Most salaried employees buying term insurance for a ₹10 LPA salary pick ₹1 crore, fill in a comparison form, and move on. That number might be exactly right — or it might leave your family ₹50 lakh to ₹1 crore short, depending on how many people rely on your income, what loans are outstanding, and what your child’s education will eventually cost. The 10x income rule is a starting point, not a final answer. This article walks you through three standard calculation methods — step by step — so you arrive at a specific number that fits your life, not a generic one-size-fits-all recommendation.

Quick Answer: Term Insurance for 10 LPA Salary

Term insurance for 10 LPA salary should usually start around ₹1 crore to ₹1.5 crore, then be adjusted for loans, dependents, child education, existing savings and current life cover. A single person may need less, while a family with debt may need more.

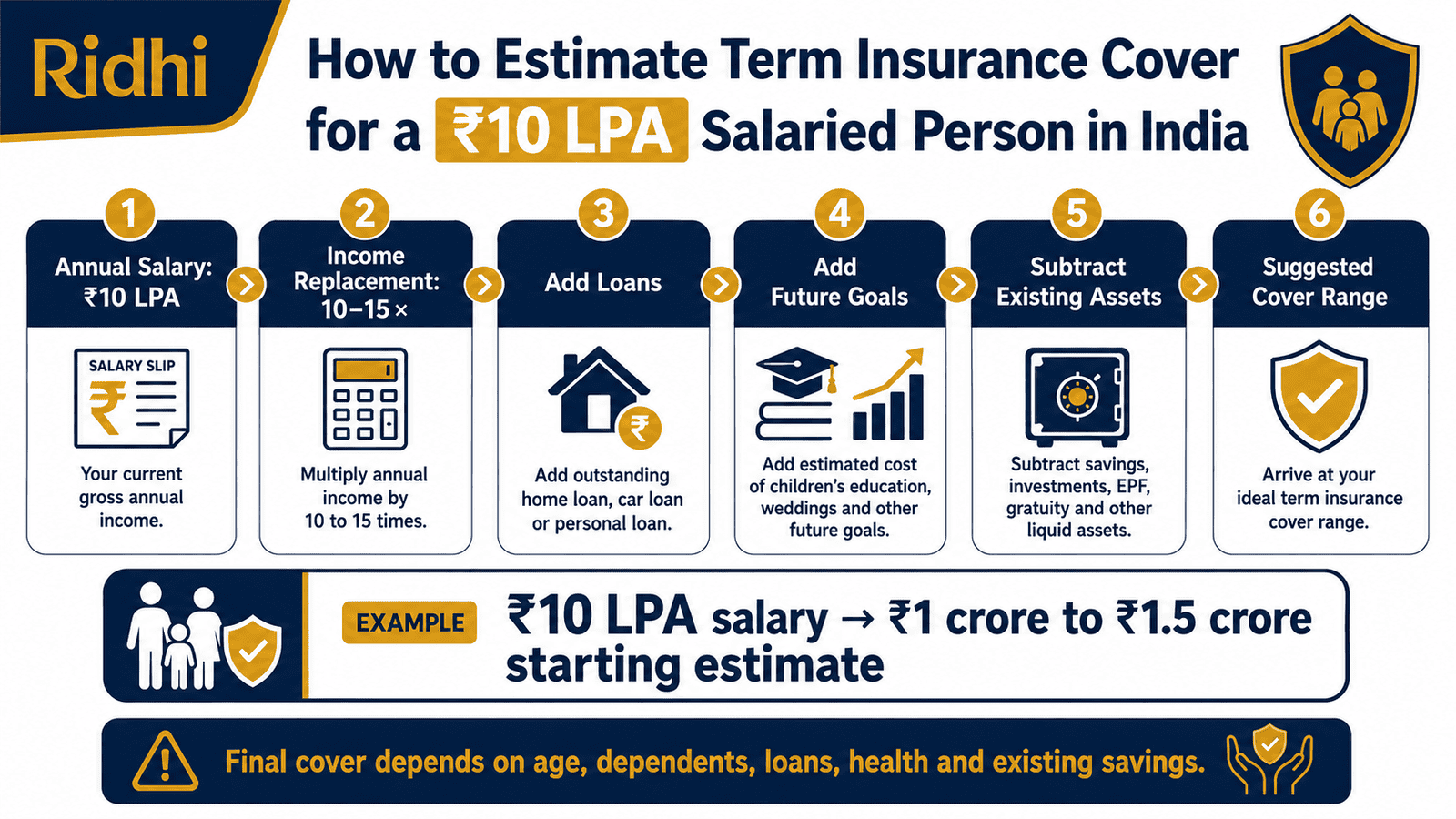

How to Calculate Term Insurance Cover for ₹10 LPA Salary

Three methods are widely used in India. Each gives a different number. The practical approach is to run all three and treat the highest result as your minimum required cover.

