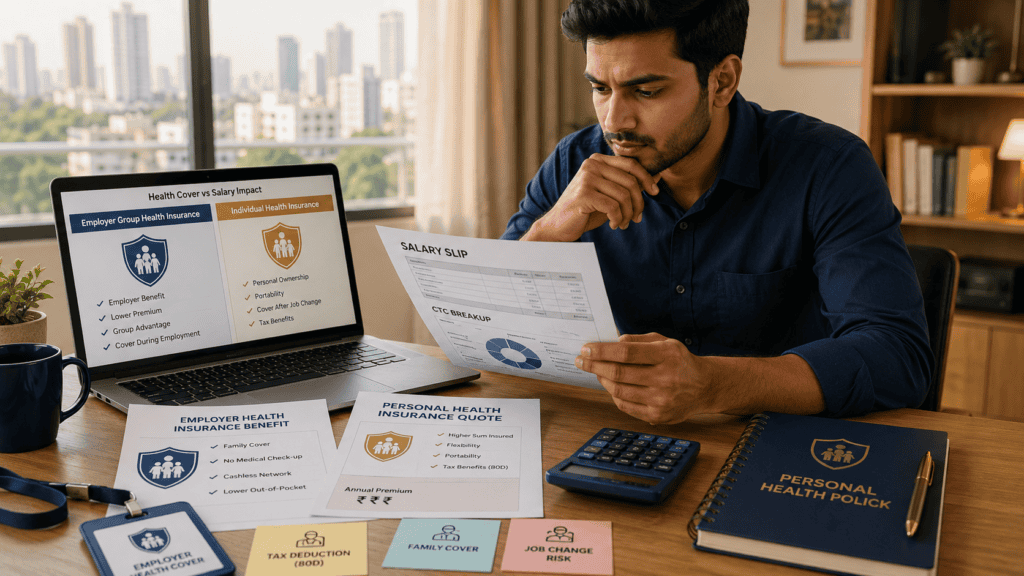

When it comes to group health insurance vs individual health insurance, most salaried employees in India make the same assumption: my company covers me, so I am taken care of. This comparison matters far more than most employees realise — and the gap between “taken care of” and “actually protected” can be expensive.

Employer group cover is real, useful, and often free on your payslip. But it is owned by your company, not by you. It can end the day you resign, retire, or get laid off. Your new employer’s policy may take 15–30 days to activate. During that window — especially if your spouse, children, or parents depend on your cover — your family could be completely uninsured.

This article breaks down the salary impact, family cover implications, job-change risk, and 80D tax angle across both options — from the viewpoint of a salaried Indian employee who wants to make a practical decision, not read a product brochure.

