Every year, salaried employees across India lose money not by investing poorly — but by not knowing what’s already in their 80C deduction list. Section 80C of the Income Tax Act gives you a way to reduce your taxable income through a set of eligible investments and expenses. But all of them share a single combined cap. Your EPF contribution may already be filling a large portion of that cap before you’ve invested a single rupee elsewhere. And the entire benefit works only if you choose the old tax regime for the relevant assessment year.

This article breaks down every major option in the 80C deduction list — EPF, PPF, ELSS, LIC premiums, NSC, tax-saving fixed deposits, tuition fees, and home loan principal — along with lock-in periods, risk levels, proof documents, and the mistakes that cost people money every March. All figures in this article must be verified from official sources before filing, as limits and rules can change with each Budget.

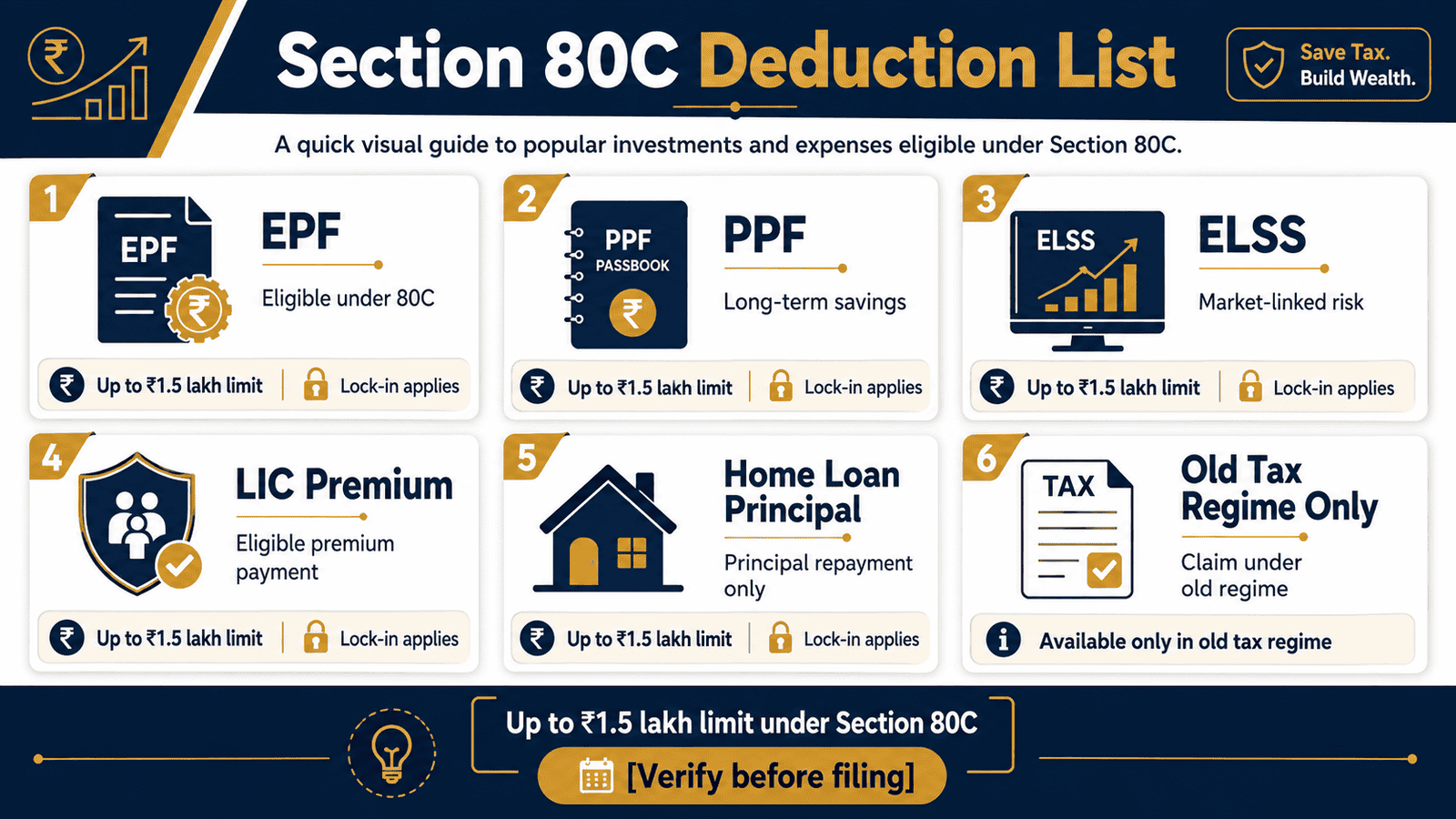

Quick Answer: 80C Deduction List

The 80C deduction list includes EPF, PPF, ELSS, eligible LIC premiums, NSC, tax-saving fixed deposits, tuition fees and home loan principal repayment. Under the old tax regime, these can reduce taxable income up to ₹1.5 lakh per year, subject to eligibility and proof rules. All options share this single cap — they do not each have a separate limit. Verify the current limit at incometax.gov.in before filing.

Key Takeaways

- The Section 80C deduction limit is ₹1.5 lakh per financial year — shared across EPF, PPF, ELSS, LIC premiums, home loan principal, and every other eligible option combined. There is no separate cap per product.

- If your basic salary is ₹60,000 per month, your employee EPF contribution alone is approximately ₹86,400 per year — over half the combined 80C limit — before you invest in anything else.

- Section 80C deductions are generally available only under the old tax regime. If you have opted for the new tax regime for the relevant assessment year, these deductions typically do not apply.

- ELSS has the shortest lock-in of any voluntary 80C investment — 3 years — but carries market risk. PPF has a 15-year lock-in and offers stable, tax-free returns with no market exposure.

- Buying a life insurance policy purely to claim the premium under 80C is one of the most common and costly tax-planning mistakes in India. The cover is usually inadequate and returns poor compared to a plain term plan plus a separate investment.

