You get your appraisal letter. It says 10% hike. You reach for a salary increment calculator, divide the numbers, and expect roughly ₹8,333 extra per month. But when salary hits your bank account, the actual increase is closer to ₹5,000 to ₹5,600. The gap is real — and it has a clear explanation.

PF, TDS, and professional tax all take their share before a hike reaches your bank account. This article explains exactly how a salary increment flows from CTC to in-hand, what inputs matter for an accurate estimate, and why your real monthly raise is almost always smaller than the number on your appraisal letter.

Quick Answer: Salary Increment Calculator

A salary increment calculator helps you estimate your new monthly in-hand salary after a hike by comparing old CTC, new CTC, taxable salary, PF, TDS and deductions. For example, a 10% hike on ₹10 LPA may not increase take-home by exactly 10% because tax slabs and payroll rules can change. Use our take-home pay estimate to calculate your full monthly salary from your revised CTC.

Salary Increment Calculator: How to Estimate Your In-Hand Pay

Work through these four steps using your own numbers. The result is an estimate — your actual payslip may differ based on salary structure, mid-year corrections, and how your employer applies the revision.

Step 1 — Calculate your new CTC.

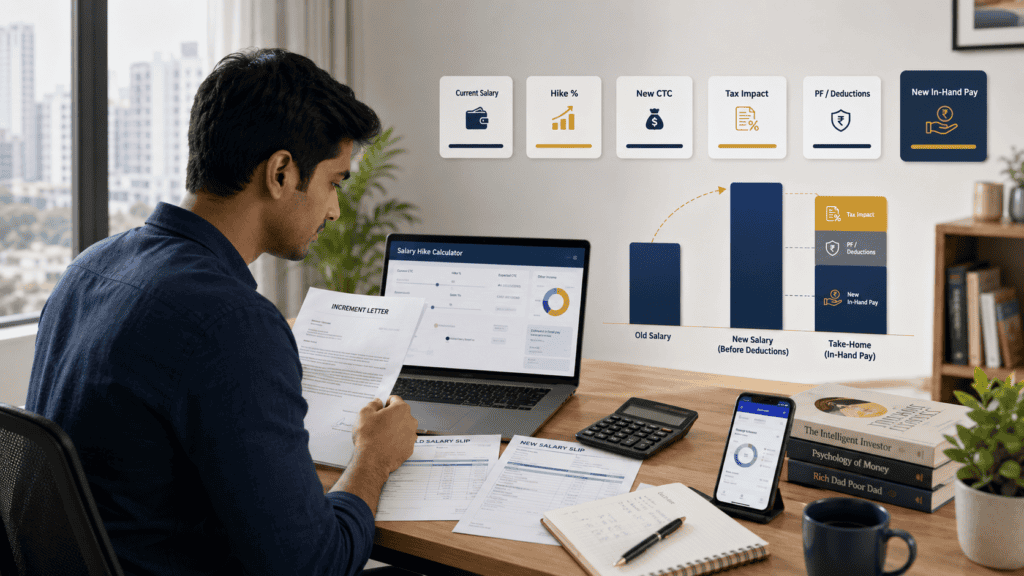

New CTC = Old CTC × (1 + Hike % ÷ 100)

Example: ₹10,00,000 × (1 + 10 ÷ 100) = ₹11,00,000.

Step 2 — Estimate monthly gross salary. Divide your annual fixed pay by 12. Fixed pay is CTC minus variable pay, employer PF contribution, and gratuity provision. Monthly gross is typically lower than CTC ÷ 12 because employer-side costs are bundled into CTC but never arrive as monthly bank credits.

Step 3 — Identify monthly deductions. Three deductions reduce monthly gross before your salary is credited: employee PF (12% of basic salary per EPFO), estimated TDS on salary (annual tax estimate divided across the year by your payroll team), and professional tax (varies by state, capped at ₹2,400/year in most states).

Step 4 — Arrive at estimated monthly in-hand.

