You open your offer letter, scan the salary breakup, and spot a line that reads CCA: ₹4,000/month. It sounds like a city-living benefit — maybe even something tax-free. Most salaried employees in India make that assumption. It is worth checking carefully before you do.

City compensatory allowance is one of the more commonly misunderstood components in Indian payslips. It sits under the earnings section, adds to gross salary, and carries a name that implies something official. Whether it actually reduces your tax burden, improves your in-hand pay meaningfully, or is simply another taxable addition to your CTC is something this article will answer directly — with a real salary example, a clear comparison with HRA and conveyance allowance, and specific guidance on what you need to verify before filing your ITR.

Quick Answer: City Compensatory Allowance

City compensatory allowance is a salary allowance some employers pay to offset higher living costs in metro or expensive cities. For most salaried employees, CCA is generally treated as taxable salary unless a specific current exemption applies, so it can increase gross pay but may not increase in-hand salary fully.

Key Takeaways

- City compensatory allowance is a discretionary, employer-decided salary component — no central law requires private employers to pay it, and the amount varies entirely by company policy.

- CCA appears under the earnings section of your monthly payslip and is counted as part of both gross salary and CTC.

- For most private-sector salaried employees, CCA is generally taxable as income from salary — it does not carry a specific statutory exemption the way HRA does under Section 10(13A) of the Income Tax Act. Verify the current position before filing your ITR.

- A ₹5,000 monthly CCA does not add ₹5,000 to your in-hand pay — after TDS, the actual take-home gain depends on your applicable income tax slab rate.

- CCA is not linked to your PF or gratuity calculation — both are based on basic salary and, where applicable, dearness allowance.

- When comparing two job offers, always evaluate net monthly in-hand salary rather than CTC — a higher CCA in one offer may simply replace a different taxable component in the other without adding real value.

Key Facts at a Glance

| Feature | Details |

|---|---|

| Full form | City Compensatory Allowance |

| Payslip location | Earnings section — alongside Basic, HRA, Special Allowance |

| Mandatory by law? | No — entirely at employer’s discretion for private sector |

| Part of gross salary? | Yes |

| Part of CTC? | Yes |

| Tax treatment | Generally taxable as salary income — verify current exemption status at incometax.gov.in before filing ITR |

| Linked to PF or gratuity? | No — PF and gratuity are based on Basic (+DA where applicable) |

| HRA-style exemption? | No equivalent Section 10(13A)-type framework — verify current rules |

| Appears in Form 16? | Yes — Part B, under salary income breakup |

| Where to verify | Payslip, offer letter, Form 16, incometax.gov.in |

For a complete breakdown of every line in your monthly payslip, see: salary slip components