- Home loan borrowers who are already repaying EMIs may find that EPF plus principal repayment fills the 80C bucket entirely — leaving no room for PPF or ELSS.

- Verify the current deduction limit, eligible options, and regime rules from the Income Tax Department at incometax.gov.in before making any investment or filing decision.

Key Facts at a Glance

| Parameter | Detail | Notes |

|---|---|---|

| Overall 80C deduction limit | ₹1.5 lakh per financial year | Shared across all eligible options; verify current limit before filing |

| Applicable tax regime | Old tax regime | New regime generally excludes 80C deductions; verify for relevant assessment year |

| Shortest lock-in (voluntary) | 3 years — ELSS mutual funds | Market-linked; returns not guaranteed |

| Longest lock-in | 15 years — PPF | Partial withdrawal allowed from year 7; verify current interest rate |

| Tax-saving FD lock-in | 5 years | No premature withdrawal; interest is taxable; verify current rate |

| Proof for EPF | Salary slip / Form 16 | Auto-reflected; usually no separate submission required |

| Proof for LIC / insurance | Premium receipt from insurer | Submit to employer during annual investment declaration period |

| Proof for home loan principal | Annual / provisional certificate from lender | Shows principal and interest components separately |

What Is the Section 80C Deduction List — and How Does It Actually Work?

Section 80C of the Income Tax Act sits within Chapter VI-A deductions — a group of provisions that reduce your gross total income before tax is computed. Think of it as a deduction bucket with a fixed capacity. Every eligible investment you make or eligible expense you pay fills that bucket. The filled portion is deducted from your taxable income. Anything you invest beyond the cap provides no additional tax benefit — it simply spills over.

This is the concept most people miss: the 80C limit is shared across all options simultaneously. EPF, PPF, ELSS, LIC premiums, tuition fees, and home loan principal all compete within the same annual ceiling. There is no separate ₹1.5 lakh each for ELSS and another ₹1.5 lakh for PPF. It is one limit, total. Understanding this one point alone prevents most of the expensive mistakes people make in February and March.