Quick Answer: Group Health Insurance vs Individual Health Insurance

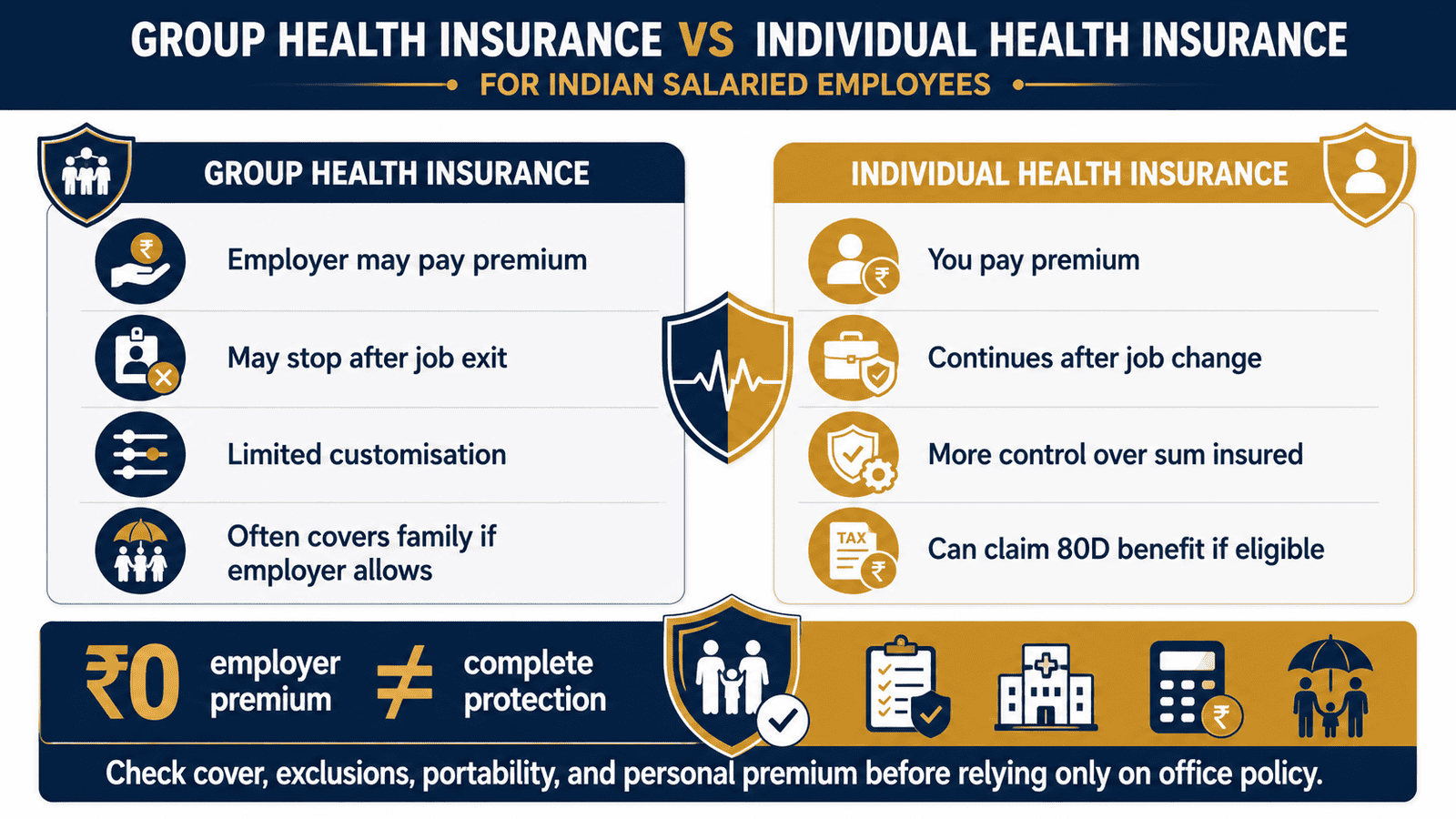

Group health insurance vs individual health insurance mainly differs in ownership and continuity. Employer group cover may cost you ₹0 directly, but it can end after resignation. Individual health insurance costs a personal premium but gives more control, portability, tax deduction eligibility, and protection during job changes.

Key Takeaways

- Employer group health insurance may require ₹0 direct monthly premium from your payslip — but it is tied to your employment and stops when you leave, which can leave your family exposed during job transitions lasting even a few weeks.

- Individual health insurance costs a real annual premium — typically ₹10,000–₹25,000 or more depending on age, sum insured, and family size — but stays active as long as you renew it, regardless of where you work.

- Section 80D of the Income Tax Act allows a deduction on eligible health insurance premiums you personally pay for yourself and family — the deduction is only available under the old tax regime; verify the current limit at incometax.gov.in before filing.

- Most employer group plans do not adequately cover parents — if your parents are financially dependent on you, a separate individual or senior citizen health policy for them is not optional, it is a planning priority.

- A job change, startup move, sabbatical, or freelancing stint can mean zero health cover for weeks if you rely only on your employer’s group policy and have no personal policy as backup.

- For most salaried families, the strongest approach is employer cover plus a personal base policy or top-up structure — the combination addresses both claim adequacy and employment-continuity risk simultaneously.

Comparison: Group Health Insurance vs Individual Health Insurance

| Parameter | Group Health Insurance (Employer) | Individual Health Insurance |

|---|---|---|

| Policy ownership | Owned by employer; employee is a group member | Owned by you; fully portable |

| Premium payment | Employer-paid, shared, or salary-deducted — varies by company policy | Paid entirely by you from personal income |

| Continuity | Ends on resignation, retirement, or termination | Continues as long as you renew each year |

| Sum insured | Fixed by employer — often ₹3–5 lakh, varies widely by company | Chosen by you — typically ₹5 lakh to ₹1 crore or more |

| Family coverage | May include spouse and children; parents often excluded or added at extra cost | You define who is covered, including parents under a separate floater |

| Customisation | Minimal — insurer, plan, and add-ons are chosen by employer | Full control over insurer, add-ons, room rent limits, sub-limits, and riders |

| Pre-existing disease waiting period | Often waived or significantly reduced for group plans | Standard waiting periods apply — typically 2–4 years depending on insurer and condition |

| Section 80D tax deduction | Not available to employee if employer pays premium | Available under old tax regime — verify current limit at incometax.gov.in |

| Portability on job change | Not portable — cover terminates when employment ends | Fully portable — you take it wherever your career goes |

| Salary or CTC impact | May appear as perquisite in CTC; no direct cash deduction if employer-paid | Out-of-pocket annual premium that reduces your investable monthly surplus |

