If you recently retired and are planning to park a lump sum in a fixed deposit, the most common question is not about the interest rate — it is whether the bank will deduct TDS and how much tax you will actually pay on the interest earned.

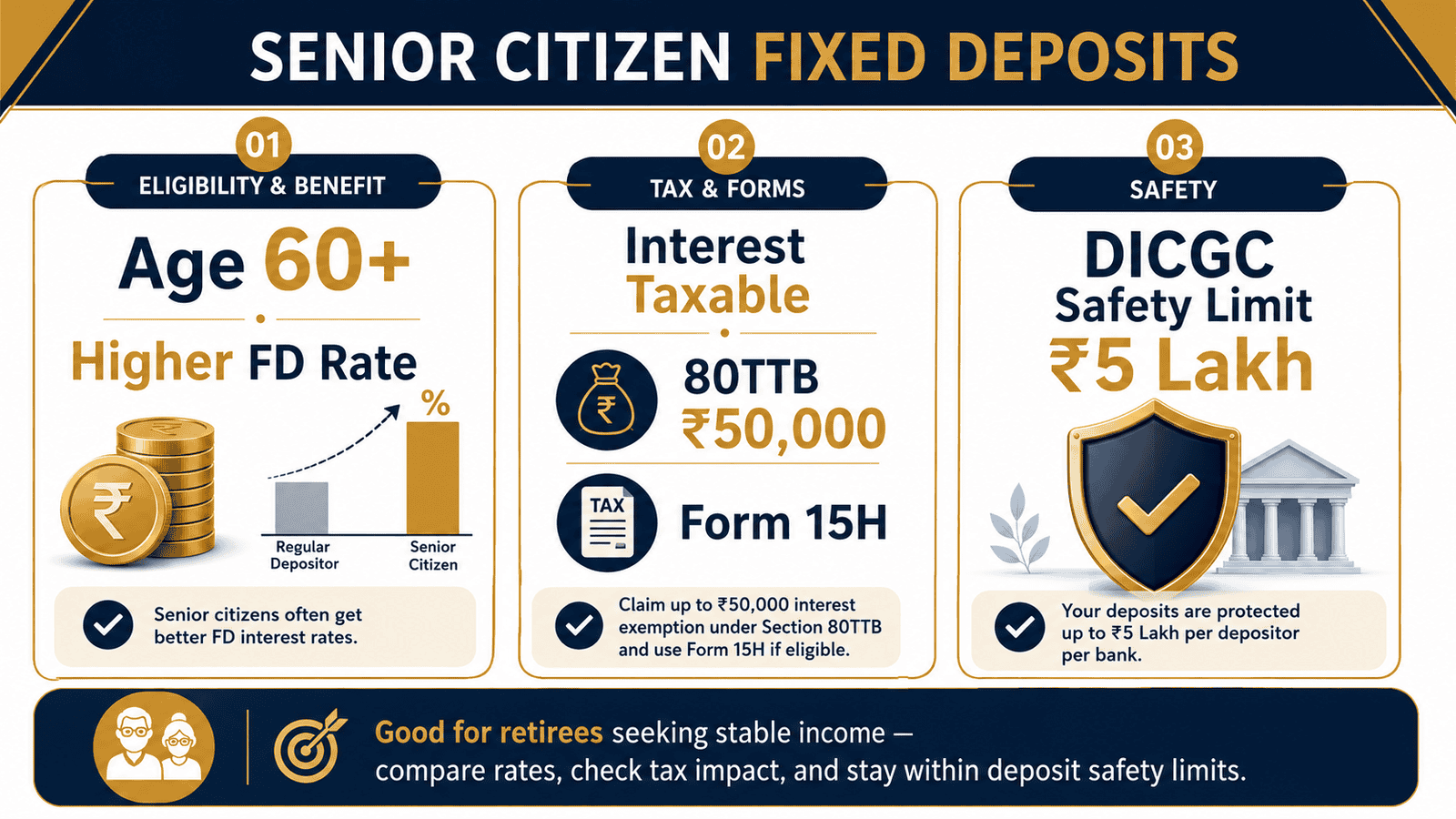

Senior citizen FDs are one of the most popular retirement income tools in India, and for good reason. Banks offer a slightly higher interest rate to depositors aged 60 and above, and the income is predictable. But the headline rate is only part of the story. Your actual return depends on your tax slab, whether you submit Form 15H, how much Section 80TTB reduces your taxable interest, and whether your deposit is protected if a bank runs into financial difficulty.

