Every year, millions of salaried employees in India pay health insurance premiums — for themselves, their spouses, their children, and their ageing parents — without fully using the tax deduction that Section 80D of the Income Tax Act was built for. Some miss it because they assume their employer’s group cover handles it. Others claim it in the wrong tax regime and wonder why the benefit doesn’t appear. And many are genuinely confused about whether a parent’s policy creates a separate deduction or eats into the same limit.

If you pay health insurance premiums out of your own pocket, understanding the 80D deduction correctly could mean a meaningfully lower tax bill — particularly when senior citizen parents are involved. This guide covers every rule that matters: who qualifies, which limits apply, what payment modes are accepted, how the parents’ bucket works, and exactly what to verify before you submit Form 16 declarations or file your ITR.

Quick Answer: What Is the 80D Deduction?

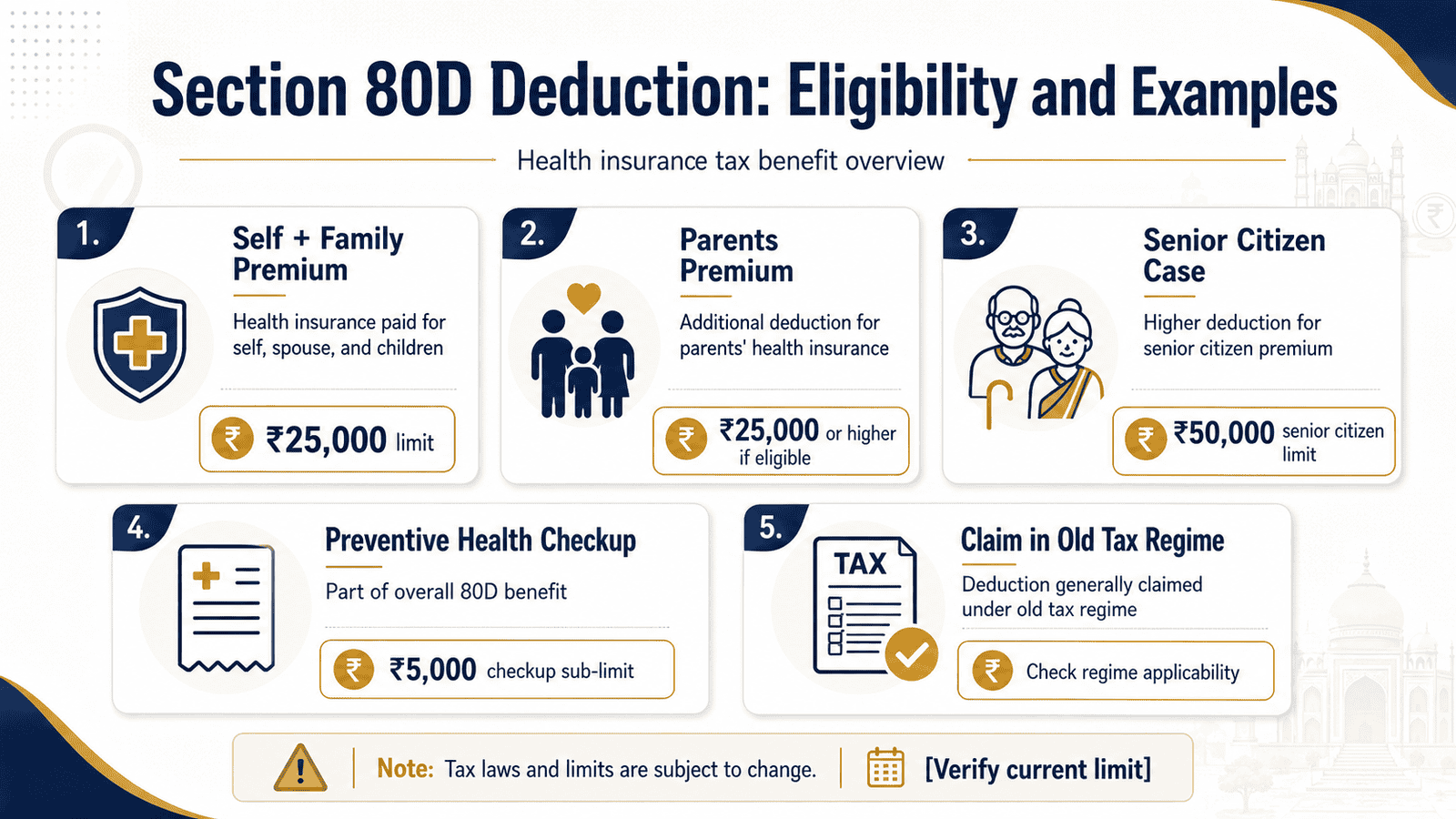

80D deduction lets taxpayers claim health insurance premiums for self, spouse, children and parents under the old tax regime. Common limits include ₹25,000 for self/family and ₹50,000 for senior citizen parents, including preventive checkups up to ₹5,000 within each limit. Parents’ premiums are treated as a completely separate deduction bucket — so your family cover and your parents’ cover each have their own ceiling. Always confirm current limits from the Income Tax Department before filing.

Key Takeaways

- Section 80D is available only under the old tax regime. If you have opted for the new tax regime, this deduction generally does not apply — check before declaring any amount.

- The self/family bucket covers premiums you pay for yourself, your spouse, and your dependent children — the common ceiling for this bucket is ₹25,000 per year.

- Parents get a completely separate deduction bucket: up to ₹25,000 if they are below 60 years, and up to ₹50,000 if they are senior citizens (60 years or above).

- If your parents are senior citizens and you pay their premium, your combined maximum 80D deduction can reach ₹75,000 — ₹25,000 for self/family and ₹50,000 for senior citizen parents.

- Preventive health checkup costs of up to ₹5,000 are included within the overall limit for each bucket — not an extra deduction on top of it.

- Only premiums you personally pay count. If your employer funds the group health insurance premium entirely, you generally cannot claim that amount under 80D.

