Rohit paid his family floater premium last October and assumed his entire family was covered from that day. Four months later, his father was admitted for a complication linked to his declared diabetes — and the insurer rejected the claim. No fraud. No error. Just a pre-existing disease waiting period that nobody had read when the policy was purchased.

Health insurance waiting periods are one of the most consequential clauses a first-time buyer overlooks. Paying premium does not make every claim payable from day one. Depending on the illness, condition, or planned treatment, your health insurance waiting period can delay a valid claim by weeks, months, or years — and the exact terms vary by insurer and policy.

This article explains every type of waiting period, how each one affects your claim, and what you must check before buying, porting, or filing under a health policy.

Quick Answer: Health Insurance Waiting Period

A health insurance waiting period is the time after policy purchase during which certain claims are not payable, except usually accidents. It can apply to initial claims, pre-existing diseases, specific illnesses or maternity. Always check the policy wording because periods may range from 30 days to several years.

Key Takeaways

- Most health insurance policies have an initial waiting period from policy inception — emergency accident hospitalisation is commonly the only exception, but this must be confirmed in your specific policy wording.

- PED waiting periods apply specifically to declared pre-existing diseases such as diabetes, hypertension, or prior surgeries. The period varies by insurer — always compare it before buying, not after a claim arises.

- If your policy includes maternity benefit, a separate maternity waiting period applies from policy start. If maternity is planned in the next one to two years, check this period before purchasing — not when you need to claim.

- Portability from one insurer to another may carry forward completed waiting-period credit under IRDAI rules, but credit applies only to waiting periods already served and is subject to insurer-specific conditions.

- Non-disclosure of a pre-existing disease at the proposal stage is the single most dangerous mistake a buyer can make — it can lead to claim rejection even after the waiting period has fully ended.

- A policy with a lower annual premium but a longer PED waiting period can leave your family with no claim reimbursement for declared conditions for years — even while premiums are being paid on time.

- Permanent exclusions are not waiting periods. They are conditions that a policy will never cover, regardless of how long it is held. Read both sections separately in the policy wording.

Key Facts at a Glance

| Waiting Period Type | Applies To | Key Claim Impact |

|---|---|---|

| Initial waiting period | All illness-related claims at policy start | Illness claims usually not payable during this window |

| PED waiting period | Declared pre-existing diseases | Claims for listed PEDs deferred until period ends |

| Specific disease waiting period | Named conditions — hernia, cataract, joint replacement | Treatment for listed conditions deferred until period ends |

| Maternity waiting period | Maternity and newborn cover, if included in plan | Maternity-related claims not payable before period ends |

| Permanent exclusion | Conditions excluded in policy wording | Never payable under that policy, regardless of policy age |

| Accident hospitalisation | Emergency hospitalisation due to accident | Commonly payable from policy start — confirm in policy wording |