This article covers the full picture — interest benefit, TDS, Section 80TTB, Form 15H, DICGC safety, payout options, and when a senior citizen FD may not be enough on its own for retirement planning.

Quick Answer: Senior Citizen FD

Senior citizen FD is a fixed deposit offered to people aged 60 or above, usually with an extra interest rate benefit over regular FDs. The interest is taxable, but eligible senior citizens can claim up to ₹50,000 deduction under Section 80TTB and submit Form 15H if conditions are met.

Key Takeaways

- Senior citizen FDs typically pay 0.25% to 0.50% more per annum than regular FD rates at the same bank — on a ₹10 lakh deposit, that difference translates to approximately ₹2,500 to ₹5,000 extra interest per year depending on the bank and tenure.

- FD interest is fully taxable as income from other sources — it is added to your total annual income and taxed at your applicable slab rate, regardless of how the bank advertises the product.

- Banks deduct TDS on FD interest once it crosses ₹50,000 per bank per financial year for senior citizens — submitting Form 15H at the start of each April prevents TDS deduction if your estimated total income tax liability for the year is nil.

- Under Section 80TTB, eligible resident senior citizens can claim a deduction of up to ₹50,000 on interest from bank FDs, savings accounts, and post office deposits in a financial year — this reduces your taxable interest income but does not eliminate tax on interest above that limit.

- DICGC insures all deposits up to ₹5 lakh per depositor per bank — principal and interest combined — so amounts above this threshold at one bank are not covered by deposit insurance.

- Premature FD withdrawal before maturity typically reduces the applicable interest rate by 0.5% to 1% — keeping your emergency funds separate from your FD corpus prevents forced early closure at a penalty.

Key Facts at a Glance

| Parameter | Detail | Key Rule |

|---|---|---|

| Eligible Age | 60 years and above | Confirm with your bank at account opening; some banks extend additional benefit at 80+ |

| Extra Interest Rate Benefit | Typically 0.25%–0.50% over regular FD rate | Varies by bank, tenure, and deposit amount — verify on the bank’s official rate page |

| Tax Treatment | Taxable — income from other sources | Added to total income and taxed at applicable slab under the Income Tax Act |

| TDS Threshold (senior citizens) | ₹50,000 interest per bank per financial year | Submit Form 15H to prevent TDS if estimated total tax liability is nil |

| Section 80TTB Deduction | Up to ₹50,000 on interest income | Available to resident senior citizens under the old tax regime only |

| DICGC Deposit Insurance | ₹5 lakh per depositor per bank | Principal and interest combined; spread large corpus across banks to stay within limit |

| Payout Options | Cumulative or non-cumulative | Non-cumulative pays monthly or quarterly; cumulative returns full principal plus interest at maturity |

| Premature Withdrawal | Allowed with penalty | Typically 0.5%–1% interest rate reduction; confirm the penalty with your bank before opening |

How Senior Citizen FD Works in India

A senior citizen FD is a standard bank fixed deposit with one meaningful addition: depositors aged 60 and above receive a marginally higher interest rate than regular FD customers at the same institution. This extra rate — typically 0.25% to 0.50% per annum, varying by bank and tenure — recognises that retirees depend on interest income as a primary cash flow source.

If you are new to fixed deposits as a savings instrument, our guide on fixed deposit basics explains how FDs work before you compare rates.

Cumulative vs Non-Cumulative FD

The most important decision after choosing a bank and tenure is the payout structure.

A cumulative FD reinvests the interest quarterly — the amount compounds over the tenure and is paid entirely at maturity alongside the principal. This works well for retirees who do not need regular income and want the corpus to grow for a future goal. The maturity value is higher than a non-cumulative FD at the same rate, principal, and tenure.

