If you have just received a ₹25 LPA offer letter — or are trying to make sense of your Form 16 estimate — the first thing you want to know is how much tax you will actually pay. Tax on 25 LPA salary is not a fixed number. It depends on whether ₹25 lakh is your CTC or gross salary, which tax regime you choose, and what deductions you can claim.

This article walks through the full calculation under both the new regime and old regime, using a realistic ₹25 lakh example. You will see the exact slab math, a comparison of both regimes, an estimated monthly TDS figure, and a clear explanation of why ₹25 LPA CTC is not always ₹25 lakh taxable salary. Note that tax rules apply to the relevant assessment year — always verify current rates before filing.

Quick Answer: Tax on 25 LPA Salary

Tax on 25 LPA salary depends on whether ₹25 lakh is gross salary or CTC. Under a simple FY 2025-26 new-regime example with ₹75,000 standard deduction, tax may be around ₹3.20 lakh including 4% cess, before considering employer-specific salary components.

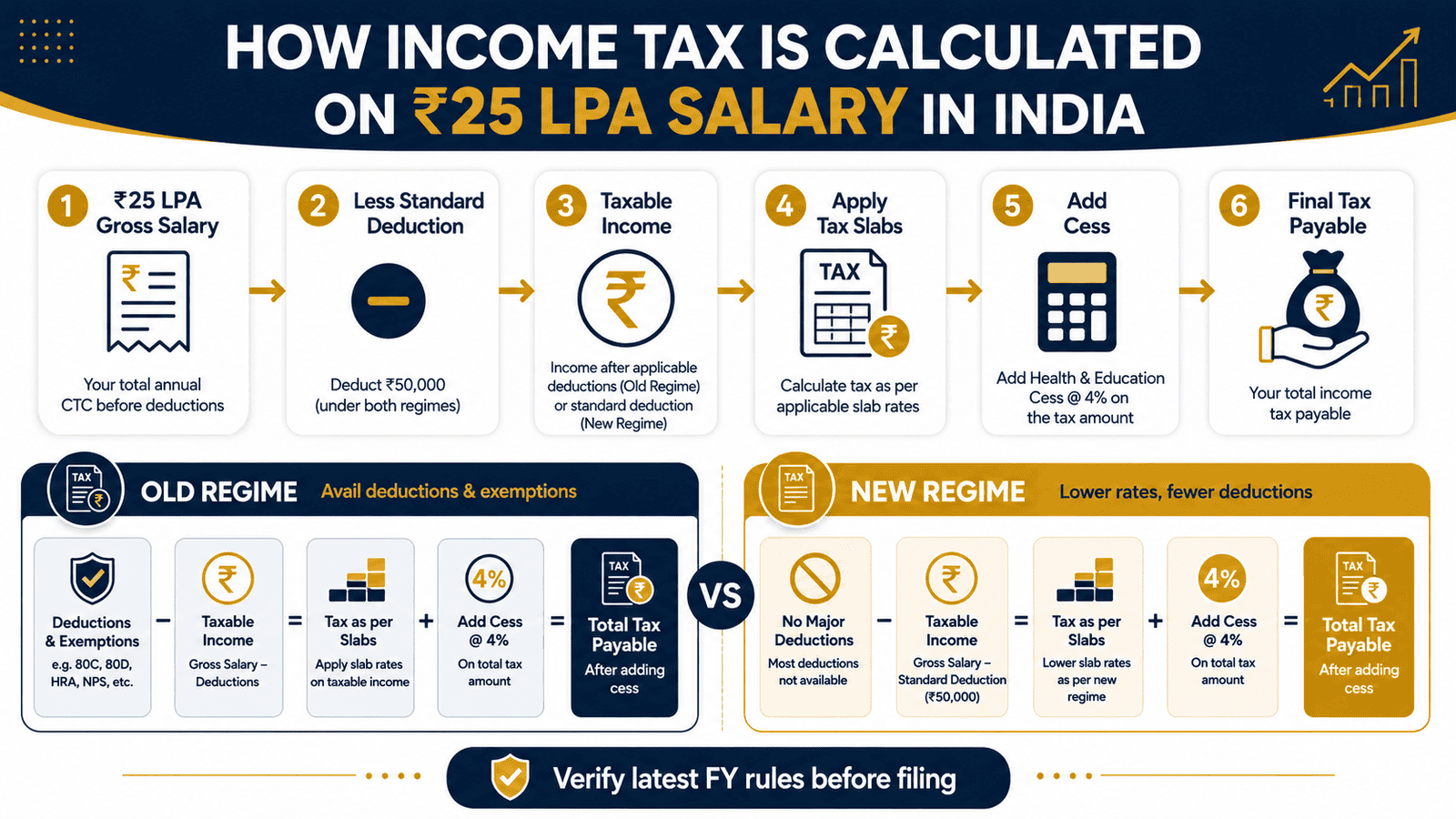

How to Calculate Tax on ₹25 LPA Salary

Income Tax Payable = Tax on Taxable Income (at Progressive Slab Rates) + 4% Health and Education Cess

New Regime Example — FY 2025-26

Gross salary: ₹25,00,000. Standard deduction: ₹75,000. Taxable income: ₹24,25,000. Section 87A rebate does not apply — taxable income is well above the rebate threshold. No surcharge applies below ₹50 lakh taxable income.

| Income Slab | Rate | Tax Amount |

|---|---|---|

| ₹0 to ₹4,00,000 | Nil | ₹0 |

| ₹4,00,001 to ₹8,00,000 | 5% | ₹20,000 |

| ₹8,00,001 to ₹12,00,000 | 10% | ₹40,000 |

| ₹12,00,001 to ₹16,00,000 | 15% | ₹60,000 |

| ₹16,00,001 to ₹20,00,000 | 20% | ₹80,000 |

| ₹20,00,001 to ₹24,00,000 | 25% | ₹1,00,000 |

| ₹24,00,001 to ₹24,25,000 | 30% | ₹7,500 |

| Tax before cess | ₹3,07,500 | |

| Add: 4% Health and Education Cess | ₹12,300 | |

| Total tax payable (new regime) | ₹3,19,800 |