Note: Coverage features, premium sharing arrangements, sub-limits, and waiting period terms vary significantly by employer, insurer, and policy. Verify the exact terms with your HR department and read the policy document carefully. If you are choosing a personal cover option, also explore whether individual or family floater health insurance suits your household before buying.

Key Facts at a Glance

| Fact | Group Policy (Employer) | Individual Policy (Personal) |

|---|---|---|

| Who holds the policy? | Employer | You |

| What triggers cover termination? | Resignation, retirement, or termination | Non-renewal only — entirely your decision |

| Pre-existing disease waiting period | Often waived under group plan terms | Typically 2–4 years — varies by insurer and condition |

| 80D tax deduction available? | No — if employer pays premium, employee gets no deduction | Yes — under old regime only; verify current annual limit at incometax.gov.in |

| Medical underwriting at enrolment? | Usually none — group enrolment at joining | Health declaration required; may involve medical tests |

| Premium basis | Group rate — not your individual age or health status | Your age, health history, sum insured, and chosen insurer |

Before assuming your employer’s group policy is sufficient, read our guide on what employer health cover actually includes — and why it may not be enough for your family’s real-world hospitalisation risk.

How Group and Individual Health Insurance Actually Work

What Employer Group Health Insurance Means in Practice

Group health insurance is a single policy that your employer buys from an IRDAI-registered insurer to cover all eligible employees — and, depending on the company’s arrangement, their immediate family. You are a member of the group, not the policyholder. This distinction is everything.

Because the insurer covers an entire group, premiums are negotiated at a group rate — typically lower than individual rates for a comparable cover. Pre-existing disease waiting periods are often waived, and you do not go through individual medical underwriting when you join. These are real advantages. According to IRDAI’s regulatory framework, group health policies operate under different terms than retail individual policies — including different renewal, portability, and claims terms.

The structural problem: the policy is not yours. If you leave the company, you leave the group. Your cover stops. There is often a gap between your last working day and your new employer’s group policy activation — sometimes 15 days, sometimes 30 days, sometimes longer. If a hospitalisation happens in that gap, the full cost is yours.

What Individual Health Insurance Means

Individual health insurance is a policy you buy directly from an IRDAI-registered insurer. You choose the sum insured, plan type, add-ons, and renewal terms. The policy is yours — it does not depend on your employment, your employer’s renewal decisions, or changes in company benefit policy.

If you are new to health insurance concepts, start with the fundamentals: read our guide on what health insurance covers, what it does not cover, and how claims actually work before comparing options.

Individual policies require underwriting. You disclose your health history, and the insurer may apply waiting periods, exclusions, or premium loading for pre-existing conditions. The logic of buying young is direct: buy at 28 with no declared conditions and your premium is locked in at a lower base rate. Wait until 38 with a diabetes diagnosis and the same cover is more expensive and comes with restrictions.

How Employer Health Insurance Appears in Your CTC

Most mid-size and large Indian employers include the cost of the group health insurance policy in the CTC structure — either as a line item under perquisites or absorbed into the total benefits package. In most cases, the employer pays the full premium and you see ₹0 deducted from your in-hand salary.

Some companies operate differently: they cover a base policy for the employee but charge an additional deduction if you want to add dependants, increase the sum insured, or top up coverage. Always confirm the exact arrangement with HR — ask whether the premium is fully employer-paid or cost-shared, and whether your dependants are actually enrolled and covered.

The Salary Impact That Most Employees Miss

The monthly payslip impact of employer group cover is ₹0. But the financial risk carried is not zero. It is a contingent liability: if a hospitalisation event, a job change, or a policy change at your employer coincides, your family faces a real cost with no insurer to cover it.