A non-cumulative FD pays out interest at regular intervals — monthly, quarterly, half-yearly, or annually. For retirees who need predictable monthly income alongside their pension, this is usually the preferred option. The interest rate on a monthly-payout non-cumulative FD is slightly lower than the annual rate because the bank calculates an equivalent periodic rate. The difference is modest but worth comparing before you decide.

Tenure, Renewal, and Premature Withdrawal

Senior citizen FDs are offered in tenures ranging from 7 days to 10 years. Most banks offer their highest rates in the 1-year to 3-year range, though this shifts with each rate revision. Longer tenures do not always mean higher rates — check the rate card across tenures before committing.

At maturity, the FD is either auto-renewed at the prevailing rate on that date or the proceeds are credited to the linked savings account. The renewal rate is the bank’s current offer on that date — not the rate when you originally deposited. If rates have fallen since your initial deposit, auto-renewal locks you in at a lower rate without any deliberate action from you.

Premature withdrawal is permitted at most banks but comes with a penalty — typically a reduction of 0.5% to 1% on the applicable interest rate for the period held. If your FD rate was 7.5% and the penalty is 1%, you receive interest calculated at 6.5% for the time deposited. This is precisely why keeping emergency funds in a liquid savings account — separate from your FD corpus — is essential for retirees who may face unexpected expenses.

Nomination and Joint Holding

Every FD should have a clearly registered and updated nominee — the person the bank will pay the proceeds to if the primary depositor passes away. Without a valid nominee, the family faces a lengthy claims process involving notarised documents and legal heir certificates. This is avoidable.

Joint FDs are an equally useful structure. Adding a spouse as a second holder under “either or survivor” operation mode means either person can operate or close the deposit independently, without additional legal steps. The senior citizen rate applies based on the age of the primary account holder.

Why Post-Tax Return Matters More Than Headline Rate

Many retirees compare only the advertised FD rates across banks. But the figure that actually affects your finances is the post-tax return — what you keep after income tax on the interest earned.

FD interest is classified as income from other sources under the Income Tax Act. It is added to your total income — pension, rental income, any other source — and taxed at your applicable slab. A retiree in the 20% tax slab loses one-fifth of all FD interest to tax. Section 80TTB can reduce the taxable portion of interest, but it does not eliminate tax on interest above the deduction limit. According to the Income Tax Department (incometax.gov.in), this deduction is available to resident senior citizens and covers interest from banks, co-operative banks, and post office deposits.

The practical implication: always calculate and compare post-tax returns. A bank offering 7.5% to senior citizens is not automatically better than one offering 7.3% if the first bank has a weaker financial profile or different compounding frequency.

Real Example: Ramesh in Pune

Ramesh, 63, recently retired from a private-sector company in Pune. He receives a monthly pension of ₹55,000 and has a retirement corpus of ₹10 lakh that he wants to place in a senior citizen FD for steady monthly income.

He compares two scenarios at his bank (rates below are illustrative examples only — verify current rates at your specific bank before depositing):

- Regular FD rate: 7.00% per annum

- Senior citizen FD rate: 7.50% per annum

On ₹10 lakh placed in a non-cumulative monthly payout FD, the annual interest works out to approximately ₹75,000 at the senior citizen rate versus ₹70,000 at the regular rate — a difference of ₹5,000 per year from the same deposit in the same bank.

Ramesh’s total gross income for the year is ₹6,60,000 (pension) plus ₹75,000 (FD interest) = ₹7,35,000 before deductions. His annual FD interest crosses the ₹50,000 TDS threshold per bank, so his bank will deduct TDS unless he submits Form 15H before the start of the financial year.

Use our FD maturity calculator to estimate your exact annual interest and maturity amount before choosing between monthly payout and cumulative options.

