Your employer deducts TDS from your salary every month — that part is handled. But what about the ₹60,000 in FD interest, the ₹80,000 you earned consulting on the side, or the capital gains from selling mutual funds this year?

Understanding advance tax meaning matters precisely here. This is the Income Tax Department’s rule that requires you to pre-pay a portion of your estimated annual income tax during the financial year — not in one lump sum when you file your ITR in July. If you miss it when you should have paid, interest starts adding up from 1 April of the assessment year.

This guide explains who needs to pay advance tax in India, how to estimate the amount, when the instalments fall due, and what happens if you pay late. All figures used are illustrative. Tax slabs, thresholds, due dates, and penalty rates can change with each Budget — verify current rules at incometax.gov.in before making any payment.

Quick Answer: Advance Tax Meaning

Advance tax meaning refers to paying income tax during the financial year instead of waiting until ITR filing. In India, taxpayers generally need to pay it when estimated tax liability after TDS is ₹10,000 or more. It is usually paid in instalments using the Income Tax Department e-Pay Tax portal.

Key Takeaways

- Advance tax applies when your estimated tax payable after TDS and TCS crosses ₹10,000 in a financial year — even if your salary TDS covers your primary income.

- Salaried employees who also earn FD interest, rent, capital gains, or freelance fees often need to estimate and pay advance tax themselves.

- Freelancers and self-employed professionals generally have no employer deducting TDS, so the full advance tax calculation falls on them each quarter.

- Missing an instalment or paying too little can trigger interest under Sections 234B and 234C — charged at 1% per month on the shortfall.