What City Compensatory Allowance Actually Means

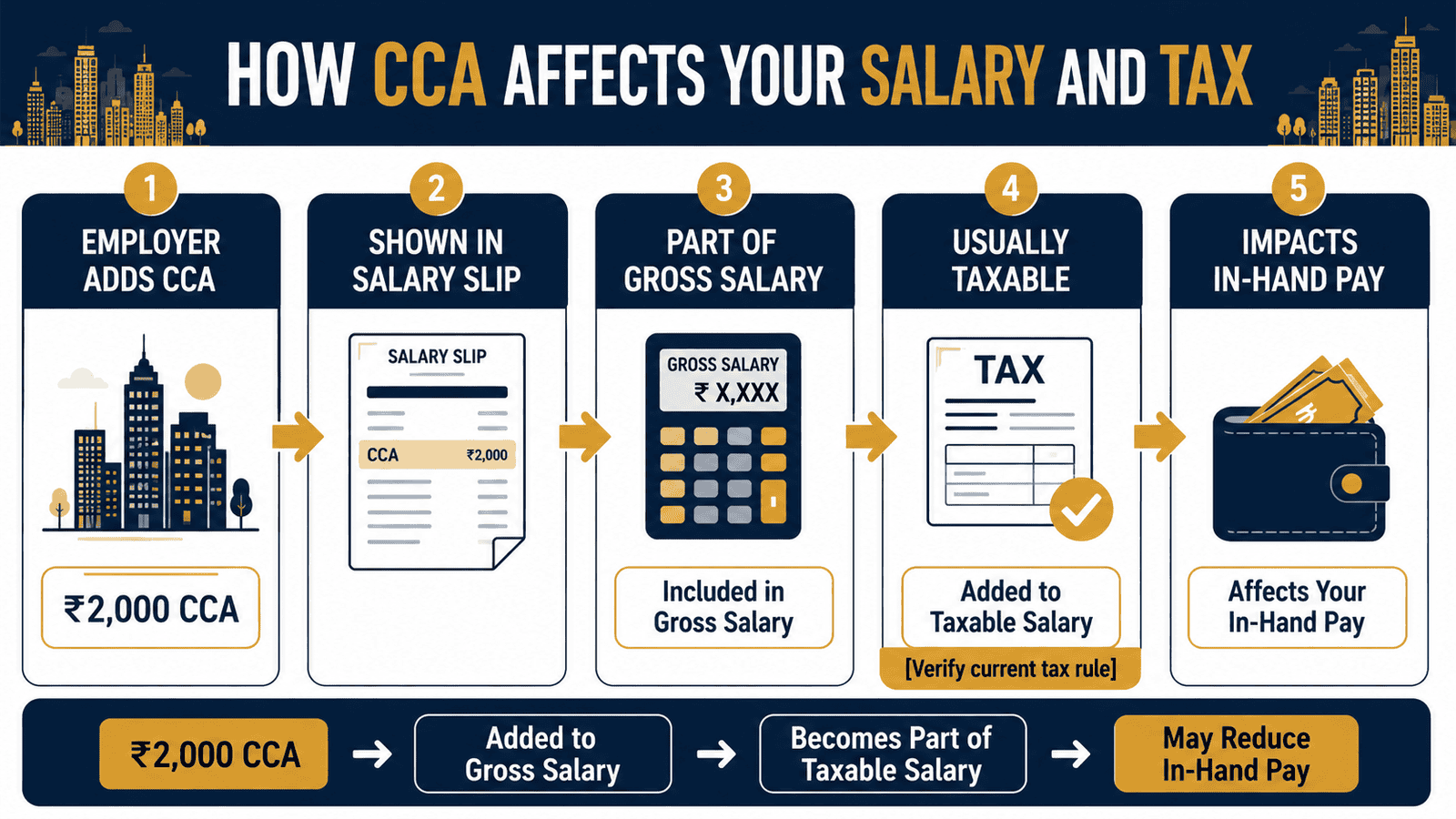

City compensatory allowance — CCA — is a salary component that some employers include in their pay structure to compensate employees posted in metro or high-cost cities. The logic is simple: a software engineer in Mumbai faces higher rent, commute costs, and daily expenses than a colleague doing the same work in a tier-2 city. CCA is the employer’s way of partially reflecting that burden in the salary breakup.

There is no central legislation that obligates private-sector employers to pay CCA. It is a payroll design decision — entirely discretionary. Some companies pay ₹2,000 a month. Others pay ₹8,000. Many do not include it at all and fold the same amount into a broader “special allowance” line. The label changes; the underlying taxability typically does not.

CCA in CTC, Gross Salary, and In-Hand Pay

Understanding where CCA sits in your compensation requires separating three things that employees often treat as one: CTC, gross salary, and in-hand salary.

Cost to company is the employer’s total annual expense — your salary, PF contributions, gratuity provisions, and any other benefits. CCA is typically included here.

Gross salary is the sum of all salary components paid to you before deductions — basic, HRA, CCA, special allowance, and other allowances. CCA adds directly to gross salary and therefore to your reported income from salary.

In-hand salary is what reaches your bank account after TDS on salary, employee PF, professional tax, and any other deductions. If CCA is taxable, TDS is deducted on it — which means a ₹5,000 CCA does not add ₹5,000 in hand. The actual gain is ₹5,000 minus the tax deducted at your applicable rate.

This gap between CTC, gross salary, and actual take-home is one of the most common points of confusion for salaried employees evaluating a new offer. For a full calculation, see: CTC and in-hand pay

Allowance vs Reimbursement — Why the Distinction Matters

CCA is structured as a salary allowance — not a reimbursement. A salary allowance is paid as a fixed monthly amount regardless of actual expenditure; you do not submit bills or receipts to receive it. A reimbursement is typically paid against actual expenses and requires documentary proof. Different provisions of the Income Tax Act may apply to each category depending on the type of allowance and any specific exemption it carries.

