Switching jobs sounds straightforward until you realise your current employer requires 60 days’ notice and your new company wants you in 30. That gap — and how you fill it — is where the notice period buyout enters the picture. Most employees focus on the offer letter and assume HR will sort the rest. Then they see a deduction in their full-and-final settlement they did not plan for, or a reimbursement that arrives smaller than promised after TDS.

Notice period buyout affects your last salary credit, your first salary at the new company, the TDS both employers deduct, and ultimately what you report in your ITR. This article explains every step: who pays whom, how payroll treats it, what Form 16 shows, and what you must verify before you file.

Quick Answer: Notice Period Buyout

Notice period buyout is the amount an employee pays, or a new employer reimburses, to leave before completing the full notice period. For example, if one month’s basic salary is ₹50,000 and one month is waived, the recovery or reimbursement can affect final salary, taxable income, TDS and Form 16 reporting.

Key Takeaways

- Notice period buyout is not free money — someone always pays, and whether that is you, your old employer’s F&F deduction, or your new employer’s salary credit, each path has a different cash and tax outcome.

- Old employer notice pay recovery reduces your F&F payout; whether it also reduces your taxable salary figure in Form 16 depends on how your payroll department reports it — not on what HR told you verbally.

- New employer reimbursement is typically added to salary income and attracts TDS — ₹60,000 reimbursed gross is not ₹60,000 in your bank account.

- You will receive two Form 16s if you changed jobs mid-year. Both must be reconciled — against each other and against your AIS on the Income Tax portal — before you file ITR.

- The employment contract clause determines the salary component used for recovery (basic or gross), the notice period length, and whether buyout is permitted at all — read it before you resign.

- Get every term in writing: the last working day, the recovery amount, the reimbursement amount, the TDS treatment, and any clawback condition. Payroll processes documents, not conversations.

Key Facts at a Glance

| Factor | What It Means | What to Verify |

|---|---|---|

| Notice period buyout | Payment to waive remaining notice days — by employee, deducted in F&F, or reimbursed by new employer | Check employment contract for clause wording and permitted method |

| Old employer recovery | Salary equivalent deducted in full-and-final settlement for days not served | Check F&F statement; confirm whether recovery reduces taxable salary in Form 16 |

| New employer reimbursement | Amount paid by new employer to compensate the notice cost; typically appears in first payslip | Confirm if it is gross or net of TDS; check how it is classified in Form 16 |

| TDS impact | Both employers may deduct TDS — old employer on F&F salary, new employer on reimbursement | Compare TDS in both Form 16s with Form 26AS and AIS on incometax.gov.in |

| Form 16 reporting | Both employers issue Form 16 covering their respective employment periods; together they form your full-year salary income | Reconcile Part A (TDS) and Part B (salary) from both Form 16s before ITR filing |

| Documents to collect | F&F statement, payslips, reimbursement letter, both Form 16s, Form 26AS, AIS | Collect before ITR filing; verify on incometax.gov.in |

Each of these entries will appear somewhere in your payslip or settlement document. If you are unsure how to read them, our guide on salary slip components explains how basic, gross, deductions, and TDS connect on a typical Indian payslip.

