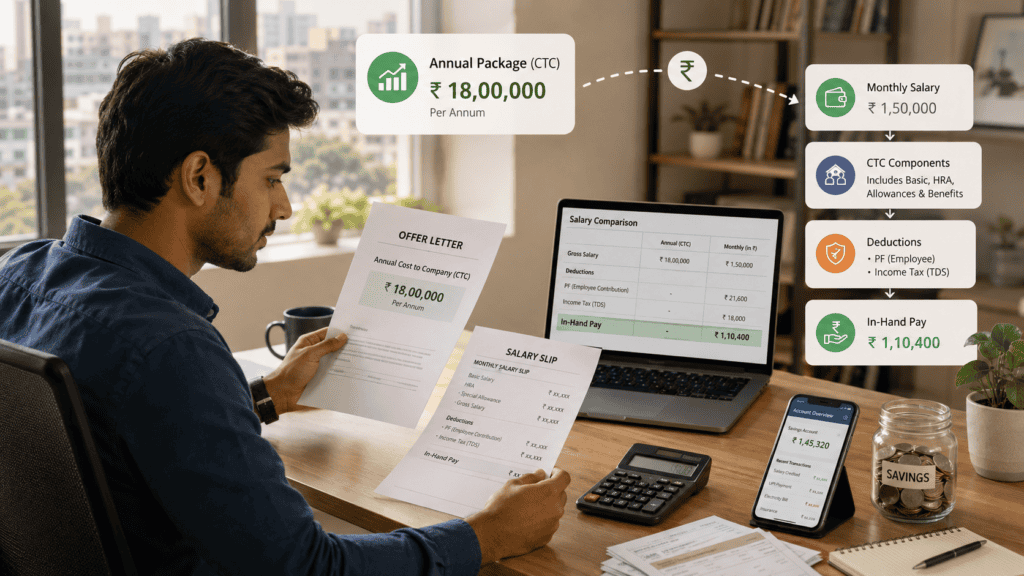

You see ₹6,00,000 on your offer letter. You divide by 12 and expect ₹50,000 in your bank account every month. Then your first salary credit arrives — and it is ₹43,000. No error, no deduction gone wrong. This is simply how annual package vs monthly salary works in India, and almost every first-time salaried employee discovers the gap the hard way.

Your employer did not shortchange you. The difference exists because your annual CTC includes costs the company bears on your behalf — employer PF, gratuity provision, insurance — that never reach your bank account as monthly cash. Then your payslip removes another set of deductions before crediting the rest. This article walks you through every layer, from the number on your offer letter to the amount your bank app actually shows, using a real ₹6 LPA example.

Quick Answer: Annual Package vs Monthly Salary

Annual package vs monthly salary means your job offer is shown as yearly CTC, while your actual monthly salary is the amount credited after deductions. For example, a ₹6,00,000 annual package may not become ₹50,000 per month because employer PF, employee PF, tax, professional tax and benefits can reduce take-home pay.

Key Takeaways

- Annual CTC is your employer’s total yearly cost — it includes contributions and benefits that never reach your bank account as monthly cash.

- A ₹6,00,000 CTC typically yields a gross monthly salary of around ₹46,000, not ₹50,000, once employer-side costs are removed.

- Employee PF at 12% of basic salary and professional tax of up to ₹200 per month (in most states that levy it) reduce your gross before your bank credit.

- Employer PF is often included inside CTC but flows to your EPFO account — it is not spendable monthly income.

- Variable pay and bonuses sit inside CTC but are paid quarterly or annually, not every month — never include them in a monthly budget.

- Always request a written monthly in-hand salary estimate from HR before accepting any job offer.