Method 1: Income Replacement (10x Rule)

Multiply your annual income by 10. At ₹10 LPA, this gives ₹1 crore as a baseline. The logic: ₹1 crore invested at a conservative 6–7% annual return generates roughly ₹6–7 lakh per year — close to replacing your take-home income for 15–20 years.

Cover = Annual Income × 10 = ₹10,00,000 × 10 = ₹1,00,00,000

This method is simple and widely cited. It is also incomplete — it ignores your outstanding loans, your children’s future education costs, and whether your spouse earns independently. Use it as a floor, not a ceiling.

Method 2: Human Life Value (HLV)

HLV estimates the present value of all future income your family would lose if you were gone today. It factors in years to retirement, household expenses, and an inflation discount rate.

HLV ≈ Annual Income × Years to Retirement × Inflation Discount Factor

For a 31-year-old planning to retire at 60 — 29 working years remaining — an approximate HLV calculation using a 7% discount rate gives a multiplier of around 14–17x. At ₹10 LPA, that puts the HLV estimate between ₹1.4 crore and ₹1.7 crore. Higher than the 10x rule, and closer to what a family genuinely needs.

Method 3: Needs Analysis (Add Liabilities, Subtract Assets)

This is the most personalised method and the one most financial planners actually use. It starts from your family’s real financial exposure — then subtracts what you already have.

Cover = Income Replacement + Outstanding Loans + Future Goals − Existing Savings − Existing Cover

Here is a worked example for a typical ₹10 LPA earner with a spouse, one child aged 4, and an active home loan:

| Component | Basis | Amount |

|---|---|---|

| Income replacement | 15x annual income | ₹1,50,00,000 |

| Home loan outstanding | Actual balance due | ₹25,00,000 |

| Child’s higher education | Projected cost, 15 years out | ₹20,00,000 |

| Spouse income gap | Career break or lower earnings period | ₹10,00,000 |

| Total Need | ₹2,05,00,000 | |

| Less: Liquid savings and mutual funds | Accessible in an emergency | −₹5,00,000 |

| Less: Employer group term cover | Typical employer-provided amount | −₹10,00,000 |

| Recommended Cover | ≈ ₹1,90,00,000 |

The needs analysis rounds to approximately ₹2 crore for this profile. For a ₹10 LPA earner with a growing family and an active home loan, ₹1 crore alone leaves a gap of almost ₹90 lakh.

For a personalised figure based on your exact salary, loans, and goals, see our detailed cover calculation guide.

Key Takeaways

- The 10x income rule gives ₹1 crore as a starting baseline for ₹10 LPA — but it ignores loans, education goals, and dependents, which typically push the number higher.

- Every ₹25 lakh of outstanding loan should be added on top of your income replacement baseline — a ₹25 lakh home loan alone takes the recommended cover from ₹1 crore to ₹1.25 crore before anything else is counted.

- Employer group term cover — typically ₹5–10 lakh — should never replace a personal term plan; it disappears the day you change jobs.

- A 31-year-old non-smoker male can expect meaningfully lower premiums than a 36-year-old for the same cover amount — buying early locks in a lower annual cost for the entire policy term.

- Policy tenure should extend to at least age 60 so your cover stays active until your dependents are financially self-sufficient and your loans are repaid.

- The needs analysis method — income replacement plus loans plus goals, minus existing savings and cover — consistently gives a higher and more accurate figure than the 10x rule alone.

- Riders such as critical illness and waiver of premium can add meaningful protection for a relatively small additional annual cost — worth evaluating at the time of purchase.