Why Old Tax Regime Applicability Is the Real Decision Point

Many people read a 80C deduction list and immediately start planning investments — without first checking which tax regime they are on. This is the single biggest planning mistake. Under the new tax regime, Section 80C deductions are generally not available. If you or your employer have selected the new regime for the relevant assessment year, the 80C list largely becomes irrelevant for that year’s tax calculation.

Before doing anything else — before buying ELSS, before opening a PPF account — check your regime. If the old regime gives you a meaningfully lower tax liability after all deductions, then 80C planning makes sense. If the new regime is already better for your income structure, chasing 80C products may lock your money away for no tax benefit. Use a old regime deductions reference to understand where Section 80C fits alongside HRA, standard deduction, and Section 24b in the full old-regime picture.

Salary-Linked: Employee Provident Fund (EPF)

For most salaried employees, EPF is the silent 80C contributor that requires no separate decision. Every month, the employee contribution — a percentage of basic salary — flows into the EPF account automatically. This amount counts toward Section 80C each financial year. It shows on your salary slip and is captured in your Form 16.

The implication is significant. If your basic salary is ₹60,000 per month, your EPF employee contribution is approximately ₹86,400 per year. That is more than half the 80C cap consumed before you have made a single voluntary investment. Many salaried employees with higher basic salaries and home loan EMIs find the bucket already full through EPF and principal repayment alone. For a full understanding of how EPF contributions, interest, and eligibility work, see EPF rules explained.

Government Savings: PPF and NSC

Public Provident Fund (PPF) is one of the most trusted options in the 80C deduction list for conservative savers. It is government-backed, has a 15-year lock-in with partial withdrawals allowed from year 7, and allows annual contributions between ₹500 and the annual 80C ceiling. Returns are tax-free at maturity — the interest earned is not added to your taxable income. Verify the current PPF interest rate from the Ministry of Finance, as it is revised quarterly.

National Savings Certificate (NSC) is a fixed-income instrument from India Post with a 5-year maturity. One unique feature: the interest accrued each year is considered reinvested in NSC and itself qualifies as an 80C deduction in subsequent years — except in the year of maturity, when the full interest is taxable. Verify the current NSC interest rate from India Post before investing.

Market-Linked: Equity Linked Savings Scheme (ELSS)

ELSS mutual funds invest primarily in equities and qualify under Section 80C with the shortest statutory lock-in of any voluntary option — 3 years from the date of each investment. They are regulated by SEBI. Returns are market-linked and not guaranteed; past performance does not indicate future results. Long-term capital gains above a specified threshold from ELSS redemptions may be taxable — verify the applicable rate with your fund house or the Income Tax Department for the relevant assessment year. Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing.

Insurance-Linked: LIC and Life Insurance Premiums

Premiums paid toward life insurance policies issued by LIC or any IRDAI-registered insurer qualify under Section 80C, subject to conditions. The premium must generally not exceed a specified percentage of the sum assured for the policy to be fully eligible — policies issued on or after a certain date face stricter criteria. Check your specific policy’s eligibility with your insurer or IRDAI directly.

The practical caution: buying an insurance policy primarily for the 80C premium deduction is rarely good financial planning. Insurance-cum-investment products (ULIPs, endowment plans) typically deliver lower internal returns than pure investment products, and their life cover is usually inadequate. A plain term plan covers the insurance need at a fraction of the premium — leaving more room for purpose-driven investments.

Loan and Expense-Based: Home Loan Principal and Tuition Fees

The principal component of a home loan EMI on a residential property qualifies as a deduction under Section 80C. This is separate from the Section 24b deduction on interest repayment. Your lender’s annual certificate shows the principal and interest components separately — use the principal figure for your 80C claim. For the full picture of how both work together, see home loan tax benefit.