Estimated monthly TDS: ₹3,19,800 ÷ 12 = approximately ₹26,650 per month.

Old Regime Example — Standard Deduction Only

Gross salary: ₹25,00,000. Standard deduction: ₹50,000. Taxable income: ₹24,50,000. Old regime slabs for individual taxpayers below 60 years: Nil up to ₹2,50,000; 5% from ₹2,50,001 to ₹5,00,000; 20% from ₹5,00,001 to ₹10,00,000; 30% above ₹10,00,000.

| Income Slab | Rate | Tax Amount |

|---|---|---|

| ₹0 to ₹2,50,000 | Nil | ₹0 |

| ₹2,50,001 to ₹5,00,000 | 5% | ₹12,500 |

| ₹5,00,001 to ₹10,00,000 | 20% | ₹1,00,000 |

| ₹10,00,001 to ₹24,50,000 | 30% | ₹4,35,000 |

| Tax before cess | ₹5,47,500 | |

| Add: 4% Health and Education Cess | ₹21,900 | |

| Total tax payable (old regime, no deductions) | ₹5,69,400 |

Estimated monthly TDS (old regime, no deductions): approximately ₹47,450 per month.

Three-Scenario Comparison

| Scenario | Taxable Income | Tax Including Cess |

|---|---|---|

| New regime — ₹75,000 standard deduction only | ₹24,25,000 | ₹3,19,800 |

| Old regime — ₹50,000 standard deduction only | ₹24,50,000 | ₹5,69,400 |

| Old regime — with ₹2,25,000 extra deductions (80C + NPS + 80D) | ₹22,25,000 | ₹4,99,200 |

Use our income tax calculator to enter your actual salary breakup and deductions for a personalised estimate under both regimes.

Key Takeaways

- A ₹25 LPA CTC is not the same as ₹25 lakh taxable salary — employer PF, gratuity, and insurance reduce your taxable base, sometimes by ₹2–4 lakh.

- Under the FY 2025-26 new regime with ₹75,000 standard deduction, estimated total tax on ₹25 lakh gross salary is approximately ₹3,19,800, including 4% cess.

- Under the old regime with no extra deductions, the same salary attracts approximately ₹5,69,400 in tax — old regime only helps when eligible deductions are large enough to close that ₹2.5 lakh gap.

- At ₹25 LPA, you typically need total deductions of around ₹8 lakh or more for the old regime to match the new regime — that requires maxing out 80C, NPS, 80D, HRA, and home loan interest simultaneously.