Key Facts at a Glance

| Parameter | Detail | Note |

|---|---|---|

| 10x income baseline (₹10 LPA) | ₹1,00,00,000 | Minimum starting point |

| Recommended for family with home loan | ₹1.5 crore – ₹2 crore | Based on needs analysis |

| Recommended policy tenure (age 31) | 29–30 years (to age 60–61) | Cover active through peak liability years |

| GST on term insurance premium | 18% | Verify at irdai.gov.in |

| Premium deduction under Income Tax Act | Section 80C, up to ₹1.5 lakh total | Verify at incometax.gov.in |

| Regulator | IRDAI (Insurance Regulatory and Development Authority of India) | irdai.gov.in |

Why ₹1 Crore May Not Be Enough for a ₹10 LPA Salary

The 10x income rule became popular because it is simple and produces a round number. But it was designed for an era of lower property prices, smaller education costs, and fewer multi-decade loans. For a salaried employee in Bengaluru or Pune taking on a ₹30–50 lakh home loan in their early 30s, the gap between what ₹1 crore covers and what the family actually needs is real.

Consider what ₹1 crore actually does for your family. Invested at 6% per year, it generates approximately ₹6 lakh annually. That replaces your take-home income on a ₹10 LPA salary reasonably well — but only before you account for the home loan EMI that still needs to be paid every month, the school fees that will only grow, and the inflation eroding the corpus over 20 years.

The Loan Factor

Any outstanding loan your family inherits represents a direct liability. A ₹25 lakh home loan does not pause because the breadwinner is gone — the EMI either continues from the insurance payout or the property faces legal complications. The cleanest solution: add every rupee of outstanding loan balance to your required cover. For a term insurance plan basics understanding, see our term plan basics guide.

The Dependent Factor

A spouse who is a homemaker, or who earns significantly less, adds a real income gap to your calculation. A child aged 4 today will need higher education funding in 14–15 years — that cost, even at modest estimates, can reach ₹20–30 lakh for a domestic college degree. Both of these are additions on top of the income replacement baseline.

Employer Group Cover: Do Not Count It

Many salaried employees factor in their employer’s group term insurance — typically ₹5 lakh to ₹10 lakh — when estimating their personal cover. This is a mistake. Group cover is contingent on employment. The day you resign, are laid off, or switch jobs, the cover ends. It should be treated as a bonus — not a pillar of your family’s financial protection. Subtract it from your needs calculation only if you are confident it will remain active throughout your earning years — which, practically, you cannot be.

When to Review Your Cover

Term insurance is not a one-time decision. A cover that was right at 31 may be insufficient at 35 after a salary hike, a second child, or a top-up home loan. Review your required cover every three to five years, and mandatorily after: marriage, birth of a child, taking a new loan, a significant salary increase, or the closure of a major loan.