How to Calculate Real Return After Tax

Annual FD Interest = Principal × Rate (%) ÷ 100

Using Ramesh’s illustrative figures (assumed rates — verify current bank rates and tax limits before depositing):

- Principal: ₹10,00,000

- Senior citizen FD rate: 7.5% p.a. (illustrative)

- Annual gross interest: ₹10,00,000 × 7.5% = ₹75,000

TDS impact: Since ₹75,000 exceeds the ₹50,000 TDS threshold for senior citizens, the bank deducts TDS at 10% (with PAN) = ₹7,500. Ramesh receives ₹67,500 as net interest after TDS. But TDS is only a prepayment of tax — his actual liability is calculated in his ITR based on total income and all applicable deductions.

Section 80TTB benefit (old regime): Ramesh can claim ₹50,000 deduction under Section 80TTB on his FD interest. His taxable FD interest reduces from ₹75,000 to ₹25,000. At the 20% slab, his actual tax on FD interest is ₹5,000 — compared to ₹15,000 without this deduction. His effective post-tax interest income is ₹70,000, equivalent to a 7.00% net return on ₹10 lakh.

| Tax Slab | Gross Annual Interest | Estimated Post-Tax Interest |

|---|---|---|

| 0% (income below exemption limit) | ₹75,000 | ₹75,000 — no tax; Form 15H applicable if tax liability is nil |

| 5% (with 80TTB, old regime) | ₹75,000 | ₹73,750 — tax of ₹1,250 on ₹25,000 after 80TTB deduction |

| 20% (with 80TTB, old regime) | ₹75,000 | ₹70,000 — tax of ₹5,000 on ₹25,000 after 80TTB deduction |

Tax slabs, deduction limits, and TDS thresholds can change with each Union Budget. Use our income tax calculator to estimate your actual tax liability based on total income and the current assessment year before making any deposit decision.

Comparison: Senior Citizen FD vs Other Options

Senior citizen FD is one product in a wider retirement income toolkit. The table below compares it with the most common alternatives — not to declare one best, but to help you see where each fits. For a detailed look at two common comparisons, see our guides on FD and RD comparison and the senior savings scheme.

| Option | How It Differs from Senior Citizen FD | Best Suited For |

|---|---|---|

| Regular FD | Same bank, same tenure — but typically 0.25%–0.50% lower rate; identical tax and TDS treatment | Depositors under age 60; same product without the senior rate advantage |

| Recurring Deposit (RD) | Monthly installment deposit instead of lump sum; interest rate slightly lower than FD; same TDS and taxability rules apply | Retirees who receive regular income and want to invest a fixed monthly amount rather than a lump sum |

| Senior Citizen Savings Scheme (SCSS) | Government-backed; quarterly interest payout only; ₹30 lakh maximum deposit; 5-year tenure with extension option; TDS applies above threshold; rate is reviewed quarterly — verify before investing | Retirees seeking government-backed security with a regulated quarterly income and a higher rate than savings accounts |

| Senior Citizen Savings Account | Fully liquid at all times; some banks offer a higher savings rate to senior citizens; no lock-in; lower interest than FD; TDS and 80TTB rules apply to interest earned | Emergency fund and short-term cash parking — not for large retirement corpus that needs to earn growth-level returns |

| Debt Mutual Fund (Conservative) | Market-linked returns with no guaranteed rate; no TDS on accrued interest; tax treatment depends on fund type, holding period, and applicable rules — seek qualified guidance before investing | Senior citizens in higher tax slabs exploring potentially tax-efficient alternatives — suitable only after independent financial advice |

How to Decide What’s Right for You

Before opening a senior citizen FD, work through these practical checkpoints:

You need monthly income to cover regular household expenses alongside your pension — THEN choose a non-cumulative FD with monthly or quarterly interest payout rather than a cumulative FD that locks the interest until maturity.

Your estimated total income for the year is below the applicable basic exemption limit and your estimated income tax liability is nil — THEN submit Form 15H to your bank at the start of each April to prevent TDS deduction on your FD interest throughout that financial year.

Your total FD deposits at one bank — across all accounts — exceed ₹5 lakh including accrued interest — THEN consider splitting the corpus across two or more banks to stay within the DICGC deposit insurance limit at each institution. Confirm current coverage at dicgc.org.in before acting.