- Section 87A rebate does not apply at ₹25 LPA — it is available only when taxable income falls below the applicable rebate threshold under the new regime.

- Monthly TDS is an employer estimate, not final tax — the actual liability is settled when you file your ITR and include all income sources.

- Surcharge does not apply at ₹25 lakh — it is triggered only above ₹50 lakh taxable income.

Key Facts at a Glance

| Parameter | New Tax Regime | Old Tax Regime |

|---|---|---|

| Gross Salary (assumed) | ₹25,00,000 | ₹25,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| Taxable Income (no extra deductions) | ₹24,25,000 | ₹24,50,000 |

| Tax Before Cess | ₹3,07,500 | ₹5,47,500 |

| Health and Education Cess (4%) | ₹12,300 | ₹21,900 |

| Total Tax Payable | ₹3,19,800 | ₹5,69,400 |

| Monthly TDS Estimate | ~₹26,650 | ~₹47,450 |

| Section 87A Rebate | Not applicable | Not applicable |

| Surcharge | Not applicable | Not applicable |

| Assessment Year | AY 2026-27 | AY 2026-27 |

How Income Tax on 25 LPA Salary Is Calculated

Before any tax figure makes sense, you need to understand what number is actually being taxed — and for most employees with a ₹25 LPA package, that number is lower than the headline CTC.

CTC Is Not Your Taxable Salary

CTC stands for cost to company — the total amount your employer spends on you. It includes your gross salary plus employer-side costs that never reach your bank account: employer PF contribution (typically 12% of basic salary), gratuity provision, group health insurance, and sometimes car lease or meal voucher costs. A ₹25 LPA CTC may correspond to a gross salary anywhere between ₹21 lakh and ₹23 lakh, depending on the employer’s structure.

Taxable salary is calculated from gross salary, not CTC. After deducting the standard deduction, any HRA exemption, and other eligible components under the applicable regime, your taxable salary may be meaningfully lower than the number on your offer letter. For a clear explanation of how gross salary is reduced before tax is applied: standard deduction explained.

Progressive Slabs Mean Your Effective Rate Is Not 30%

A common misreading is that falling in the 30% slab means all income is taxed at 30%. That is not how Indian income tax works. Only the income within each slab band is taxed at that band’s rate. At ₹24,25,000 taxable income under the new regime, only ₹25,000 (the amount above ₹24 lakh) is taxed at 30%. The rest is taxed progressively through lower bands.

The result: your effective tax rate on ₹25 lakh gross salary under the new regime is approximately 12.8% — not 30%. This distinction matters when you are comparing offers, negotiating salary, or planning monthly expenses. For a deeper look at how gross salary, CTC, and taxable income differ: taxable salary calculation.

Health and Education Cess Is Mandatory

After computing the slab-based tax, 4% Health and Education Cess is added on the total tax amount. This applies under both regimes and to every taxpayer. At ₹25 LPA new regime, cess adds ₹12,300 — taking total tax from ₹3,07,500 to ₹3,19,800. There is no way to avoid cess; it is not a deductible expense.

Why Your Employer’s Monthly TDS May Differ

TDS is an employer estimate. Your employer divides the projected annual tax by 12 to deduct a roughly equal amount each month. This estimate is based on the regime you declared, the deductions you submitted, and the salary components visible to payroll. If your actual income — including interest, capital gains, freelance work, or rental income — differs from what your employer estimated, your final tax at ITR time will be different from TDS deducted.

According to Income Tax Department guidelines, employees are responsible for declaring all income in their ITR, regardless of what TDS was deducted by the employer. TDS is advance tax — not final tax.

Section 115BAC and the New Regime Default

The new tax regime under Section 115BAC is the default regime for FY 2025-26. If you do not actively declare old regime to your employer, TDS will be calculated under the new regime. You can switch regime at the time of filing your ITR, but switching mid-year creates TDS reconciliation complexity. Declare your regime early in the financial year.