Key Facts at a Glance

| Term | What It Means | Credited to Bank Monthly? |

|---|---|---|

| Annual Package / CTC | Total yearly employer cost: cash salary plus PF, gratuity, insurance, benefits | No — yearly total, not monthly cash |

| Gross Monthly Salary | Monthly cash earnings before deductions: basic + HRA + allowances | No — deductions still apply |

| Employee PF Deduction | 12% of basic salary deducted from gross each month | No — credited to EPFO account |

| Professional Tax | State-level tax on salary; varies by state, up to ₹2,400 per year in applicable states | No — remitted to state government |

| TDS on Salary | Tax deducted at source on estimated annual income; rises with income level | No — remitted to Income Tax Department |

| Net / In-Hand Salary | Amount that lands in your bank after all deductions | Yes — this is your actual credit |

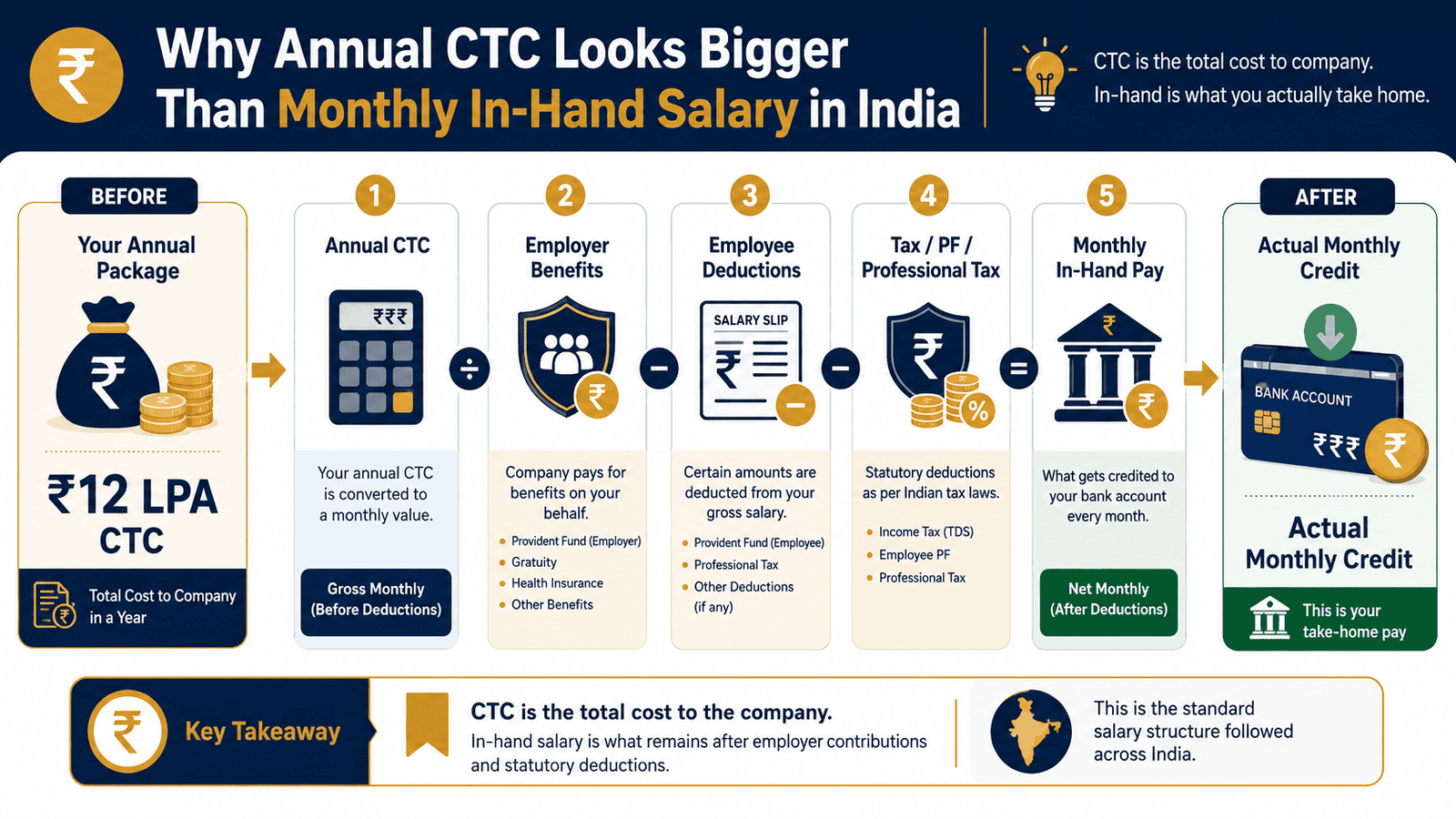

Why Annual Package vs Monthly Salary Is Not a Simple Division

Most job offers in India are quoted as annual CTC — Cost to Company. This is the total amount your employer associates with keeping you employed for one year. It includes every rupee the company spends, whether that money ever reaches your bank account or not. Your monthly in-hand salary is a different number entirely, arrived at after two separate stages of reduction.