Monthly In-Hand ≈ Monthly Gross − Employee PF − Monthly TDS − Professional Tax

The table below applies this logic to three common hike scenarios on a ₹10 LPA base CTC. All figures are illustrative estimates — actual in-hand depends on your salary structure, tax regime, deductions claimed, and current slab rates.

| Scenario | Key Inputs | Estimated Result |

|---|---|---|

| 5% hike — ₹10.5 LPA | Monthly gross up ~₹3,500; basic up ~₹1,500 | In-hand increase ~₹2,700–₹3,000/month |

| 10% hike — ₹11 LPA | Monthly gross up ~₹6,500; basic up ~₹3,000 | In-hand increase ~₹5,000–₹5,600/month |

| 20% hike — ₹12 LPA | Monthly gross up ~₹13,000; basic up ~₹6,000 | In-hand increase ~₹9,800–₹10,800/month |

Key Takeaways

- A 10% CTC hike on ₹10 LPA adds approximately ₹5,000–₹5,600 to monthly in-hand pay — not ₹8,333 — because PF, TDS, and professional tax all increase alongside the hike.

- Employee PF is 12% of basic salary. If basic salary rises with the hike, PF deductions rise too — reducing immediate take-home while adding to your retirement savings.

- A hike that pushes your annual taxable income across a tax slab threshold increases monthly TDS from the revision month, sometimes sharply in the first cycle.

- Variable pay and performance bonuses included in CTC are not credited monthly — your fixed monthly gross is the only correct base for in-hand calculations.

- Professional tax is a state-level deduction capped at ₹2,400/year in most states; it is relatively stable but varies by state and income threshold.

- The payslip — not the hike letter or any calculator — is the only reliable confirmation of your actual revised in-hand salary.

Key Facts at a Glance

| Term | Definition | Impact on In-Hand Salary |

|---|---|---|

| Old CTC | Current total cost to company, annual | Starting point for hike percentage calculation |

| New CTC | Old CTC × (1 + hike %) | Higher CTC does not mean the same % increase in monthly in-hand |

| Monthly gross salary | Fixed pay components credited before deductions | Base from which PF, TDS, and PT are subtracted |

| Employee PF | 12% of basic salary, deducted monthly per EPFO | Reduces monthly credit; builds retirement corpus |

| Standard deduction | Flat annual deduction from gross salary for tax computation | Reduces taxable income; slightly lowers TDS |

| TDS on salary | Employer deducts estimated annual tax and credits monthly | Largest variable deduction — rises with higher taxable income |

| Professional tax | State-level employment tax, max ₹2,400/year in most states | Small fixed monthly deduction; varies by state |

| Estimated in-hand | Monthly gross − PF − TDS − professional tax | Amount credited to your bank account each month |

Why Your Salary Increment Does Not Fully Convert to In-Hand Pay

CTC hike versus gross salary hike

Your CTC includes components that do not arrive as monthly bank credits. Employer PF contribution (12% of basic salary) is a CTC cost your employer pays on your behalf — it goes directly to your EPFO account, not into your salary transfer. Gratuity provisions, group health insurance premiums, and similar benefits add to CTC but reduce the visible monthly credit.

When CTC increases by ₹1,00,000, the actual increase in monthly gross salary is typically ₹5,000 to ₹7,500 — depending on how your employer structures the revised breakup. The remainder is absorbed by employer-side CTC costs. To understand exactly how CTC differs from what you actually earn, read our guide on CTC versus in-hand.

The path from CTC to bank credit

Think of salary as passing through three layers before it becomes a bank deposit. First, CTC is reduced by employer-side costs (employer PF, gratuity provision) to arrive at gross salary. Second, gross salary is reduced by employee-side deductions (employee PF, professional tax) to arrive at net salary. Third, TDS is deducted from this based on your estimated annual tax liability.

A salary increment adds to CTC — but each layer takes its share before the increase reaches you. This is why a 10% CTC hike rarely translates into anything close to a 10% in-hand increase. For a side-by-side breakdown of these salary layers with worked examples, see our article on gross and net pay.

How PF interacts with a salary hike

Employee PF is 12% of basic salary. If your employer raises basic salary as part of the revised structure — which is common — employee PF rises proportionally. A basic increase from ₹30,000 to ₹33,000 per month adds ₹360 to your monthly PF deduction. That ₹360 is not lost: both the employee share and the employer’s matching contribution continue to earn EPF interest. But it does reduce immediate take-home relative to what you might have expected.

Some employers cap basic salary increases to control PF growth, absorbing the hike more heavily into special allowances. This increases take-home but slows retirement savings growth. Your payslip will show exactly where the revised pay has been allocated.