Because CCA is an allowance with no bill-submission requirement, it does not fit into the category of expense-linked allowances where the exempt portion is capped at actual spend. Verify how your employer has treated CCA in the TDS calculation — and confirm its classification when you review your Form 16.

What Tax Treatment to Expect

Under Indian income tax rules, allowances received as part of salary are generally taxable under income from salary unless a specific exemption provision applies. HRA has a defined exemption formula under Section 10(13A). Conveyance allowance rules have evolved over time and are now largely absorbed into the standard deduction framework. CCA does not have an equivalent named statutory exemption the way HRA does.

For private-sector employees, CCA is generally treated as fully taxable salary income. Rules governing specific allowances can, however, be updated through Budget notifications or official circulars — which is why verifying the current treatment from incometax.gov.in before computing your tax liability or filing your ITR is always the right step. The word “generally” is important: it reflects common treatment, not a guarantee that no exemption will ever apply to your specific situation or employer category.

Cost of Living Allowance — Other Names for the Same Component

In different payroll systems across India, you may see CCA referred to as cost of living allowance, metro allowance, city allowance, or location allowance. These are functionally the same idea. All carry the same verification requirement: check your payslip, ask payroll how it is treated in TDS, and review Form 16 Part B before filing your ITR.

Real Example: Ankit’s CCA in His Bengaluru Salary Slip

Ankit, 29, is a software engineer at a mid-size IT company in Bengaluru drawing a CTC of approximately ₹12 lakh per year. His monthly salary breakup includes: Basic — ₹40,000 | HRA — ₹16,000 | City Compensatory Allowance — ₹5,000 | Special Allowance — ₹14,000 | Gross Monthly Salary — ₹75,000.

His employer’s TDS computation treats all four components as taxable income from salary. HRA exemption is calculated separately on the HRA component based on actual rent paid. CCA is not exempt — it adds ₹5,000 to his gross taxable salary every month.

At an applicable income tax slab rate of 20%, Ankit effectively keeps approximately ₹4,000 of the ₹5,000 CCA after TDS — not the full amount. His annual CCA of ₹60,000 adds approximately ₹48,000 to his in-hand income over the year, not ₹60,000.

The key insight: CCA improves Ankit’s gross pay and CTC headline, but its after-tax value is meaningfully smaller than it appears. When comparing a competing offer, Ankit should calculate net monthly salary — not compare CTC lines — because a similar CTC structured differently could net him more or less in hand.

How to Calculate CCA’s Impact on Taxable Salary

Gross Salary = Basic + HRA + CCA + Conveyance Allowance + Special Allowance + Other Allowances

Taxable Salary = Gross Salary − Exempt Allowances (if any) − Standard Deduction

Using Ankit’s numbers, if CCA is fully taxable and no specific exemption applies, the ₹60,000 annual CCA is added to his taxable salary figure. The actual in-hand benefit depends on his applicable slab rate and regime choice:

| Applicable Tax Rate | Annual CCA Amount | Approx. In-Hand Gain |

|---|---|---|

| 20% slab | ₹60,000 | ~₹48,000/year (~₹4,000/month) |

| 30% slab | ₹60,000 | ~₹42,000/year (~₹3,500/month) |

These figures are illustrative. Your actual in-hand impact depends on total taxable income, tax regime, surcharge, and applicable cess. Use a salary calculator with your actual declarations to get a precise estimate: monthly take-home pay

Comparison: CCA vs HRA vs Conveyance vs Special Allowance

| Component | Purpose | Tax Treatment Note |

|---|---|---|

| City Compensatory Allowance (CCA) | Offset higher living costs in expensive cities | Generally fully taxable — no specific statutory exemption for private sector; verify current rules |

| HRA (House Rent Allowance) | Cover rental accommodation cost | Partly exempt under Section 10(13A) if rent is actually paid — formula-based calculation; verify current rules |

| Conveyance / Transport Allowance | Cover daily commute expenses | Largely absorbed into standard deduction post-2018 reform; verify current treatment with employer |

| Special Allowance | Residual or balancing salary component | Generally fully taxable — treated as income from salary in most payroll systems |

| Basic Salary | Foundation salary — base for PF, gratuity, HRA | Fully taxable; also determines statutory benefit calculations linked to it |