Individual health insurance converts that contingent risk into a fixed, predictable monthly outflow — typically ₹1,000 to ₹2,500 or more per month depending on age, family size, and sum insured. That monthly payment buys continuity: cover that cannot be cancelled by an employer’s decision, a restructuring, or an HR delay.

For families — particularly those with children, dependent parents, or a planned career transition — this is the core argument for owning personal health insurance alongside employer cover. Read more on why employer health insurance, while valuable, is often not a complete solution for a family’s long-term medical risk.

Real Example: Rohan’s Cover Gap Analysis

Rohan, 32, is a software engineer in Pune earning ₹18 lakh CTC. His employer provides a ₹5 lakh family floater group health cover for him, his spouse, and their two-year-old child. His parents are not included in the group policy. His payslip deduction for this cover: ₹0.

Rohan is planning a job switch in the next six months. His new employer’s group policy activates 30 days after his joining date. That means Rohan and his family — including his spouse, who is expecting a second child — will have zero active employer health cover for at least 30 days between jobs.

He looks into buying a ₹10 lakh personal family floater. An indicative annual premium for a family of three to four (two adults in their early 30s and one to two children) from a reputable IRDAI-registered insurer is approximately ₹18,000–₹22,000 per year — though the actual premium depends on age, health history, sum insured, insurer, and plan features. He must verify exact quotes directly with insurers before deciding.

At ₹18,000 per year, that is ₹1,500 per month. If Rohan pays this premium himself under an eligible individual policy and files under the old tax regime, he may be able to claim a deduction under Section 80D of the Income Tax Act — subject to current applicable limits and conditions. See our full breakdown in the 80D deduction guide for health insurance before filing.

Key insight: Rohan’s employer cover costs ₹0 per month — but it leaves his family unprotected during his job transition, excludes his parents entirely, and carries only a ₹5 lakh cap at a time when a single hospitalisation in a Pune private hospital can cost ₹3–8 lakh or more.

How to Calculate the Salary Impact of Your Health Cover Decision

Net annual salary impact = Personal premium paid − Eligible tax benefit (if applicable under old tax regime)

Step-by-Step Working Using Rohan’s Numbers

Assumption: Rohan buys a ₹10 lakh personal family floater at ₹18,000 per year. He is in the 30% tax bracket and files under the old regime.

| Scenario | Key Inputs | Annual Cash Impact |

|---|---|---|

| Employer group cover only | ₹0 direct premium; ₹5 lakh sum insured; no 80D deduction available | ₹0 outflow — but full job-continuity risk and no personal policy continuity |

| Personal cover added — old tax regime | ₹18,000/year premium; 30% bracket; 80D deduction claimed | ₹18,000 outflow − ~₹5,400 estimated tax saving = net ~₹12,600/year (≈ ₹1,050/month) |

| Personal cover added — new tax regime | ₹18,000/year premium; no 80D deduction available | ₹18,000 outflow = ₹1,500/month, no tax offset |

Important: The ₹18,000 premium and ₹5,400 tax saving are illustrative assumptions only. Actual premium varies by age, health, insurer, and plan. The 80D deduction is available only under the old tax regime and is subject to current statutory limits — verify at incometax.gov.in before filing. Use our take-home salary calculator to understand how this premium fits your actual monthly in-hand budget.

The broader point: ₹1,050–₹1,500 per month is a modest and predictable outflow compared to the financial exposure of a ₹4–8 lakh hospitalisation during a coverage gap. The option with ₹0 monthly cost is not automatically the financially safer option.

How to Decide What’s Right for You

You are single, in your mid-20s, and at a stable employer with decent group cover — employer insurance may handle near-term hospitalisation needs, but buying a personal base policy now locks in a lower premium before any health conditions develop. Starting early is cheaper than correcting later.

You are married with children and your employer’s group floater covers only ₹3–5 lakh for the entire family — compare that cap against realistic private hospital bills in your city before assuming the cover is adequate. A single ICU admission can consume the full limit.

Your parents are financially dependent on you and are not covered under your employer’s group plan — a separate individual or senior citizen health policy for them should be treated as a financial priority, not an optional add-on.

You are planning a job switch, moving to a startup, going freelance, or taking a career break — personal health cover should be in place before the transition begins, not after you realise there is a gap.

