You own a flat and someone pays you rent every month. That rent feels like extra income — and it is. But the Income Tax Department sees it differently. Rental income sits in its own tax bucket called “Income from House Property,” and it comes with its own set of deductions, rules, and ITR schedules that many landlords get wrong. If you are a salaried employee receiving ₹30,000–₹40,000 a month in rent, you are not alone in wondering whether you owe tax on the entire amount or only on what remains after deductions. This article walks you through the full rental income tax calculation in India: what counts as taxable, which deductions reduce your bill, and how to declare it correctly in your ITR without missing a single step.

Quick Answer: Rental Income Tax

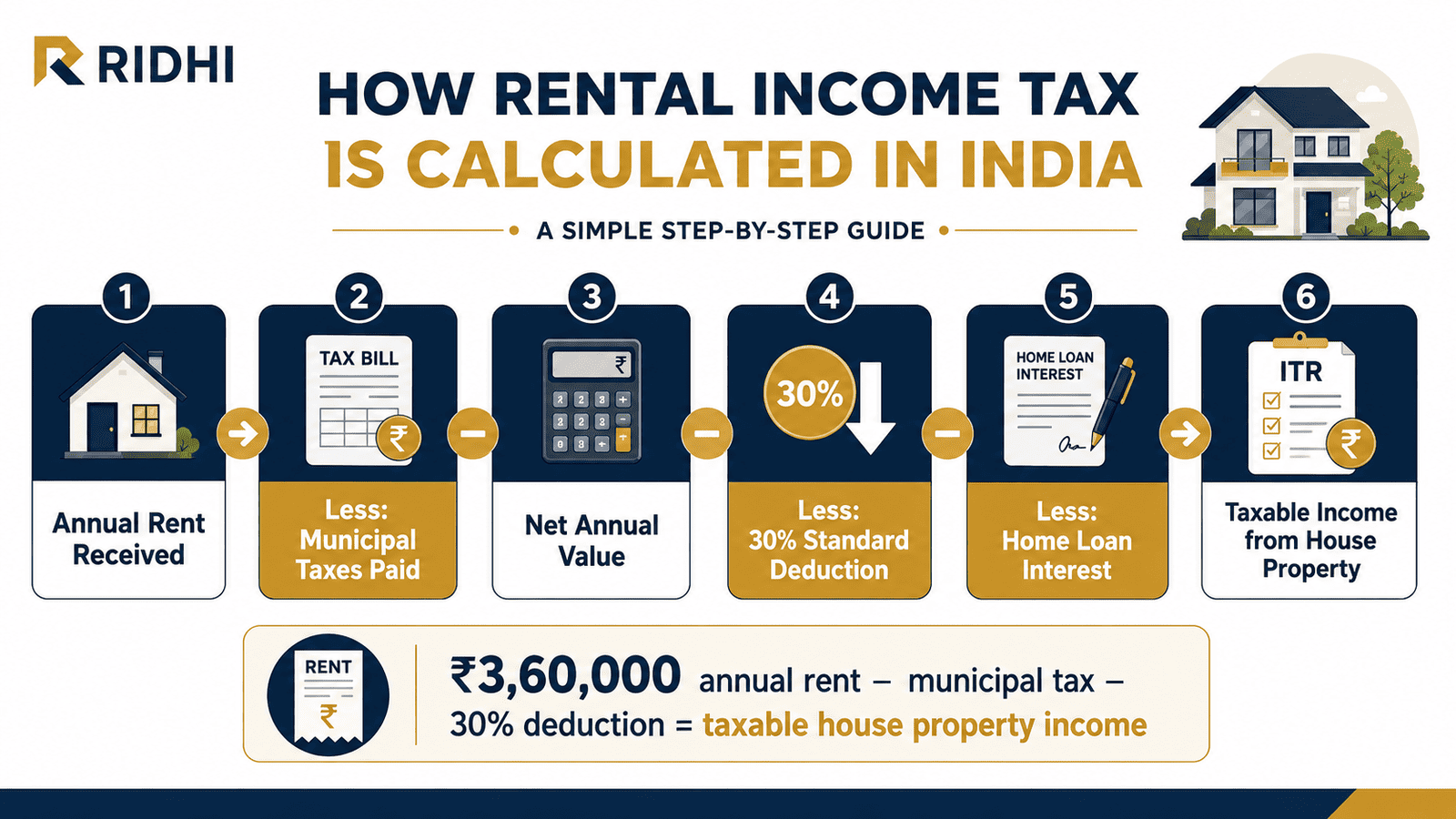

Rental income tax is calculated under “Income from House Property” after reducing eligible municipal taxes, a 30% standard deduction, and allowed home loan interest. For example, ₹3,60,000 yearly rent is not fully taxable if valid deductions apply and the final amount is declared in ITR.

Key Takeaways

- Rental income is taxed under “Income from House Property” — not under “Income from Other Sources” for most landlords.

- The 30% standard deduction under Section 24(a) is automatically applied on Net Annual Value, reducing taxable income by nearly one-third before any other claim.

- If your property has a home loan, the interest paid is deductible under Section 24(b) — with no upper limit for a let-out property under the old tax regime.

- Municipal taxes actually paid by the owner in the financial year are deducted from Gross Annual Value before arriving at Net Annual Value.

- If your net tax liability exceeds ₹10,000 for the year, you must pay advance tax in four instalments — failure attracts interest under Section 234B and 234C.

- Rental income shows up in your AIS and Form 26AS if TDS was deducted — always cross-check before filing to avoid a notice.

- Under the new tax regime, Section 24(b) interest deduction on a let-out property is still allowed, but the set-off against other income is restricted.

Key Facts at a Glance

| Parameter | Rule / Limit | Applicable To |

|---|---|---|

| Tax head | Income from House Property | All rental income from property |