The critical difference between CCA and HRA: HRA has a defined exemption formula under Section 10(13A) of the Income Tax Act that employees can use to reduce taxable income if they actually pay rent. CCA currently has no equivalent mechanism for private-sector employees. For a complete view of how basic salary affects PF, gratuity, and overall tax liability, see: basic salary impact

For a full explanation of how conveyance allowance works and what its current tax position is, see: conveyance allowance rules

How to Decide What’s Right for You

You are reviewing an offer letter that includes CCA — ask the employer’s HR team for the actual monthly in-hand estimate, not just the CTC breakup. CCA may inflate the headline CTC number without proportionally improving what reaches your bank account.

You are comparing two job offers where one has a higher CCA — calculate net monthly salary for both using the same tax assumptions before deciding. A ₹5,000 CCA difference may result in under ₹4,000 difference in hand after TDS at a 20% slab.

Your CCA was increased during a recent salary revision — check whether basic salary or HRA was simultaneously reduced to accommodate it. An employer shifting amount from basic to CCA may lower your PF accumulation and gratuity entitlement over time, even if gross pay stays identical.

You are filing your ITR and are unsure whether to include CCA — check Form 16 Part B first. Your employer will have already included it in the taxable salary figure if they treat it as taxable. Do not adjust the figure without a documented basis.

You are in the 30% income tax slab and your CTC includes a large CCA amount — explore whether your salary structure can be partially restructured toward tax-efficient components such as NPS employer contribution, where applicable under current rules. Verify options with your HR team and a tax professional.

CCA is not a meaningful financial benefit if your employer has simply renamed a taxable special allowance as CCA without changing the total taxable salary figure — in that scenario, it is a labelling convention, not a compensation advantage worth prioritising in negotiations.

Common Mistakes to Avoid

Assuming CCA Is Tax-Free

Many employees see “City Compensatory Allowance” and assume it comes with a tax exemption — the way HRA does.

For most private-sector salaried employees, CCA is generally treated as fully taxable income from salary with no specific exemption. If this assumption goes unchecked, you may under-declare income or miscalculate advance tax, potentially leading to a demand notice from the Income Tax Department during ITR processing.

Always verify how CCA is categorised in your Form 16 before filing. A named allowance does not automatically carry a named exemption.

Confusing CCA with HRA

Both components appear under earnings in a payslip and both relate to city-related costs. But the similarity ends there.

HRA has a specific exemption formula under Section 10(13A) of the Income Tax Act — it can reduce your taxable income if you actually pay rent and meet the conditions. CCA has no equivalent mechanism. Treating CCA as if it carries HRA-type exemption can lead to incorrect deduction claims, which may trigger a scrutiny assessment.

Check both components separately in Form 16 and apply HRA exemption only on the HRA row.

Comparing Job Offers on CTC Alone

A ₹15 lakh CTC offer heavily loaded with CCA and special allowance may result in less in-hand pay than a ₹14.5 lakh CTC offer structured with more tax-efficient components — depending on your total income and regime.

The difference can easily be ₹2,000–₹4,000 per month — which adds up to ₹24,000–₹48,000 over a year. Always request a net monthly salary estimate from the prospective employer before accepting.

CTC is a cost-accounting number. In-hand salary is what you live on.

Ignoring TDS Deducted on CCA

If your employer treats CCA as taxable — which is the common treatment — TDS will be deducted on it every month throughout the year. Employees who do not account for this in their investment declarations or tax computation may end up with an unexpected demand at year-end, particularly if they have other income sources such as rental income or interest.

Review your monthly payslip to confirm that TDS is being computed on the correct gross taxable salary figure, including CCA.

Not Checking Form 16 Before Filing ITR

CCA may be listed under different labels in different payroll systems. Some employers list it explicitly; others fold it into a broader allowance category. If you file your ITR without reconciling Form 16 Part B against your payslips, you risk under-reporting income or claiming an exemption that does not apply.

Download Form 16 every year, verify the salary breakup line by line, and raise any discrepancy with your payroll team before the ITR filing deadline.

Expecting CCA to Build PF or Gratuity

Provident fund contributions are calculated on basic salary plus dearness allowance — not on CCA or most other allowances. An employee who expects higher PF accumulation because of a large CCA component in their CTC will find that expectation unmet.