- Cash payment is not permitted for insurance premium deductions under 80D — use UPI, NEFT, cheque, or a card. Cash is accepted only for preventive health checkup expenses.

Key Facts at a Glance

The table below covers the key parameters at a glance. For a complete picture of all deductions available when you choose the old tax regime, see the old regime deductions guide.

| Parameter | Rule / Limit |

|---|---|

| Section under IT Act | Section 80D, Income Tax Act, 1961 |

| Who can claim | Individual taxpayer (resident or non-resident, salaried or self-employed) |

| Self/family bucket — who is covered | Policyholder, spouse, dependent children |

| Parents’ bucket — who is covered | Father and/or mother (financial dependency is not mandatory) |

| Self/family deduction limit | ₹25,000 per year |

| Parents’ limit (parents below 60 years) | ₹25,000 per year |

| Parents’ limit (senior citizen parent, 60+ years) | ₹50,000 per year |

| Preventive health checkup sub-limit | Up to ₹5,000 within the overall limit (applies per bucket) |

| Maximum combined deduction | ₹75,000 (non-senior self + senior citizen parents); ₹1,00,000 (both self and parents are senior citizens) |

| Tax regime | Old tax regime only |

| Premium payment mode | Non-cash required (UPI, NEFT, IMPS, cheque, card); cash permitted only for preventive checkup |

What Is the 80D Deduction and How Does It Work?

Section 80D of the Income Tax Act allows you to reduce your taxable income by the amount you spend on qualifying health insurance premiums and preventive health checkup expenses. It is a deduction from taxable income — not a refund of your premium. If you claim ₹25,000 under 80D, your taxable income drops by ₹25,000. At a 20% slab rate, that translates to ₹5,000 in actual tax saved. At 30%, the same deduction saves ₹7,500. You are not receiving money back — you are paying tax on a smaller income figure.

This distinction matters. The primary reason to buy health insurance should always be financial protection against medical emergencies. The tax deduction is a secondary benefit — a useful one, but never the foundation of the decision. Before you evaluate premium amounts through a tax lens, make sure you understand health cover and what your policy actually pays for when you need it most.

The Two Separate Deduction Buckets

The most important structural feature of Section 80D is that it operates in two completely separate limits. Your own family’s premiums and your parents’ premiums do not compete for the same ceiling — they each have their own cap.

- Bucket 1 — Self/Family: Premiums you pay for yourself, your spouse, and your dependent children. The common limit is ₹25,000 per year.