| Standard deduction (Section 24a) | 30% of Net Annual Value | Let-out and deemed let-out property |

| Home loan interest (Section 24b) | Actual interest paid — no upper cap for let-out | Let-out property, old tax regime |

| Municipal tax deduction | Actual amount paid by owner during the FY | Let-out and deemed let-out property |

| TDS by tenant | 10% if monthly rent exceeds ₹50,000 | Tenant is required to deduct |

| Loss set-off cap (new regime) | House property loss cannot be set off against salary | New tax regime taxpayers |

| Advance tax threshold | ₹10,000 net liability triggers advance tax requirement | All taxpayers including salaried |

| ITR form | ITR-1 (one let-out property) or ITR-2 (two or more) | Salaried landlords |

How Rental Income Tax Works in India

Most people assume rental income is simply rent received minus expenses. The Income Tax Act works differently. It has a specific formula that starts from a concept called Gross Annual Value — not just the rent you collected.

The Three Property Types You Need to Know

Before calculating, you need to identify which category your property falls into. taxable income basics vary depending on the income head, and house property is one of the five defined heads under the Income Tax Act.

- Self-occupied property: You live in it. No rental income arises. Section 24(b) interest deduction is capped at ₹2 lakh per year under the old regime.

- Let-out property: You have rented it out. Actual rent received forms the basis of your Gross Annual Value.

- Deemed let-out property: If you own more than two properties and do not live in all of them, the additional ones are treated as deemed let-out — even if they are vacant — and a notional rent is added to your income.

Gross Annual Value: What It Means

Gross Annual Value (GAV) is the higher of: the actual rent received or receivable, or the fair rental value of the property (what the property could reasonably earn). For most standard residential lets, actual rent received is taken as GAV. According to Income Tax Department guidelines on incometax.gov.in, GAV for a let-out property is determined based on actual rent where rent is not below the expected fair value.

From GAV to Net Annual Value

Once you have the GAV, subtract municipal taxes actually paid by you (the owner) during the financial year. This gives you the Net Annual Value (NAV).