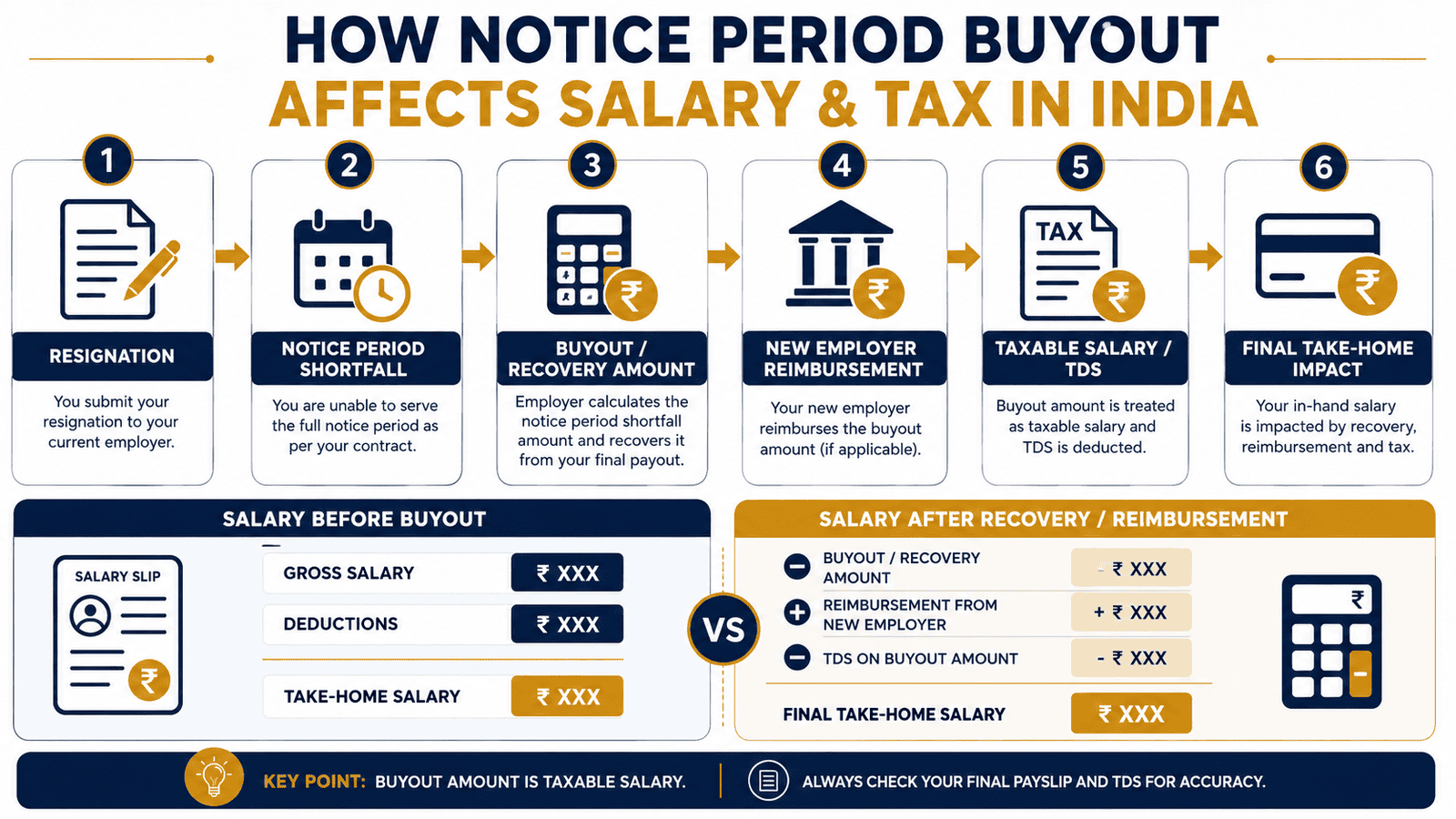

How Notice Period Buyout Works in India

Most offer letters and employment contracts in India include a clause requiring you to serve a notice period — typically 30, 60, or 90 days — before leaving. This clause gives the employer time to find and onboard a replacement. If your new company wants you to join earlier, you face a shortfall: days your current employer expects you to be present but you will not be.

Three Things That Can Happen — and They Are Not the Same

These terms are often used interchangeably in conversations with HR. They are not the same in payroll or tax terms.

- Employee-paid buyout: You pay the old employer directly — either as a separate payment before your last day, or it is deducted from your F&F settlement. The cost comes entirely from your pocket.

- Old employer notice pay recovery: The old employer deducts the shortfall equivalent from your full-and-final settlement. You do not write a separate cheque — it simply reduces the net amount you receive.

- New employer reimbursement: After joining, your new employer credits an amount equal to the recovery — often in your first payslip or as a joining benefit. This is not automatically tax-free.

Understanding how CTC and in-hand pay differ is important here — because a reimbursement that looks attractive in an offer letter may land significantly smaller in your bank account after TDS is applied.