- Bucket 2 — Parents: Premiums you pay for your father and/or mother. This bucket has its own separate limit — ₹25,000 if your parents are below 60 years, and ₹50,000 if either parent is a senior citizen (60 years or above).

If you are paying for both, both limits apply simultaneously. That is why families with senior citizen parents can reach combined 80D deductions of ₹75,000 or more in a single financial year.

Does Your Parents’ Age Make a Difference?

Yes — significantly. If either of your parents is 60 years of age or above, they qualify as a senior citizen under the Income Tax Act. The parents’ deduction limit increases to ₹50,000 once that threshold is crossed. You do not need both parents to be senior citizens — even one parent aged 60 or above brings the higher limit into play for the parents’ bucket.

Importantly, your parents do not need to be financially dependent on you. The only requirement is that you are the one actually paying the premium.

Why Employer Group Health Insurance Usually Does Not Help Here

If your employer pays the entire group health insurance premium on your behalf, you cannot claim that amount as a personal 80D deduction. The premium was not paid by you — it is an employer benefit, and it is accounted for differently in payroll and tax terms.

However, some employers offer voluntary top-up or enhancement policies where you pay an additional premium yourself. That self-paid portion may be eligible. Always check your salary slip or HR portal to confirm exactly who is funding which portion of the premium before declaring anything in your ITR.

What Counts as a Preventive Health Checkup?

Section 80D includes a sub-limit for preventive health checkup expenses — annual health screenings, blood work, diagnostic panels, and similar tests. The eligible amount is up to ₹5,000 within each bucket, not over and above the overall limit. In practice: if your self/family bucket is ₹25,000 and you have paid ₹22,000 in premiums, only ₹3,000 more of checkup expenses is eligible within that bucket. Preventive health checkup is the only item under 80D for which cash payment is permitted — all insurance premiums must be paid through non-cash modes.

The Old Tax Regime Dependency — The Rule That Catches Most People Off Guard

Section 80D is a Chapter VI-A deduction. Under the new tax regime (Section 115BAC), most Chapter VI-A deductions — including 80D — are generally not available. If you have opted for the new tax regime, the health insurance premiums you pay do not reduce your taxable income through Section 80D.

Many salaried employees assume all deductions apply automatically. They do not. Before you rely on 80D to shape your tax planning, confirm that the old tax regime actually results in a lower tax bill for your specific income and deduction profile. Use the compare tax regimes guide to evaluate your position before committing.

Real Example: Ananya’s Family and Parent Insurance Claims

Ananya, 34, is a product manager in Bengaluru earning ₹18 lakh per year. She has a family floater policy covering herself, her husband Karthik, and their 5-year-old daughter — the annual premium is ₹21,000, paid by UPI every April. Her family also does a preventive health checkup in November at a diagnostic centre: total cost ₹4,000 paid through a debit card.

Ananya’s parents — her father is 65 and her mother is 63, both retired in Mysuru — have separate individual health policies. The combined annual premium for both is ₹46,000, which Ananya pays by NEFT each year.

How her 80D deduction adds up:

- Self/family bucket: ₹21,000 (premium) + ₹4,000 (preventive checkup) = ₹25,000 — exactly at the limit

- Parents’ bucket: ₹46,000 (both senior citizens) — under the ₹50,000 cap, so full amount is eligible

- Total 80D deduction: ₹71,000

If Ananya files under the old tax regime at the 20% slab, this ₹71,000 deduction saves her approximately ₹14,200 in income tax. Without the parents’ bucket, she would save only ₹5,000 — the parents’ separate limit is what makes the real difference.

How to Calculate Your 80D Deduction

Working out your eligible 80D deduction follows five steps.

80D Deduction = [Lower of: Self/Family Premium + Preventive Checkup, or Self/Family Limit] + [Lower of: Parents’ Premium + Preventive Checkup, or Parents’ Limit]

Step 1: Identify who each policy covers — self/family or parents. One policy cannot be split across both buckets.

Step 2: Separate your total premiums paid into the two buckets.

Step 3: Apply the applicable limit to each bucket. Self/family: ₹25,000. Parents below 60: ₹25,000. Senior citizen parents (60+): ₹50,000.

Step 4: Add both buckets to get your total eligible 80D deduction.