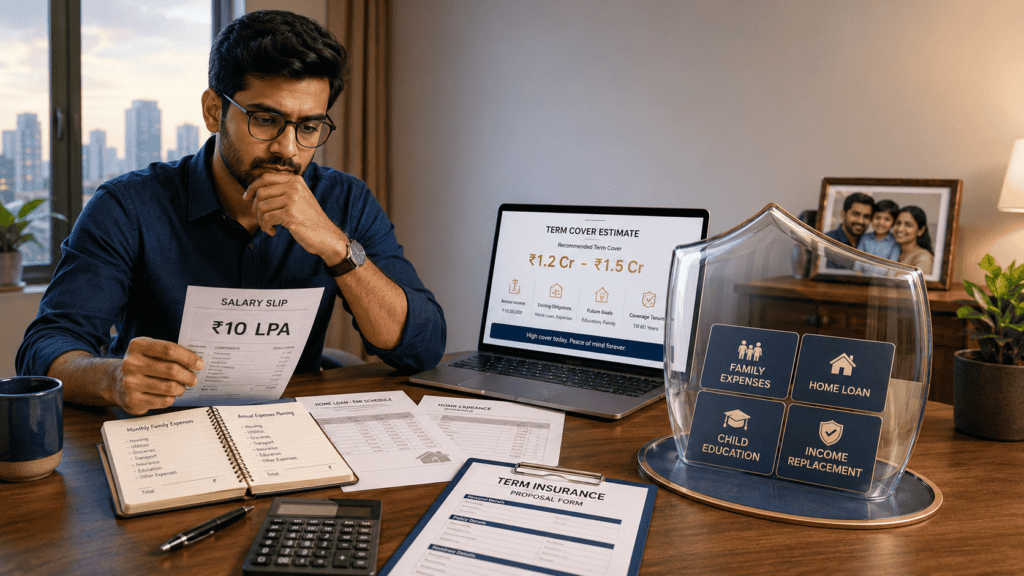

Real Example: Rohan Menon, Software Engineer, Bengaluru

Rohan Menon, 31, works as a mid-level software engineer in Bengaluru and earns ₹10 LPA in CTC. His take-home is approximately ₹72,000–74,000 per month — you can estimate yours using the take-home salary calculator. Rohan’s wife Priya is a teacher earning ₹4.8 LPA. They have a four-year-old daughter. They took a ₹25 lakh home loan two years ago, with ₹23 lakh still outstanding. Rohan currently has no personal term plan — only a ₹10 lakh group cover through his employer.

Running the needs analysis: ₹1.5 crore income replacement (15x) plus ₹23 lakh outstanding loan plus ₹20 lakh for his daughter’s higher education plus ₹10 lakh for Priya’s income gap period — totalling ₹2.03 crore. Subtract ₹4 lakh in accessible savings and ₹10 lakh employer cover: recommended personal cover is approximately ₹1.89 crore — which he should round up to ₹2 crore for a clean sum assured.

The key insight: Rohan needs roughly twice what the 10x rule alone suggested. His loans and his daughter’s education costs are the difference.

Comparison: ₹1 Crore vs ₹1.5 Crore vs ₹2 Crore

| Parameter | ₹1 Crore | ₹1.5 Crore | ₹2 Crore |

|---|---|---|---|

| Covers 10x income rule | Yes | Yes | Yes |

| Covers ₹25L home loan + income | No | Yes | Yes |

| Covers child education (₹20L) | No | Borderline | Yes |

| Covers spouse income gap | No | Partial | Yes |

| Best suited for | Single, no loans, no dependents | Small family, single loan | Family with loans and education goals |

| Indicative annual premium range (31M, non-smoker) | Verify before publishing | Verify before publishing | Verify before publishing |

Note: Premiums vary by age, health status, policy tenure, insurer, and underwriting assessment. Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing. Indicative premium figures should be confirmed directly with IRDAI-registered insurers at the time of application.

How to Decide What’s Right for You

You are single, have no dependents, and carry no outstanding loans — THEN ₹1 crore may be adequate as a starting cover, especially if you plan to review it within three years upon starting a family.

You have an outstanding home loan above ₹15 lakh — THEN add the full outstanding balance on top of your income replacement figure; ₹1 crore will leave your family holding the EMI liability.

Your spouse does not work or earns less than ₹5 LPA — THEN add at least ₹10–15 lakh to cover the income gap period; a homemaker spouse cannot immediately replace a lost income of ₹10 LPA.

You have two children under the age of 10 — THEN add ₹15–20 lakh per child for higher education costs; these amounts compound over 10–15 years and should be locked in now while premiums are low.

You want to evaluate your insurer’s claim track record before buying — THEN check the claim settlement ratio guide before comparing premium prices.

You already have liquid savings or mutual fund investments above ₹20 lakh — THEN subtract that amount from your needs analysis total; existing assets reduce how much insurance your family needs to remain financially stable.

You are in your early 30s with a family, active home loan, and young children — do NOT settle for ₹1 crore without running the full needs analysis; the income replacement gap alone at this life stage almost always points to ₹1.5 crore or higher.

Common Mistakes to Avoid

Stopping at the 10x Rule

The 10x income rule gives ₹1 crore for ₹10 LPA — and many people treat that as the final answer.

It ignores loans, education goals, dependent needs, and inflation entirely. For a family with even a single outstanding loan, the gap between ₹1 crore and actual needs is ₹25–50 lakh or more.

Run all three methods — income replacement, HLV, and needs analysis — and use the highest result.

Counting Employer Group Cover as Personal Insurance

Employer group term cover is a workplace benefit, not a personal asset.

When you change jobs — and most salaried employees do, multiple times — that cover disappears. If your new employer offers no group plan, you are temporarily uninsured. At a new age and with a potential health condition, buying fresh cover will cost significantly more.

Treat employer cover as a bonus. Build your own personal plan independently.