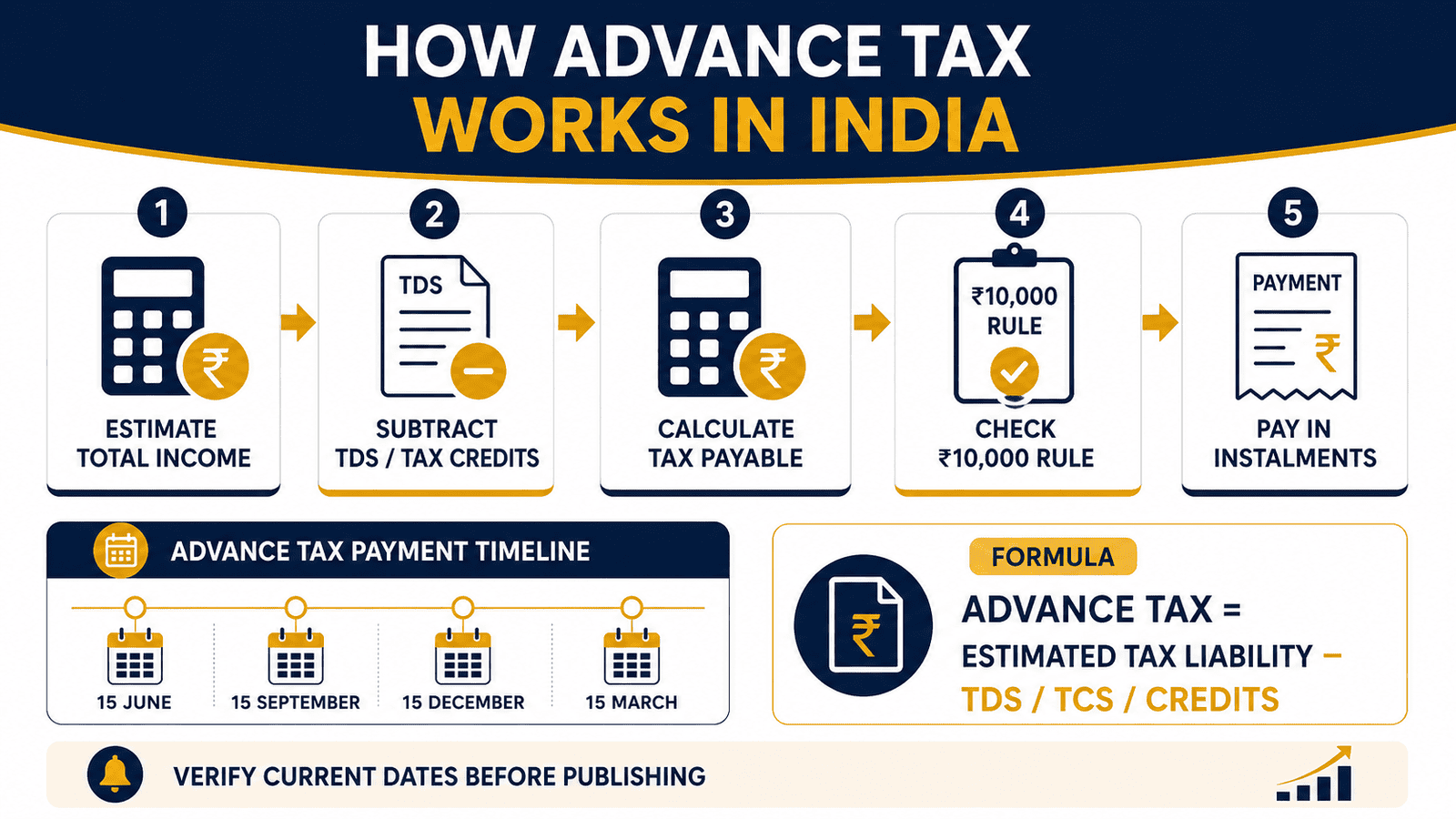

- Standard instalment schedule: 15% by 15 June, 45% by 15 September, 75% by 15 December, 100% by 15 March — verify current dates and percentages before each payment.

- Resident senior citizens without income from business or profession are generally exempt from paying advance tax under Section 207 of the Income Tax Act.

- Always verify current thresholds, due dates, and interest rates directly on incometax.gov.in — not a third-party summary — before calculating or paying.

Key Facts at a Glance

| Item | Detail | Verify Before Paying |

|---|---|---|

| What it is | Pre-payment of estimated annual income tax during the financial year itself | — |

| Governing section | Section 208 of the Income Tax Act, 1961 | incometaxindia.gov.in |

| Threshold | Estimated tax after TDS/TCS is ₹10,000 or more | Confirm current threshold |

| Instalment due dates | 15 Jun (15%), 15 Sep (45%), 15 Dec (75%), 15 Mar (100%) | Confirm current dates and percentages |

| Penalty interest | Sections 234B and 234C — 1% per month on shortfall | Confirm current interest rate |

| Senior citizen exemption | Resident senior citizens without business or profession income — Section 207 | Confirm current eligibility conditions |

| Payment portal | e-Pay Tax on incometax.gov.in — official portal only | Use official URL only |

What Advance Tax in India Actually Means

Most people think of income tax as something you calculate and pay when filing your ITR — usually in July or before the deadline. Advance tax flips that timeline. The government expects you to estimate your income for the full financial year, work out the likely tax, and pay it in instalments during the year itself.

This is not an extra tax. Your total liability does not increase because of advance tax. You are simply paying an estimated portion of what you would owe anyway — earlier. The benefit to the government is steady revenue through the year. The benefit to you is avoiding a large lump-sum payment at ITR time and, more importantly, avoiding interest penalties.

Section 208: the rule that makes it compulsory

Section 208 of the Income Tax Act, 1961 makes advance tax mandatory for any taxpayer — individual, HUF, firm, or company — whose estimated tax liability for the financial year is ₹10,000 or more after accounting for TDS and TCS already deducted or expected. If your gap is below ₹10,000, advance tax is technically not compulsory, though you may still pay early if you wish.

There is one significant exemption. Section 207 of the Act exempts resident senior citizens who do not have any income from business or profession from the advance tax requirement. They are still liable for the full tax — they simply pay it at the time of filing their ITR through self-assessment, without the quarterly instalment obligation.