Step 5: Multiply by your income tax slab rate to estimate tax saved — but run a full regime comparison before you finalise anything. The use income calculator on Ridhi lets you compare both regimes with your actual deduction figures.

| Scenario | Premium Paid | Eligible 80D Deduction |

|---|---|---|

| Self/family only, non-senior | ₹21,000 premium + ₹4,000 checkup | ₹25,000 (at cap) |

| Self/family + parents below 60 | ₹21,000 + ₹23,000 parents | ₹44,000 |

| Self/family + senior citizen parents (Ananya) | ₹25,000 + ₹46,000 parents | ₹71,000 |

| Maximum possible (non-senior self + senior parents) | ₹25,000+ self/family + ₹50,000+ parents | ₹75,000 (both buckets at cap) |

Comparison: Section 80D vs Section 80C

Health insurance deductions and investment-linked deductions are frequently confused. They operate completely independently — and both can be claimed together under the old tax regime, meaning they do not compete for the same limit. For a full list of what counts under 80C, see the compare with 80C guide.

| Parameter | Section 80D | Section 80C |

|---|---|---|

| What you claim | Health insurance premiums, preventive checkup | EPF, PPF, ELSS, LIC premium, home loan principal, others |

| Deduction limit | ₹25,000 to ₹1,00,000 (depends on family profile) | ₹1,50,000 per year |

| Extra parents’ deduction bucket | Yes — separate limit | No |

| Can both be claimed together | Yes | Yes |

| Cash payment for premium | Not allowed | Varies by instrument |

| Tax regime | Old tax regime only | Old tax regime only |

| Type of benefit | Healthcare expense deduction | Savings and investment incentive |

How to Decide What’s Right for You

You are on the old tax regime and pay health insurance premiums personally — declare the exact premium amount under Section 80D in your ITR or employer tax declaration. Do not miss this; it costs you nothing extra to claim it.

Your parents are 60 years or above and you pay their health insurance — claim the parents’ bucket separately. The additional ₹25,000 to ₹50,000 in deduction can reduce your tax bill by ₹5,000 to ₹15,000 depending on your slab rate.

Your employer pays the full group health insurance premium and you pay nothing directly — you cannot claim 80D for that policy. Check whether you pay a voluntary top-up or have bought a separate personal policy outside your employer’s cover.

Your parents are senior citizens and have no health insurance yet — evaluate your regime first. If the old tax regime suits your overall income and deduction profile, buying a parent policy before March 31 of the relevant financial year can unlock up to ₹50,000 additional deduction for that year.

You are deciding between an individual plan and a family floater for covering your parents — read the family floater choice guide before buying. The policy structure also affects your documentation when claiming the deduction.

Your total deductions under the old regime — including 80D, 80C, HRA, and others — do not result in a meaningfully lower tax than the new regime’s lower slab rates — stay on the new regime. Do not buy additional insurance just to chase a deduction that does not improve your net outcome.

Your only reason for buying health insurance is to claim the 80D tax deduction — reconsider the decision. A policy bought purely for tax benefit, with a low sum insured or many exclusions, is unlikely to protect your family financially when a real hospitalisation occurs. Insurance is protection first, tax saving second.

Common Mistakes to Avoid

Claiming 80D While on the New Tax Regime

Many salaried employees declare 80D to their employer or enter it in their ITR without realising they have opted for the new tax regime — where this deduction is generally not available. The employer payroll system may accept the input without flagging the conflict.

Always confirm your regime choice before submitting any deduction declaration to HR or filing your ITR.

Claiming the Employer-Paid Group Premium as Personal 80D

If your employer funds the group health insurance premium fully, that amount is not eligible for your personal 80D deduction. It was not your expenditure. Employees who declare an employer-paid premium as self-paid are filing an incorrect claim that can attract scrutiny during ITR processing.

Check your pay slip to confirm who actually pays the premium before declaring anything.

Paying the Insurance Premium in Cash

Health insurance premium paid in cash is entirely ineligible for Section 80D deduction — this is a statutory rule, not a grey area. If you pay ₹21,000 in cash to your agent or insurer, that full amount becomes ineligible, even if the policy is legitimate and active.

Always pay by UPI, NEFT, IMPS, cheque, or a debit or credit card. Save the payment screenshot or transaction reference as proof.