Salary Impact: What Changes in Your F&F

Your full-and-final settlement statement from the old employer typically shows: earned salary for days worked in the last month, leave encashment (if applicable), notice pay recovery as a deduction, and net TDS. The amount credited to your account is what remains after all these entries.

What matters for income tax, however, is what the employer reports as your taxable salary — and that can differ from what you physically received. Some employers report the full salary (before recovery) as taxable income and show the recovery as a separate deduction. Others reduce the gross salary figure itself before computing TDS. This difference is exactly why two employees at the same company with the same shortfall can end up with different taxable salary figures in their Form 16.

Tax Treatment: Why It Is Not Straightforward

Under Section 15 of the Income Tax Act, salary is taxable on a “due” or “received” basis — whichever is earlier. Notice pay recovery is a payroll-level deduction, not a provision explicitly covered by a single income tax rule that defines whether it reduces taxable salary in all cases. Different employers — and different tax positions — apply different treatments.

The practical question is: did the old employer include the recovered amount in the salary figure shown in Form 16? If yes, that amount is in your taxable salary even though you did not receive it in cash. If no, the payroll team excluded it from the taxable figure before computing TDS.

The new employer reimbursement creates a parallel question. When your new employer pays you a notice period reimbursement in the context of employment, it is generally treated as salary income — regardless of whether the label on the payslip says “reimbursement,” “joining benefit,” or “notice buyout compensation.” TDS is computed accordingly. This means you may effectively pay tax on the reimbursement even though the underlying recovery reduced your old employer income.

Why Form 16 Is the Document That Decides

Form 16 from your old employer covers salary earned and TDS deducted up to your last working day. Form 16 from your new employer covers salary earned and TDS deducted from your joining date. Together, they determine the full-year taxable salary income you report in your ITR. If the old employer’s Form 16 includes the recovery amount in taxable salary, and the new employer’s Form 16 includes the reimbursement, your ITR salary income reconciliation must account for both. Discrepancies between these figures and your AIS can trigger queries from the Income Tax Department. Verify early — not at the last minute before the ITR deadline.

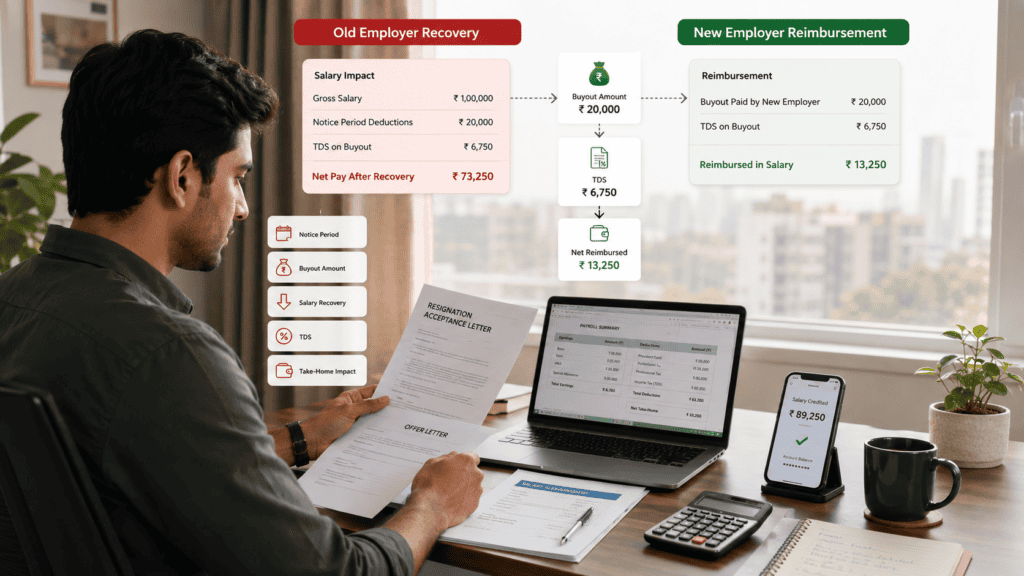

Real Example: Rohit’s Notice Period Buyout in Bengaluru

Rohit, 29, is a software engineer in Bengaluru earning ₹18 LPA CTC with a basic salary of ₹60,000 per month. His current employer requires a 60-day notice period. He receives an offer from a new company and negotiates a 30-day joining date — leaving a 30-day shortfall.