Your employer’s sum insured is under ₹5 lakh and hospitalisation costs in your city regularly exceed ₹3–4 lakh — consider adding a top-up or super top-up plan to extend effective cover at a lower premium than buying a larger base policy from scratch. Read about how top-up health insurance extends your cover and whether the structure suits your existing employer policy.

You are in the 30% tax bracket, file under the old regime, and personally pay a health insurance premium — the 80D deduction reduces your effective annual cost meaningfully. A ₹25,000 premium under full deduction eligibility effectively costs less than ₹18,000 out-of-pocket. Verify the current deduction limit before calculating.

You should not treat employer group health insurance as your only long-term health financial plan — regardless of how generous the current benefit appears. It is linked to your employment, can change at your employer’s renewal, and ends at the exact moment a job transition makes you most financially vulnerable.

Common Mistakes to Avoid

Assuming Employer Cover Is Permanent

Group health insurance ends when employment ends — this is the single most expensive assumption salaried employees make. Many employees discover this only when they are between jobs and face a hospitalisation with no active policy.

A standard private hospital admission in a tier-1 Indian city can cost ₹2–10 lakh or more. Without active cover, the full amount comes directly from your savings or leads to debt. The financial damage compounds if the event happens while you are also adjusting to a salary gap.

Buy a personal policy before you resign — not after.

Not Checking Who Is Actually Covered Under Your Group Plan

Employees regularly assume their group plan covers spouse, children, and parents. In practice, employer group plans vary widely: some cover the employee only, some cover spouse and children at no extra cost, and some include parents at an additional salary deduction.

Ask HR for the group policy schedule in writing — specifically who is listed as a covered dependant, what sum insured applies to each person, and what exclusions or co-pay conditions apply to family members.

If your parents are not covered, do not assume they are.

Ignoring Sub-Limits, Room Rent Caps, and Co-Pay Clauses

A ₹5 lakh sum insured does not mean ₹5 lakh is available for every type of claim. Many policies include room rent sub-limits — for example, 1% of sum insured per day — that cap your room category and proportionately reduce all associated charges if you exceed the limit.

If your room rent sub-limit is ₹5,000 per day and you choose a ₹8,000-per-day room, the insurer may reduce your entire claim proportionately — not just the room charge. IRDAI’s consumer education portal at irdai.gov.in explains sub-limit mechanics in detail.

Read the policy document before you need it, not after a claim is rejected.

Waiting Until You Have a Health Condition to Buy Personal Insurance

Individual health insurance uses underwriting. If you disclose a pre-existing condition — diabetes, hypertension, thyroid disorder — the insurer may impose a waiting period, additional exclusion, or premium loading for that condition. Buying early, when healthy, avoids all of this.

A ₹10 lakh family floater bought at 28 can cost 30–50% less annually than the same cover purchased at 40 with a declared condition. The difference compounds over decades of renewal.

Treating ₹0 Monthly Deduction as Zero Financial Risk

Employer group cover may show ₹0 on your payslip. But zero deduction is not the same as zero risk. The hidden cost is the coverage gap exposure during employment transitions, the lack of control over your insurer or plan terms, and the fact that your employer can change group policy terms at their renewal without your input.

Think of it as a benefit with conditions — valuable during employment, unreliable as a standalone long-term plan.

Forgetting That Personal Policy Premiums Rise With Age

Health insurance premiums increase with each year of age. Delaying a personal policy by five years may save ₹15,000–₹30,000 in cumulative short-term premiums. But it can result in substantially higher annual premiums for the next 30–40 years — plus the risk of needing to buy cover after a health event has already been diagnosed and declared.

Choosing a Policy Based Only on Premium

A low-premium individual policy with heavy sub-limits, a high co-pay, a narrow hospital network, or a low claim settlement ratio may perform much worse in an actual claim than a slightly more expensive policy with better terms. Before choosing any health policy, check the claim settlement ratio in the latest IRDAI annual report and confirm which hospitals in your city offer cashless settlement.

When This May Not Be the Right Choice

If your monthly cash flow is already stretched: Balancing EMIs, an emergency fund, and insurance premiums simultaneously is a real constraint for many salaried employees. If adding ₹1,500–₹2,500 per month in health insurance premium creates genuine financial pressure, a smaller base policy or a top-up structure that costs less may be a more sustainable starting point than a large comprehensive plan.

If your employer already provides high cover with good terms: If your group policy covers ₹10–20 lakh for the whole family, includes your parents, has cashless access at hospitals near you, and imposes minimal sub-limits, the immediate urgency for a large additional personal policy may be lower — though a modest base continuity policy is still worth maintaining to protect against the job-change gap.