Treating the Preventive Checkup as a Bonus Deduction

The ₹5,000 preventive health checkup sub-limit sits within the overall bucket limit, not over and above it. If your self/family bucket limit is ₹25,000 and you have already paid ₹24,000 in premiums, only ₹1,000 more of checkup expenses is eligible — not a fresh ₹5,000.

Plan your premium and checkup spending together within each bucket, not separately.

Forgetting Parent-Policy Documentation

The parents’ bucket is a completely separate claim line — and it requires separate documentation. You need the policy schedule, premium receipt, and bank payment proof for each parent’s policy. Losing any of these before filing means losing the deduction for that bucket.

Maintain a dedicated digital folder with all health insurance documents, organised by financial year.

Claiming a Premium That Exceeds the Cap Without Adjusting

If you pay ₹60,000 as your senior citizen parents’ health insurance premium, only ₹50,000 is eligible under the parents’ bucket. The excess ₹10,000 cannot be carried forward, claimed in a different section, or used elsewhere — it simply falls away.

Before filing, check the applicable limit for each bucket and enter the lesser of the premium paid or the cap, not the full premium amount automatically.

Claiming for In-Laws, Siblings, or Other Relatives

Section 80D covers only your own father and mother in the parents’ bucket. In-laws, siblings, grandparents, aunts, and uncles do not qualify for either bucket. Claiming a sibling’s premium as part of your 80D deduction is an incorrect return that can be flagged during ITR processing.

When This May Not Be the Right Choice

The 80D deduction is genuinely useful — but it should not be the engine behind financial decisions it was not designed to drive.

- If you are on the new tax regime, 80D generally does not apply. Switching to the old regime purely to claim this deduction must be justified by your entire deduction profile — 80D alone is unlikely to make the old regime better if your other deductions are limited.

- If you are buying a health policy with a low sum insured — say, ₹2 lakh — simply to stay within a “comfortable premium” for the deduction, you are almost certainly underinsured. A single hospitalisation in a Tier 1 city can easily cost ₹5 lakh to ₹10 lakh. The tax saving does not compensate for that gap.

- If you are buying a parents’ policy with long waiting periods for pre-existing conditions or significant exclusions, the deduction benefit may not offset the inadequacy of the coverage in a real medical event.

- If your premium outgo is already stretching your monthly budget — prioritise adequate cover at a sum insured that makes sense for your family’s health risk. Then claim whatever deduction is available, rather than buying cover optimised for the deduction ceiling.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Section 80D is defined under the Income Tax Act, 1961, and is updated through Finance Bills with each Union Budget. Deduction limits, eligible persons, payment mode conditions, and regime applicability are all set by the Act. Insurance-related terms — policy exclusions, waiting periods, and claim conditions — are regulated separately by IRDAI.

- Income Tax Department — incometax.gov.in (for Section 80D rules, ITR filing guidance, and regime applicability)

- IRDAI — irdai.gov.in (for health insurance regulations and policyholder guidelines)

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Declare your health insurance premium to your employer early in the financial year — October or November is the right window. This way the deduction is factored into your monthly TDS calculations throughout the year, rather than being a lump-sum adjustment in February or March.

- Keep a single digital folder — labelled by financial year — with the policy schedule, premium payment receipt, and bank transaction screenshot for every policy you intend to claim. Retrieving these during ITR filing season takes minutes when they are organised.

- The date that counts for 80D is the date of actual premium payment, not the policy start date or renewal date. If your policy renews on April 15 and you pay on April 15, it counts for the new financial year — not the previous one. Do not assume last year’s March payment applies to this year’s ITR.

- Never pay a health insurance premium in cash — even a partial amount. If any portion of the premium for a policy is paid in cash, the eligibility of the entire premium for that policy under 80D can be questioned. Use digital payment modes exclusively.

- If your parents are approaching 60, plan ahead. A parent who turns 60 during a financial year may qualify for the higher senior citizen limit for that year — verify the exact rule applicable for the assessment year you are filing.

- Run the full old regime versus new regime comparison every year before filing — your income, deductions, and the tax rules all shift annually. What was optimal last year may not be optimal this year. Do not carry forward last year’s regime choice without recalculating.

Frequently Asked Questions

Can I claim the 80D deduction under the new tax regime?