TDS and the tax regime after a hike

Your payroll team estimates your annual taxable income at the start of the financial year. When a hike is processed mid-year, they recalculate the remaining tax liability and spread it over the remaining months. This means TDS can jump noticeably in the first revised payroll cycle, then normalise.

The regime you are on — old or new — determines how taxable salary is computed. Under the new tax regime, a standard deduction is available from gross salary before income tax is computed. Under the old regime, deductions under Section 80C, HRA, Section 24b, and others may reduce taxable income further. A hike that pushes your taxable salary above a key threshold in either regime triggers a higher marginal tax rate on the additional income, meaningfully increasing TDS. The Income Tax Department at incometax.gov.in is the authoritative source for current slab rates and standard deduction limits.

Real Example: Rohan’s 10% Hike in Pune

Rohan, 29, is a software analyst in Pune earning ₹10 LPA CTC. His current salary structure: Basic ₹30,000/month, HRA ₹15,000/month, Special Allowance ₹20,000/month — monthly gross ₹65,000. Monthly deductions: employee PF ₹3,600 (12% of basic), professional tax ₹200, estimated TDS ₹1,900. Rohan’s monthly in-hand is approximately ₹59,300.

After a 10% hike, his new CTC is ₹11 LPA. Revised structure: Basic ₹33,000/month, HRA ₹16,500/month, Special Allowance ₹22,000/month — monthly gross ₹71,500. Revised deductions: employee PF ₹3,960, professional tax ₹200, estimated TDS ₹2,900 (higher, as annual taxable income has grown). New monthly in-hand: approximately ₹64,440.

Actual monthly in-hand increase: approximately ₹5,140. The monthly share of a ₹1,00,000 CTC hike — ₹8,333 — is the figure most employees expect. The gap of approximately ₹3,193 per month reflects higher PF contributions and increased TDS on a larger taxable income. All TDS figures here are illustrative estimates; actual TDS depends on the tax regime, deductions claimed, and current slab rates as published by the Income Tax Department. Use the salary slip components guide to identify each of these line items on your own payslip.

Key insight: CTC arithmetic will consistently overstate your monthly in-hand gain. Always calculate from revised monthly gross — not from CTC ÷ 12.

Comparison: 5% vs 10% vs 20% Hike on ₹10 LPA

| Hike Scenario | New CTC and Gross Change | Estimated Monthly In-Hand Increase |

|---|---|---|

| 5% hike — ₹10.5 LPA | Gross up ~₹3,500/month; basic up ~₹1,500 | ~₹2,700–₹3,000; modest TDS rise if within same slab |

| 10% hike — ₹11 LPA | Gross up ~₹6,500/month; basic up ~₹3,000 | ~₹5,000–₹5,600; TDS rises as taxable income grows |

| 20% hike — ₹12 LPA | Gross up ~₹13,000/month; basic up ~₹6,000 | ~₹9,800–₹10,800; significant TDS jump if slab changes |

All ranges are illustrative estimates. Actual in-hand increase depends on your exact salary breakup, tax regime, deductions claimed, variable pay allocation, and whether the revision is mid-year or at year start.

How to Decide What’s Right for You

Your entire hike is in fixed pay — THEN your monthly gross increases from the revision month. Use the formula in this article to estimate in-hand after PF and TDS adjustments. The first revised payslip will confirm the actual number.

A significant portion of your hike is in variable pay or annual performance bonus — THEN your fixed monthly gross may increase far less than the headline CTC hike. Ask HR for the fixed versus variable pay breakup before planning monthly expenses around the new CTC figure.

Your hike pushes annual taxable income above a key income tax threshold — THEN TDS will increase from the revised month. Review whether your current tax regime still makes sense. Use our comparison of the old or new regime to run this check after every appraisal cycle.

Your basic salary increases with the hike — THEN employee PF (12% of basic) also increases. Plan your monthly budget from the actual in-hand figure, not gross. The extra PF contribution earns EPF interest and grows your retirement corpus — it is not a deduction to resent.

Your revision is mid-year — THEN payroll may recalculate total annual tax liability across the remaining months. TDS in the first revised cycle can be higher than subsequent months as the annual estimate is corrected. Wait for month two before drawing conclusions about your stabilised in-hand.

Your revised payslip does not reflect the hike within one payroll cycle of the effective date — do not assume it is being processed silently. Follow up with HR using the appraisal letter as reference and confirm the payroll effective date.