Tuition fees paid to recognised schools, colleges, or universities in India for a full-time course qualify for up to two children. Only the tuition component counts — development fees, transport, hostel charges, and donation amounts are excluded. Fees paid to overseas institutions do not qualify. Tax-saving fixed deposits with scheduled banks (5-year lock-in) and contributions to the Senior Citizens Savings Scheme (SCSS) also fall within the 80C deduction list. Interest on tax-saving FDs is taxable in the year it accrues, even if the FD hasn’t matured.

Real Example: Ankit’s 80C Bucket in Bengaluru

Ankit, 32, is a software engineer in Bengaluru earning ₹18 lakh per year, with a basic salary of ₹7.2 lakh annually — or ₹60,000 per month. He is on the old tax regime and wants to know how much room he actually has under Section 80C before buying any new product.

Step 1 — EPF employee contribution: 12% of ₹7.2 lakh = ₹86,400 per year. This is auto-deducted and reflected in his salary slip.

Step 2 — LIC term plan premium: Ankit pays ₹18,000 per year for a term insurance policy. This qualifies under 80C.

Step 3 — Home loan principal: His lender’s certificate shows ₹45,600 in principal repayment for the year.

Total already claimed: ₹86,400 + ₹18,000 + ₹45,600 = ₹1,50,000.

Ankit’s 80C bucket is entirely full — without a single voluntary investment in PPF or ELSS. If he buys ₹50,000 of ELSS in March thinking he is saving tax, he gains nothing additional from Section 80C. Understanding exactly how each payment flows into taxable income matters — use a taxable salary calculation to map this for your own salary structure.

How to Calculate Your 80C Utilisation

Before buying any 80C product, run this simple calculation to know how much room you actually have:

Eligible 80C Claim = Lower of (Total Eligible 80C Payments) or (Annual 80C Limit)

Step 1: Find your employee EPF contribution for the year from your salary slip or Form 16.

Step 2: Add eligible LIC or life insurance premiums paid during the year.

Step 3: Add home loan principal repayment from your lender’s annual certificate.

Step 4: Add tuition fees paid for children, if applicable.

Step 5: Add any voluntary investments — PPF, ELSS, NSC, or tax-saving FD.

Step 6: Cap the total at the annual 80C limit. Only the capped amount is deductible.

| Scenario | Total Eligible Payments | Deduction Claimed |

|---|---|---|

| EPF only (₹60K basic/month) | ₹86,400 | ₹86,400 |

| EPF + LIC + home loan principal (Ankit) | ₹1,50,000 | ₹1,50,000 |

| Same as above + ₹50,000 ELSS | ₹2,00,000 | ₹1,50,000 (capped; verify current limit) |

The third row is where money gets wasted every March. Investing ₹50,000 in ELSS on top of an already-full 80C bucket produces zero additional tax deduction — while locking funds for three years.

Comparison: Major 80C Options at a Glance

| 80C Option | Risk and Lock-in | Best Suited For |

|---|---|---|

| EPF (Employee contribution) | Low Risk Automatic; no separate lock-in | All salaried employees — mandatory and auto-counted |

| PPF | Low Risk 15-year lock-in | Conservative long-term savers; tax-free returns |

| ELSS Mutual Funds | Market Risk 3-year lock-in | Those comfortable with equity risk; shortest voluntary lock-in |

| LIC / Life Insurance Premium | Insurance-linked Policy term applies | Those with genuine life insurance need — not for returns |

| Home Loan Principal | Loan Repayment No separate lock-in | Home loan borrowers already in repayment |

| Tax-Saving FD | Low Risk 5-year lock-in | Those wanting guaranteed returns; interest is taxable |

| NSC | Low Risk 5-year lock-in | Conservative investors; accrued interest reinvested as 80C |

Mutual fund investments are subject to market risks. Past performance does not guarantee future returns. For a deeper analysis of how the two most popular voluntary 80C investments compare on risk, return, and liquidity, see PPF versus ELSS.