What CTC Actually Contains

CTC is not your salary — it is your employer’s total annual expenditure on employing you. A typical private-sector CTC bundles several categories together:

- Fixed cash pay: Basic salary, HRA, special allowance, conveyance, food allowance.

- Employer-side contributions: Employer PF (12% of basic salary), gratuity provision (approximately 4.81% of basic per year), and group health insurance premium.

- Variable pay: Performance bonus or incentive component, usually paid quarterly or annually.

- Other benefits: Meal vouchers, company car benefit, telephone reimbursement — valued and added to the CTC total.

Employer PF, gratuity, and insurance are real costs for the company. But they do not arrive in your bank every month. Employer PF goes to your EPFO account. Group insurance protects you but delivers no monthly cash. Gratuity is paid as a lump sum only when you leave after completing five or more years of service. Understanding CTC and in-hand pay as genuinely separate numbers is the foundation of reading any offer letter correctly.

Gross Salary: What You Actually Earn in Cash Each Month

Once you strip out employer-side non-cash costs from monthly CTC, what remains is your gross salary. This is the earnings total shown on your payslip — basic salary + HRA + allowances — before any deductions are applied.

For a ₹6,00,000 CTC, if the employer PF, gratuity provision, and group insurance together amount to ₹4,000 per month, your monthly gross salary is ₹46,000 — not ₹50,000. That ₹4,000 gap is money the company spent on you that never passed through your hands. This is the first reason the bank credit is lower than CTC divided by 12.

What Happens After Gross Salary

Gross salary is still not your take-home pay. Your employer applies three further deductions before crediting your account:

Employee PF contribution: Under EPFO rules, employees contribute 12% of basic salary to their provident fund each month. On a basic salary of ₹20,000, that is ₹2,400 per month — deducted from gross before you receive anything. This money goes to your EPFO account, accessible at retirement or under specific withdrawal rules.

Professional tax: This is a state government tax on salaried employees. Not all states levy it, and the rate varies where it does exist. In Maharashtra, employees earning above ₹10,000 per month pay ₹200 per month in professional tax. In Karnataka, the slab structure is different. Your deduction depends entirely on which state you work in.

TDS on salary: Your employer deducts tax at source each month based on your estimated annual income and chosen tax regime. At lower income levels — such as ₹6 LPA with a standard deduction applied — TDS may be zero under the new tax regime. As income rises, TDS becomes a meaningful monthly deduction that can run into several thousand rupees.

After all three, what is left is your net salary — the amount credited to your bank. This is the number to use for rent, EMI, groceries, and savings planning. Nothing else is usable monthly cash.

Fixed Pay and Variable Pay: Not the Same Thing

Many CTC structures include a variable pay component — a performance-linked amount typically paid quarterly, half-yearly, or annually. If your ₹6,00,000 CTC includes ₹60,000 of variable pay, your guaranteed monthly fixed cash is based on the remaining ₹5,40,000 only. The variable portion arrives in lump sums when targets are met and the company releases it. Treating variable pay as a predictable monthly salary is one of the most expensive mistakes a first-time employee can make.

Real Example: Rohit’s First Salary Surprise in Pune

Rohit, 25, has just joined his first job as a junior software developer in Pune. His offer letter says ₹6,00,000 per annum. He expects ₹50,000 credited every month. Before joining, HR sends him a salary breakup sheet:

| Component | Monthly (₹) | Reaches Bank Account? |

|---|---|---|

| Basic Salary | 20,000 | Yes (part of gross) |

| House Rent Allowance (HRA) | 10,000 | Yes (part of gross) |

| Special Allowance | 16,000 | Yes (part of gross) |

| Gross Monthly Salary | 46,000 | Before deductions |

| Employer PF (12% of basic) | 2,400 | No — goes to EPFO account |

| Gratuity Provision (~4.81% of basic) | 962 | No — paid at exit after 5 years |

| Group Health Insurance | 638 | No — benefit, not cash |

| Total Monthly CTC | 50,000 | — |

Rohit’s payslip then deducts from his gross of ₹46,000: employee PF of ₹2,400, professional tax of ₹200 (Maharashtra), and TDS of ₹0 (his income falls below the taxable threshold after standard deduction under the new tax regime). Total deductions: ₹2,600.