His old employer calculates recovery on basic salary: (₹60,000 ÷ 30) × 30 shortfall days = ₹60,000, deducted from his F&F settlement. His last month’s earned salary (30 days worked) is ₹60,000. After the ₹60,000 recovery and applicable TDS, the bank credit is considerably lower than Rohit had planned for.

His new employer agrees to reimburse ₹60,000 — paid in his first month’s salary. The new employer adds this to his monthly CTC for TDS computation. His first month at the new company shows a higher-than-usual salary TDS calculation because the reimbursement effectively inflates that month’s taxable salary.

At year end, Rohit receives Form 16 from both employers. He verifies that the old employer’s Form 16 reflects the actual salary paid (net of recovery) and that the new employer’s Form 16 includes the reimbursement in gross salary. He reconciles both against his AIS before filing. The key insight: the reimbursement was not tax-free — it was taxed as salary, and Rohit’s net gain from the early joining was real but smaller than the gross figures suggested.

How to Calculate Notice Period Buyout Amount

The most common formula employers use for recovery is:

Recovery Amount = (Monthly Salary Basis ÷ 30) × Shortfall Days

The salary basis can be basic salary only, or gross monthly salary — your employment contract or payroll team will confirm which applies. This distinction matters significantly: if your gross salary is ₹1,20,000 per month but basic is ₹60,000, the recovery under a gross-salary clause is double.

Rohit’s calculation:

- Monthly basic salary: ₹60,000

- Total notice period: 60 days

- Days served: 30 | Shortfall: 30 days

- Recovery = (₹60,000 ÷ 30) × 30 = ₹60,000

Use a monthly in-hand pay estimate to understand how your first month at the new company will actually look after the reimbursement is added to salary and TDS is deducted.

| Scenario | Key Inputs | Recovery Amount |

|---|---|---|

| 30-day shortfall, basic ₹60,000 | ₹60,000 ÷ 30 × 30 | ₹60,000 |

| 15-day shortfall, basic ₹75,000 | ₹75,000 ÷ 30 × 15 | ₹37,500 |

| 45-day shortfall, gross ₹1,20,000 | ₹1,20,000 ÷ 30 × 45 | ₹1,80,000 |

Comparison: Old Employer Recovery vs New Employer Reimbursement

These two events happen in sequence but are treated separately by payroll and income tax. How you understand taxable salary calculation from salary changes depending on which employer you are looking at. According to Income Tax Department guidance, salary is assessed under the head “Salaries” and includes all amounts due or received in the context of employment — the label on the payslip does not override the underlying treatment.

| Aspect | Old Employer’s Side | New Employer’s Side |

|---|---|---|

| What happens | Deducts shortfall from F&F; treatment in taxable salary varies by employer | Credits reimbursement; typically added to salary for TDS computation |

| Who bears the cost | Employee — through reduced F&F payout | New employer — but TDS reduces what employee actually receives |

| Where it appears | F&F statement; possibly in Form 16 salary figure | First payslip (reimbursement line); Form 16 Part B of new employer |

| Salary impact | Reduces cash received from F&F | Increases first month salary credit (before TDS) |

| TDS possibility | TDS on full or adjusted salary depending on payroll treatment of recovery | TDS likely deducted if reimbursement is added to salary head |

| Your required action | Get F&F breakup in writing; check Form 16 Part B for recovery treatment | Confirm in writing how reimbursement is classified; check Form 16 Part B |

How to Decide What’s Right for You

your new employer offers notice period reimbursement in writing — confirm whether the amount is gross or net of TDS before you treat it as a full offset. ₹60,000 reimbursed gross may become ₹42,000–₹48,000 after TDS depending on your tax bracket.

your new company salary is significantly higher — calculate the actual take-home gain from joining one month earlier, not just the CTC difference. Even a ₹30,000 net monthly gain over 11 months outweighs a ₹60,000 one-time recovery cost.