How to Decide What’s Right for You

You are currently on the new tax regime — THEN Section 80C deductions generally do not apply. Do not buy PPF, ELSS, or any product primarily for 80C saving. First check whether switching to the old regime produces a better tax outcome using the income tax calculator.

Your EPF contributions, home loan principal, and insurance premiums already total ₹1.5 lakh — THEN do not invest in PPF or ELSS for 80C purposes. There is no additional deduction to claim. Direct any further investment toward goals that do not depend on 80C.

You are on the old tax regime, have unused 80C headroom, and need stable long-term savings — THEN PPF may be worth considering. It offers government-backed, tax-free returns. But account for the 15-year lock-in and your liquidity needs before committing.

You have unused 80C room, a 5-year or longer investment horizon, and can accept equity market volatility — THEN ELSS may be worth exploring. The 3-year lock-in is the legal minimum, but equity investments typically benefit from staying invested longer.

You are considering a life insurance policy primarily for the 80C premium deduction — THEN stop and reconsider. A term plan covers your life insurance need at a fraction of the cost. The remaining 80C room is better used in PPF or ELSS aligned with actual financial goals.

You do not have a funded emergency reserve, or you expect a significant liquidity need within 3–5 years — THEN do not lock money into tax-saving FDs, NSC, or PPF. Breaking a lock-in in a financial emergency often costs more — in penalties and opportunity loss — than the original tax saving was worth.

Common Mistakes to Avoid

Assuming Each 80C Option Has a Separate Limit

A very common misconception: believing that EPF has its own ₹1.5 lakh cap, ELSS has another, and PPF has a third.

All options share a single combined limit. Investing ₹1.5 lakh in ELSS while your EPF is already at ₹80,000 means ₹80,000 of that ELSS investment generates zero additional tax deduction — and is locked away for three years anyway.

Always add up all existing 80C contributions before buying any new product.

Forgetting to Count EPF

EPF is deducted silently every month at source. Many employees forget to include it when calculating how much 80C room they have left.

A basic salary of ₹50,000 per month generates approximately ₹72,000 in EPF employee contributions per year — nearly half the 80C cap — before a single voluntary investment is made.

Pull your latest salary slip and check the EPF line before making any 80C investment decision this financial year.

Buying Last-Minute Insurance for Tax Saving

Rushing to buy a ULIP or endowment plan in February or March purely to hit the 80C limit is one of the most expensive annual traditions in Indian personal finance.

These products carry high charges, require multi-year premium commitments, and deliver inadequate life cover relative to what a term plan provides at a fraction of the premium. Missing a future renewal can lead to policy lapse and loss of invested capital.

Buy a term plan for insurance. Invest separately — and only in 80C products if you genuinely have unused headroom and they align with your goals.

Claiming 80C Deductions Under the Wrong Tax Regime

Some employees declare 80C investments to their employer even after choosing the new tax regime — expecting deductions that the new regime does not allow.

This creates a mismatch in Form 16, can cause errors in ITR filing, and may result in incorrect TDS computation for the year.

Confirm your chosen regime with your payroll team at the start of the financial year and align your investment declarations accordingly.

Missing the Employer’s Proof Submission Deadline

Most employers collect investment proof between December and February. Miss this window and your employer deducts higher TDS from your salary in the remaining months of the year.

While you can still claim the deductions when filing your ITR, the short-term cash flow impact of extra TDS can be several thousands of rupees.

Set a reminder in November each year to gather all proof — premium receipts, lender certificates, PPF statements, and ELSS fund statements — before the deadline.

Double-Counting or Misclassifying Home Loan Deductions

Home loan principal repayment falls under Section 80C. Home loan interest repayment falls under Section 24b — a separate deduction with its own limit. These are two different sections with two different rules.

Some borrowers claim the entire EMI under one section, or miss one of the two deductions entirely. Others claim both principal and interest under 80C, which is incorrect.

Your lender’s annual certificate shows both components separately. Use the principal figure for 80C and the interest figure for Section 24b.