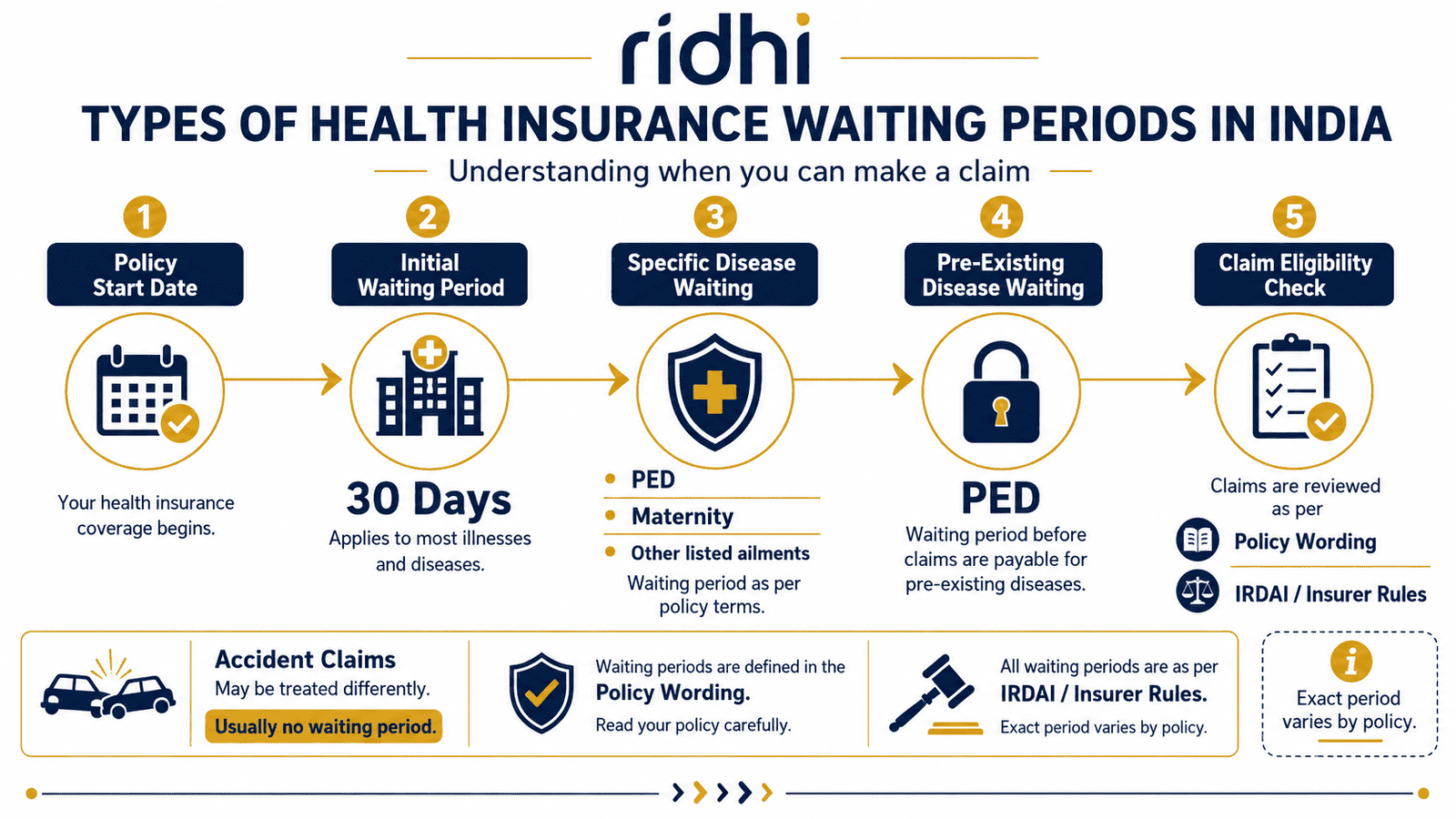

How Health Insurance Waiting Periods Actually Work

When you purchase a health insurance policy, the insurer sets a policy inception date — usually the date of issuance or the date your first premium is received. But the claim eligibility date is not always the same as the policy start date. A waiting period is the gap between the two.

During a waiting period, your policy is technically active. Your premium is paid. Your policy number exists. Your insurer is valid. But claims for specific conditions or illness types are not admissible. The policy schedule and policy wording define exactly which waiting periods apply, how long each lasts, and what falls outside them.

Why Insurers Apply Waiting Periods

Health insurance is not a reimbursement scheme for known upcoming medical costs. It is risk protection for uncertain future events. Waiting periods exist to prevent a buyer from purchasing a policy specifically because a hospitalisation is already scheduled — a surgery already planned, a delivery already in progress, or a condition already diagnosed and needing treatment this month.

Without waiting periods, the insurance pool would be used as advance payment rather than shared risk cover. Waiting periods keep premiums manageable for healthy policyholders and ensure the product functions as insurance rather than a health savings withdrawal.

Temporary Waiting Periods vs Permanent Exclusions

Many buyers confuse these two — and it is an expensive confusion. A waiting period is temporary. Once it ends, the previously restricted condition becomes claimable under the policy with no additional approval or declaration required.