Buying Endowment or ULIP Instead of Term

Mixing insurance and investment in a single product almost always results in inadequate cover at a high premium.

A ₹1 crore endowment plan would cost several times more per year than a ₹1 crore term plan, leaving less money for actual investments. The returns on endowment policies also rarely beat inflation after adjusting for the opportunity cost. See why most experts prefer term over endowment for pure protection needs.

Keep insurance and investment completely separate.

Choosing Too Short a Policy Tenure

A policy that ends at age 50 or 55 leaves you uninsured through your peak loan repayment years and while your children are still financially dependent.

A home loan taken at 31 for 20 years runs until age 51. A child entering college at 18 will do so when you are 35 — still well within your need for cover.

Set the policy term to at least age 60, or to when your youngest child is likely self-sufficient.

Not Disclosing Pre-Existing Health Conditions

Undisclosed medical history is among the most common grounds for claim rejection during underwriting at the time of a death claim.

Insurers conduct medical underwriting at the time of purchase and reassess during claim settlement. Concealing a condition to lower the premium creates the exact risk your family is trying to avoid.

Disclose everything at purchase — hypertension, diabetes, prior surgeries — and let the insurer price it accordingly.

Comparing Insurers Only on Premium Price

A lower annual premium from an insurer with a weak claim settlement track record is a false saving.

The premium difference between insurers on ₹1 crore cover can be ₹2,000–4,000 per year. Over a 30-year policy, that is a ₹60,000–₹1.2 lakh saving — real money, but meaningless if the claim is disputed when it matters most.

Always compare claim settlement ratios, complaint volume, and insurer solvency ratios alongside premium figures.

Skipping a Review After Major Life Events

A cover that was calculated at 31 — single income, ₹25 lakh loan — may be inadequate at 35 after a salary increase to ₹15 LPA, a second child, or a top-up loan of ₹10 lakh.

Set a calendar reminder to review cover every three to five years, and mandatorily within three months of marriage, childbirth, a new property purchase, or a significant salary change.

When This May Not Be the Right Choice

Term insurance is the right foundation for most salaried earners — but the specific cover amounts discussed here may not apply to everyone.

If you are approaching retirement with no financial dependents and your loans are nearly repaid, the case for ₹2 crore in term cover weakens significantly — your corpus likely provides adequate protection.

If your dependents — spouse, children — are already financially independent and have their own income, the income replacement need for a large cover amount reduces substantially.

If you carry significant employer-provided cover that is contractually guaranteed and portable (rare, but possible in some government roles or public sector units), that portion of your cover need may already be met.

If you have no dependents at all and your financial goals are entirely self-funded, a smaller cover with a focused critical illness rider may serve your risk exposure better than a large pure term plan. For more on employer-linked cover limitations, see our guide to employer cover and its limits.

“If any of these apply to your situation, it may be worth exploring alternatives before committing.”

Official Rules and Where to Verify

Term insurance in India is regulated and its rules — including maximum cover limits, underwriting norms, premium guidelines, and claim settlement obligations — are subject to change with each IRDAI circular or budget update.

- IRDAI (Insurance Regulatory and Development Authority of India) — irdai.gov.in — Governs all term insurance products, insurer licensing, claim settlement norms, and policyholder protection rules in India.

- Income Tax Department — incometax.gov.in — For rules on Section 80C deduction eligibility for term insurance premiums and related tax treatment.

“Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.”

Expert Tips

- Buy at 30–31, not 35–36. A five-year delay on a ₹1.5 crore policy can add ₹2,000–5,000 per year in annual premium — and that higher rate is locked in for the entire 25–30 year policy term. Buying early is the single biggest premium saving available to you.

- Choose a policy tenure that runs to at least age 60. Do not optimise for a shorter term to reduce the premium — the purpose of term insurance is to cover your peak liability years, and those typically run through age 55–60.

- Evaluate a critical illness rider at the time of purchase. A critical illness diagnosis does not result in a death benefit — but it can end your income just as surely. Adding a ₹20–25 lakh critical illness rider at purchase age is almost always cheaper than buying a standalone critical illness policy later.

- Do not mix cover amounts across one term plan and multiple smaller policies without a clear purpose. Consolidating into one or two large policies simplifies nomination, claim processing, and renewal tracking for your family.