NAV = GAV − Municipal Taxes Paid by Owner

Important: municipal taxes paid by the tenant do not qualify. Only taxes paid by you in that specific financial year are deductible — even if they relate to arrears of a previous year.

Section 24 Deductions: Where Your Tax Bill Shrinks

Section 24 of the Income Tax Act provides two deductions from NAV:

- Section 24(a) — Standard Deduction: A flat 30% of NAV. This is automatic — you do not need to prove any expenses. Repairs, insurance, painting, maintenance — all covered under this flat rate.

- Section 24(b) — Home Loan Interest: Actual interest paid on a home loan for the let-out property. No upper cap applies under the old tax regime for let-out properties. Under the new tax regime, the deduction is still available but the resulting loss cannot be set off against salary income.

What About the New Tax Regime?

Under the new tax regime, Section 24(b) interest on a let-out property remains deductible — this is a common misconception. What changes is that if after all deductions your house property income turns negative (a loss), you cannot set it off against your salary or any other income head. The loss can be carried forward for eight years and set off against future house property income only.

This is a major difference for salaried landlords with large home loans on rented properties. If you are comparing regimes, our new vs old tax regime comparison covers this trade-off in detail.

TDS on Rent — When Your Tenant Deducts Tax

If your tenant pays you more than ₹50,000 per month, they are legally required to deduct TDS at 10% under Section 194-IB. This TDS is reflected in your AIS and Form 26AS. When you file your ITR, you claim this TDS as credit. Failure to report this income while TDS has already been deducted is one of the fastest ways to attract a mismatch notice from the Income Tax Department.

Real Example: Rohit’s Hyderabad Flat

Rohit, 38, is a salaried IT manager in Bengaluru earning ₹28 lakh per year. He owns a flat in Hyderabad that he has let out at ₹35,000 per month — a total of ₹4,20,000 for FY 2024-25. He paid ₹18,000 in municipal taxes for the flat during the year. He also has a home loan on this property, and the interest paid during the year was ₹1,20,000.

Rohit’s Gross Annual Value is ₹4,20,000 (actual rent received). After deducting ₹18,000 in municipal taxes paid by him, the Net Annual Value is ₹4,02,000. The 30% standard deduction under Section 24(a) works out to ₹1,20,600. His Section 24(b) home loan interest deduction is ₹1,20,000. This leaves him with a taxable house property income of just ₹1,61,400 — not ₹4,20,000. That final amount gets added to his salary income and taxed at his applicable slab rate. Since Rohit is in the 30% bracket, the actual tax on his rental income works out to approximately ₹48,420.

How to Calculate Rental Income Tax

Taxable House Property Income = GAV − Municipal Taxes − 30% of NAV − Home Loan Interest (Section 24b)

Step-by-step using Rohit’s figures:

- Gross Annual Value (actual rent received): ₹4,20,000

- Less: Municipal taxes paid by owner: ₹18,000

- Net Annual Value (NAV): ₹4,02,000

- Less: Standard deduction 30% of NAV (Section 24a): ₹1,20,600

- Less: Home loan interest (Section 24b): ₹1,20,000

- Taxable House Property Income: ₹1,61,400

| Scenario | Key Inputs | Taxable Amount |

|---|---|---|

| No home loan | Rent ₹4,20,000, Municipal tax ₹18,000, No loan interest | ₹2,81,400 |

| With home loan interest ₹1,20,000 | Rent ₹4,20,000, Municipal tax ₹18,000, Interest ₹1,20,000 | ₹1,61,400 |

| Higher loan interest ₹2,50,000 | Rent ₹4,20,000, Municipal tax ₹18,000, Interest ₹2,50,000 | ₹31,400 (loss may arise) |

Use our income tax calculator to estimate your total tax liability after adding house property income to your salary.