A permanent exclusion is different. It is a condition or treatment that the policy will never cover, regardless of how many years you hold it or how many renewals you complete. Common examples in Indian health policies include congenital conditions, self-inflicted injuries, cosmetic procedures, and dental treatment in most standard plans.

These appear in two different sections of the policy wording. Read both. Assuming that waiting for the waiting period to end will eventually unlock a permanently excluded condition is a common and costly misunderstanding.

Where to Find Waiting Periods in Your Policy Documents

Waiting periods appear in three places. The policy schedule is the document with your name, sum insured, and buyer-specific terms — it may list your specific PED waiting period duration. The policy wording is the controlling contract — it defines every term, condition, and exclusion that governs your cover. The customer information sheet (CIS) is a standardised summary that IRDAI requires insurers to provide, highlighting key waiting periods and exclusions in plain language.

Of these, the policy wording governs. If the brochure or sales summary implies faster coverage than the policy wording actually grants — the policy wording controls. Many claim disputes arise precisely because buyers read the brochure but not the policy wording. To understand the full picture of what health insurance covers and what it does not, the policy wording is the only reliable document.

Why Waiting Periods Deserve as Much Attention as Premium

When comparing two health insurance plans, most buyers focus on annual premium, sum insured, and network hospital list. Waiting periods are equally important — and for families with any medical history, they can matter more than premium.

A plan with a PED waiting period of 1 year may carry a higher annual premium than a plan with a 3-year PED waiting period. For a 28-year-old with no declared conditions, the difference may be immaterial. For a family where a parent has hypertension or a member has prior surgery history, the 1-year plan can deliver meaningful claim access years earlier — making the higher premium worth far more than the difference paid.

According to IRDAI guidelines, health insurers are required to clearly disclose all waiting periods in the policy wording and in the customer information sheet. If any waiting period is unclear or absent from the written policy document — raise it in writing with the insurer before purchasing.

Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing.

Real Example: Rohit’s Family Floater and Four Different Claims

Rohit, 34, is a senior software engineer in Pune earning ₹24 lakh per year. He buys a ₹10 lakh family floater health insurance policy covering himself, his wife Priya, and his parents. His father has Type 2 diabetes — declared honestly at the proposal stage. Priya and Rohit plan to start a family within two years, and the policy includes maternity benefit.

Rohit’s accident: Two weeks after the policy starts, Rohit fractures his wrist in a road accident. The claim is processed — accident hospitalisation is payable from policy inception under his plan’s wording, and the insurer confirms this applies here.

Father’s diabetes complication: Six months into the policy, Rohit’s father is hospitalised for a diabetic foot ulcer. The claim is deferred — the PED waiting period for declared diabetes has not completed. The family pays ₹38,000 out-of-pocket for that admission.

Priya’s maternity: Priya is expecting in 18 months. The policy’s maternity waiting period is 3 years from inception. The delivery costs will not be covered — the couple has to fund this separately.

Rohit’s viral fever hospitalisation: Eight months in, Rohit is admitted for a severe viral infection. This is an illness, not an accident, but the initial waiting period has passed. The claim is processed normally.

One active policy. Four scenarios. Three different outcomes — all correct under the policy wording. For more on how waiting periods apply differently to individual and floater structures, see individual vs family floater health insurance — which is better.

Comparison: Waiting Period Types at a Glance

| Type | Applies To | What to Check |

|---|---|---|

| Initial waiting period | All illness claims at policy start | Policy wording — exact number of days from inception date |

| PED waiting period | Declared pre-existing diseases | Policy schedule — disease name and waiting period duration |

| Specific disease waiting period | Named conditions and listed procedures | Policy wording waiting-period list — named conditions vary by insurer |

| Maternity waiting period | Maternity and newborn benefit, if plan includes it | Policy wording — months or years before maternity claims become payable |

| Permanent exclusion | Conditions listed as excluded in policy wording | Exclusions section of policy wording — separate from waiting periods |

| Accident hospitalisation | Emergency treatment following an accident | Policy wording — confirm accident is explicitly excluded from initial waiting period |

How to Decide What’s Right for You

You are buying a family floater that includes parents with declared diabetes, hypertension, or prior surgery — compare the PED waiting period across shortlisted plans, not just the annual premium. A shorter PED waiting period on a slightly costlier plan may deliver claim access years earlier.