Common Mistakes to Avoid

Calculating the hike on monthly in-hand instead of annual CTC

Many employees multiply their current monthly in-hand by the hike percentage and expect that as extra monthly credit.

If monthly in-hand is ₹59,300 and CTC is ₹10 LPA, a 10% hike adds ₹1,00,000 to CTC — not ₹5,930 to monthly in-hand. Applying the hike percentage to in-hand produces a number that is both mathematically wrong and significantly lower than the actual hike.

Always apply the hike percentage to annual CTC first, then estimate the monthly in-hand impact using the deduction steps in this article.

Treating the full monthly CTC gain as spendable income

Dividing a ₹1,00,000 annual hike by 12 gives ₹8,333 on paper. After PF and TDS, the actual monthly credit can be ₹5,000 to ₹5,600.

Committing to a new EMI or higher rent based on ₹8,333 before seeing the first revised payslip can create a cash flow problem — especially if TDS spikes sharply in month one of the revision. Wait for the payslip, then plan.

Ignoring variable pay and bonus splits in the hike letter

A revised CTC of ₹12 LPA may include ₹1.5 lakh in annual variable pay. That ₹12,500/month exists on paper only — it is not a monthly credit.

Always request the fixed pay versus variable pay breakup from HR. Your fixed monthly gross — not total CTC — is the only correct base for monthly budget or EMI planning after an increment.

Forgetting that TDS can spike in the first revised payroll month

When a mid-year hike is processed, payroll corrects the annual tax estimate across remaining months. TDS in the first revised cycle is sometimes higher than what will stabilise later.

If TDS looks unusually high in month one of the revised salary, ask your HR or payroll team whether it normalises from the following month. This is expected payroll behaviour, not an error.

Not accounting for PF increase if basic salary rises

A ₹3,000 increase in monthly basic salary adds ₹360 per month to employee PF deduction — ₹4,320 less in annual take-home than a simple CTC calculation would suggest.

Factor in the revised PF deduction when estimating in-hand after a hike. Check the new basic salary on your revised payslip and recalculate PF accordingly before finalising any monthly plan.

When This May Not Be the Right Choice

A salary increment calculator provides a useful directional estimate but may not be reliable in these situations:

Complex salary structures with flexible benefit plans or perquisites. If your CTC includes car lease, accommodation, club membership, or LTA components, the taxable treatment differs from standard salary components. A simple calculator will not capture this and may significantly understate your actual TDS.

Your hike CTC includes a joining bonus or one-time retention payment. These inflate the headline CTC but are typically taxable in the year of receipt and are not monthly credits. Comparing a revised CTC that includes such a bonus to your old CTC overstates the real recurring raise.

You have other income sources — rental income, capital gains, freelance, or interest income. TDS on salary depends on total annual income, not salary alone. A calculator modelling only salary income will underestimate your actual tax deduction after a hike.

You are mid-year changing tax regime or your employer is migrating payroll systems. These transitions can produce temporary deduction anomalies that do not reflect your steady-state in-hand salary.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Every figure used in a salary increment calculator — tax slabs, standard deduction, EPF contribution rates, and professional tax limits — is subject to change with each Union Budget or regulatory update. Verify current rates from these official sources before relying on any estimate:

- Income Tax Department — incometax.gov.in: Current income tax slabs, standard deduction amount, TDS provisions on salary, and details of the old and new tax regimes for the applicable financial year.

- EPFO — epfindia.gov.in: EPF contribution rates, applicable wage ceiling for statutory contributions, and both employer and employee contribution rules.

- State government finance or labour department: Professional tax rates and income thresholds vary by state. Check your state government’s relevant department for the slab applicable at your work location.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Do not plan your post-hike budget from the appraisal letter. Wait for the first revised payslip — it shows exactly what arrived after PF, TDS, and professional tax. Salary planning from CTC instead of actual credits is one of the most common sources of post-hike financial stress.

- After every increment, re-run your old-versus-new tax regime comparison. A hike that crosses a key income threshold can shift which regime saves more tax for the year. What was optimal at ₹10 LPA may not be at ₹11 LPA or ₹12 LPA. Use our detailed comparison of the old or new regime as a starting point.

- Commit 20–30% of every real in-hand gain to a SIP increase or recurring deposit before lifestyle expenses expand to fill the gap. Automate the step-up on the same day the revised salary is credited. A framework for this is in our guide on how to invest every hike.