Comparison: Old Tax Regime vs New Tax Regime for Rental Income

| Parameter | Old Tax Regime | New Tax Regime |

|---|---|---|

| 30% standard deduction (Section 24a) | Allowed | Allowed |

| Municipal tax deduction | Allowed | Allowed |

| Home loan interest Section 24(b) — let-out | Allowed, no cap | Allowed, no cap |

| Set-off of house property loss against salary | Allowed up to ₹2L | Not allowed |

| Carry-forward of unabsorbed loss | 8 years | 8 years — HP loss only |

| Section 80C benefit on principal repayment | Allowed up to ₹1.5L | Not available |

| Best suited for | High loan interest, multiple deductions | Lower loan burden, simpler filing |

Read more about home loan tax benefit rules including Section 24(b) and 80C to understand how rental income interacts with your loan deductions.

How to Decide What’s Right for You

You have a home loan on your rented-out property with annual interest above ₹1.5 lakh — the old tax regime likely gives you a better outcome because you can set off up to ₹2 lakh of house property loss against salary income.

Your let-out property is fully paid off (no home loan) — the difference between regimes is smaller; compare your full tax liability before choosing, as new regime slabs may still save you more overall.

Your rental income is under ₹1 lakh per year after all deductions — and you have no other major deductions — the new tax regime’s lower slab rates may reduce your overall liability.

You receive monthly rent above ₹50,000 — confirm your tenant is deducting TDS at 10% and that it appears in your AIS. Missing TDS credit at filing causes delays and notices.

You own more than two properties — any additional property beyond two is treated as deemed let-out; notional rent is added to your income even if the flat is vacant. Verify the deemed rent figure before filing.

Your total tax payable for the year exceeds ₹10,000 — you are liable for advance tax in four instalments. Missing these attracts penal interest under Section 234B and 234C.

You do not pay municipal taxes personally (the tenant bears them under your rental agreement) — you cannot claim that deduction. Only expenses you actually pay qualify.

Common Mistakes to Avoid

Declaring Rent as “Income from Other Sources”

Many first-time landlords report rental income under “Income from Other Sources” instead of “Income from House Property.”

This forfeits all Section 24 deductions — the 30% standard deduction and home loan interest — potentially costing you thousands in excess tax. On ₹4,20,000 in rent, the 30% standard deduction alone saves ₹1,26,000 from your taxable base.

Always use the House Property schedule in ITR-1 or ITR-2.

Claiming Municipal Taxes You Didn’t Pay

The deduction for municipal taxes is available only on amounts actually paid by the owner during that financial year.

If your tenant pays the municipal tax under the agreement, or if you paid arrears of a previous year in the current year, the rules around admissibility differ. Overclaiming this deduction can trigger a scrutiny notice.

Claim only what you personally paid in that FY, with a receipt to support it.

Ignoring the Advance Tax Obligation

Salaried employees often assume their employer’s TDS covers all tax. When rental income pushes net tax liability over ₹10,000, advance tax applies.

Missing the 15 June, 15 September, 15 December, and 15 March deadlines attracts interest under Section 234B (1% per month on unpaid tax) and Section 234C (1% per month on shortfall per instalment). On ₹50,000 of extra tax, this can add ₹4,000–₹6,000 in interest over a year.

Add rental income to your salary, estimate total tax, subtract employer TDS, and check if the balance exceeds ₹10,000. If it does, pay advance tax.

Not Cross-Checking AIS and Form 26AS Before Filing

If your tenant deducted TDS, it will appear in your AIS. If you report a different rent figure in your ITR, the mismatch triggers an automated notice.

Always check your AIS and Form 26AS before finalising your rental income declaration. Our guide on AIS and Form 26AS explains exactly how to read and reconcile both.

Skipping the Deemed Let-Out Calculation

If you own three or more properties, the ones beyond two are automatically deemed to be let out — even if they are vacant and earning nothing.

The Income Tax Department calculates a notional rent for these properties and adds it to your income. Many taxpayers discover this only after receiving a notice. Identify all your properties, classify them correctly, and compute deemed rent before filing.

