You have a health insurance policy. Then a family member is hospitalised and suddenly you are scrambling — does the insurer pay the hospital directly, or must you pay first and claim later? Who do you call? What papers do you need? How long does it take?

The health insurance claim process catches most Indian families off guard — not because it is complicated, but because nobody explained it before the emergency happened. Having a policy is step one. Knowing how to activate it successfully is step two, and most people skip that entirely.

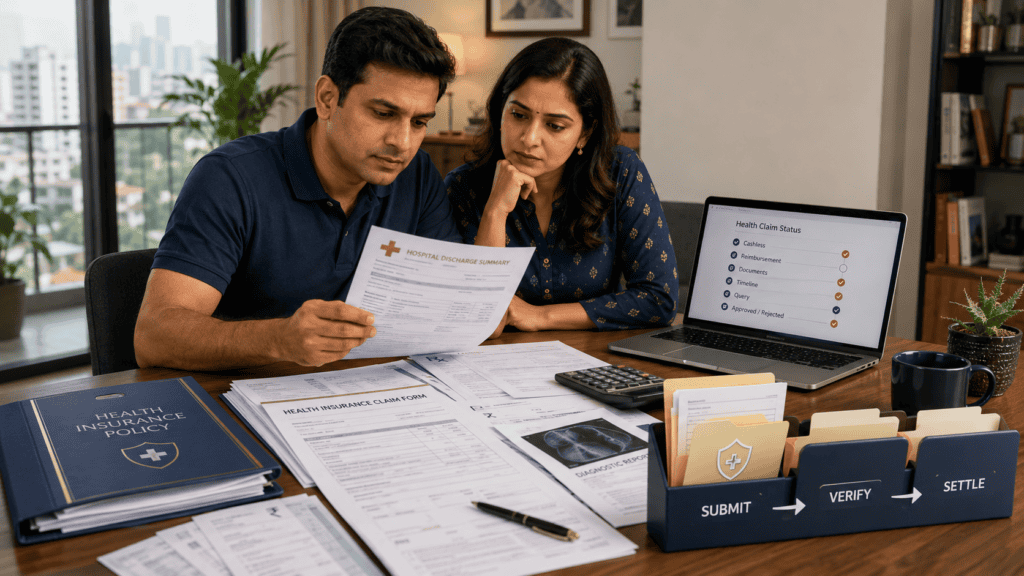

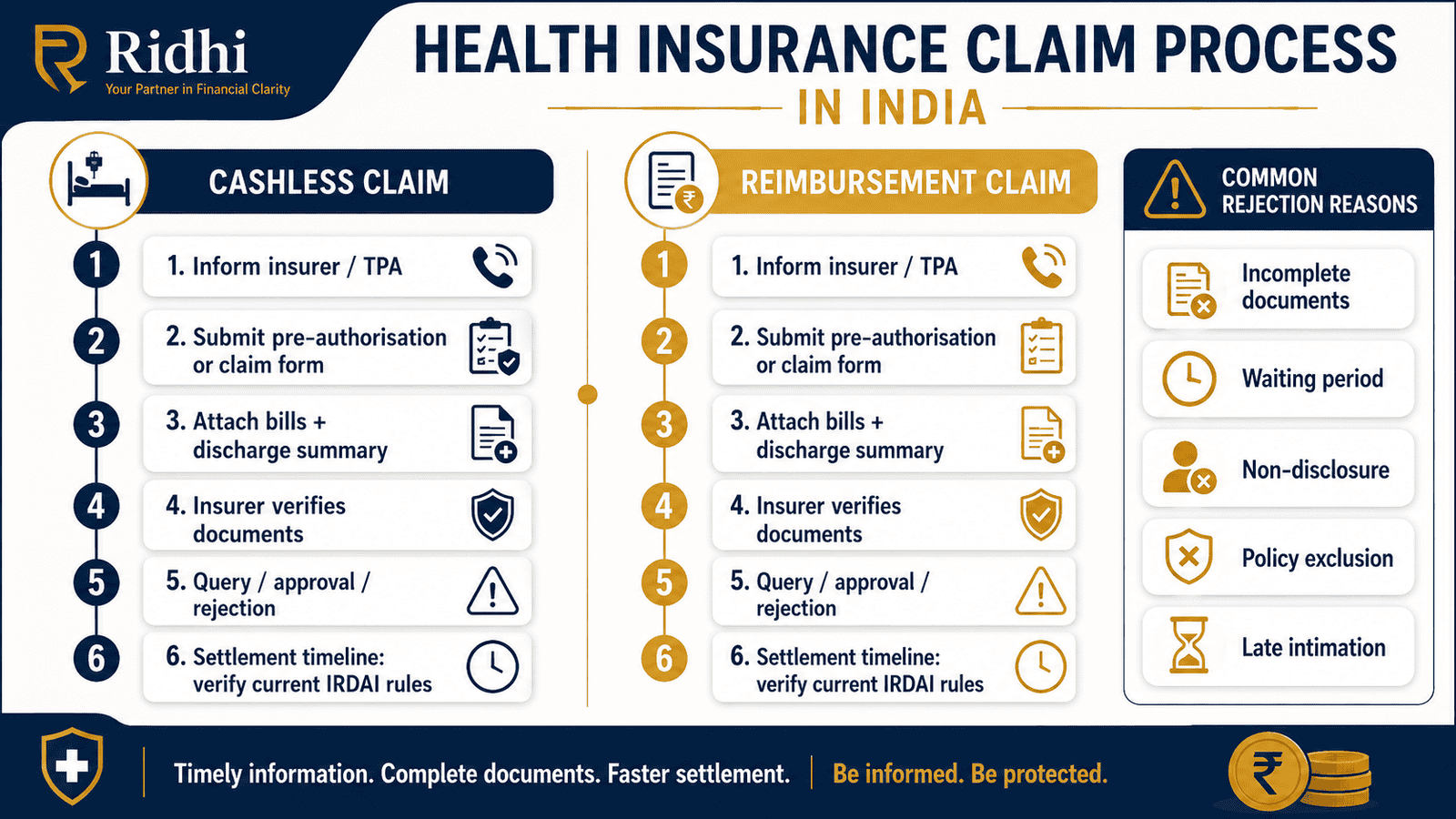

Claims in India follow two routes: cashless and reimbursement. Each has its own documents, timelines, and pitfalls. This guide walks you through both — what to do, when to do it, and how to avoid the mistakes that get claims delayed or rejected.

Quick Answer: Health Insurance Claim Process

The health insurance claim process is the step-by-step method of informing your insurer, submitting hospital documents, completing claim forms, answering queries, and receiving cashless approval or reimbursement. In India, families should keep at least 6 key documents ready, including bills, discharge summary, prescriptions, reports, claim form, and policy details.

Key Takeaways

- Cashless claims are processed through network hospitals where the insurer settles the bill directly — but you still need prior authorisation through the hospital insurance desk before or at the time of admission.

- Reimbursement claims require you to pay the full hospital bill first and then submit original bills, discharge summary, prescriptions, and diagnostic reports — one missing document can delay the entire settlement.

- Three of the most common claim rejection triggers are active waiting periods, policy exclusions, and non-disclosure of pre-existing diseases on the original proposal form.

- Claim timelines, intimation windows, and exact document requirements vary by insurer and policy — always confirm the full checklist with your insurer or TPA before discharge.

- Even an approved cashless claim may be partially settled due to room rent sub-limits, co-pay clauses, non-payable consumables, or benefit caps in your policy.

- If your insurer rejects or underpays a valid claim, you can escalate to the insurer’s grievance cell and, if still unresolved, through IRDAI’s official grievance redressal mechanism.