His monthly in-hand salary: ₹43,400. Not ₹50,000 — and not because of any error. This is salary structure working exactly as designed. Understanding how basic salary impact ripples through PF, HRA, and gratuity helps Rohit see why restructuring basic salary can shift his take-home meaningfully.

How to Calculate Monthly In-Hand Salary from Annual CTC

There is no single universal formula because salary structures vary by employer. But this five-step method gives a reliable working estimate:

Monthly In-Hand ≈ (Annual Fixed Cash CTC ÷ 12) − Employee PF − Professional Tax − TDS

Step 1 — Start with annual CTC. Use the total from your offer letter. For Rohit: ₹6,00,000.

Step 2 — Remove employer-side non-cash costs. Ask HR what portion is employer PF, gratuity, and insurance. For Rohit: ₹2,400 + ₹962 + ₹638 = ₹4,000 per month, or ₹48,000 per year. Fixed cash CTC: ₹5,52,000.

Step 3 — Divide by 12. ₹5,52,000 ÷ 12 = ₹46,000 monthly gross salary.

Step 4 — Subtract employee PF and professional tax. Employee PF = 12% of basic = ₹2,400. Professional tax = ₹200 (Maharashtra). Total: ₹2,600.

Step 5 — Subtract estimated TDS. At ₹6 LPA with a standard deduction applied, TDS is often ₹0 under the new tax regime. This changes as income rises above the taxable threshold.

Result: ₹46,000 − ₹2,600 = ₹43,400 per month in-hand.

Numbers for your own CTC will differ based on your employer’s structure, state, variable pay split, and tax regime. Run it through our actual take-home pay calculator to get a figure tailored to your package in seconds.

| Scenario | Annual CTC | Estimated Monthly In-Hand (Indicative) |

|---|---|---|

| Junior employee, basic ~40% of gross, no variable | ₹6,00,000 | ₹42,000–₹44,500 |

| Mid-level employee, basic ~45% of gross, 10% variable | ₹10,00,000 | ₹66,000–₹72,000 |

| Senior employee, basic ~50% of gross, 20% variable | ₹15,00,000 | ₹88,000–₹97,000 |

These ranges are illustrative. Actual in-hand depends on employer structure, state of employment, tax regime chosen, and applicable deductions.

Comparison: Annual Package vs Gross Salary vs Net Salary vs In-Hand

Four salary terms, four different numbers — and each one is useful for a different purpose:

| Salary Term | What It Is | Use It For |

|---|---|---|

| Annual Package / CTC | Total employer cost per year: cash salary + PF + gratuity + insurance + benefits | Comparing offers at a headline level; market benchmarking |

| Monthly Gross Salary | Cash earnings per month before deductions: basic + HRA + allowances | Understanding your earnings structure; checking payslip |

| Monthly Net Salary | Gross minus employee PF, professional tax, TDS | Tax filing; verifying payslip accuracy |

| Monthly In-Hand / Take-Home | Amount credited to your bank account each month | Budgeting, rent, EMI planning, savings decisions |

CTC is a negotiation number. In-hand is a living number. Never use CTC to plan rent or EMIs — the gap can easily be ₹6,000–₹15,000 per month depending on package size and structure. For a clear walkthrough of how these layers interact with real examples, read our guide on gross and net salary.