You are likely to need funds within the next 12 months — for a medical expense, a family event, or an unexpected repair — THEN keep that amount in a liquid savings account or a short-tenure FD rather than a 3–5 year locked deposit. Our emergency fund amount guide helps you estimate the right reserve before you commit the rest to FDs.

Your nominee details are blank, outdated, or refer to someone who has passed away — THEN update them at the bank before opening any new FD or renewing an existing one. This single step prevents months of delays for your family.

Your total income falls in the 30% tax bracket and your FD interest income is substantial — a senior citizen FD will deliver a significantly lower post-tax return than the headline rate suggests. Comparing alternatives with a qualified financial adviser before committing the entire corpus to FDs is worth the time.

Common Mistakes to Avoid

Chasing the Highest Rate Without Checking Bank Safety

Some smaller banks and NBFCs advertise FD rates 1%–2% above large public-sector or private banks.

A higher rate from a lesser-known institution can reflect higher business risk. DICGC insurance covers only ₹5 lakh per depositor per bank — amounts above that limit in a single bank are not insured. If the institution faces financial trouble, recovery of the uninsured portion can take years.

Check the bank’s RBI-regulated status and credit rating before depositing retirement corpus into any institution offering unusually high rates.

Assuming Senior Citizen FD Interest Is Tax-Free

This is perhaps the single most common mistake among first-time retirees. FD interest is taxable income — there is no exemption solely because you are a senior citizen.

Section 80TTB reduces the taxable portion up to ₹50,000 per year, but interest above that limit is fully taxable at your slab rate. A retiree earning ₹1,50,000 in annual FD interest still pays tax on ₹1,00,000 after the deduction. At 20%, that is ₹20,000 in additional tax — a material amount for a retiree managing a fixed corpus.

Always calculate the post-tax return before comparing FD options across banks.

Confusing Form 15H With a Permanent Tax Exemption

Submitting Form 15H tells the bank not to deduct TDS at source. It does not make your FD interest tax-free.

If your total income for the year exceeds the taxable threshold after all deductions, you still owe income tax — and you must declare the full FD interest income in your ITR. Submitting Form 15H when you have a genuine tax liability is treated as a false declaration under the Income Tax Act and can attract penalties.

Submit Form 15H only if your estimated total income tax for the financial year is genuinely nil.

Locking the Entire Retirement Corpus in One Long-Tenure FD

Placing ₹20 lakh in a single 5-year FD at today’s rate means you cannot take advantage if rates rise significantly next year.

Premature closure to capture a better rate costs you a penalty of 0.5%–1%, reducing your effective return. An FD ladder — splitting the same corpus across 1-year, 2-year, and 3-year deposits — ensures one FD matures annually, giving you the option to reinvest at the prevailing rate without any penalty.

Create multiple FDs with staggered maturity dates rather than one large deposit.

Forgetting to Update Nominee Details

Nominee details are often left unchanged for years — sometimes referring to a person who is no longer alive.

Without a valid nominee, the family must submit notarised indemnity bonds, legal heir certificates, and succession documents to claim the FD proceeds after a depositor’s death. This process can take months and is entirely avoidable.

Verify and update nominee details every time you open a new FD or renew an existing one.

Missing the Maturity Date and Accepting Auto-Renewal

If you do not give explicit instructions before maturity, most banks auto-renew the FD at the prevailing senior citizen rate on that date — which may be noticeably lower than your original rate if the rate cycle has shifted.

Many retirees discover the lower renewal rate only after the next interest payout. Setting a calendar reminder one week before each FD maturity date gives you time to compare current rates and give deliberate instructions to the bank.

When This May Not Be the Right Choice

You are in the 30% tax slab. FD interest is taxed at your marginal rate. After accounting for Section 80TTB and tax, the effective post-tax return on a senior citizen FD at 7.5% for a 30% taxpayer is considerably lower than the headline number. Other regulated instruments may offer a better post-tax outcome — worth evaluating with a qualified adviser.