Generally, no. Under the new tax regime (Section 115BAC), most Chapter VI-A deductions — including Section 80D — are not available. If you have opted for the new tax regime, health insurance premiums you pay do not reduce your taxable income through 80D. Verify the current rules and any Budget amendments at incometax.gov.in before filing your ITR.

Can I claim 80D for my parents’ health insurance?

Yes. Premiums you pay for your parents’ health insurance fall under a separate deduction bucket under Section 80D. This is entirely in addition to the self/family bucket — both limits apply independently. Your parents do not need to be financially dependent on you for you to be eligible. You simply need to be the person paying the premium.

Is the 80D limit higher for senior citizen parents?

Yes. If either of your parents is 60 years or above, the parents’ bucket limit increases to ₹50,000. If both parents are below 60, the parents’ bucket limit is ₹25,000. You do not need both parents to be senior citizens — one parent crossing the 60-year threshold is enough to trigger the higher limit for the entire parents’ bucket. Verify the applicable age threshold for your assessment year before filing.

Is preventive health checkup included in the 80D deduction?

Yes — but it is a sub-limit within the overall bucket ceiling, not an additional separate deduction. You can claim up to ₹5,000 for preventive health checkup expenses within each bucket (self/family or parents). If your bucket limit is ₹25,000 and you have used ₹23,000 on premiums, only ₹2,000 more of checkup expenses is eligible — not a fresh ₹5,000. Cash payment is permitted for preventive health checkup expenses, unlike insurance premiums.

Can I claim 80D for my employer’s group health insurance premium?

Not if your employer pays the premium entirely on your behalf. If the premium is funded by your employer as part of your CTC or employee benefits package, it is not your personal expenditure and is not eligible for Section 80D. If you voluntarily pay an additional top-up premium yourself — separate from the employer-funded policy — that self-paid amount may be eligible. Confirm with your HR or payroll team exactly who funds which portion.

Is cash payment allowed for 80D claims?

Cash payment is not allowed for health insurance premiums under Section 80D. All insurance premium payments must be made through non-cash modes — UPI, NEFT, IMPS, cheque, or a debit or credit card. The only exception is preventive health checkup expenses, for which cash payment is permitted. Always retain payment proof in a non-cash mode before declaring a premium under 80D.

What is the maximum 80D deduction I can claim in a single financial year?

If you are a non-senior citizen and your parents are senior citizens (60+), the maximum combined 80D deduction is ₹75,000 — ₹25,000 for self/family and ₹50,000 for senior citizen parents. If you are also a senior citizen (60+), your self/family limit may also be higher, potentially allowing a combined maximum of ₹1,00,000. Verify the current limits that apply to your specific assessment year before filing.

Can I claim 80D for in-laws or siblings?

No. Section 80D covers only your own father and mother in the parents’ bucket. Your spouse’s parents (in-laws), your siblings, and other relatives do not qualify for either the self/family bucket or the parents’ bucket. If you pay premiums for a sibling’s health policy, that amount is not eligible under Section 80D.

How do I actually claim 80D when filing my ITR?

In your ITR, navigate to the Chapter VI-A deductions section and enter the relevant amounts under Section 80D. You will typically need to specify the premium paid for self/family, the premium paid for parents, and whether your parents are senior citizens. No document is submitted with the ITR itself — but keep all policy schedules, premium receipts, and payment proofs readily accessible in case of any scrutiny or notice from the Income Tax Department.

What happens if I pay a higher premium than the 80D cap allows?

You can only claim up to the applicable cap — not the full premium paid. If you pay ₹60,000 for senior citizen parents’ policies and the cap is ₹50,000, only ₹50,000 is eligible. The excess ₹10,000 cannot be carried forward to the next financial year, claimed under a different section, or used in any other way under Section 80D. It simply does not qualify for deduction.

Final Verdict

The 80D deduction is one of the most practical tax benefits available to Indian salaried families — because it rewards something you should be doing anyway: maintaining adequate health insurance. If you are on the old tax regime and pay premiums personally for yourself, your family, and your senior citizen parents, the combined deduction can reach ₹75,000 or more, translating to meaningful tax savings at the 20% or 30% slab rate.

But the deduction should follow the insurance decision — not drive it. Buy the cover that genuinely protects your family, in the tax regime that actually suits your income profile. Do not underinsure, and do not chase 80D in a regime where it does not apply. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.