Maternity is planned within the next two years — check the maternity waiting period before you purchase. If the waiting period is 3 years or more, you will need to fund maternity costs independently regardless of whether you hold the policy.

You are porting from one insurer to another — request written confirmation from the new insurer about which completed waiting periods will be credited under IRDAI portability rules. Do not assume credit is automatic for all conditions.

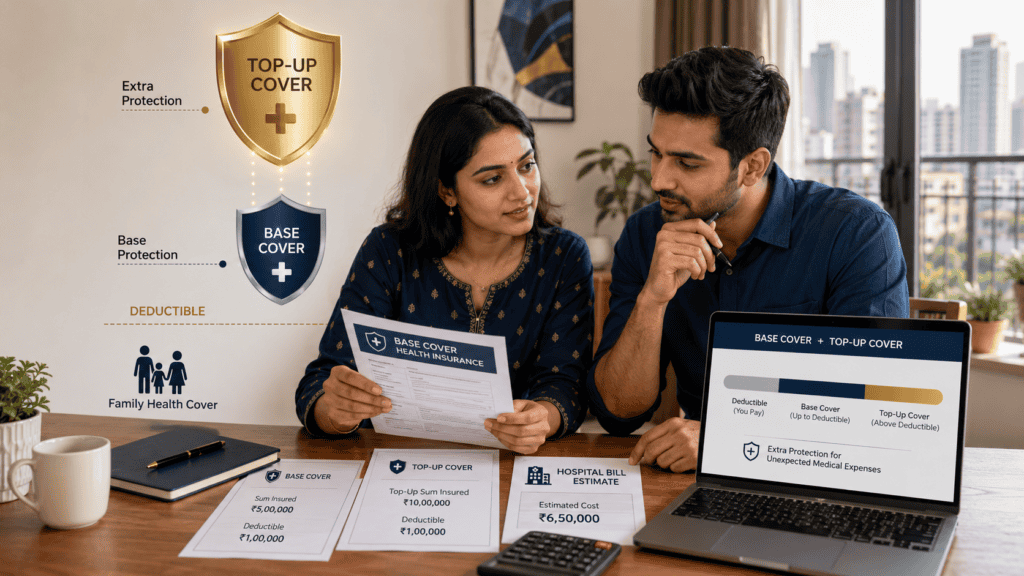

You are buying a top-up or super top-up plan alongside your base policy — note that top-up plans carry their own waiting periods, independent of your base policy. See how top-up health insurance extends your coverage before assuming your base policy’s completed waiting periods transfer to the top-up layer.

You are currently healthy and buying at age 25 to 30 with no medical history — the PED waiting period is less critical today, but buying early means waiting periods complete well before any significant health risk develops in later decades.

You are comparing two plans at a similar premium — the one with a shorter PED waiting period and a broader accident exception is generally more useful for a family with dependants or anyone with a medical history.

You expect health insurance to cover a surgery already scheduled or a delivery expected within the next few months — the waiting period will not be waived. Health insurance is risk protection for uncertain future events, not advance payment for known upcoming medical costs.

Common Mistakes to Avoid

Choosing a Plan on Premium Alone

Selecting the lowest annual premium without reading the waiting-period schedule is a common and expensive mistake.

A plan with a 3-year PED waiting period for declared hypertension means ₹0 in claim reimbursement for that condition for three years — even while you pay every premium on time. A plan with a higher annual premium and a 1-year PED waiting period may deliver far greater real value if your family has any declared medical history.

Always read the waiting-period schedule in the policy wording before finalising any plan.

Assuming All Claims Are Covered From Day One

Many first-time buyers assume that paying the first premium activates full coverage immediately.