Claiming Section 24(b) Interest Without a Home Loan Statement

Section 24(b) deduction requires an interest certificate from your lender, showing the split between principal and interest for the year.

Without this, the claim is unsupported. If the assessment officer asks for it during scrutiny and you cannot produce it, the deduction is disallowed — and you face tax plus interest on the shortfall.

Download your loan statement by 31 March each year and file it away before you start your ITR.

Using ITR-1 When You Have Two or More Rental Properties

ITR-1 is valid only for salaried individuals with income from one house property. If you own two or more let-out properties, you must file ITR-2.

Filing ITR-1 when ITR-2 is required is technically a defective return and can be rejected by the department, requiring refiling within the notified deadline.

Check how many properties you own, how many are let out, and confirm the correct form before starting your return.

When This May Not Be the Right Choice

Renting out a property is not always the optimal financial move from a tax perspective. Consider these situations carefully before deciding.

If your property carries a large home loan and you opt for the new tax regime, the interest deduction cannot reduce your salary income. You pay tax on a higher salary base while the rental income after deductions adds to it — your net tax bill may be higher than expected.

If you own multiple properties and the deemed let-out rental values are high relative to your actual income, the notional income addition could push you into a higher tax slab, increasing tax on your salary as well.

If you are a senior citizen on a fixed pension with one rental property, the rental income calculation is the same — but any loss from house property cannot be set off against pension income classified under “salaries” once you opt for the new regime.

If you plan to sell the property soon, the rental income and capital gains interaction — especially indexed cost of acquisition — deserves a separate review before filing.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Rental income tax rules in India are governed by the Income Tax Act, 1961 — specifically Sections 22 to 27 (House Property) and Section 24 (Deductions). Filing obligations and ITR form requirements are notified by the Central Board of Direct Taxes each year.

Verify current rules and limits from these official sources:

- Income Tax Department — incometax.gov.in (House Property income guidelines, ITR utilities, AIS portal)

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Before filing, use the ITR filing checklist to make sure you have all documents ready — including your rent receipts, municipal tax receipts, and home loan interest certificate.

Expert Tips

- Download your home loan interest certificate from your lender’s portal before 1 April each year. The interest-principal split is needed for both Section 24(b) and Section 80C — waiting until July leads to rushed filings and errors.

- If your tenant pays you more than ₹50,000 per month, send them a reminder in March to ensure TDS is deposited before year-end. Undeposited TDS does not appear in your AIS, and you cannot claim credit for it at filing.

- Keep a running spreadsheet of rent received, municipal tax paid, and repair expenses. Even though repairs are covered under the flat 30% deduction, having records helps if your return is picked up for scrutiny.

- Pay your advance tax on rental income before 15 March each year. If your employer’s TDS covers your salary tax but rental income adds ₹15,000+ to the liability, the ₹10,000 threshold is crossed — and interest under Section 234C starts from June. See our guide on advance tax rules for exact instalment calculations.

- If you own a second property and it is vacant, check whether it qualifies as your second self-occupied property. Under current rules, up to two properties can be self-occupied with zero annual value — but you must declare this explicitly in your ITR, not leave it blank.

- If you are considering selling the flat after renting it out, note that rental income received over the years does not affect the cost of acquisition for capital gains purposes — the two calculations are separate.

- Use the old tax regime calculator to compare your total liability before switching. The regime choice is made at filing, but the math needs to be done before March 31 if your employer needs guidance on TDS deductions for the year.

Frequently Asked Questions

Is rental income added to my salary and taxed at the same rate?

Yes. Income from House Property is added to your total income after deductions and taxed at your applicable slab rate. If you are in the 30% bracket, your taxable house property income is also taxed at 30% plus surcharge and cess.

Can I claim the 30% standard deduction if I have no home loan?

Yes. The 30% standard deduction under Section 24(a) is automatic and applies regardless of whether you have a home loan. It is calculated on the Net Annual Value and is meant to cover all maintenance, repairs, and management costs without requiring you to submit any bills.

