and your basic salary level.

How Income Tax Reduces Your Monthly In-Hand

Your employer estimates your annual tax liability each April and deducts one-twelfth of it every month as TDS. The amount depends on your gross salary, which tax regime you choose, and the investments or deductions you declare to HR. Under the new tax regime for AY 2026-27, the standard deduction of ₹75,000 directly reduces taxable income, and Section 87A can make regular salary income tax-free up to an effective salary level of ₹12.75 lakh. For a full breakdown of how TDS is computed each month, see our guide on income tax on salary.

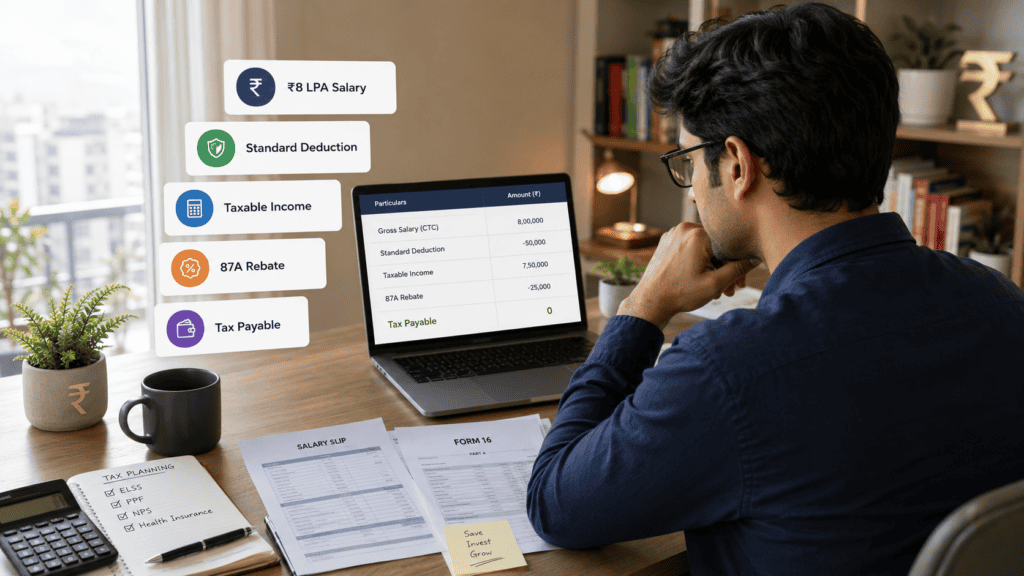

Real Example: Priya’s ₹12 Lakh CTC, Decoded

Priya, 27, is a product analyst at a Bengaluru tech startup. Her offer letter shows ₹12,00,000 CTC. Here is exactly how that figure breaks down and what she actually receives each month.

| CTC Component | Annual (₹) | Monthly (₹) |

|---|---|---|

| Basic Salary | 4,80,000 | 40,000 |

| HRA (50% of basic) | 2,40,000 | 20,000 |

| Special Allowance | 2,94,000 | 24,500 |

| Leave Travel Allowance | 24,000 | 2,000 |

| Variable Pay (paid annually) | 60,000 | — |

| Gross Salary | 10,98,000 | 91,500 |

| Employer EPF (12% of basic) | 57,600 | 4,800 |

| Gratuity (4.81% of basic) | 23,088 | 1,924 |

| Group Health Insurance | 21,312 | 1,776 |

| Total CTC | 12,00,000 | 1,00,000 |

Priya opts for the new tax regime for FY 2025-26 / AY 2026-27 and has no special-rate income such as capital gains. Her monthly deductions:

- Employee EPF (12% of ₹40,000 basic): ₹4,800

- Professional Tax (Karnataka): ₹200 in most months and ₹300 in February

- TDS (new regime, regular salary income within the effective ₹12.75L salaried threshold): ₹0

- Total deductions: ₹5,000/month in most months

Monthly in-hand: ₹91,500 − ₹5,000 = ₹86,500

Priya receives around ₹86,500 in her bank in most months — about 86.5% of the monthly CTC figure of ₹1,00,000. In February, Karnataka professional tax can make the number ₹100 lower. The remaining CTC gap is split across her EPFO account, gratuity provisioning, health insurance costs, and state-level professional tax. None of it is necessarily lost — but most is not accessible as spending money today. That is the gap nobody explains until the first salary arrives.