It does not. Most standard health insurance policies apply an initial waiting period to all illness-related claims from inception. A claim filed for a non-accident illness within this window is typically rejected — regardless of how large the sum insured is.

Check the “waiting period” and “exclusions” sections of your policy wording before assuming illness coverage has started.

Hiding Pre-Existing Diseases at the Proposal Stage

Non-disclosure of a pre-existing disease — diabetes, hypertension, thyroid disorder, past surgery, ongoing medication — is the most dangerous mistake a health insurance buyer can make.

If a claim is filed and the insurer discovers an undisclosed PED during claim investigation, the claim can be rejected and the policy may be voided. Non-disclosure does not remove the waiting period — it replaces a temporary delay with a permanent claim risk across the entire policy life.

Declare every known condition at the proposal stage. There is no financial benefit to concealment, and the cost of discovery is severe.

Confusing Cashless Authorisation With Guaranteed Claim Settlement

A cashless authorisation letter means treatment can begin at a network hospital without upfront payment from your pocket.

It does not mean the claim is finally settled. If treatment later proves to fall within a waiting period — for instance, a condition identified during admission that is subject to a specific-disease waiting period — the insurer can reject the claim after discharge. Read how cashless vs reimbursement hospitalisation works to understand the difference clearly. Always retain original bills and discharge summaries regardless of the claim route used.

Forgetting to Check Waiting Periods When Adding a New Family Member

Adding a parent, spouse, or newborn to an existing family floater policy can trigger a fresh waiting period for that new member.

A parent added at renewal may face a new initial waiting period and PED waiting period even if your own waiting periods have been completed for years. Check the insurer’s policy wording on mid-term additions and new-member waiting-period treatment — do not assume the family policy’s completed periods apply to every new addition.

Treating a Permanent Exclusion as a Waiting Period

Some conditions listed in a policy are not subject to a waiting period — they are permanently excluded.

Waiting for any amount of time will not make a permanently excluded condition claimable. Congenital anomalies, self-inflicted injuries, and certain cosmetic procedures are examples that Indian health insurers commonly exclude permanently. These appear in the “exclusions” section of the policy wording — separate from the waiting-period section. Read both.

When This May Not Be the Right Choice

A standard health insurance policy with typical waiting-period structures may not meet your immediate medical needs in these specific situations:

A planned surgery is already booked: If an orthopaedic, cardiac, or elective surgery is scheduled within the next 60 to 90 days, a freshly purchased policy is unlikely to cover it. The specific-disease or initial waiting period will apply from the policy start date, not from your expected admission date.

Maternity is expected before the waiting period ends: If you are already pregnant or planning to conceive in the next 12 months, a new policy’s maternity waiting period will almost certainly not be complete in time for the delivery costs to be claimed.

A parent needs immediate cover for a significant pre-existing disease: Buying a policy for a parent who requires treatment for a declared condition in the near term means that specific treatment will be deferred until the PED waiting period completes. The policy is still worth buying — but the timing of benefit must be understood clearly.

You have only employer group cover and no personal policy continuity: If your employer’s group plan lapses when you change jobs or retire, you may need to restart all waiting periods afresh on a new personal policy. See why employer health cover alone may not be enough and why building personal policy continuity early matters.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Waiting-period rules, claim admissibility conditions, portability entitlements, and health insurance product standards in India are governed by IRDAI regulations and individual insurer policy wording. Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- IRDAI — irdai.gov.in — Regulatory guidelines on health insurance product standards, waiting periods, portability rules, and insurer obligations to disclose terms.

- Your insurer’s policy wording — The controlling document for your specific plan. Not the brochure. Not the sales pitch. Not the CIS summary. The full policy wording governs in any claim dispute.

- Policy schedule — The document issued with your policy that lists your name, sum insured, waiting periods, and buyer-specific terms.

- Customer information sheet (CIS) — A standardised one-page summary mandated by IRDAI that highlights key waiting periods and exclusions in accessible language.

- Licensed insurance advisor or IRDAI-registered intermediary — For specific questions about claim eligibility, waiting-period comparison, or portability terms before purchase or before filing a claim.