How to Decide What’s Right for You

When evaluating a job offer, salary hike, or monthly budget, use these if/then statements to make the right call:

you have received an offer letter showing a CTC but no salary breakup — THEN ask HR for a component-wise structure before accepting. A ₹10 LPA offer with 25% variable pay and employer PF inside CTC can deliver a lower fixed monthly credit than a ₹8.5 LPA offer with 100% fixed pay and employer PF outside CTC.

you are comparing two job offers — THEN compare fixed monthly in-hand, not headline CTC. Two identical ₹12 LPA offers can have meaningfully different take-home amounts depending on how basic salary is set and how much variable pay is included.

you are planning monthly rent, an EMI, or a SIP amount — THEN base it on your confirmed net in-hand salary only. CTC divided by 12 will overstate your usable monthly income by ₹5,000 or more in most cases.

your CTC includes a variable component of 15% or more — THEN build your entire monthly budget on the fixed in-hand only. Treat variable pay as a bonus when it arrives. It is performance-linked and not guaranteed every month.

you just joined a new job — THEN compare your first three payslips against the offer letter breakup carefully. Payroll setup errors — wrong basic salary entry, incorrect PF rate, wrong tax regime selected — are most common in the first quarter.

you have received a written salary breakup showing fixed gross and estimated in-hand — THEN do not sign the offer or begin any monthly financial commitment based on CTC alone. A verbal promise of “approximately ₹X in-hand” is not a reliable planning figure.

Common Mistakes to Avoid

Dividing CTC by 12 and Treating It as Take-Home Pay

The most widespread mistake among first-time employees: ₹6,00,000 ÷ 12 = ₹50,000, so the bank credit must be ₹50,000.

CTC includes employer PF, gratuity, insurance, and other costs that never pass through your bank. On a ₹6 LPA package, the gap between CTC/12 and actual bank credit can be ₹6,000–₹8,000 per month — a difference of ₹72,000–₹96,000 in real spending power across a year. Planning a rent or EMI on this assumption can create serious cash flow pressure.

Ask HR for a gross-to-net salary simulation before accepting any offer. A reputable employer will provide it without hesitation.

Counting Employer PF as Your Monthly Income

Employer PF appears in the CTC breakdown and looks like money coming to you. It is not.

Employer PF goes directly to your EPFO account — inaccessible as monthly spending money. If your monthly CTC is ₹50,000 and includes ₹2,400 in employer PF, your gross cash salary is ₹47,600 or lower, not ₹50,000. Including employer PF in a monthly budget calculation will leave you short every single month.

Identify the employer-side PF figure on your offer letter breakup and exclude it from any monthly cash calculation.

Treating Variable Pay as Guaranteed Monthly Salary

If your CTC includes ₹60,000 in annual variable pay, some employees mentally convert that to ₹5,000 per month and spend accordingly.

Variable pay arrives in lump sums — quarterly, half-yearly, or annually — and only when performance targets are achieved. If targets are missed, part or all of it may not be paid. Your guaranteed fixed monthly income is based only on the fixed component of CTC.

Budget exclusively on fixed in-hand. When variable pay arrives, treat it as a windfall — not salary.

Forgetting Professional Tax When Moving States

Professional tax is levied in Maharashtra, Karnataka, West Bengal, Tamil Nadu, and several other states — but not all. If you move from a non-PT state to a PT state for a job, your monthly take-home will be lower than expected.

In Maharashtra, the monthly deduction is ₹200 for employees earning above ₹10,000. Small but consistent — ₹2,400 per year leaving your account that you did not plan for.

Check the professional tax rules of your specific work state before budgeting after any relocation or job change.

Ignoring TDS as Income Grows

At ₹6 LPA, TDS may be zero. But by ₹10 LPA or ₹12 LPA, monthly TDS can run to several thousand rupees depending on investments, HRA claims, and the tax regime chosen.

Employees who plan expenses based on gross salary without accounting for rising TDS can face a cash flow squeeze mid-year, especially if they switch jobs and the new employer recalculates TDS on the full-year estimated income.

Ask your payroll team for an annual TDS projection when you join. Revisit it every April when the new financial year begins.

Never Reading the Salary Slip After Joining

Many first-time employees look only at the final bank credit and ignore the full payslip.

Payroll setup errors are not uncommon — wrong basic salary, incorrect PF deduction, wrong tax regime applied. Each error compounds month after month until someone catches it. A PF deduction error of ₹500 per month means ₹6,000 over a year — lost quietly.