If retirement savings through EPF are a priority, ask specifically about the basic salary percentage in any offer — not the CCA amount.

Not Asking Payroll How CCA Is Treated

Tax treatment of CCA can vary in edge cases — particularly for government employees, employees in certain regulated industries, or where employer-specific policies apply. Assuming the standard private-sector treatment without confirming it with your payroll team is a risk, especially if you are doing your own advance tax calculation or ITR computation outside of Form 16.

A single email to payroll asking “Is CCA included in my taxable salary for TDS?” takes minutes and removes uncertainty at filing time.

When This May Not Be the Right Choice

City compensatory allowance may not translate into a meaningful benefit in your specific situation if any of the following apply:

Your employer has restructured your salary to introduce CCA. If basic salary or HRA was reduced to accommodate the CCA addition, your gross pay and tax position may be unchanged — or worse, your PF base and gratuity entitlement may have dropped. Verify the before-and-after in-hand impact explicitly.

CCA is simply another name for special allowance. Some payroll systems relabel taxable balancing components as “CCA” without any city-cost rationale. If the tax treatment is identical to what was previously called special allowance, the benefit is zero beyond rebranding.

You are in a lower income bracket where the difference is negligible. For employees with total income under ₹7 lakh, the in-hand impact of a ₹2,000–₹3,000 CCA is marginal after tax. Focusing on total gross salary, HRA structure, and 80C utilisation will have a much larger effect on take-home and tax savings than the presence or absence of CCA.

Your actual city living costs far exceed the CCA amount. A ₹3,500 CCA in Mumbai or Bengaluru, where rent alone can be ₹20,000–₹50,000 per month, provides minimal cost relief. Salary negotiations based on total in-hand pay and actual cost-of-city differential are more effective than focusing on CCA as a standalone component.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

The tax treatment of salary components — including city compensatory allowance — is governed by the Income Tax Act and related Budget notifications. Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- Income Tax Department — incometax.gov.in — for current rules on taxability of salary allowances, applicable exemption provisions, and ITR filing requirements for salaried employees

- Your employer’s payroll or HR team — for how CCA is specifically classified in your TDS computation and salary structure

- Form 16 (Part B) — the employer-issued document showing the exact salary breakup, taxable components, and any exemptions claimed for the financial year

- EPFO — epfindia.gov.in — if you need to confirm which salary components form part of your PF wage base and whether CCA has any PF-related relevance in your employer’s structure

For a step-by-step explanation of how taxable salary is computed from your gross pay, see: taxable salary calculation

Expert Tips

- When you receive an offer letter that includes CCA, ask HR for the estimated monthly in-hand figure — not just the annual CTC. This takes one email and removes the most common salary expectation mismatch before you join.

- If your employer allows salary restructuring, check whether NPS employer contribution (deductible under Section 80CCD(2)) or another tax-efficient component can replace part of a high CCA. At a 30% slab, converting ₹5,000/month of taxable CCA into an NPS employer contribution could save approximately ₹1,500/month in TDS — verify current limits and rules at incometax.gov.in before acting.

- Download Form 16 Part B every April after financial year end and reconcile the salary breakup against your payslips month by month. If CCA is listed differently or an exemption appears that was not discussed with payroll, raise it before filing ITR.

- Keep all payslips and offer letters for at least three years. If the Income Tax Department raises a query about salary income or TDS mismatch, having the salary-component breakup from each month resolves most disputes quickly.

- When evaluating a city transfer or relocation, do not rely on CCA as your cost-of-living adjustment benchmark. Compare net monthly salary at the new city location against actual rent, commute, and cost estimates — the gap is often wider than the CCA amount covers.

- If two competing job offers have different CCA amounts within a similar CTC range, run both through a take-home salary calculator using the same regime and investment declarations. Small CCA differences routinely disappear or reverse once actual TDS is applied at your slab.

Frequently Asked Questions

What is city compensatory allowance in salary?

City compensatory allowance is a salary component some employers pay to employees posted in metro or high-cost cities, intended to partially compensate for higher living expenses. It appears under the earnings section of a monthly payslip and is counted as part of gross salary and CTC. No central law mandates it for private-sector employees — it is an employer payroll policy decision.