Advance tax vs TDS vs self-assessment tax

These three terms trip up almost every first-time filer. Here is the plain distinction.

TDS (Tax Deducted at Source) is deducted by someone else before they pay you — your employer on salary, your bank on FD interest, your client on freelance fees. It shows up in your Form 16, Form 16A, and Annual Information Statement (AIS).

Advance tax is what you calculate and pay yourself, proactively, during the financial year — when your estimated total tax after all TDS and TCS will likely cross ₹10,000.

Self-assessment tax is the balance you pay at or before filing your ITR, after accounting for advance tax already paid, TDS, and TCS. If you missed advance tax entirely and owe a large balance, self-assessment tax covers it — but interest under Sections 234B and 234C may have already accumulated.

The starting point for any of these calculations is knowing your total taxable income — not just your salary figure. Calculate taxable income from all sources before estimating your tax liability.

Who needs to pay advance tax

In practice, advance tax applies to a wider set of people than most realise:

- Salaried employees who also earn FD interest, rental income, capital gains from equity or property, freelance consulting fees, or dividend income above the exempt threshold.

- Freelancers, independent consultants, and professionals where no single employer deducts TDS on the full income.

- Business owners under normal tax provisions — not presumptive taxation — where quarterly advance tax is mandatory above the threshold.

- Investors who realise significant short-term or long-term capital gains during the year from mutual funds, shares, property, or gold.

- Landlords whose tenants do not deduct TDS, or where TDS does not cover the full rental income tax obligation.

Why salary TDS alone may not be enough

Your employer calculates TDS on salary based on the income declaration you submit at the start of the year — your HRA claim, 80C investments, home loan interest, and similar items. That TDS is calibrated to cover salary income only. It does not automatically account for FD interest your bank is crediting, freelance earnings from a side project, capital gains from selling a mutual fund, or rent from a property you own.

If that extra income is large enough, the gap between total tax owed and TDS already deducted can easily cross ₹10,000 — triggering the advance tax requirement. This catches many salaried employees off guard, particularly those who receive a large bonus mid-year, sell assets between April and March, or take on consulting work on the side.

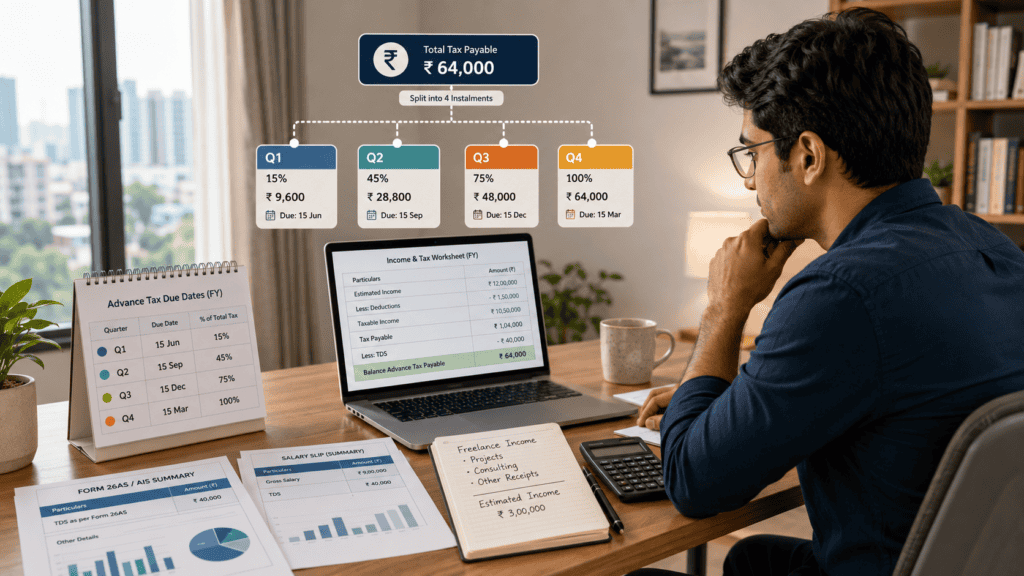

Real Example: Rohan’s Salary Plus Side Income

Rohan, 31, is a product manager in Bengaluru earning ₹18 lakh per year as salary. His employer deducts approximately ₹1,20,000 in TDS from his salary across the financial year, based on his annual declaration.