Real Example: Rohan, Software Engineer, Bengaluru

Rohan, 31, works as a senior software engineer at a Bengaluru technology firm. His offer letter shows ₹25 LPA CTC. When HR shares the breakup, the structure looks like this:

- Basic salary: ₹10,00,000

- House Rent Allowance: ₹5,00,000

- Special allowance: ₹5,50,000

- Employer PF (12% of basic): ₹1,20,000

- Gratuity provision: ₹48,077

- Group insurance: ₹30,000

- Performance bonus (variable): ₹2,51,923

Rohan’s gross salary — the part reflected in his payslip — is approximately ₹20,50,000 to ₹22,50,000 per year depending on when his bonus is paid and whether the employer treats it as part of fixed pay. His ₹25 LPA CTC includes ₹1,98,077 in employer-side costs that are never credited to his account. After applying the ₹75,000 new-regime standard deduction, his taxable salary may be closer to ₹19.5–₹21.5 lakh — not ₹25 lakh.

Key insight: Rohan is not taxed on ₹25 lakh. His actual tax under the new regime is likely lower than the ₹3,19,800 in the worked example above, because his gross salary is below ₹25 lakh once employer PF and gratuity are separated. Always ask for your gross salary figure — not just CTC — before estimating tax.

Comparison: New Tax Regime vs Old Tax Regime for ₹25 LPA

| Parameter | New Tax Regime | Old Tax Regime |

|---|---|---|

| Standard Deduction | ₹75,000 | ₹50,000 |

| HRA Exemption | Not available | Available |

| Section 80C (up to ₹1.5 lakh) | Not available | Available |

| Section 80D Health Insurance | Not available | Up to ₹25,000–₹50,000 |

| Home Loan Interest — Section 24b | Not available | Up to ₹2,00,000 |

| NPS — Section 80CCD(1B) | Not available | Up to ₹50,000 |

| Documentation Required | Minimal | Extensive |

| Estimated Tax (no extra deductions) | ₹3,19,800 | ₹5,69,400 |

| Who Benefits Most | Low deduction profiles | High deduction + exemption profiles |

For a complete breakdown of which regime suits different salary and deduction profiles, read: old versus new regime.

How to Decide What’s Right for You

You have no HRA claim, no 80C investments beyond employer PF, no health insurance premium, and no home loan — the new regime will almost certainly produce lower tax at ₹25 LPA. No further analysis needed.

You pay rent in a metro city, have maxed out 80C at ₹1,50,000, pay NPS, and have a home loan — run both regimes through a tax calculator. The old regime gap narrows significantly and may cross over depending on your total claim.

Your ₹25 LPA figure is CTC and your actual gross salary is ₹21–₹23 lakh — your taxable income is lower than the examples in this article. Recalculate using your actual gross salary figure from your payslip, not your offer letter.

You received a mid-year bonus or salary hike — inform your employer’s payroll team to revise the projected TDS. If TDS is not adjusted, you may face a large payable tax amount when filing your ITR.

You have ESOP or RSU income, capital gains from stocks or mutual funds, or rental income in addition to salary — your total taxable income is higher than your salary alone and must be computed across all income heads in your ITR.

You do not have supporting documents for HRA, investment, or home loan claims ready before your employer’s declaration deadline — do not choose old regime without proofs in hand. Unverified deductions are reversed, and TDS is recovered in the remaining months of the year.

Common Mistakes to Avoid

Treating ₹25 LPA CTC as ₹25 Lakh Taxable Salary

CTC includes employer PF, gratuity, group insurance, and other costs that are never credited to your account.

If you calculate tax on ₹25 lakh but your gross salary is actually ₹22 lakh, you are planning on a false base. Equally, if you forget to include variable pay, you may underprovide for TDS and face a shortfall at ITR time.

Ask your HR or payroll team for three specific numbers: gross salary, taxable salary, and projected annual TDS. These are different from CTC.

Forgetting That Bonus Is Taxable in the Year It Is Paid

A performance bonus credited in March is taxable income for that financial year — not the next.

Employers typically spike TDS in the month the bonus is processed to recover any shortfall created by the additional income. A ₹2 lakh bonus in March in the 30% bracket can reduce your in-hand salary that month by ₹60,000–₹70,000 in additional TDS. This surprises many employees.

Before your bonus month, ask payroll what the TDS impact will be so you are prepared.

Choosing Old Regime Without Documentary Proof Ready

Declaring old regime to your employer and then failing to submit HRA receipts, 80C statements, or home loan certificates by the employer’s deadline — usually January or February — means deductions are reversed.

Payroll then recovers the shortfall TDS across the last two or three months of the financial year, significantly reducing in-hand salary. Keep all proofs ready before you make the declaration, not after.