- Declare all health conditions honestly at application — the minor premium loading for a managed condition is far less painful than a claim rejection 20 years later, when your family needs the payout most.

- Compare at least three to four IRDAI-registered insurers on claim settlement ratio, complaint ratio, and solvency margin — not just on premium. The annual premium difference between insurers matters less than the claim experience.

- Review your sum assured every time your outstanding loan balance increases significantly — a home loan top-up of ₹15 lakh should trigger a fresh needs analysis within 30 days.

Frequently Asked Questions

Is ₹1 crore term insurance enough for a ₹10 LPA salary?

For a single person with no dependents and no outstanding loans, ₹1 crore may be adequate as a starting point. For a married person with children and an active home loan, ₹1 crore typically falls short — the needs analysis method usually points to ₹1.5 crore to ₹2 crore for this income and family profile.

How do I calculate exactly how much term insurance I need?

Use the needs analysis method: start with 15x your annual income as an income replacement base, add all outstanding loan balances, add projected future education and dependent costs, then subtract your existing liquid savings and any personal term cover you already hold. The result is your required sum assured. For a detailed walkthrough, see our cover calculation guide.

What is a good annual premium for ₹1 crore term insurance at age 31?

Premiums vary significantly based on the insurer, health status, gender, smoking history, policy tenure, and current underwriting norms. Always obtain quotes from multiple IRDAI-registered insurers and compare at the time of purchase. Indicative ranges change frequently — verify current figures directly with insurers before applying.

Can I include my employer’s group term insurance in my total cover calculation?

You should not rely on employer group cover as a permanent part of your protection plan. It ends when your employment ends — and you cannot predict when that will happen. Treat it as a temporary supplement, not a structural part of your family’s financial safety net. Build your personal term plan independently of what your employer provides.

Can I get ₹2 crore term insurance if I earn ₹10 LPA?

Yes. Most insurers allow cover up to 20–25x of annual income for salaried individuals, subject to underwriting. ₹2 crore is within the normal eligible range for a ₹10 LPA earner. Actual eligibility depends on your age, health, existing insurance, and the insurer’s underwriting guidelines at the time of application.

What happens if I already have a ₹50 lakh endowment policy?

An endowment policy provides a death benefit — so ₹50 lakh of endowment cover can be subtracted from your total cover need in the needs analysis. However, endowment premiums are far higher than term premiums for the same sum assured. The question worth asking is whether those premium amounts could be better deployed in a separate term plan plus a diversified investment, rather than combined in an endowment product.

Is the premium paid on term insurance tax deductible?

Yes. Premiums paid on term insurance policies are eligible for deduction under Section 80C of the Income Tax Act, subject to the overall ₹1.5 lakh annual limit across all 80C investments. Verify current eligibility conditions and income tax regime implications at incometax.gov.in before filing.

What is the right policy tenure for someone who is 31 years old?

At 31, a policy term of 29–30 years — covering you to age 60 or 61 — is widely recommended. This ensures cover remains active through your peak loan repayment years, your children’s dependent years, and until your retirement corpus is large enough to provide financial security without insurance.

What is the claim settlement ratio and why does it matter when choosing a term plan?

The claim settlement ratio is the percentage of claims an insurer paid out of total claims received in a financial year. A higher ratio — generally above 95% — indicates an insurer that is more likely to honour a claim when your nominee files one. It matters as much as the annual premium when evaluating a term plan, because an unpaid claim defeats the entire purpose of buying insurance.

Can I buy ₹1 crore now and top up my cover later?

You can buy an additional term policy at a later date — there is no rule against holding multiple term plans from different insurers. However, premiums at 35 or 40 will be higher than at 31, and any new health conditions may affect eligibility or premium. Buying the right amount now, rather than relying on a future top-up, is the lower-risk and lower-cost approach.

Final Verdict

For a ₹10 LPA salaried earner with a family, active home loan, and young children, term insurance for 10 LPA salary should realistically start at ₹1.5 crore — and the needs analysis method will often point higher, toward ₹2 crore, once loans, education goals, and dependent income gaps are factored in. ₹1 crore satisfies the 10x income rule but leaves a significant coverage gap for most family profiles. Single earners with no dependents and minimal debt may reasonably start at ₹1 crore and review it within three years. The most important step is to run a personalised needs analysis rather than picking a round number by habit. “Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.”

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.