Key Facts at a Glance

| Parameter | Cashless Claim | Reimbursement Claim |

|---|---|---|

| Who pays the hospital | Insurer settles directly with the network hospital | Policyholder pays first; insurer reimburses later |

| Where it applies | Insurer or TPA empanelled network hospitals only | Any eligible hospital, including non-network |

| Key documents needed | Pre-auth form, policy card, doctor prescription, investigation reports | Original bills, discharge summary, prescriptions, reports, claim form, policy details |

| Common rejection reasons | Waiting period active, treatment excluded, incomplete pre-auth | Missing originals, late submission, non-disclosed pre-existing disease |

| Escalation path | Insurer grievance cell → IRDAI grievance mechanism | Insurer grievance cell → IRDAI grievance mechanism |

How the Health Insurance Claim Process Works in India

A health insurance claim is a formal request to your insurer — or to the Third Party Administrator (TPA) managing your policy — to release the cover promised in your policy document. It does not start automatically when you are admitted to hospital. You have to initiate it, document it, and follow up on it.

TPAs are licensed intermediaries who handle claims, maintain network hospital lists, and respond to policyholder queries on behalf of the insurer. Not every insurer uses a TPA — many have shifted to in-house claim processing. Your policy schedule will tell you which applies to your policy. Save those contact details before you need them.

The Cashless Claim Process: Step by Step

Cashless claims apply when your hospital is part of the insurer’s empanelled network. These hospitals have a dedicated insurance desk that coordinates directly with the insurer or TPA on your behalf.

For planned hospitalisation: Contact the insurer or TPA at least 48 to 72 hours before admission. The hospital insurance desk typically fills the pre-authorisation form for you. Attach the treating doctor’s recommendation, investigation reports, and your health card or policy number. The insurer reviews the request and either approves, partially approves, or raises an insurer query.

For emergency admission: Inform the insurer or TPA as soon as the patient is stabilised — the hospital insurance desk can initiate the pre-authorisation process. Even in an emergency, the sooner you notify, the fewer complications arise with approval timing.

Once approved, the insurer settles the eligible bill directly with the hospital. You pay only the balance — the co-pay portion if your policy has one, any room rent difference if you chose a category above your policy limit, and non-payable items listed in your policy.

Even when using cashless, collect all original documents before leaving the hospital at discharge: the discharge summary, itemised final hospital bill, lab and diagnostic reports, and prescriptions. You may need them if you appeal a partial rejection or if related treatment continues.

To understand what your policy is likely to cover before you reach the claim stage, start with our guide on health cover basics.

The Reimbursement Claim Process: Step by Step

Reimbursement applies when the treating hospital is not in the network, when cashless pre-authorisation is denied, or when you paid the bill upfront and need to recover the eligible amount.

- Intimate your insurer: Do this within the timeframe stated in your policy — typically within 24 hours of an emergency admission, and before or at the time of a planned admission. Late claim intimation is a cited reason for deduction or rejection.

- Collect every original document at discharge: Itemised hospital bill, discharge summary, all investigation and diagnostic reports, doctor prescriptions, pharmacy receipts, and completed claim form. Photocopies are generally not accepted in place of originals for the first submission.

- Submit the complete claim package within the deadline: Most policies require submission within 15 to 30 days of discharge — the exact window is in your policy document; verify with your insurer before submitting.

- Respond to insurer queries promptly: The insurer may ask for missing reports, diagnosis clarification, or additional forms. Delayed responses stall settlement directly.

- Settlement: After all documents are verified and queries are resolved, reimbursement is credited to your registered bank account.

Both routes have trade-offs worth understanding before hospitalisation. Our detailed guide on cashless or reimbursement hospitalisation covers the full comparison.

Why Cashless Claims Are Sometimes Partially Settled

An approved cashless claim does not mean the full hospital bill is covered. Partial settlements happen for specific reasons:

- Room rent sub-limits: If your policy caps room rent at ₹3,000 per day and you chose a ₹5,500 room, the insurer may apply a proportionate reduction to all associated charges — nursing, OT fees, doctor visits — not just the room difference.