your old employer calculates recovery on gross salary rather than basic — the buyout amount can be 2x to 2.5x higher than you assumed. Verify the exact clause in your employment contract before you commit to an early exit date.

the new employer’s reimbursement has a clawback clause — meaning you must return it if you resign within 12 or 24 months — factor this as a financial risk, not just an HR formality, before accepting.

your old employer is willing to negotiate — a partial or full notice waiver without any cash payment is always the better outcome. Ask before assuming a buyout is the only path.

your new employer reimburses the notice period cost — the entire recovery comes from your own savings at a time when you are already managing a job transition. In this case, serving the full notice period or negotiating a longer joining date is worth reconsidering before you resign.

Common Mistakes to Avoid

Assuming the Reimbursement Is Tax-Free

Many employees hear “reimbursement” and assume it is a cost recovery that falls outside taxable income.

When a new employer pays a notice period reimbursement as part of your employment, it is generally treated as salary income and TDS is computed on it. If your monthly salary is ₹1,50,000 and ₹60,000 reimbursement is credited in the same month, TDS is computed on ₹2,10,000 for that month — noticeably higher than you may have planned for. The verbal promise of “we will cover your notice period” does not determine the tax treatment; the payslip classification does.

Ask HR to confirm in writing whether TDS will be deducted on the reimbursement before you accept the offer.

Filing ITR Without Reconciling Both Form 16s

If you changed jobs mid-year, you will receive two Form 16s. A common mistake is filing ITR based on only the new employer’s Form 16, missing the old employer’s salary income and TDS entirely.

The Income Tax portal’s AIS will include salary reported by both employers. If your ITR does not match what is in AIS, it can trigger a defective return notice or a tax demand. Reconcile Part A (TDS) and Part B (salary details) from both Form 16s before you enter any figure in your return.

Use the income tax portal at incometax.gov.in to download your AIS and Form 26AS mid-year — do not wait until filing season.

Not Collecting the F&F Statement Before Your Last Day

The full-and-final settlement statement is the only document that shows exactly what the old employer paid and deducted. If you leave without it, you will not know how the recovery was classified until Form 16 arrives months later.

You are entitled to a written F&F breakup. Request it before or on your last working day. If payroll says it will be emailed later, follow up within a week — not at ITR filing time in July.

Confusing CTC Promise With Net Cash

Offer letters sometimes describe notice period reimbursement as a “joining benefit” within the CTC structure without clarifying the after-TDS amount. ₹60,000 shown in the CTC grid is not ₹60,000 in your bank account.

Ask for the expected net-in-hand amount after TDS before you calculate whether the reimbursement truly covers your recovery. The difference can be ₹10,000–₹20,000 depending on your tax slab.

Not Checking the Notice Period Clause Before Resigning

Some employees discover only after resigning that their contract specifies 90 days, not 60. At a basic salary of ₹80,000, a 30-day miscalculation means an unexpected ₹80,000 recovery.

Read the notice period clause in your appointment letter before your resignation date. Calculate the exact shortfall in days. Do not rely on what you were told during onboarding or what a colleague experienced.

Relying on Verbal HR Approval Without a Written Record

HR may verbally agree to waive part or all of the notice period. But if it is not documented, payroll may process a full recovery in the F&F settlement regardless of what was said.

Get an email confirmation from HR — specifically the HR manager, not just a recruiter — stating the notice days waived, the agreed last working day, and the recovery amount (if any). This email is your only protection if payroll processes the F&F differently.

When This May Not Be the Right Choice

A notice period buyout is not always the right financial decision. It may not make sense if:

- Your new employer does not reimburse — the full recovery comes from your own cash at a time when you are transitioning. At ₹75,000 basic and a 45-day shortfall, that is ₹1,12,500 out of your savings.

- The reimbursement has conditions you have not read fully — clawback clauses requiring repayment if you leave within 12 or 24 months can leave you out of pocket twice if plans change.

- Your old employer uses gross salary for recovery — the buyout amount can be significantly higher than expected, and the benefit of joining a few weeks earlier may not justify it.