Comparison: CTC vs In-Hand Salary

| Parameter | CTC | In-Hand (Net) Salary |

|---|---|---|

| What it represents | Total annual employer cost — all benefits included | Cash deposited in your bank account monthly |

| Includes employer EPF? | Yes | No |

| Includes gratuity? | Yes | No |

| Tax already deducted? | No | Yes — TDS removed |

| Best used for | Comparing job offers | Monthly budgeting and EMI planning |

| Home loan eligibility | Sometimes accepted | Preferred by most lenders |

| Shown on Form 16? | Not directly | Salary, deductions, and TDS details are reflected in Form 16 where applicable |

How to Decide What’s Right for You

you are comparing two job offers at similar CTCs — THEN request the gross salary and basic salary percentage from both companies. A ₹12L CTC with 50% basic gives a higher EPF corpus but lower monthly in-hand than a ₹12L CTC with 35% basic, even when income tax is nil under the new regime. The right structure depends on whether you prioritise take-home today or a larger retirement fund later.

your annual salary income is up to ₹12.75 lakh under the new regime — THEN your taxable income can fall to ₹12 lakh after the ₹75,000 standard deduction and Section 87A can reduce regular slab-tax liability to nil, meaning your monthly in-hand may be gross salary minus EPF and professional tax only.

you pay rent above ₹12,000/month in a metro city and have 80C investments above ₹1 lakh — THEN compare your tax liability under both regimes before declaring your choice to HR. The old regime may give you meaningfully higher monthly in-hand. See our old vs new tax regime guide to calculate which suits your profile.

your salary structure loads most of the CTC into special allowance and keeps basic low (below 35% of gross) — THEN your monthly in-hand is higher now, but your EPF corpus will be noticeably smaller after 20 years. The trade-off is ₹3,000–₹5,000 more per month today versus a reduced retirement balance.

your CTC includes ESOPs or equity grants — THEN the headline CTC overstates your accessible monthly income. Your actual cash in-hand may be ₹20,000–₹50,000 lower than a standard CTC-to-in-hand calculation suggests, since equity vests over 3–4 years and depends on company performance.

you have completed 5 continuous years at your current employer — do not count gratuity as accessible savings or include it in your monthly budget. Leaving before 5 years means forfeiting this component of your CTC entirely in most standard employment structures.

Common Mistakes to Avoid

Dividing CTC by 12 to Estimate Monthly Pay

The most common mistake freshers make: divide CTC by 12 and assume that is their monthly take-home. It is not. Employer EPF, gratuity, and insurance — already inside the CTC — never appear in your bank account. On a ₹12L CTC, this creates a gap of ₹8,500/month before any deductions are applied.

Always ask HR for the gross salary figure, then work out deductions from there.

Not Asking for the Salary Breakup Before Accepting an Offer

Two offers at the same CTC can result in very different monthly in-hand figures depending on the basic salary percentage. Higher basic means higher employee EPF deduction, higher employer PF cost inside CTC, and higher gratuity provisioning — all of which reduce accessible monthly income. Many companies share a one-line CTC number; always request the full breakup showing each component before signing.

Treating Variable Pay as Monthly Income

Performance bonuses, sales incentives, and annual increments are often counted in CTC but paid quarterly or annually. A ₹12L CTC with ₹1,20,000 in variable pay means only ₹10,80,000 in guaranteed fixed gross — and even variable pay depends on appraisal ratings and company performance.

Build your monthly budget on fixed gross salary only. Treat variable pay as a bonus when it arrives, not as a guaranteed monthly entitlement.