- Non-payable items: Most standard policies exclude consumables such as gloves, surgical gauze, syringes, and bandages from the reimbursable amount.

- Co-pay clauses: If your policy has a 10% or 20% co-pay requirement, that percentage of every approved amount stays out of pocket.

- Disease-specific sub-limits or benefit caps: Some policies cap coverage for specific conditions regardless of actual expenses incurred.

Real Example: Ramesh Sharma’s Father’s Hospitalisation in Bengaluru

Ramesh Sharma, 38, senior sales manager in Bengaluru earning ₹18 lakh per year, holds a family floater policy with a ₹5 lakh sum insured. His 68-year-old father is admitted to a network hospital for a planned knee replacement surgery. The expected bill: ₹2.4 lakh.

Ramesh visits the hospital insurance desk the evening before admission. The desk submits the pre-authorisation form along with the surgeon’s recommendation and pre-op reports. The insurer approves ₹1.9 lakh — excluding ₹28,000 in non-payable consumables and applying a proportionate deduction because his father chose a room above the policy’s daily room rent limit.

On discharge day, Ramesh pays ₹50,000 — the gap between the total bill and the approved cashless amount. He collects the discharge summary, itemised bill, all diagnostic reports, and prescriptions. He scans and stores digital copies immediately as a backup.

If the hospital had been outside the insurer’s network, Ramesh would have paid the full ₹2.4 lakh upfront and filed a reimbursement claim — submitting every original document within the submission deadline in his policy.

Key insight: Check whether your preferred hospital is in the network and whether your room rent limit matches the standard ward category — before the admission date, not after.

Comparison: Cashless vs Reimbursement Health Insurance Claim

| Parameter | Cashless Claim | Reimbursement Claim |

|---|---|---|

| Who pays the hospital | Insurer settles directly with the network hospital | You pay the full bill; insurer reimburses you later |

| Where it applies | Insurer or TPA empanelled hospitals only | Any eligible hospital under your policy terms |

| Upfront cash needed | Minimal — only non-payables, co-pay, room excess | Full bill — recovered later after settlement |

| Planned hospitalisation | Preferred — submit pre-auth 48–72 hrs before | Available if cashless is not possible |

| Emergency hospitalisation | Available — initiate through hospital insurance desk on admission | Use if no network hospital nearby or cashless denied |

| Document risk | Lower — hospital desk coordinates with insurer | Higher — all originals required; one gap delays the claim |

| Best suited for | Planned surgeries at known network hospitals | Non-network hospitals, travel emergencies, cashless denial |

How to Decide What’s Right for You

Your hospital is in the insurer’s network and the treatment is not under an active waiting period or policy exclusion — request cashless authorisation through the hospital insurance desk before or at admission.

Your hospital is outside the network or cashless pre-authorisation is denied — proceed with reimbursement. Pay the bill, preserve every original document, and submit the complete claim package within the deadline specified in your policy.

You hold a family floater policy and a large claim has already been approved this year — check the remaining sum insured before scheduling any other procedure for a family member in the same policy year.

Your cashless claim is only partially approved — do not dispute at the hospital counter. Note the shortfall amount, pay the gap, collect all documents at discharge, and raise a formal query with the insurer after leaving the hospital.

You receive an insurer query after filing a reimbursement claim — respond within the window stated in the query letter. Unanswered queries are treated as incomplete submissions and will stall settlement indefinitely.

Do not assume health insurance will cover the entire hospital bill — if your policy has a co-pay clause, room rent sub-limit, or disease-specific cap, the insurer will not settle 100% of the amount even on a fully valid claim. Plan for the gap in advance.

If a previous claim on your family floater has significantly reduced available cover, this is a good time to review your coverage structure. Our guide on individual versus family floater health insurance explains when each option works better for families like yours.

Common Mistakes to Avoid

Not Intimating the Insurer Within the Required Window

Most policies specify an intimation deadline — typically within 24 hours of emergency admission and before or at planned admission.