During the year, Rohan also earns ₹50,000 in FD interest and ₹80,000 from a short-term consulting project for a startup. Neither fully has TDS deducted at the rate applicable to his income bracket.

Rohan’s rough picture (illustrative only — verify current slabs, cess, standard deduction, and rebate rules before filing):

- Total gross income: ₹19,30,000 (salary + FD interest + consulting fees)

- Standard deduction (new regime): ₹75,000

- Estimated taxable income: ₹18,55,000

- Estimated tax at applicable slabs plus 4% cess: approximately ₹2,95,000 — illustrative only

- TDS already deducted by employer: ₹1,20,000

- Balance advance tax likely due: approximately ₹1,75,000

This ₹1,75,000 gap is well above the ₹10,000 threshold. Rohan should have checked his position before 15 June and paid in four instalments. Waiting until July ITR filing would have meant interest under Sections 234B and 234C ticking on the unpaid amount from April 1 of the assessment year. Salary TDS explained — see why the gap between TDS deducted and actual tax owed opens so easily.

How to Calculate Advance Tax

The core formula is straightforward:

Advance Tax Payable = Estimated Annual Tax (including cess and surcharge, if applicable) − TDS Deducted or Expected − TCS Credited

Work through five steps before each instalment date:

- Estimate total income for the full financial year — salary, FD interest, rent received, capital gains already realised, freelance income, business profits. Include income you expect to earn for the remainder of the year, not just what you have received so far.

- Choose your tax regime (old or new) and apply the deductions or exemptions applicable to your situation. Under the new regime, standard deduction applies. Under the old regime, 80C, 80D, HRA, home loan interest deductions, and others are available.

- Calculate estimated tax at the applicable slabs for the financial year, then add 4% health and education cess. Add surcharge if your income crosses the applicable bracket. Verify current slabs and cess rates before calculating.

- Subtract TDS and TCS already deducted or expected to be deducted before 31 March of the financial year.

- Check the balance. If it is ₹10,000 or more, divide it across the four instalment dates using the applicable percentages and pay through the e-Pay Tax portal at incometax.gov.in.

| Scenario | Estimated Tax After TDS | Advance Tax Required? |

|---|---|---|

| Only salary, TDS covers full liability | Under ₹10,000 | Not required |

| Salary + FD interest + consulting (Rohan) | ~₹1,75,000 (illustrative) | Required |

| Freelancer with no employer TDS | Full estimated annual tax liability | Required |

For a step-by-step estimate using current tax slabs before paying, use a verified and updated tool: Tax calculator guide.

Advance Tax Applicability by Taxpayer Type

| Taxpayer Type | Why Advance Tax May Apply | Most Common Mistake |

|---|---|---|

| Salaried — salary income only | Usually covered by employer TDS; advance tax may not apply if gap is under ₹10,000 | Assuming TDS always equals total tax without checking actual liability after declarations |

| Salaried with extra income | FD interest, rent, capital gains, or consulting fees push total tax above TDS deducted from salary | Not estimating extra income until March and discovering a large interest bill at ITR time |

| Freelancer or consultant | No employer TDS; clients may deduct 10% TDS but that often does not cover full tax at higher incomes | Under-estimating income at the June instalment and then missing the September and December dates |

| Business owner (non-presumptive) | Business profits are taxable; quarterly advance tax is mandatory above the threshold | Using last year’s profit as estimate without adjusting for actual year-to-date growth |

| Investor with capital gains | Short-term or long-term gains from equity, mutual funds, property, or gold can add significant tax mid-year | Realising a large gain in February and not factoring it into the December or March instalment |

Freelancers face the most complex advance tax situation of any taxpayer type — irregular income, multiple clients, variable TDS, and no single employer managing the annual picture. For a dedicated walkthrough: Freelancer tax payment — advance tax calculation and payment steps for independent professionals.