What is the difference between a let-out and deemed let-out property for tax purposes?

A let-out property is one you have actually rented out. A deemed let-out property is one the Income Tax Act treats as rented even if it is vacant — because you own more than two properties and it is not your primary residence. The tax calculation is similar for both, except deemed rent uses the fair market rental value rather than actual rent received.

Is there a limit on Section 24(b) interest deduction for a rented property?

Under the old tax regime, there is no upper cap on Section 24(b) home loan interest deduction for a let-out property. If your interest paid is ₹5 lakh, you can claim ₹5 lakh. Under the new tax regime, the deduction is still allowed with no cap, but if the resulting house property loss cannot be set off against other income — it can only be carried forward for eight years against future house property income.

What happens if my rental income after deductions turns into a loss?

If Section 24(b) interest exceeds your NAV after the standard deduction, your house property income becomes negative — a loss. Under the old tax regime, you can set off up to ₹2 lakh of this loss against your salary income in the same year. The remainder is carried forward for eight years. Under the new tax regime, no current-year set-off against salary is permitted.

Can I claim both Section 24(b) and Section 80C for the same home loan?

Yes, but they cover different parts. Section 24(b) applies to interest paid on the loan. Section 80C applies to principal repayment — up to ₹1.5 lakh. Both can be claimed simultaneously under the old tax regime. Under the new regime, Section 80C is not available.

Is TDS on rent compulsory for all tenants?

TDS applies when an individual or HUF tenant pays rent exceeding ₹50,000 per month. In such cases, the tenant must deduct TDS at 10% under Section 194-IB and deposit it with the government. For rents below this threshold, no TDS obligation falls on the tenant — though the landlord must still declare the rental income.

Which ITR form should I file if I have one rental property and one salary?

ITR-1 (Sahaj) is valid for salaried individuals with income from one house property, provided total income does not exceed ₹50 lakh. If you have two or more house properties, or if your income exceeds ₹50 lakh, use ITR-2.

What documents do I need to support my rental income declaration?

Keep rent receipts or bank transfer records showing rent received, the municipal tax payment receipt for the year, your home loan interest certificate from the bank, and the rental agreement. These are not uploaded during filing but must be available if your return is selected for scrutiny.

What is the assessment year for FY 2024-25 rental income?

Rental income earned in Financial Year 2024-25 (April 2024 to March 2025) is reported in Assessment Year 2025-26. Always mention the correct assessment year in your ITR to avoid processing errors.

Final Verdict

Rental income tax in India is manageable once you understand the three-step formula: start with Gross Annual Value, subtract municipal taxes and the 30% standard deduction, then subtract eligible home loan interest. For most salaried landlords, the actual taxable rental income is significantly lower than the rent they collect. The critical decision is choosing the right tax regime — the old regime wins when you carry a large home loan and can set off the resulting loss against salary; the new regime may suit smaller or loan-free rental income. Either way, check your AIS before filing, pay advance tax if liability exceeds ₹10,000, and use the right ITR form. For a full view of your combined tax liability, try the income tax calculator with your salary and rental figures together. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Neha Kulkarni writes about the financial side of home buying, renting, property decisions, and real estate costs in India. Her content helps readers think beyond the EMI and understand the total cost of owning or buying a home.

She covers topics such as rent vs buy, home loan planning, down payment, stamp duty, registration charges, brokerage, maintenance cost, property tax, furnishing cost, home insurance, builder payment plans, resale property checks, home loan affordability, total cost of ownership, and hidden costs in property decisions.

Neha’s writing is practical, family-focused, and cost-conscious. She uses Indian city examples, ₹ calculations, and decision checklists to help readers evaluate whether a property decision fits their income, savings, loan eligibility, and long-term plans. Her articles are useful for first-time home buyers, salaried couples, families, and people comparing rent with home ownership. Since property rules, stamp duty, registration charges, local taxes, home loan rates, and legal requirements vary by state and city, readers should verify current details from official state, lender, and legal sources.