Ignoring Professional Tax in Monthly Budget Planning

Employees in Maharashtra and Karnataka routinely forget professional tax when estimating their first in-hand. At ₹200 in most months and ₹300 in February in Karnataka above the applicable threshold, that is ₹2,500/year quietly absent from every monthly plan. Small — but it causes a recurring surprise for employees who don’t account for it upfront.

Verify your state’s professional tax rate and salary slab before finalising your budget.

Not Declaring Investments to HR Before the April Deadline

If you skip your annual investment declaration to HR, your employer defaults to maximum TDS — treating your full gross salary as taxable without any deductions. You will get a refund via ITR, but your monthly in-hand is lower all year and the refund takes months to process. Submit investment declarations in April and update them if your financial situation changes significantly mid-year.

Assuming Employer EPF Is a Bonus Over and Above Salary

Employer EPF is already inside the CTC your recruiter quoted. It is not extra money given to you on top of salary — it is a cost the company has already counted in the ₹12L total. When a recruiter mentions “employer PF as an added benefit,” they are describing a component already built into the CTC figure they showed you. Do not factor it as additional income when comparing two offers at the same CTC.

When This May Not Be the Right Framework

The standard CTC-to-in-hand calculation works well for most regular salaried employees — but four situations produce meaningfully different results.

If your CTC includes a significant ESOP or equity grant (especially common at early-stage startups), the headline CTC overstates guaranteed cash income. ESOPs typically vest over 3–4 years and depend on company performance. Your actual monthly cash in-hand could be ₹20,000–₹60,000 lower than a CTC-based estimate suggests.

If your salary includes reimbursement-heavy components — fuel, driver, books, telephone allowance — those components are inside CTC but require you to submit bills monthly. If you do not claim them, you do not receive them, and the formula does not apply accurately.

If you are freelancing or on a contract arrangement, CTC does not apply at all. As a contractor, you bear your own EPF registration, health insurance, and tax obligations — a completely different net income calculation is needed.

If your variable component exceeds 20–25% of CTC, your monthly in-hand will fluctuate with appraisal cycles and should not be modelled on a static formula built around fixed gross salary.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

EPF contribution rates, income tax slabs, standard deduction amounts, professional tax schedules, and gratuity rules can all change with each Union Budget, EPFO circular, or state government notification. Always verify current figures directly from the official source before making any financial decision.

- EPF contribution rates, account management, and passbook: EPFO — epfindia.gov.in

- Income tax slabs, standard deduction, TDS rules, and Form 16: Income Tax Department — incometax.gov.in

- Professional tax rates and salary slabs: Your state’s commercial tax or finance department portal — rates vary by state and are updated periodically

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before accepting any offer, email HR asking for the full CTC breakup showing basic, HRA, special allowance, LTA, variable pay, employer EPF, gratuity, and insurance as separate line items. If the company shares only a total number, ask for the details — the structure matters more than the headline.

- Check your EPF passbook on the EPFO member portal (epfindia.gov.in) once every quarter. Both your employee contribution and the applicable employer-side PF entries should show up. If recent months are missing, your employer may not be remitting on time — raise it with HR and follow up formally.

- If your regular salary income is up to ₹12.75L annually under the new regime, verify whether your tax liability is nil before allowing your employer to deduct TDS. Submit your tax regime choice to HR at the start of April each year and recheck your Form 16 at year-end to confirm TDS matches your actual liability .

- If your employer offers a Flexible Benefit Plan (FBP) that lets you allocate special allowance into meal coupons, books and periodicals allowance, or telephone reimbursement, use it. These components reduce your taxable income. Combined, they can add ₹1,000–₹2,000 to your effective monthly in-hand if your employer’s FBP policy and current tax rules allow it.

- For home loan applications, use your last 3 months’ salary bank credits — not your offer letter CTC — as income documentation. Most lenders calculate loan eligibility on net (in-hand) salary, and many exclude variable pay unless it is consistent across 12 months of payslips.

Frequently Asked Questions

Why is my in-hand salary so much lower than my CTC?