Late claim intimation is one of the most common grounds for claim deduction or rejection. Even if the treatment is fully covered, missing the intimation window gives the insurer grounds to question the validity of the claim and may reduce the settled amount.

Save your insurer’s 24-hour helpline number and TPA contact in every family member’s phone well before any hospitalisation occurs.

Losing Original Bills and Reports

For reimbursement claims, original documents — not photocopies — are typically required: bills, discharge summary, diagnostic reports, and prescriptions.

Once originals are lost or misplaced, the hospital may not reissue them in the exact format required by the insurer. A valid claim can be denied entirely due to document gaps that could have been prevented.

At discharge, collect all originals before leaving the hospital floor. Scan and store digital copies immediately as a backup.

Filing a Claim During an Active Waiting Period

Health policies carry multiple waiting periods: an initial waiting period for all illnesses, a pre-existing disease waiting period, and condition-specific waiting periods.

Filing a claim for a condition under an active waiting period will result in rejection — regardless of how medically necessary the treatment was. Many families only discover this after the claim is already submitted and denied.

Check which waiting periods apply to the specific diagnosis before filing. For a full breakdown, read our guide on health insurance waiting period rules and their impact on claims.

Choosing a Room Above the Policy’s Room Rent Limit

If your policy caps room rent at ₹3,000 per day and you occupy a ₹6,000 room, the insurer does not just deduct the ₹3,000 daily difference.

Most policies apply a proportionate deduction across all associated charges — nursing, OT fees, doctor consultation, and procedures — in the same ratio. On a ₹3 lakh bill, this can cost you ₹45,000 to ₹70,000 out of pocket on top of the room difference.

Before admission, confirm your policy’s room rent limit and book the appropriate ward category at the treating hospital.

Ignoring Policy Exclusions and Non-Payable Items

Most standard health policies exclude consumables such as gloves, syringes, surgical gauze, and certain personal care items billed by the hospital.

If you assume the entire itemised hospital bill will be covered, the shortfall at discharge will come as an unwelcome surprise. Read the non-payable items schedule in your policy document before any planned hospitalisation.

Not Disclosing Pre-Existing Diseases on the Proposal Form

Non-disclosure of a pre-existing condition — even if accidental — is grounds for claim repudiation. If you did not declare a condition at proposal stage and it becomes relevant to a claim, the insurer can reject the claim and potentially cancel the policy entirely.

Always disclose accurately when buying or porting a health policy. A longer waiting period at purchase is far less damaging than a repudiation when you need the cover most.

Not Responding to Insurer Queries After Submission

After a reimbursement claim is submitted, the insurer or TPA will often raise queries — a missing investigation report, a clarification on the diagnosis, or an additional claim form.

Delays in responding are treated as an incomplete submission. The settlement clock effectively stops until every query is answered. Monitor your registered mobile and email for query notifications after every claim submission.

When This May Not Be the Right Choice

Health insurance covers a wide range of hospitalisation costs — but not every hospital bill will be covered in full, or at all. Here are situations where you should not expect complete coverage from your policy:

The treatment falls under a policy exclusion: Cosmetic procedures, dental treatment (unless from an accident), optical correction, and most alternative medicine treatments are excluded by standard health policies. If the admitted condition is listed as a policy exclusion in your document, the claim will not be approved regardless of medical necessity.

The condition has an active waiting period: Pre-existing diseases, maternity benefits, specific conditions, and certain procedures carry mandatory waiting periods. A claim filed during this period will be rejected. This does not mean your policy is invalid — it means that condition is not yet covered under your current policy term.

Your available sum insured is exhausted or sub-limits apply: If your remaining sum insured is ₹2 lakh and the hospital bill is ₹3.8 lakh, health insurance covers only up to the available limit. The remaining ₹1.8 lakh is entirely out of pocket — regardless of how comprehensive your policy otherwise is.

The treatment is not medically necessary under policy terms: Elective procedures, wellness check-ups, and preventive treatments are typically not covered unless your policy has a specific rider or add-on for them.