Inflation is eroding your real purchasing power. If the FD rate is 7% and inflation runs between 5%–7%, the real return — in terms of what your interest actually buys — is modest or close to flat. Long-tenure FDs lock you into a rate that may feel inadequate two or three years from now, particularly for medical and lifestyle expenses that tend to inflate faster.

You need frequent or unpredictable access to funds. An unexpected medical bill, home repair, or family emergency can force premature FD closure and trigger a penalty rate reduction. If your life stage requires high liquidity, keeping a larger share in savings accounts or short-tenure FDs is more practical than locking everything into multi-year deposits.

Your entire retirement corpus is in one product or one bank. Relying solely on FD interest for retirement income — with no SCSS allocation, liquid reserve, or other buffer — leaves you exposed to rate cycles. If rates fall at renewal, your monthly income drops immediately with no alternative source to cushion the impact.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Before opening or renewing a senior citizen FD, confirm the following from official sources — do not rely on rate aggregator websites or third-party summaries for regulatory figures:

- Income Tax Department — incometax.gov.in: Current Section 80TTB deduction limit, TDS threshold for senior citizens, Form 15H eligibility and submission process, income tax slabs and basic exemption limits, and ITR filing requirements for interest income.

- RBI — rbi.org.in: Regulations governing scheduled commercial banks, FD interest rate guidelines for banks, premature withdrawal provisions, and safe custody norms.

- DICGC — dicgc.org.in: Current deposit insurance coverage limit per depositor per bank, list of eligible insured institutions, and the claims process.

- Your bank’s official website: Current senior citizen FD rates by tenure, minimum deposit amount, auto-renewal policy, nomination and joint-holder procedures, and premature withdrawal penalty percentage.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Build an FD ladder instead of one large deposit. Divide your corpus — for example ₹3 lakh each in 1-year, 2-year, and 3-year tenures — so one FD matures each year. You can reinvest each maturity at whatever rate is prevailing, without locking the full corpus into a rate that may fall at renewal.

- Compare annualised post-tax returns, not just headline rates. A bank offering 7.8% where you are in the 20% slab after 80TTB may give you a lower post-tax income than a 7.5% FD at a safer institution. Calculate the net rupee amount before deciding — not the percentage alone.

- Submit Form 15H in the first week of April every year. Many senior citizens forget to submit it at the start of the financial year and then claim TDS refund in their ITR — a process that takes several months. Submitting Form 15H in April prevents the deduction from the first interest payout of the year.

- Keep emergency funds completely separate from your FD corpus. A minimum of 3–6 months of household expenses — plus a medical contingency buffer — should remain in a savings account at all times. This ensures you never need to break a long-tenure FD under pressure and incur a penalty rate reduction.

- Set a calendar reminder before each FD maturity date. Auto-renewal at a lower prevailing rate is one of the most avoidable losses for retirees. A reminder seven to ten days before maturity gives you time to review current rates, compare options, and give the bank explicit instructions before the automatic rollover happens.

- Confirm whether the senior citizen rate applies to renewals, not only fresh deposits. Some banks offer promotional rates on new deposits but auto-renew at their standard published senior citizen card rate. Ask the bank explicitly about the renewal rate policy before the maturity date — and get confirmation in writing or through your net banking record.

Frequently Asked Questions

Is senior citizen FD interest tax-free in India?

No. FD interest is taxable as income from other sources and added to your total annual income. Section 80TTB allows eligible resident senior citizens to deduct up to ₹50,000 of interest income in a financial year under the old tax regime — this reduces the taxable portion but does not eliminate tax on the full amount. Interest above the deduction limit is taxed at your applicable slab rate.

What age qualifies for senior citizen FD benefits?

Most scheduled commercial banks offer the senior citizen FD rate to depositors aged 60 years and above. Some institutions extend a further enhanced rate to very senior citizens aged 80 and above. The exact age threshold and additional benefit vary by bank — confirm at the time of account opening. Post offices do not currently offer a separate senior citizen rate on their time deposit product.

Can a senior citizen submit Form 15H to avoid TDS on FD interest?