How to Decide What’s Right for You

Your only income is salary and your employer’s TDS matches your full tax liability for the year — you likely do not need to pay advance tax separately. Verify this mid-year using Form 26AS or AIS rather than assuming.

You earn FD interest, rental income, or any amount where no TDS is deducted at source — estimate this income by May each year and check whether the total tax gap, after all expected TDS, crosses ₹10,000.

You sold equity mutual funds, shares, or property this year — calculate the capital gains tax separately and add it to your advance tax estimate before the next instalment date. Capital gains surprises are among the most common causes of large interest bills.

You are a freelancer or consultant with no employer TDS — treat advance tax as a mandatory quarterly task, not something to figure out in March. Your entire estimated annual tax is your advance tax base, reduced only by whatever TDS clients actually deduct.

You switched jobs mid-year — your new employer may not know how much TDS your previous employer already deducted. Manually check Form 26AS to avoid a shortfall or accidental double-payment before the next instalment date.

You are a resident senior citizen without any income from business or profession — advance tax does not apply to you under Section 207. You settle your tax through self-assessment or at ITR filing, without the quarterly instalment obligation.

The tax regime you choose — old or new — directly changes your estimated tax and therefore your advance tax liability. Before finalising your estimate: Old versus new regime — which is better for salaried employees.

Common Mistakes to Avoid

Assuming salary TDS covers all income

Employer TDS is calculated only on salary-related income and the deductions you declared at the start of the year.

FD interest, freelance fees, capital gains, and rental income are not automatically covered. If these sources add up to ₹3–4 lakh of extra income, the additional tax could be ₹30,000–₹60,000 or more depending on your bracket — all of it subject to advance tax rules if not settled in time.

Check your total income picture from all sources before each instalment date, not just at the end of the year.

Ignoring bonus income until March

Annual performance bonuses are taxable in the financial year they are received. Many salaried employees get a large bonus in Q3 or Q4 and only realise in February that their TDS gap has widened.

A ₹2 lakh bonus can add ₹60,000 or more to your tax bill at a 30% slab. By December, two instalment dates have already passed.

Recalculate your advance tax estimate immediately after receiving a bonus and top up your payment before 15 March if needed.

Waiting until ITR filing to estimate your tax

All four advance tax instalment dates fall inside the financial year — 15 June, 15 September, 15 December, and 15 March. ITR filing typically happens in July, after the financial year has already ended.

Waiting until July means you have missed all four dates. Interest under Sections 234B and 234C starts from 1 April of the assessment year on the unpaid amount. On a ₹2 lakh shortfall, that adds roughly ₹2,000 per month in interest — before any reconciliation.

Set a reminder in May, before the 15 June instalment, to estimate your annual tax for the year ahead.

Entering the wrong assessment year on the challan

Advance tax paid for FY 2025-26 must be mapped to Assessment Year 2026-27 on the challan.

Entering the wrong AY means the payment credit does not appear against the correct year in your ITR. Rectification requests can delay your return processing and refund, even if the money was paid on time.

Double-check the Assessment Year field before confirming any payment on the e-Pay Tax portal.

Not downloading and saving the challan receipt

The challan counterfoil contains your BSR code, challan serial number, and date of deposit — the three fields your ITR needs to credit the payment.

Mismatches between what you paid and what appears in Form 26AS can delay processing and require a rectification filing. Download the challan PDF immediately after completing each payment and save it in a dedicated folder.

Paying through unofficial or third-party portals

Advance tax must be paid through the official Income Tax e-Pay Tax portal at incometax.gov.in, or through an authorised bank branch using the physical challan.