Ignoring Other Income Sources When Estimating Tax

Interest from savings accounts and fixed deposits, capital gains from mutual funds or equity, and rental income are all taxable and must be declared in your ITR — even if your employer has already deducted TDS on salary.

Many employees with ₹1–2 lakh in FD interest assume the bank has handled it. The bank has deducted 10% TDS on interest — but your marginal rate may be 20% or 30%, and the balance must be paid when you file.

Confusing TDS Deducted With Final Tax Liability

TDS is an advance deduction — an employer estimate based on declared salary and deductions. Final tax is computed when you file your ITR. If your TDS exceeded your liability, you receive a refund. If your actual tax is higher due to undeclared income, a wrong regime choice, or missed deductions, you pay the difference.

For a clear explanation of how TDS on salary is calculated and what happens when it is under or over-deducted: salary TDS basics.

Not Switching Regime Before the Employer’s Annual Declaration Deadline

The financial year opens a window to declare your regime to your employer — typically April. Once TDS starts being deducted under one regime, mid-year switching creates reconciliation complexity for payroll.

You can always choose a different regime at the time of filing your ITR (subject to conditions for business income), but the TDS already deducted under the wrong regime may require a refund claim. Decide early and declare on time.

When This May Not Be the Right Choice

The calculations in this article assume a single employer, gross salary equal to ₹25 lakh, no mid-year job change, and no income outside salary. This framework may not apply accurately to you if:

- Your ₹25 LPA is CTC, not gross salary — your actual taxable base may be ₹2–4 lakh lower, changing both the tax amount and the regime comparison.

- You have ESOP vesting, RSU income, or capital gains in the same year — these attract special tax rates and materially change total tax liability.

- You changed employers during the year — each employer will have deducted TDS independently, and the combined income may push you into a higher effective slab.

- Your total taxable income approaches ₹50 lakh — surcharge applies above this threshold and increases the effective tax rate significantly.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Tax slabs, standard deduction limits, cess rates, surcharge thresholds, and rebate eligibility for FY 2025-26 (AY 2026-27) are governed by the Income Tax Act, 1961 as amended by Finance Act 2025. The official sources for current rules are:

- Income Tax Department — incometax.gov.in: Current slab rates, AY 2026-27 return filing, TDS credit verification in Form 26AS, and Form 16 reconciliation.

- PIB / Ministry of Finance — pib.gov.in: Budget 2025 press releases and official announcements on slab changes, rebate limits, and regime rules.

For the full FY 2025-26 new regime slab structure and eligibility conditions: current new slabs.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Ask your HR or payroll team for three specific numbers before the financial year begins: gross salary, projected taxable salary, and projected annual TDS. CTC alone is not enough to plan your tax accurately.

- Run both regimes through a tax calculator before submitting your declaration — especially if you pay rent, have 80C investments, or service a home loan. At ₹25 LPA, the difference between regimes can be ₹1.5–2.5 lakh depending on your deduction profile.

- If your bonus is paid in Q4, check with payroll what the TDS impact will be in that month. A ₹2 lakh bonus in the 30% slab may spike your monthly deduction by ₹60,000–₹70,000 in that pay cycle.

- If you are claiming HRA under the old regime, calculate your exemption precisely — it is the minimum of actual HRA received, 50% of basic (metro) or 40% of basic (non-metro), and actual rent paid minus 10% of basic salary. Many salaried employees claim less than they are legally entitled to.

- Reconcile your Form 26AS TDS credit statement on incometax.gov.in with your Form 16 before filing ITR. Mismatches between what your employer reported and what appears in 26AS can trigger notices from the department.

- If you switched jobs mid-year, provide your new employer a declaration of income and TDS from the previous employer so they can compute the balance TDS correctly for the rest of the year.

- Do not leave 80C investments to the last week of March. Under time pressure, fund selection suffers. Plan by December so your employer’s final TDS computation reflects the correct declarations.

Frequently Asked Questions

How much tax on ₹25 lakh salary under the new regime for FY 2025-26?

Under the new tax regime with ₹75,000 standard deduction, taxable income on ₹25 lakh gross salary is ₹24,25,000. Tax before cess is ₹3,07,500. After 4% Health and Education Cess, total tax payable is approximately ₹3,19,800 for AY 2026-27. Monthly TDS works out to roughly ₹26,650. Verify current slab rates at incometax.gov.in before filing.