When This May Not Be the Right Choice

Actively maximising the 80C deduction list makes sense only in specific circumstances. Here are four situations where it may not be the right priority:

- The new tax regime gives you a better outcome: If your income structure benefits more from the new regime’s lower slab rates — even without deductions — switching to the old regime just to claim 80C can result in paying more tax overall. Always run the comparison first.

- Your 80C bucket is already full: If EPF, home loan principal, and insurance premiums have consumed the full annual limit, there is no room for additional voluntary 80C investments. Any further investing should be goal-driven, not tax-deadline driven.

- You have no emergency reserve: Locking ₹1.5 lakh into PPF or a 5-year tax-saving FD without a funded emergency buffer is a liquidity risk. Unexpected expenses during the lock-in period can force costly short-term borrowing — far more expensive than the tax you saved.

- You are conflating insurance with investment: If your reason for buying an insurance-linked product is primarily the 80C premium deduction, the product is likely a poor fit. Separate your insurance planning from your tax planning entirely.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- Income Tax Department — incometax.gov.in: For the current Section 80C deduction limit, eligible investments and expenses, regime applicability, applicable assessment year rules, and ITR filing guidance.

- EPFO — epfindia.gov.in: For current EPF contribution rates, interest rate announcements, and UAN-linked passbook access to verify annual contributions.

- SEBI — sebi.gov.in: For ELSS fund regulations, scheme information documents, and mutual fund investor rights. Also check AMFI (amfiindia.com) for fund-specific disclosures.

- IRDAI — irdai.gov.in: For life insurance premium eligibility rules, policy-specific conditions, and insurer-level verification for LIC and other insurers.

- Your lender’s website or branch: For the annual interest certificate showing your home loan’s principal and interest split — essential for claiming both Section 80C and Section 24b correctly. See also home loan tax benefit for a full explanation.

Expert Tips

- In January or early February, pull your latest salary slip, home loan certificate, and insurance premium receipts and add up your total existing 80C contributions before buying anything new. Most salaried employees discover the bucket is already 70–90% full from EPF and existing commitments alone.

- If you are in the 30% tax bracket, on the old tax regime, and do have genuine unused 80C headroom — ELSS has the shortest lock-in of any voluntary option at 3 years. Consider it before the financial year ends, but only after understanding that returns are market-linked and not guaranteed.

- Request your home loan’s provisional certificate from your lender in April each year — not March. It shows estimated principal and interest for the full year ahead, letting you plan remaining 80C room accurately from the start instead of guessing in February.

- If you have two children in school or college, their tuition fees very likely qualify under Section 80C. Many employees overlook this and invest in unnecessary products when tuition alone could contribute meaningfully to the limit. Collect fee receipts that show the tuition component separately from other charges.

- Do not treat PPF and ELSS as interchangeable based on lock-in alone. PPF gives stable, tax-free, government-backed returns over 15 years. ELSS gives equity market exposure with a 3-year minimum lock-in. The right choice depends on your time horizon, risk appetite, and liquidity needs — not just which one shows up first on a list.

- Talk to your employer’s payroll or HR team in April or May about the investment declaration cycle. Knowing the submission deadline for proof documents prevents the very common problem of excess TDS deductions in the final quarter of the financial year.

Frequently Asked Questions

Is EPF included in the Section 80C deduction?

Yes. The employee’s own contribution to EPF — typically a percentage of basic salary — qualifies under Section 80C and is counted within the annual limit. The employer’s matching contribution is not included in the employee’s 80C deduction. Since this deduction happens automatically through payroll, many employees underestimate how much of the cap is already consumed before they invest voluntarily.

Is PPF better than ELSS for 80C tax saving?

Neither is universally better — they serve different purposes. PPF offers stable, government-backed, tax-free returns with a 15-year lock-in, making it better for conservative savers with long horizons. ELSS offers equity market exposure with a shorter 3-year lock-in and higher growth potential, but returns are not guaranteed. Mutual fund investments are subject to market risks. The right choice depends on your goals, time horizon, and risk tolerance — not just the tax saving.