Yes, provided your estimated total income tax for the financial year is nil. A senior citizen (aged 60 or above) can submit Form 15H to the bank requesting that TDS not be deducted. If you submit Form 15H when you actually have a tax liability, it constitutes a false declaration under the Income Tax Act and can attract penalties. Estimate your total income carefully — including pension, FD interest, rental income, and all other sources — before submitting.

Is FD interest deductible under Section 80TTB?

Yes. Section 80TTB allows resident senior citizens to deduct up to ₹50,000 from total interest income in a financial year. The deduction covers interest from bank savings accounts, fixed deposits, recurring deposits, and post office deposits. It is available only under the old tax regime — if you opt for the new tax regime, this deduction is not available. Verify the current limit and applicability at incometax.gov.in before filing your ITR.

Is senior citizen FD safer than mutual funds?

Bank FDs offer predictable, contracted returns that do not fluctuate with market movements. Mutual funds carry market risk — returns are not guaranteed and vary with the underlying assets. However, bank FDs are not unconditionally safe either — deposits above ₹5 lakh per depositor per bank are not covered by DICGC insurance. Diversifying across banks reduces concentration risk. Neither product is universally safer — suitability depends on your income need, risk tolerance, corpus size, and time horizon.

Should retirees choose monthly payout or cumulative FD?

It depends on your immediate cash flow need. If you need monthly income to supplement your pension and cover household expenses, a non-cumulative FD with monthly payout is the more practical structure. If your pension covers regular expenses and you do not need the FD interest immediately, a cumulative FD compounds the interest and delivers a higher maturity value. Compare the actual rupee monthly payout (not just the rate) between the two options before deciding.

What happens if I withdraw my FD before the maturity date?

Premature withdrawal is allowed at most banks but carries a penalty — typically a reduction of 0.5% to 1% on the interest rate applicable for the period you held the deposit. For example, if your FD rate was 7.5% and the premature penalty is 1%, interest is calculated at 6.5% for the actual holding period. Confirm the exact penalty percentage in your FD terms before opening — it varies across banks and sometimes across tenures within the same bank.

Can I open a joint FD and still get the senior citizen rate?

Yes, you can open a joint FD with a spouse or family member. The senior citizen rate applies when the primary account holder is aged 60 or above — the age of the second holder does not affect the rate eligibility. Most banks allow “either or survivor” operation mode, meaning either holder can independently operate, renew, or close the FD. Confirm the operation mode and joint-holder rules with the bank at the time of opening.

Does TDS get deducted on the full interest amount or only the portion above ₹50,000?

TDS is applied on the total interest amount from that bank once it crosses the ₹50,000 threshold in a financial year for senior citizens — not only on the excess. For example, if your total FD interest from one bank is ₹60,000, TDS at 10% (with PAN) is calculated on the full ₹60,000 = ₹6,000. You can claim credit for this TDS against your actual tax liability when filing your ITR. The 10% rate applies when PAN is submitted — it is 20% without PAN. Verify current TDS rates at incometax.gov.in.

Is 80TTB available under the new tax regime?

No. Section 80TTB deduction is available only under the old tax regime. If you opt for the new tax regime — which has lower slab rates but eliminates most deductions — you cannot claim 80TTB. This means your entire FD interest income is taxable at the new regime slab rates without the ₹50,000 reduction. Whether the old or new regime results in lower tax depends on your total income, other deductions, and applicable slab — calculate both before choosing for a financial year.

Final Verdict

Senior citizen FD remains one of the most practical tools for retirement income stability in India — predictable, bank-regulated, and backed by a modest extra rate over regular FDs. For retirees like Ramesh who need steady monthly cash flow without market exposure, a well-structured FD portfolio addresses the income certainty need effectively.

But the real value of a senior citizen FD depends on three things: your post-tax return after accounting for your slab and Section 80TTB, the financial strength of the bank you choose, and whether your liquidity is managed separately outside the FD corpus. Chase only the highest headline rate and you may end up with less post-tax income than a slightly lower rate at a larger, more stable institution.

Use senior citizen FD for what it does well — stable, predictable income — and pair it with a separate emergency reserve, updated nominee details, and an FD ladder so no single rate cycle disrupts your retirement cash flow. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.