Phishing websites copy the look of the official portal and capture your banking credentials. Bookmark the official URL directly and never pay through links received in SMS, WhatsApp, or email.

When This May Not Be the Right Choice

Advance tax is a legal obligation, not an optional strategy — but there are genuine situations where it may not apply to you at all.

Your estimated tax gap is under ₹10,000. If the balance tax after subtracting all TDS and TCS is below the current threshold, advance tax is not compulsory. You settle the small remaining balance at self-assessment time before or during ITR filing.

Your employer TDS fully covers your total tax liability. Some salaried employees in a straightforward salary-only situation, with all deductions correctly declared, find that TDS clears their entire bill. Verify this mid-year using Form 26AS — not at the end of March when it is too late to make changes.

You are a resident senior citizen without business or professional income. Section 207 of the Income Tax Act specifically exempts this group from the advance tax instalment requirement. You are still liable for the full tax — but pay it through self-assessment rather than quarterly instalments.

Your income situation is highly complex. Foreign income, large capital gains from property, business losses being carried forward, or unusual transactions make a DIY advance tax estimate risky. In these cases, a chartered accountant’s review before June is more reliable than a rough calculator estimate.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Advance tax rules — the threshold, instalment dates, percentage breakdown, interest rates, and exemption conditions — are governed by the Income Tax Act, 1961 and may be updated with each Union Budget or CBDT notification.

- Income Tax Department e-filing and payment portal: incometax.gov.in — e-Pay Tax, challan history, Annual Information Statement (AIS), Form 26AS

- Income Tax Department reference site: incometaxindia.gov.in — Act provisions, circulars, FAQs, and official interpretations

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Before estimating your advance tax gap, reconcile your existing TDS credits against what your employer has deducted. Read Form 16 — how to read your Form 16 and verify TDS before filing your ITR.

Expert Tips

- Set a May reminder every year — not a June one. The first instalment is due 15 June. Estimating in May gives you time to gather income data, choose your regime, run the numbers, and pay without rushing. Most people who miss the June date never bothered to estimate in May.

- Recalculate after every significant financial event. Sold shares in August? Received a ₹3 lakh consulting payment in October? Got a joining bonus from a new employer? Each of these changes your annual tax estimate. Recalculate before the next instalment date and top up if the gap has widened.

- Track TDS through your AIS, not just Form 16. Form 16 covers only salary TDS. Your Annual Information Statement (AIS) on the e-filing portal shows TDS from banks, clients, and all other sources. Use both to get the complete picture before estimating advance tax.

- Use a tax calculator for estimates — then verify against official slabs. Online calculators are useful for quick estimates but may not reflect the latest Budget changes. Always confirm slab rates, cess, and standard deduction figures at incometax.gov.in before making any payment.

- Maintain a simple quarterly income tracking sheet. A basic spreadsheet with salary, FD interest credited, consulting fees received, TDS deducted by each source, and advance tax paid — updated every quarter — takes 20 minutes and prevents a ₹30,000–₹40,000 interest surprise at ITR time.

- If you switch jobs mid-year, consolidate both Form 16s before the December instalment. Each employer deducts TDS as if salary from them is your only income. Adding both salaries together often creates a tax gap — or an excess — that only becomes visible when you consolidate. Check this by September.

Frequently Asked Questions

What is advance tax in simple words?

Advance tax is income tax you pay in instalments during the financial year itself — not in one payment when you file your ITR. The government requires this so that large tax amounts are collected progressively through the year, matching when income is actually earned rather than waiting until July filing season.

Who needs to pay advance tax in India?

Any taxpayer whose estimated income tax for the year, after subtracting TDS and TCS already deducted or expected, is ₹10,000 or more. This includes salaried employees with significant non-salary income, freelancers, business owners, and investors with large capital gains. Resident senior citizens without business or profession income are exempt under Section 207 — verify current exemption conditions at incometaxindia.gov.in.