Expert Tips

- Buy personal health insurance early — before any illness develops: A policy bought at 27 or 28 with a clean medical history completes its PED and specific-disease waiting periods years before significant health risks typically emerge. Waiting until your 40s means starting a fresh waiting period precisely when claims become statistically more likely — and premiums more expensive.

- Declare every pre-existing condition at the proposal stage: Diabetes, hypertension, thyroid disorders, prior surgeries, ongoing prescriptions — every known condition. Non-disclosure is the leading cause of late-stage claim rejection in health insurance disputes in India. The short-term gain of avoiding a higher loading is not worth the long-term claim risk.

- Compare waiting periods alongside sub-limits and co-pay clauses: A policy with a short PED waiting period but a 1% room-rent sub-limit or a 20% co-pay on every claim can still produce a large out-of-pocket cost at claim time. Compare these features together, not in isolation.

- Save your proposal form and medical disclosure confirmation permanently: If a claim is ever challenged on non-disclosure grounds, your completed proposal form is your primary evidence of honest declaration. Keep both a digital copy and a physical copy — indefinitely.

- Evaluate your insurer using claim settlement ratio data, but do not stop there: A high claim settlement ratio is necessary but not sufficient. An insurer may settle most claims but do so slowly, with high dispute rates, or across a narrow cashless hospital network. Use claim settlement ratio data as one input among several — not the only criterion.

- When porting, initiate the process before your renewal date — not after: IRDAI portability rules require you to apply for porting at least 45 days before your policy renewal date. Missing this window forces a fresh renewal with the same insurer or a restart of waiting periods on a new policy with a different insurer.

Frequently Asked Questions

What is waiting period in health insurance?

A waiting period is a defined time after policy purchase during which certain claims are not payable. Types include an initial waiting period that applies to all illness claims at policy start, a PED waiting period for declared pre-existing diseases, a specific disease waiting period for named conditions, and a maternity waiting period if maternity benefit is included. Emergency accident hospitalisation is commonly exempt from the initial waiting period — but this must be confirmed in your policy wording.

Can I claim health insurance during the waiting period?

Claims for illness types covered by a waiting period clause are generally not admissible during that window. Emergency accident hospitalisation is typically payable from policy inception in most standard health plans — but the exact scope depends on your specific policy wording. A non-accident illness claim filed during the initial waiting period is usually rejected regardless of the sum insured.

Is accident hospitalisation covered during the waiting period?

Most Indian health insurance policies exempt accident-related emergency hospitalisation from the initial waiting period. However, what qualifies as an “accident” and which associated costs are covered depends on your specific policy wording — not on general industry practice. Confirm this explicitly in your policy schedule and policy wording before assuming accident cover is active from day one.

What is PED waiting period in health insurance?

PED stands for pre-existing disease. A PED waiting period is the time from policy purchase during which claims related to a declared pre-existing condition — such as diabetes, hypertension, heart disease, or thyroid disorder — are not payable. The duration varies by insurer and plan. Once the PED waiting period ends, the declared condition becomes claimable under all other standard policy terms — provided it was disclosed honestly at the proposal stage.

Can the waiting period be reduced or waived?

Some insurers offer plans with reduced waiting periods as a specific product feature, usually at a higher premium. Whether any waiting period can be reduced depends entirely on the insurer and the specific plan — there is no regulatory obligation on any insurer to reduce waiting periods on request. If a reduced waiting period is a priority, verify this feature directly in the policy wording before purchasing, not in the sales brochure.

Does porting my health insurance policy help with waiting periods?

Under IRDAI portability rules, when you move from one insurer to another, the new insurer must credit completed waiting periods — meaning if your PED waiting period was fully served under your previous policy, you should not have to serve it again for the same declared conditions. Portability credit is not always automatic, and conditions apply. Confirm in writing with both the outgoing and incoming insurer before initiating the port.

Is maternity covered immediately under a health insurance policy?