- The tax and cash-flow impact is still unclear — if neither payroll department has confirmed the treatment in writing and you cannot calculate the net impact, pushing your start date back by two to four weeks may be the lower-risk option.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Notice period buyout touches both employment contract law (which varies by state and sector) and income tax rules. For tax purposes, salary income — including reimbursements treated as salary — is assessed under the head “Salaries” in the Income Tax Act. TDS on salary is governed by the relevant provisions under the Act and is deducted by the employer based on estimated annual income.

Verify your specific situation using these official sources:

- Income Tax Department — incometax.gov.in: For salary tax rules, TDS on salary, Form 16 guidance, AIS, Form 26AS, and ITR filing. This is where you confirm current assessment year rules and check if your TDS is correctly credited.

- EPFO — epfindia.gov.in: For PF settlement after resignation. Your last working day affects when PF withdrawal claims can be submitted. Verify current PF withdrawal rules, especially if your notice period exit date differs from your resignation date.

Before filing your ITR, use our guide on Form 16 details to understand how to read and reconcile both employers’ documents.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before you resign, ask payroll — not just HR — three specific questions in writing: What salary component is used for recovery (basic or gross)? How will the recovery appear in Form 16? Will the reimbursement be added to salary and attract TDS? The payroll team processes numbers; HR sets expectations. They are not always aligned.

- Calculate your net monthly gain before deciding to buy out. Add up the after-TDS reimbursement you will actually receive, subtract the F&F recovery, and compare that to the incremental take-home from joining one month earlier. If the numbers do not justify the buyout, push for a later joining date.

- Download your AIS from the Income Tax portal soon after your last working day. It shows salary and TDS entries from all employers. If the old employer’s TDS entry does not appear within 30–45 days of your F&F, contact payroll — delayed TDS deposits can create mismatch issues at ITR time.

- If your reimbursement has a clawback clause, calendar it. Set a reminder for 3 months before the clawback period ends. If you are considering another job change in year 2, know exactly what you owe before you resign again.

- Reconcile both Form 16s before filing — not on filing day. Add up Part B salary figures from both documents, verify the cumulative TDS in Part A, and match against AIS. If a figure differs, contact payroll for a correction or revised Form 16 before the ITR deadline — corrections after filing are possible but require more effort.

- If you personally paid the buyout without any reimbursement, preserve the bank transfer record or payment receipt. This is relevant if payroll queries arise later, or if you consult a tax professional about your final settlement treatment.

Frequently Asked Questions

Is notice period buyout taxable in India?

The buyout or recovery amount affects the salary credited and may affect the taxable salary figure reported in Form 16, but there is no single definitive provision in the Income Tax Act that covers all situations. How the old employer’s payroll department reports the recovery — and how the new employer classifies the reimbursement — determines the actual tax treatment. Verify the treatment with payroll and check Form 16 Part B for both employers before drawing a conclusion for your specific case.

Is the reimbursement from my new employer taxable?

Generally yes. When a new employer pays a notice period reimbursement in the context of your employment, it is typically treated as part of salary income and included in gross salary for TDS computation. The fact that the old employer deducted a recovery does not automatically create an offsetting deduction at the new employer — both events are treated separately. The net result can mean you pay tax on the reimbursement even though the recovery reduced your old employer income. Verify with your new employer’s payroll team how the reimbursement is classified.

Can notice pay recovery from my old employer reduce my taxable salary?

This depends entirely on how your employer’s payroll department handles it. Some employers reduce the taxable salary figure by the recovery amount before computing TDS — in which case the recovery does not show up in taxable income. Others include the full salary in taxable income and show the recovery as a separate deduction. Form 16 Part B reflects which approach was applied. If you believe the treatment in your Form 16 is incorrect, raise it with payroll before the financial year closes — corrections after year-end are harder to process.

What happens to TDS when notice pay recovery is deducted from my F&F?

TDS on salary is computed by the employer on estimated annual income. If the F&F salary is reduced due to notice pay recovery, the TDS for that period should reflect the adjusted computation — but the exact deduction depends on how payroll treats the recovery in taxable income. Check your final payslip, your F&F statement, and compare the TDS deducted against what appears in Form 26AS and AIS on incometax.gov.in to confirm it was deposited correctly.