Because CTC includes employer-side costs — employer PF contribution, gratuity (4.81% of basic), and health insurance — that go to separate accounts, never your bank account. On top of this, your gross salary is further reduced by employee EPF, professional tax, and TDS. On a ₹12L CTC, the combined effect typically reduces monthly take-home by ₹15,000–₹20,000 compared to the monthly CTC figure.

Is employer EPF included in my CTC?

Yes. Your employer’s EPF contribution — generally linked to 12% of basic wages plus dearness allowance in covered establishments — is already counted inside the CTC they quoted you. It is not extra money given on top of salary; it is a cost the company budgeted within the total. It goes directly into your EPFO account and earns interest annually. You can access it at retirement or under specific EPFO withdrawal rules before retirement.

What is professional tax and how much is deducted monthly?

Professional tax is a state-level tax collected by your employer and remitted to the state government where it applies. The amount depends on your state and salary slab. Karnataka can deduct ₹200 in most months and ₹300 in February once salary crosses the applicable threshold; Maharashtra can go up to ₹2,500/year. Delhi, Haryana, and Rajasthan generally do not levy professional tax on salaried employees, while Gujarat can levy ₹200/month above its salary threshold.

Can I negotiate my salary structure to increase my monthly in-hand?

Yes, within limits set by your employer. If a flexible structure is offered, requesting higher special allowance and lower basic reduces your employee EPF deduction and increases in-hand. The trade-off is real: lower basic also means lower employer EPF, smaller gratuity, and reduced HRA exemption if you are renting. More monthly cash today; smaller retirement corpus and gratuity later.

What is the standard deduction on salary?

The standard deduction is a flat amount subtracted from your gross salary before income tax is calculated — no bills or proof required. Under the new tax regime for AY 2026-27, it is ₹75,000 for salaried taxpayers. If Priya’s gross salary is ₹10,98,000, her taxable income drops to ₹10,23,000 after applying this deduction — reducing her annual tax liability by approximately ₹7,500–₹11,250 depending on her applicable slab.

Is gratuity paid monthly or as a lump sum?

Gratuity is paid as a lump sum — when you resign, retire, or are terminated. It does not flow monthly even though your employer provisions for it monthly within your CTC. It becomes payable only after completing 5 continuous years of service with the same employer in standard regular employment cases. The 5-year condition is not required where employment ends due to death or disablement. Leaving before 5 years typically means forfeiting gratuity entirely under most standard employment contracts.

What percentage of CTC do employees typically receive as in-hand?

For most Indian salaried employees, in-hand salary is 65–80% of CTC. The exact figure depends on your tax bracket, basic salary as a proportion of CTC, state of employment (for professional tax), and tax regime choice. Freshers and mid-level employees with regular salary income up to ₹12.75L under the new regime can receive closer to 82–87% of monthly CTC because their TDS may be zero after standard deduction and Section 87A rebate. Senior employees in the 30% tax bracket frequently take home only 65–70% after high TDS.

What happens to the EPF deducted from my salary?

Your employee EPF contribution, generally 12% of basic wages plus dearness allowance in covered establishments, is deposited into your EPF account maintained by EPFO, alongside your employer’s matching contribution. The combined balance earns interest at the rate declared by EPFO for the relevant financial year. You can track the balance on the EPFO member portal (epfindia.gov.in). Full withdrawal is available at retirement; partial withdrawal is permitted for specific purposes such as home purchase, medical treatment, or sustained unemployment under EPFO rules.

Final Verdict

If you are a salaried employee in India — whether evaluating an offer, planning your first EMI, or simply trying to understand why your bank balance is lower than the CTC number HR gave you — understanding the CTC vs in-hand salary gap is foundational. Your CTC is what your employer budgets for you. Your gross salary is what they pay you. Your in-hand salary is the only number that pays your rent, your SIP, and your monthly commitments.

For most employees in the ₹8L–₹15L CTC range, monthly in-hand is ₹15,000–₹22,000 below the CTC-implied monthly figure. Most of that gap is employer EPF, gratuity, and income tax. Plan your budget on actual bank credits, not CTC. And each April, review your tax regime declaration with HR — the right choice can add ₹3,000–₹8,000 to your monthly take-home. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.