Read your full salary slip components every month. Verify gross, every deduction, and net against your offer letter. It takes two minutes and can catch errors before they accumulate.

When This May Not Be the Right Choice

The standard CTC-to-in-hand logic works cleanly for conventional salaried roles in the private sector. But it may not apply neatly in these situations:

Sales and commission-heavy roles: If a significant portion of your “package” is commission or incentive-linked, there is no reliable fixed monthly in-hand. Your earnings will swing month to month based on targets and payouts — the standard CTC calculation does not capture this.

Startups offering ESOPs or large joining bonuses: Employee stock options are often included in CTC valuations but are not spendable until vesting conditions are met and you actually sell the shares. A joining bonus is a one-time credit, not a recurring monthly component. Both can inflate the headline CTC figure significantly.

Contract or gig roles without employment benefits: Contractors may not have EPF, professional tax treatment, or employer-side benefits included in their billing rate. A ₹6 LPA contract role and a ₹6 LPA permanent role are not financially equivalent.

Government and PSU jobs: Central and state government salary structures follow a pay matrix system with Dearness Allowance, HRA rules, and pension-related deductions that differ substantially from private-sector CTC frameworks. The CTC concept itself is less directly applicable here.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Salary deduction rules, PF contribution rates, and tax treatment are governed by official regulations that can change with each Budget or policy update. Always verify current figures directly from the relevant authority:

- EPFO — epfindia.gov.in: Employee and employer PF contribution rates, EPFO passbook, withdrawal and transfer rules, and any changes to the contribution structure.

- Income Tax Department — incometax.gov.in: TDS on salary, tax slab rates under the old and new tax regimes, standard deduction limits, and Form 16 details.

- Your state government’s commercial tax or labour department: Professional tax slabs and income thresholds applicable in your specific state — there is no central rate; it varies by state.

- Your employer’s HR and payroll team: Your specific salary breakup, variable pay policy, benefits valuation, and monthly payslip clarifications.

For a detailed explanation of how employer PF contribution is structured — and how it differs from employee PF — read our dedicated guide.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before signing any offer, ask HR for a month-by-month salary simulation in writing. Request a document showing gross salary, all deductions, and estimated net in-hand. This one ask prevents months of budget confusion after joining and is entirely reasonable to make of any formal employer.

- Negotiate on fixed gross or fixed cash CTC — not total CTC. Employers can inflate CTC with low-cost benefits and employer-side contributions. Anchoring your negotiation on fixed monthly cash gives you a clearer picture of what you are actually getting.

- Ask explicitly whether employer PF is inside or outside your quoted CTC. Some employers quote CTC excluding employer PF — your true CTC is higher in that case. Others include it, which compresses your gross cash component. This single question can shift your monthly in-hand estimate by ₹2,000–₹5,000.

- Build your monthly budget on 80–85% of your in-hand if your CTC has a significant variable component. A 15% variable pay structure means 15% of your package is not guaranteed monthly cash. Budget only on what you know you will receive every month.

- Verify your first three payslips against the offer letter carefully. Payroll setup errors are most common in the first quarter after joining — wrong basic salary, incorrect tax regime selection, PF deduction on the wrong base. Catch them early before they compound into a refund or deficit situation at year-end.

- Check whether your employer is applying your HRA exemption correctly. If you pay rent and your salary includes HRA, your employer should factor in HRA exemption when computing monthly TDS. If they are not, you may be overpaying tax each month and reclaiming it only at ITR filing — a cash flow delay you can avoid by submitting your rent proofs to HR promptly.

Frequently Asked Questions

Is annual package the same as CTC?

Yes — in Indian employment usage, annual package and CTC (Cost to Company) refer to the same number. It is the total yearly cost an employer incurs to employ you, covering cash salary, employer PF, gratuity provision, group insurance, and any other benefits included in your offer letter. The terms are used interchangeably across most companies and HR communications.

Is monthly salary the same as in-hand salary?

Not necessarily. “Monthly salary” can refer to either gross monthly salary (your total cash earnings before deductions) or net monthly salary (after deductions). In-hand salary — also called take-home salary — is specifically the amount credited to your bank account after employee PF, professional tax, and TDS have been deducted. Always clarify which number you are being quoted, especially during job offer discussions.