Where does the notice period buyout appear in Form 16?

For your old employer: the recovery may affect the gross salary figure in Form 16 Part B depending on payroll treatment. TDS deducted for that period appears in Part A. For your new employer: the reimbursement is typically included in gross salary reported in Form 16 Part B, and TDS on it shows in Part A. Together, both Form 16s must be read to understand your total taxable salary income for the year and the total TDS deposited on your behalf.

What if my old employer and new employer treat the buyout differently?

This is the most common source of confusion for employees who change jobs mid-year. If the old employer includes the recovery in taxable salary and the new employer also includes the reimbursement as salary, your combined Form 16 income may be higher than your net cash receipts. Reconcile both Form 16s against AIS before filing. If there is a genuine discrepancy — amounts that do not reflect what was actually paid or recovered — contact both payroll teams in writing and request clarification or a revised Form 16 before your ITR deadline.

Can I claim the buyout amount I personally paid as a deduction in my ITR?

There is no specific provision under the Income Tax Act that allows an employee to claim a notice period buyout paid personally as a deduction from salary income. The amount you paid personally is not recoverable through a standard tax deduction. If you received a reimbursement that was taxed as salary, you cannot separately deduct the original cost. If you believe your specific facts support a different position, consult a qualified tax professional before filing — do not assume a deduction exists without confirmation.

What happens to my PF when I leave due to a notice period buyout?

Your PF balance is not directly affected by the buyout itself — it accumulates based on your actual service. However, your last working day, as recorded by your employer with EPFO, determines when you can submit a PF withdrawal or transfer claim. Ensure your HR or payroll team records your actual last working day accurately. If there is a discrepancy in your UAN records, it can delay PF settlement. Verify current PF withdrawal rules at epfindia.gov.in.

Is it financially better to serve the notice period or buy it out?

Serving the full notice period is almost always better financially if your new employer does not reimburse the cost — you keep the salary you would otherwise lose to recovery. If the new employer reimburses and the after-TDS amount genuinely covers the recovery, buying out may make sense — especially if the salary increment at the new company is significant. Calculate the actual net take-home gain from joining one month earlier against the after-TDS reimbursement you will receive. Do not compare gross figures.

Do all employers allow a notice period buyout?

No. Whether a notice period can be bought out depends on your employment contract and company policy. Some contracts explicitly allow buyout; others require written mutual agreement; some prohibit it entirely or restrict it for senior roles or employees in critical projects. Even if buyout is technically permitted, the employer may decline based on business reasons. Read your contract clause before assuming buyout is an option, and get written HR approval before communicating a joining date to your new employer.

What documents should I keep after a notice period buyout?

Keep: (1) your old employer’s F&F settlement statement, (2) last month’s payslip from old employer, (3) written HR approval for notice period waiver or buyout, (4) new employer’s reimbursement letter or email, (5) first payslip from new employer showing reimbursement entry, (6) Form 16 from both employers, and (7) AIS and Form 26AS printouts for the relevant financial year. Retain all of these for at least one year after filing ITR — longer if you receive any query or notice.

Final Verdict

A notice period buyout can be a practical solution when you need to join a new company earlier than your current employer’s notice period allows. If the new employer reimburses the cost, the after-TDS amount covers the recovery, and the net financial gain from an earlier start justifies it — the buyout makes sense. But the cash flow and tax treatment of a notice period buyout are rarely as clean as the HR promise suggests.

Both the recovery from the old employer and the reimbursement from the new employer affect taxable salary, TDS, and Form 16. The label on the payslip does not override the income tax treatment. Verify both with payroll — in writing — before you resign and before you file ITR.

Documentation matters more than verbal confirmation at every stage here. Get the recovery amount, the reimbursement terms, the TDS treatment, and any clawback clause confirmed in writing. If you are still working through how your overall salary structure breaks down before or after the move, start with how CTC and in-hand pay connect to what you actually receive each month.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.