No. If your policy includes maternity benefit, a separate maternity waiting period applies from the policy inception date. Maternity-related claims filed before this period ends are not admissible. The duration of this waiting period varies by insurer and plan. If maternity cover within the next one to two years is important, verify the waiting period before purchasing — not after the delivery has been planned.

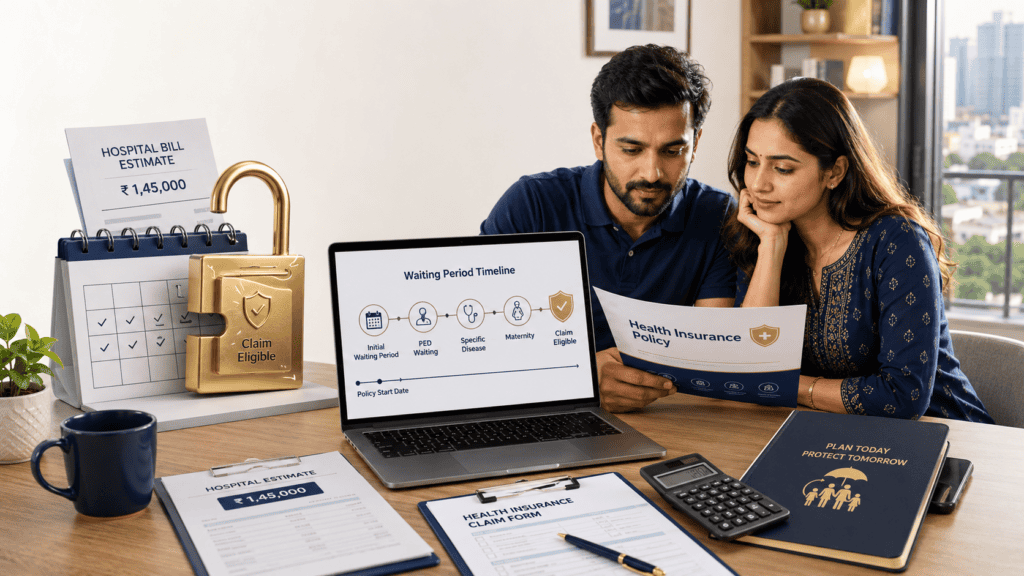

Can a claim be rejected after the waiting period is over?

Yes. The waiting period ending removes the timing restriction — it does not guarantee claim approval. A claim can still be rejected for non-disclosure of a pre-existing disease discovered during claim investigation, for treatment falling under a permanent exclusion, for exceeding room-rent sub-limits or co-pay clauses, or for incomplete documentation. Always read the full policy wording and retain all hospitalisation documents regardless of whether the waiting period has passed.

What is a moratorium period in health insurance?

A moratorium period is a regulatory protection under IRDAI guidelines. After continuous coverage for a specified number of years, the insurer generally cannot repudiate a claim solely on the grounds of non-disclosure of a pre-existing disease — except in cases of proven fraud. The moratorium period is separate from waiting periods. It does not override waiting periods or make excluded conditions claimable. Check current IRDAI guidelines for the applicable moratorium period, as this can change with regulatory updates.

What is the difference between a waiting period and a permanent exclusion?

A waiting period is temporary — once it ends, the restricted condition becomes claimable under the policy. A permanent exclusion means the condition is never covered, regardless of how many years the policy has been held or renewed. Congenital conditions, self-inflicted injuries, and cosmetic procedures are commonly permanently excluded in standard Indian health plans. These appear in the “exclusions” section of the policy wording — read it separately from the waiting-period section.

Final Verdict

A health insurance waiting period is not a minor clause buried in fine print — it directly determines whether your next family claim is paid, deferred, or denied. A policy that looks affordable on premium today may leave a significant gap if the PED waiting period runs for years while a declared condition needs treatment.

The approach that works is straightforward: buy early before any illness develops, declare every known condition honestly at proposal stage, read the policy wording and not just the brochure, and compare waiting periods alongside premium and sum insured. If you are adding parents to a family floater or buying alongside a top-up plan, check waiting periods for each policy separately — they are not automatically linked.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.