Do salaried employees need to pay advance tax?

Not always. If your employer’s TDS fully covers your annual tax liability, you do not need to pay advance tax separately. But if you also earn FD interest, rental income, consulting fees, or capital gains that push your total tax gap above ₹10,000 after all TDS is accounted for, you do need to pay the difference in instalments across the year.

What are the advance tax instalment due dates?

The standard schedule is: 15% by 15 June, 45% by 15 September, 75% by 15 December, and 100% by 15 March. Taxpayers opting for presumptive taxation under Section 44AD or 44ADA typically pay 100% in a single instalment by 15 March. Verify current dates, percentages, and presumptive scheme eligibility on incometax.gov.in before each payment date.

How do freelancers calculate advance tax?

A freelancer estimates total billing expected for the full year, subtracts eligible deductions (50% of gross receipts under Section 44ADA for professionals, or actual verified expenses under normal provisions), calculates tax at applicable slab rates plus cess, subtracts any TDS already deducted by clients, and pays the remaining balance in four instalments. Because freelance income is irregular, it is important to update the estimate before each due date rather than relying on the June estimate for the entire year.

What happens if advance tax is not paid?

If advance tax paid is less than 90% of your assessed tax for the year, interest under Section 234B applies at 1% per month (simple interest) from 1 April of the assessment year until the date of actual payment. Section 234C applies separately for shortfalls at each individual instalment date, even if you eventually pay the full amount by 15 March. Both sections can apply simultaneously. Verify current interest rates and calculation method at incometaxindia.gov.in before estimating any penalty.

Can I pay advance tax in one instalment instead of four?

Under normal provisions, the instalment schedule is spread across four due dates. However, taxpayers covered by the presumptive taxation scheme under Section 44AD or 44ADA can pay their entire advance tax liability in a single instalment by 15 March. If you are not on presumptive taxation and pay everything in one shot in March, Section 234C interest may still apply for the earlier missed instalments — even though the total amount paid was correct.

How can I pay advance tax online?

Go to incometax.gov.in, open the e-Pay Tax section, log in with your PAN, select the advance tax challan (Challan 280, Type of Payment: Advance Tax), enter the correct Assessment Year, choose your payment mode (net banking, debit card, or NEFT/RTGS through your bank), complete the payment, and immediately download the challan receipt containing the BSR code, serial number, and payment date. Use only the official portal — never pay through links shared in SMS, email, or WhatsApp.

Is advance tax the same as self-assessment tax?

No. Advance tax is paid during the financial year in four instalments, before the year ends on 31 March. Self-assessment tax is the balance you pay after the year ends — before or at the time of filing your ITR — to settle whatever remains after advance tax paid, TDS, and TCS are all accounted for. Both use Challan 280 on the e-Pay Tax portal, but with different payment type codes. Getting this wrong creates mismatches in your ITR.

What is Section 208 of the Income Tax Act?

Section 208 is the provision that makes advance tax compulsory for any person whose estimated tax liability for the year is ₹10,000 or more. It is the legal basis for the entire advance tax system — without it, paying tax during the year would be optional. Consult incometaxindia.gov.in or a qualified tax professional for the precise current text and any amendments after recent Budgets.

Final Verdict

Advance tax meaning is simple once you see it for what it is: a timing rule, not an extra charge. Your total income tax obligation does not increase because of advance tax — you are simply paying estimated portions of it during the year instead of all at once when you file your ITR. But delay has a real cost: interest under Sections 234B and 234C runs at 1% per month and starts from 1 April of the assessment year.

If you are salaried with extra income — FD interest, consulting fees, rent, capital gains — check your tax gap before 15 June each year. If you are a freelancer or self-employed, advance tax is not optional: estimate conservatively, pay on time, and recalculate whenever your income picture shifts significantly. Use a reliable calculator as a starting point, then verify current slabs and thresholds at incometax.gov.in before paying.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.