Even with a valid, active health policy, unexpected shortfalls during hospitalisation are common. Maintaining a dedicated cash buffer helps cover these gaps without financial stress. Our emergency fund calculator can help you work out how much to set aside: how much money should you keep in an emergency fund.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Health insurance claim rules, document requirements, timelines, and grievance procedures in India are governed by the Insurance Regulatory and Development Authority of India (IRDAI). These rules can and do change with regulatory circulars, budget updates, and policy amendments.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- IRDAI — irdai.gov.in: Policyholder rights, claim handling regulations, network hospital empanelment guidelines, and the official IRDAI grievance redressal process.

- Your insurer’s official website: Policy wordings, current network hospital list, claim forms, TPA contact details, and grievance cell contact.

- Your policy document and schedule: Exact waiting periods, room rent sub-limits, co-pay clauses, exclusions, intimation windows, and reimbursement submission deadlines.

- Insurer grievance cell: First escalation point for a disputed or rejected claim. Response timelines for grievances are regulated by IRDAI.

- IRDAI official grievance mechanism: If the insurer’s grievance cell does not resolve the complaint within the stipulated period, policyholders can approach the IRDAI’s official redressal process — details are available at irdai.gov.in.

Expert Tips

- Save claim contacts before you ever need them. Store your insurer’s 24-hour helpline, TPA contact number, policy number, and health card details in a shared family messaging group — not just on one person’s phone. In an emergency, whoever reaches the hospital first can call immediately.

- Verify network hospitals before booking planned treatment. Network hospital lists change at every policy renewal. Log in to your insurer’s portal or call the TPA to confirm your preferred hospital is still empanelled before scheduling an appointment or surgery.

- Build a physical and digital claim folder. Keep your policy document, health card, Aadhaar, PAN, past hospitalisation records, and specialist prescriptions in one dedicated folder — both physical and scanned digital copies. Hunting for documents during a hospitalisation is a source of error and delay that is entirely preventable.

- Read exclusions and waiting periods at every renewal. Most families read the policy brochure once at purchase and never look again. Review the exclusions page, sub-limits, and co-pay details at each renewal — these terms can change when you switch plans or add family members.

- Do not evaluate an insurer by claim settlement ratio alone. A high claim settlement ratio indicates that most claims are being paid — but it does not tell you the average payout amount or how disputed claims are handled. Use it as one signal alongside network strength, sub-limit structure, and policyholder feedback. Our guide on claim settlement ratio explains exactly how to read and apply this metric when choosing an insurer.

- Respond to insurer queries the same day they arrive. Every day you delay a query response is a day added to your settlement timeline. Set a calendar reminder the moment a query notification arrives on your registered mobile or email.

- Never discard claim documents after settlement. Retain all original bills, discharge summaries, and diagnostic reports for at least three years after every claim. You may need them for Section 80D deductions on your income tax return, for a related follow-up claim, or if a future insurer queries your medical history during underwriting.

Frequently Asked Questions

What documents are required for a health insurance claim?

The standard checklist includes the completed claim form, original hospital bills and receipts, itemised final bill, discharge summary, treating doctor’s prescription, diagnostic and investigation reports, pharmacy receipts, and your policy document or health card. For cashless claims, the hospital insurance desk submits most documents on your behalf. For reimbursement claims, the policyholder is responsible for assembling every original document and submitting within the deadline. The exact list may vary by insurer — confirm with your insurer or TPA at the time of intimation.

How long does health insurance claim settlement take?

IRDAI regulates claim settlement timelines for health insurers, but the specific mandated periods are subject to regulatory updates — always verify the current timelines at irdai.gov.in. In practice, cashless approvals are typically given before or during hospitalisation. Reimbursement claims are processed after complete document submission and are faster when no insurer queries are raised. Claims with missing documents or pending queries take longer until fully resolved.

What is the difference between a cashless and reimbursement health insurance claim?