How much tax on ₹25 lakh salary under the old regime?

Under the old regime with only ₹50,000 standard deduction and no other deductions, taxable income is ₹24,50,000 and total tax including cess is approximately ₹5,69,400. If you add deductions such as 80C (₹1,50,000), NPS (₹50,000), and 80D (₹25,000), the figure comes down to around ₹4,99,200 — still higher than the new regime in this example. You need total deductions of roughly ₹8 lakh for the old regime to become competitive at this salary level.

Is tax calculated on CTC or gross salary for a ₹25 LPA package?

Tax is calculated on gross salary, not CTC. CTC includes employer PF, gratuity provision, and group insurance — costs borne by the employer that do not appear in your payslip. A ₹25 LPA CTC may correspond to a gross salary of ₹21–₹23 lakh depending on the employer’s structure. Always ask for your gross salary figure before estimating tax.

What is the monthly TDS on ₹25 LPA salary?

Under the new regime with ₹75,000 standard deduction, estimated monthly TDS is approximately ₹26,650 (₹3,19,800 ÷ 12). Under the old regime with no deductions, monthly TDS would be approximately ₹47,450. Actual TDS depends on your salary breakup, declared regime, declared deductions, and whether bonus is included in any given month.

Can I reduce tax on ₹25 LPA salary?

Yes. Under the new regime, the revised slab structure already reduces your rate burden significantly compared to the old regime. If you want to use the old regime, deductions such as 80C (₹1,50,000), NPS 80CCD(1B) (₹50,000), 80D health insurance (up to ₹25,000–₹50,000), HRA exemption (city and rent dependent), and Section 24b home loan interest (up to ₹2,00,000) can reduce taxable income. At ₹25 LPA, you need approximately ₹8 lakh in total deductions for the old regime to match the new regime’s tax figure.

Is ₹25 LPA eligible for Section 87A rebate?

No. Section 87A rebate under the new regime applies only when taxable income is below the applicable threshold. A ₹25 lakh gross salary produces taxable income of approximately ₹24,25,000 after the standard deduction — well above the rebate limit. No Section 87A relief applies at this income level. The rebate benefits lower income earners, not those at ₹25 LPA.

What happens if I receive an ESOP or RSU payout in the same year as my ₹25 LPA salary?

ESOP and RSU perquisites are taxable in the year of exercise or vesting, as perquisite income under the head “Salaries.” The fair market value on the date of vesting above the exercise price is added to your salary and taxed at slab rates. This can push your total taxable income significantly higher than your salary alone — and may create a surcharge liability if the total exceeds ₹50 lakh. Your employer should ideally include this in TDS computation; verify in your Form 16 Part B.

Does surcharge apply to a ₹25 LPA salary?

No. Surcharge for individual taxpayers applies only when taxable income exceeds ₹50 lakh. At ₹25 LPA gross salary, taxable income after standard deduction is around ₹24,25,000 under the new regime — well below the surcharge threshold. Surcharge is not applicable under either regime at this salary level.

Is the new regime always better for ₹25 LPA earners?

Not necessarily — it depends on your deduction profile. With minimal deductions, the new regime is significantly better (approximately ₹3.20 lakh vs ₹5.69 lakh). But if you pay significant rent and claim HRA, max out 80C, contribute to NPS, have health insurance, and service a home loan with substantial interest, the old regime can narrow the gap. The correct answer comes from running both regimes with your actual numbers, not from a general rule.

Final Verdict

For most salaried employees with a ₹25 lakh salary and a limited deduction profile, the new tax regime for FY 2025-26 is the simpler and lower-tax option — approximately ₹3,19,800 versus ₹5,69,400 under the old regime with no extra deductions. It requires far less paperwork and no investment commitments to claim the benefit.

If you have significant HRA, 80C, home loan interest, and NPS contributions — and can document all of it before your employer’s deadline — the old regime is worth a careful calculation. But at ₹25 LPA, you need roughly ₹8 lakh in total eligible deductions before the old regime becomes the better choice.

The most important step is to use your actual gross salary and your real deduction numbers — not just the headline CTC — to compare both regimes. Use our income tax calculator to see both figures side by side before you file or submit your employer declaration. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.