Is LIC premium eligible under Section 80C?

Yes, life insurance premiums paid to LIC or any IRDAI-registered insurer for policies covering yourself, your spouse, or dependent children can qualify under 80C, subject to conditions. The premium must generally not exceed a specified percentage of the sum assured for the policy to be fully eligible, and policies issued on or after a particular date face tighter eligibility criteria. Verify your specific policy’s eligibility with your insurer or IRDAI for the relevant assessment year.

Can home loan principal repayment be claimed under 80C?

Yes. The principal component of your home loan EMI on a residential property qualifies as a Section 80C deduction, within the overall annual limit. This is separate from the Section 24b deduction on home loan interest, which has its own limit. Your lender’s annual interest certificate shows both components — use the principal figure for the 80C claim and the interest figure for Section 24b. Verify current eligibility conditions from the Income Tax Department.

Is Section 80C available under the new tax regime?

Generally, no. Under the new tax regime, most Chapter VI-A deductions including Section 80C are not available. If you opt for the new regime for the relevant assessment year, you forgo 80C deductions — including the benefit of your own EPF contribution being counted as a deduction. Always verify the current applicable rules at incometax.gov.in, as regime-level rules can change with each Budget.

Can I claim more than ₹1.5 lakh under Section 80C?

No. The Section 80C deduction is capped at the applicable annual limit regardless of how much you invest across all eligible options. If your total eligible payments exceed the cap, only the capped amount reduces your taxable income. Any excess investment provides no additional deduction under Section 80C — though some individual instruments may have their own supplementary deductions under other sections, such as Section 80CCD for NPS contributions above 80C.

What documents do I need to claim 80C deductions?

Documents vary by option: salary slip or Form 16 for EPF (usually auto-reflected), premium payment receipt for LIC or insurance, annual interest certificate from your lender for home loan principal, PPF passbook or account statement, ELSS fund statement with NAV and units, school or college fee receipts showing the tuition component, and FD certificate for tax-saving FDs. Keep originals organised and submit to your employer before their investment declaration deadline each year.

Does tuition fee for children qualify under Section 80C?

Yes. Tuition fees paid to a recognised school, college, university, or educational institution located in India for a full-time course qualify under Section 80C for up to two children. Only the pure tuition component counts — development fees, transport, hostel, library fees, and donations are excluded. Fees paid to institutions outside India do not qualify. Collect fee receipts that separate the tuition amount from other charges.

What is the lock-in period for ELSS mutual funds?

ELSS funds have a statutory lock-in of 3 years from the date of each investment, making them the shortest-lock-in option among voluntary 80C investments. Units cannot be redeemed before 3 years. After the lock-in period, there is no obligation to sell — many investors stay invested longer to benefit from potential equity growth. Mutual fund investments are subject to market risks; returns are not guaranteed.

Can a husband and wife both claim Section 80C separately?

Yes. Each individual taxpayer has an independent annual 80C limit. A husband and wife can each claim up to the applicable limit based on their own eligible investments and expenses — such as separate PPF accounts, individual insurance policies, or each paying tuition fees from their respective income. Joint investments may have different rules depending on how ownership and payment are structured — verify with the Income Tax Department for your specific situation.

Final Verdict

The 80C deduction list is a genuinely useful tax planning tool — but only when used after understanding what’s already in your bucket. For salaried employees on the old tax regime with real headroom remaining after EPF, home loan principal, and insurance premiums, PPF or ELSS can reduce taxable income meaningfully. At the 30% slab, every rupee of legitimate deduction counts. But the starting point is always the same: add up what you already have before buying anything new.

If your 80C bucket is already full, the most valuable thing this article can do for you is save you from a wasted investment. If the new tax regime gives you a better outcome without any deductions, the 80C list simply does not apply to your filing this year. Make the regime decision first. Then check headroom. Then invest with purpose.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.