If you have a pre-existing condition under active management: Buying a personal policy with a pre-existing diagnosis will likely trigger a waiting period of 2–4 years for that specific condition. This means the new policy does not cover that condition immediately. Do not cancel or reduce employer cover in anticipation of personal cover activating — let the waiting period complete first before making any changes to existing cover.

If you are comparing purely on premium without reading the policy document: A cheap individual policy with aggressive sub-limits, a high co-pay, or exclusions for common conditions may provide less real-world protection than a higher-premium plan with clean terms. Paying less for cover that does not pay out at the critical moment is not a saving — it is a false floor.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Health insurance regulation, tax deduction rules, policy portability terms, and premium structures all change with IRDAI guideline updates, Union Budget announcements, and individual insurer decisions. No single article — including this one — should be your final source before a purchase or tax filing decision.

- IRDAI (Insurance Regulatory and Development Authority of India) — irdai.gov.in: Verify insurer registration status, consumer rights, group vs. individual policy regulations, portability rules, claim settlement norms, and how sub-limits and co-pay terms are regulated.

- Income Tax Department — incometax.gov.in: Verify the current Section 80D deduction limit for health insurance premiums, eligibility conditions, which tax regime permits the deduction, and applicable filing requirements for the current assessment year.

- Your employer’s HR department: Request the group mediclaim policy schedule in writing — including covered dependants, sum insured per person, sub-limits, co-pay clauses, TPA details, claim process, and what happens to your cover on resignation, retirement, or notice period completion.

- Your chosen insurer directly: For individual policies, verify waiting periods for pre-existing conditions, cashless network hospital lists in your city, room rent limit structures, and the step-by-step claim process before purchasing.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Do not cancel a personal policy just because your employer now gives group cover. If you already own an individual health policy, keep it active. The continuity of your personal policy — especially the waiting period clock that has already run — is valuable and cannot be cheaply restarted once interrupted.

- Buy personal cover before your first job switch, not after. The worst time to discover a coverage gap is when a family member needs hospitalisation between your last day at one company and your first covered day at the next. If a career move is likely in the next 12 months, a personal policy should be in place today.

- Read sub-limits, co-pay, and room rent caps before you sign anything. Two policies with identical ₹10 lakh sum insured can pay out very differently for the same hospitalisation if one has a 1% room rent cap and 20% co-pay and the other does not. Premium is one number; effective payout is another.

- Treat employer cover as a first-layer benefit — not a financial plan. Group health insurance reduces your immediate out-of-pocket exposure during employment. It is not designed to be — and should not be treated as — a substitute for long-term personal health financial planning.

- Review your coverage after every major life event. Marriage, childbirth, a parent becoming financially dependent, a significant salary increase, or a job switch are all valid triggers to reassess whether your existing group and personal cover still matches your actual risk and family situation.

- If you are in the 30% bracket under the old regime, your personal premium is cheaper than the sticker price. A ₹25,000 annual premium with a full 80D deduction at 30% has an effective net cost of approximately ₹17,500 or less — verify the current deduction ceiling at incometax.gov.in before calculating your actual saving.

- Check the claim settlement ratio before choosing an insurer. IRDAI publishes annual insurer-wise claim settlement data. An insurer settling 98% of claims provides meaningfully more certainty than one at 88% — even if the premium difference is ₹1,000–₹2,000 per year. A policy that does not pay out when needed is not insurance.

Frequently Asked Questions

Is employer health insurance enough in India?

For most salaried employees, employer group health insurance provides useful baseline cover during employment — but it is rarely sufficient on its own. Common limitations include low sum insured (₹3–5 lakh for a family), exclusion of parents, sub-limits on room rent and certain conditions, and the most material risk: cover ends when you leave the company. For families with dependants or employees with job mobility, a personal policy supplements both adequacy and continuity.

Does group health insurance continue after resignation?

In most cases, employer group health insurance stops on your last working day or at the end of the notice period, depending on company and insurer policy. Some IRDAI-registered insurers allow portability of a group cover to an individual plan — but this must be requested within a specified window and the terms and premium will change. Verify the portability option with your HR and insurer before your resignation date, not after your last day.

Is health insurance part of CTC in India?