Why is CTC higher than in-hand salary?

CTC includes employer-side costs that never reach your bank account — employer PF, gratuity provision, and group insurance premium. These are real expenses for the company on your behalf, but they flow to your EPFO account, to a gratuity fund, or to an insurer. Your payslip then deducts employee PF, professional tax, and TDS from the remaining gross salary. The combined effect can leave your in-hand salary ₹6,000–₹15,000 lower per month than CTC divided by 12.

Is employer PF deducted from my monthly salary?

No — employer PF is contributed by your employer on top of your gross salary and goes to your EPFO account. However, when employer PF is included inside the CTC figure, it reduces the gross cash component of your package. So it is not deducted from your bank credit — but its inclusion in CTC means your gross salary is lower than CTC implies. Separately, employee PF (also 12% of basic) is deducted from your gross salary before your bank credit each month.

What is the difference between gross salary and net salary?

Gross salary is your total monthly cash earnings before any deductions — basic salary, HRA, and all allowances added together. Net salary is what remains after subtracting employee PF, professional tax, and TDS from gross. Net salary is effectively the same as your in-hand or take-home pay — the amount that actually enters your bank account.

How do I calculate take-home salary from CTC?

Remove the employer-side costs — employer PF, gratuity provision, insurance — from monthly CTC to get gross salary. Then subtract employee PF at 12% of basic salary, professional tax at the applicable rate for your state, and estimated TDS based on your income and tax regime. The result is your estimated net in-hand. Because salary structures vary, use our take-home calculator for a faster and more accurate result based on your specific inputs.

Should I compare job offers by CTC or in-hand salary?

Compare by fixed monthly in-hand salary, not CTC. Two offers with identical CTC figures can produce meaningfully different take-home amounts depending on how basic salary is set, how much variable pay is included, and whether employer PF is inside or outside the CTC. Request a gross-to-net salary simulation from each employer before making your comparison. CTC is a headline — in-hand is the reality.

Is variable pay included in my monthly salary?

Variable pay is included in your annual CTC, but it is not typically paid monthly. It is disbursed quarterly, half-yearly, or annually — and only when performance targets are achieved. If targets are missed or partially met, you may receive less than the full variable component. Never include variable pay in your monthly budget. Treat it as a bonus when it is actually credited.

Can I negotiate my salary structure, not just the total CTC?

Yes — and it is worth doing. You can request a higher basic salary (which raises your PF contributions, HRA exemption, and eventual gratuity), ask to convert variable pay into fixed pay for more predictable income, or request that employer PF be placed outside the CTC so your gross cash component is higher. Many employers allow structure adjustments, particularly for mid-level and senior roles. Frame the request around monthly in-hand clarity, not just a higher number.

What happens if my employer does not deduct professional tax in a state that charges it?

If your employer operates in a state that levies professional tax but does not deduct it from your payslip, the liability may fall on you or on the employer depending on the state’s specific rules. For most formal employers with payroll software, this is handled automatically. If you notice professional tax is absent from your payslip while working in a state that charges it — Maharashtra, Karnataka, West Bengal, Tamil Nadu, for example — flag it with your HR or payroll team promptly.

Final Verdict

The gap between annual package vs monthly salary is not a mystery once you see the structure clearly. CTC is your employer’s total cost — it includes PF, gratuity, insurance, and benefits that serve you but never land in your bank account every month. Your actual take-home is what remains after those employer-side costs are removed and employee-side deductions — PF, professional tax, TDS — are applied to the gross.

For market benchmarking and offer comparisons, the annual CTC number is useful. For rent, EMI, SIP, and every real financial decision in your life, only your fixed monthly in-hand salary counts. A ₹6 LPA offer that credits ₹43,400 per month and a ₹7 LPA offer that credits ₹47,500 are not as far apart as the headline gap suggests — and a ₹8 LPA offer with 30% variable can actually put less in your bank each month than a ₹7 LPA fully fixed package.

Before accepting any offer, ask for a full written salary breakup and a net monthly in-hand estimate. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.