Is city compensatory allowance taxable or exempt?

For most private-sector salaried employees, CCA is generally treated as fully taxable income from salary. It does not carry a specific statutory exemption comparable to what HRA receives under Section 10(13A) of the Income Tax Act. Tax rules can change with each Budget or notification, so always verify the current treatment from incometax.gov.in and cross-check with your Form 16 before filing your ITR.

Is CCA part of CTC?

Yes. CCA is typically included in the cost-to-company calculation. It also adds to gross salary. However, because it is generally taxable, it does not offer the same effective value as tax-exempt or tax-advantaged components at the same CTC figure — the in-hand gain is smaller than the stated CCA amount once TDS is factored in.

Does CCA appear in my payslip?

Yes. CCA typically appears under the earnings section of your monthly payslip alongside basic salary, HRA, and special allowance. Some employers label it “City Compensatory Allowance”; others abbreviate it as “CCA.” If you cannot find it by either name, check with your HR or payroll team for the exact label used in your company’s salary system.

What is the difference between CCA and HRA?

HRA — House Rent Allowance — is a salary component specifically linked to rental accommodation, with a defined tax exemption formula under Section 10(13A) of the Income Tax Act. If you pay rent and meet the conditions, HRA exemption can meaningfully reduce your taxable income. CCA is a city cost-of-living allowance with no equivalent exemption framework for private-sector employees. HRA requires rent receipts to claim exemption; CCA does not involve bill submission and does not carry a comparable exemption calculation.

What is the difference between CCA and conveyance allowance?

Conveyance or transport allowance is specifically intended to cover daily commute costs between home and workplace. CCA is a broader city cost-of-living allowance with no commute-specific rationale. The tax treatment of conveyance allowance has also evolved — it was largely absorbed into the standard deduction framework after 2018. CCA has no specific commute link and should be verified for its current tax treatment separately from conveyance-related provisions.

Does CCA increase my in-hand salary?

It increases your gross salary, but the actual in-hand gain is smaller than the stated CCA amount because TDS is deducted on it. As an illustrative example: if CCA is ₹5,000 per month and your applicable slab rate is 20%, the approximate in-hand gain after TDS would be around ₹4,000 per month. At a 30% slab, it would be approximately ₹3,500. The exact figure depends on your total taxable income, tax regime, and applicable cess — calculate using your actual declared income and regime choice.

Can I ask my employer to restructure CCA into a more tax-efficient component?

Some employers allow salary restructuring within the same CTC. If your employer offers this, it may be worth exploring whether shifting part of the CCA into NPS employer contribution — eligible for deduction under Section 80CCD(2) — reduces your total TDS. Confirm restructuring options with HR, verify the current deduction limits at incometax.gov.in, and consult a qualified tax professional before making any changes to your salary structure.

What happens if my offer letter mentions CCA but my payslip does not show it?

CCA is not a statutory entitlement in the private sector, so enforceability depends on your employment contract. If the offer letter explicitly states a CCA amount that is not appearing in your payslip, that is a contractual matter. Compare your offer letter, appointment letter, and payslips carefully, then raise the discrepancy in writing with your HR department.

Is CCA the same as special allowance?

Not necessarily — though both are typically taxable. Special allowance is a residual or balancing component in many Indian salary structures, used to make the total CTC add up to the target figure. CCA carries a city-cost rationale by name. In practice, some employers use the two interchangeably in their payroll systems. What matters is how each component is treated in your TDS computation and what appears in Form 16 Part B — the label is secondary to the tax classification.

Final Verdict

City compensatory allowance is a legitimate salary component worth understanding — but it is not a guaranteed tax-saving benefit. For most private-sector salaried employees, CCA adds to gross salary and is generally treated as taxable income from salary, which means a ₹5,000 CCA adds roughly ₹3,500–₹4,000 to in-hand pay after TDS — not the full amount. It is fundamentally different from HRA and should not be evaluated with the same exemption assumptions.

If you are assessing a job offer, use net monthly in-hand salary as your benchmark — not CTC. If you are filing your ITR, verify how CCA is classified in your Form 16 and do not claim exemptions that are not applicable. For a complete picture of how your salary components interact with your take-home pay, start here: CTC and in-hand pay

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.