Yes, in most mid-size and large Indian companies, the employer’s premium payment for group health insurance is included in the CTC breakdown as a perquisite or benefit. Some companies show it as a separate line item; others absorb it silently into the total package. If you are unsure, ask HR for a written CTC breakup and confirm whether the premium is fully employer-paid or cost-shared with you.

Can I claim 80D for employer health insurance?

No — if your employer pays the health insurance premium on your behalf, you cannot claim a Section 80D deduction for it. The deduction applies only when you personally pay eligible health insurance premiums for yourself, your spouse, children, or parents. If you pay a portion of the group plan premium directly from your salary, that personal contribution may be eligible — verify the exact conditions with a tax professional and check incometax.gov.in for the current deduction limit and regime eligibility.

Should I buy individual health insurance if my company gives group cover?

For most salaried employees — especially those who are married, have children or dependent parents, or are likely to change jobs in the next two to three years — buying a personal base policy alongside employer cover is sound financial planning. Employer cover is employment-linked and ends at resignation. A personal policy provides continuity regardless of your employment status. The monthly cost of a basic family floater is typically ₹1,000–₹2,000, which is modest relative to the hospitalisation costs it protects against.

What happens to health insurance when I change jobs?

When you resign, your employer group health insurance ends — typically on your last working day or the last day of your notice period. Your new employer’s group policy usually takes 15–30 days or more to activate after you join. During this gap, you and your family may have no active health cover. If you hold a personal individual policy, it continues without any interruption and covers you throughout the transition. This is the most practical, day-to-day argument for owning personal cover independent of where you work.

Is group mediclaim better than personal health insurance?

Each has genuine advantages. Group mediclaim wins on cost (often free to employee), ease of enrolment (no individual underwriting), and relaxed pre-existing disease terms. Personal health insurance wins on continuity, portability, customisation, family flexibility, and 80D benefit eligibility. For most salaried employees, the right answer is not one versus the other — it is both, with employer cover as the first layer and personal cover for continuity and adequacy.

Can I cover my parents under employer health insurance?

It depends entirely on your employer’s group policy terms. Some companies allow parents to be added as covered dependants, sometimes at an additional premium deducted from salary. Many companies do not include parents in the standard group plan at all. Verify directly with your HR department before assuming parent cover exists. If parents are not covered or the cover is inadequate, a separate senior citizen individual health policy is worth considering — particularly given higher hospitalisation frequency and costs with age.

What is the waiting period difference between group and individual health insurance?

Group mediclaim policies frequently waive standard waiting periods — including for pre-existing diseases — which is a meaningful benefit if you join a company while managing a health condition. Individual health insurance applies standard waiting periods: typically 30 days for initial cover (accidents usually excepted), and 2–4 years for pre-existing conditions depending on the insurer. Buying a personal policy early — before any health condition is diagnosed and declared — protects you from long waiting periods precisely when cover would matter most.

Can I claim Section 80D under the new tax regime?

No. Section 80D deduction for health insurance premium is not available under the new tax regime, which is the default regime in India from FY 2023-24 onward. The deduction is only available if you explicitly opt for the old tax regime. If you are under the new regime and personally paying health insurance premium, you still receive full insurance protection — but without a tax offset on the premium cost. Verify current regime rules and deduction limits at incometax.gov.in or with a registered tax professional before filing.

Final Verdict

Group health insurance vs individual health insurance is not an either-or choice for most salaried employees in India — it is a layering decision. Employer group cover is a genuine financial benefit: it adds meaningful hospitalisation protection during your employment years at no or low direct cost, and it often comes with relaxed underwriting. Use it fully. But do not build your family’s health financial plan around it.

Individual health insurance gives you what employer cover structurally cannot: continuity across job changes, portability through career transitions, the ability to cover parents who may be excluded from your group plan, and potential 80D tax efficiency under the old regime. For families — especially those with dependants, health risks, or any probability of career change in the next three to five years — personal cover is a practical financial necessity, not a premium upgrade.

The clearest approach for most salaried employees: maintain employer cover as a first-layer benefit during employment, add a personal base policy or top-up structure for continuity and claim adequacy, and review your total cover after every major life event — marriage, a new child, a parent becoming dependent, a salary increase, or a job switch.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing. Premiums, coverage terms, waiting periods, and policy features vary by insurer, age, health status, and plan. Verify current terms with your insurer and IRDAI-registered intermediaries before making any decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.