In a cashless claim, the insurer settles the approved bill directly with the network hospital — you pay only the non-covered portion at discharge. In a reimbursement claim, you pay the full hospital bill upfront and file a claim to recover the eligible amount. Cashless is smoother for planned hospitalisation at a known network hospital. Reimbursement is used when the hospital is outside the network, cashless is unavailable, or the claim is made after you have already paid.

What should I do if my health insurance claim is rejected?

First, read the rejection letter carefully — the insurer is required to state the specific reason. If the rejection is due to a missing document, gather the required document and resubmit. If you believe the rejection is incorrect or unfair, file a formal written complaint with your insurer’s grievance cell and keep a copy. If the grievance cell does not resolve the issue within the IRDAI-regulated period, escalate through the IRDAI’s official grievance redressal mechanism. Maintain all correspondence and claim reference numbers throughout.

Can a health insurance claim be partly approved?

Yes, partial approvals are common and are not the same as a rejection. An insurer may approve the eligible components of a bill and exclude non-payable consumables, room rent excess, co-pay portions, or charges outside your policy’s benefit cap. When a cashless claim is partially approved, the shortfall is payable by you at discharge. For reimbursement, only the eligible portion is credited. If you believe items were incorrectly excluded, you can raise a query with the insurer after settlement.

Are non-medical items like attendant charges and food covered by health insurance?

Generally, no. Most standard health policies do not cover attendant charges, food, beverages, or comfort items billed during hospitalisation. These are typically listed under the non-payable items schedule in your policy document. If you believe a specific charge should be covered, cross-check it against your policy before expecting reimbursement — do not assume coverage based on the hospital including it in the bill.

Is original document submission required for reimbursement claims?

Yes, for most insurers. Original bills, discharge summary, and diagnostic reports are standard requirements — not photocopies — for the primary submission. Some insurers may accept certified copies for follow-up or supplementary submissions, but originals are expected at first filing. Confirm the exact document format required with your insurer at claim intimation, not after discharge.

What is a TPA and how does it affect my health insurance claim?

A Third Party Administrator (TPA) is a licensed intermediary authorised by IRDAI to manage health insurance claims on behalf of insurers. If your insurer works through a TPA, the TPA issues your health card, maintains the network hospital list, handles cashless pre-authorisation requests, and manages claim queries. Your TPA’s name and contact details appear on your health card and policy schedule — contact the TPA directly for all claim-related matters when a TPA is involved.

Can I claim for a daycare procedure that did not require an overnight stay?

Most standard health policies require a minimum 24-hour hospitalisation for a claim. However, IRDAI has specified a list of daycare procedures — treatments that no longer require overnight admission due to medical advances — that are covered even without a 24-hour stay. Whether your specific procedure qualifies depends on your insurer’s approved daycare list. Check this list with your insurer before the procedure, not after.

Is it mandatory to inform the insurer before planned hospitalisation?

Yes, for cashless claims it is always required — pre-authorisation cannot happen without prior notification. For reimbursement claims under planned admissions, most policies also require pre-admission intimation within a specified window. The exact requirement is in your policy document. Filing without prior intimation for a planned admission may give the insurer grounds to reduce or reject the claim even if the treatment itself is fully covered.

Final Verdict

The best experience with the health insurance claim process is the one you prepare for before hospitalisation — not the one you piece together in the middle of an emergency. Check network hospitals before booking treatment. Know your room rent limits, waiting periods, and policy exclusions before you walk into a hospital. Collect original documents at discharge, not after.

For most families, cashless is the smoother route — but only if the hospital is empanelled and the treatment is covered. If cashless is denied or unavailable, a well-documented reimbursement claim filed promptly and followed up quickly will get settled.

If a claim is unfairly rejected, escalate — politely and in writing. IRDAI’s grievance redressal mechanism exists specifically to protect policyholder rights, and insurers are regulated on how they handle disputes.

Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing. Premiums and coverage terms vary by age, health condition, insurer, and policy type.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.