- If your basic salary increased with the hike, check your EPF passbook within 60 days to confirm the updated contribution is being deposited. Payroll delays in notifying EPFO can result in contributions being processed at the old basic rate for one or two months.

- Ask HR for the formal revised salary breakup document — not just the offer letter or hike letter. This shows Basic, HRA, Special Allowance, variable pay, employer PF, and gratuity provision separately, giving you all the inputs needed to build an accurate in-hand estimate.

- Revisit your emergency fund target after every increment. If monthly expenses or EMI obligations have grown, a 3–6 month emergency fund calibrated to your old expenses is now underfunded. Recalibrate in the second month after your revised salary has stabilised.

Frequently Asked Questions

How do I calculate a 10% salary hike?

Multiply your current annual CTC by 0.10 to find the hike amount, then add it to CTC. For example, 10% on ₹10 LPA = ₹1,00,000 — new CTC is ₹11 LPA. Then estimate monthly gross (annual fixed pay ÷ 12), subtract employee PF (12% of basic), estimated TDS, and professional tax to arrive at estimated monthly in-hand.

Does a CTC hike increase in-hand salary by the same percentage?

No. A 10% CTC hike almost never produces a 10% increase in monthly in-hand salary. The gap comes from increased employee PF if basic salary rises, higher TDS as taxable income grows, and employer-side CTC components like employer PF and gratuity that never arrive as monthly credits. In most mid-bracket salary scenarios, the actual in-hand increase is roughly 60–70% of the implied monthly CTC gain.

Why did my TDS increase after my salary hike?

When your salary increases, your employer recalculates estimated annual tax on the revised income. If the higher taxable salary crosses a higher slab, a greater marginal rate applies on the additional income. Payroll spreads the revised annual tax estimate across the remaining months of the financial year — which can cause TDS to be higher in the first revised month before it normalises. This is expected payroll behaviour, not an error. Verify current slab rates at incometax.gov.in.

Does PF increase after a salary increment?

Yes, if your basic salary increases with the hike. Employee PF is 12% of basic. If basic goes from ₹30,000 to ₹33,000/month, PF rises from ₹3,600 to ₹3,960/month. The additional ₹360 per month reduces immediate take-home but increases the amount accumulating in your EPFO account — both the employee and employer shares earn EPF interest. Verify current EPF contribution rates at epfindia.gov.in.

Is salary increment taxable in India?

Yes. All salary income — including increments — is taxable under the head “Income from Salary” as per the Income Tax Act. Your total annual taxable salary (gross minus applicable deductions or standard deduction depending on your regime) determines your tax liability. Your employer adjusts TDS from the revision month to reflect the higher income. Verify provisions for the current assessment year at incometax.gov.in.

What is the salary increment percentage calculator formula?

To find the hike percentage: Hike % = ((New CTC − Old CTC) ÷ Old CTC) × 100. For example, if old CTC is ₹10 LPA and new CTC is ₹11 LPA, hike % = ((11 − 10) ÷ 10) × 100 = 10%. This tells you the percentage applied to CTC — the actual in-hand impact requires the full deduction calculation described earlier in this article.

Can my in-hand salary decrease after a hike?

Permanently, no. But in the first payroll cycle after a mid-year revision, TDS may spike as payroll corrects the annual tax shortfall across remaining months. This typically normalises in month two. If in-hand genuinely decreases and does not recover after two to three payroll cycles, review the payslip carefully and raise it with HR immediately.

Which calculator should I use for take-home after a hike?

Start with the step-by-step formula in this article for a quick estimate of the hike’s impact. For a complete monthly in-hand calculation from your full new CTC — including all components, deductions, tax regime choice, and HRA — use our take-home pay estimate tool.

Final Verdict

A salary increment calculator is a useful starting point — but the payslip delivers the truth. Before committing to any new EMI, SIP target, or rent increase after a hike, wait for your first revised salary credit and compare it directly to your previous month’s payslip.

As a practical rule: expect your actual monthly in-hand increase to be roughly 60–70% of the implied monthly CTC gain, depending on your tax bracket, basic salary structure, and whether the revision is mid-year. The remainder is absorbed by higher PF contributions, increased TDS, and employer-side CTC costs that were never monthly credits.

Judge every salary increment by its real in-hand impact — not the appraisal letter headline. Use this salary increment calculator logic alongside our full take-home pay estimate for the most complete picture. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.