If you earn ₹15 LPA and your employer asks you to declare a tax regime before April, you are making a decision that affects TDS deductions every month for the entire financial year — and getting it wrong can mean either excess deductions or a surprise shortfall at filing time. The question of tax saving for 15 LPA salary has no universal answer. It depends on whether you pay rent, how much you invest in 80C, whether you have health insurance, whether your employer contributes to NPS, and how your salary is structured. This article compares both regimes using FY 2025-26 (AY 2026-27) rules, with a worked example, a step-by-step calculation, and a clear decision framework — so you can enter your own numbers into the official calculator before committing to a regime.

Quick Answer: Tax Saving for 15 LPA Salary

Tax saving for 15 LPA salary depends on your eligible deductions, HRA, NPS and standard deduction. A ₹15 lakh salaried employee should compare old and new regime tax after reducing ₹75,000 standard deduction and all valid old-regime deductions before choosing.

Key Takeaways

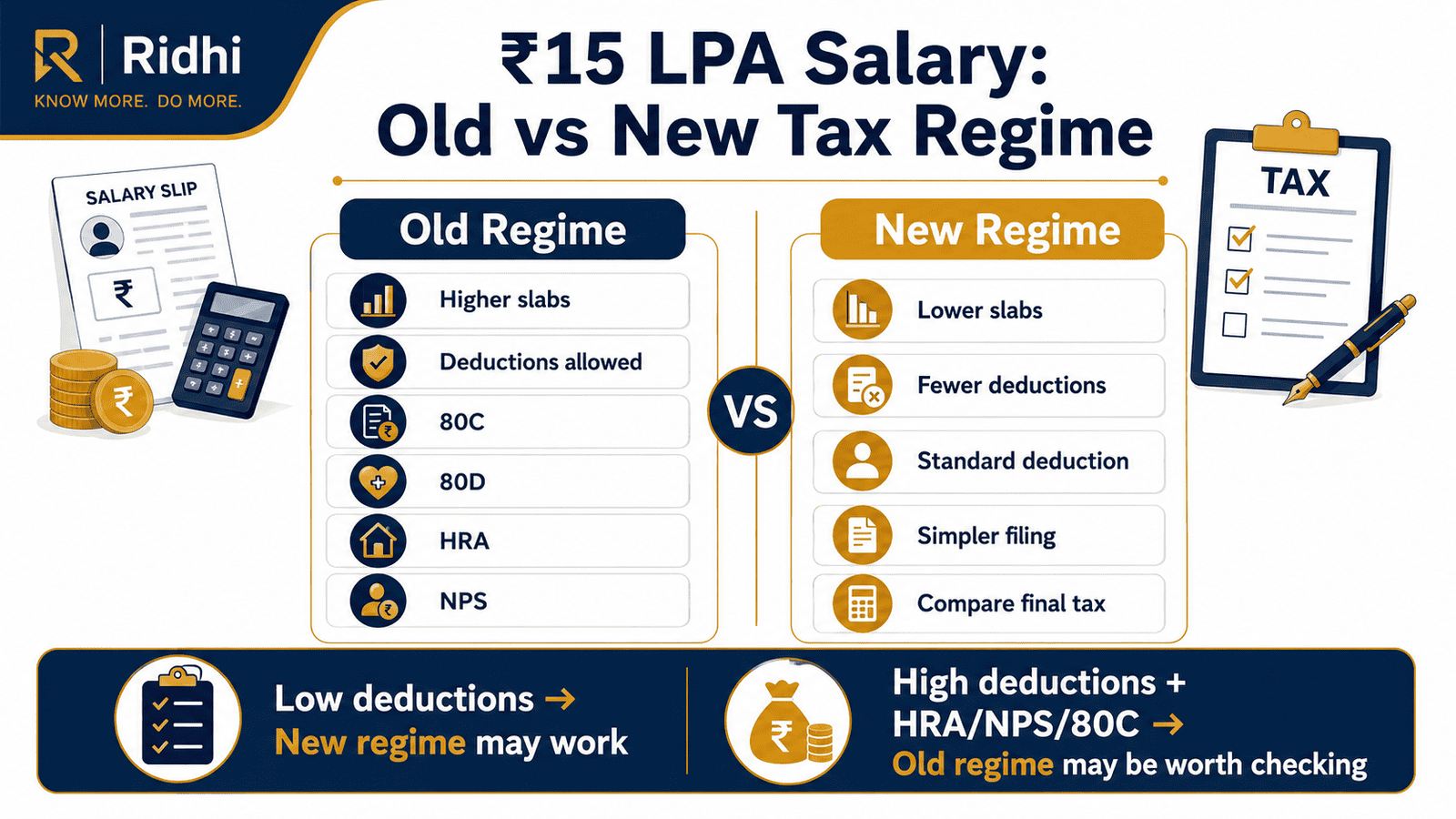

- At ₹15 LPA, the new tax regime for FY 2025-26 gives salaried employees a ₹75,000 standard deduction and applies significantly lower slab rates — making it the default starting point for comparison, not a fallback option.

- The old regime allows ₹50,000 standard deduction but opens up 80C (up to ₹1,50,000), Section 80D, HRA exemption under Section 10(13A), and NPS deduction under 80CCD(1B) — all of which can substantially reduce taxable income.

- In a typical metro-city scenario with moderate rent, maxed 80C, ₹25,000 health insurance, and NPS, the new regime still saves more tax at ₹15 LPA — the old regime must produce very high combined deductions to beat it.

- The old regime can outperform the new regime at ₹15 LPA only when total old-regime deductions (beyond standard deduction) reach approximately ₹5–6 lakh, which typically requires substantial HRA from a metro city combined with maxed 80C, 80D for self and parents, and NPS.

- TDS deducted by your employer is a provisional calculation based on your declaration — your final tax liability is settled only when you file your ITR with verified figures.

- Your regime choice at employer declaration can generally be revisited before filing your ITR for that financial year, giving you a second opportunity to compare both sides with actual deduction figures.

- Tax slabs, standard deduction amounts, rebate limits, and deduction caps for AY 2026-27 must be verified directly at incometax.gov.in before filing — these figures can change with every Budget.

Comparison: Old Tax Regime vs New Tax Regime for ₹15 LPA

| Parameter | Old Tax Regime | New Tax Regime |

|---|---|---|

| Standard Deduction (Salaried) | ₹50,000 | ₹75,000 |

| Section 80C (up to ₹1,50,000) | Allowed | Not Allowed |

| Section 80D (Health Insurance) | Allowed | Not Allowed |

| HRA Exemption — Section 10(13A) | Allowed | Not Allowed |

| NPS Self-Contribution — 80CCD(1B) | Allowed (up to ₹50,000) | Not Allowed |

| Home Loan Interest — Section 24(b) | Allowed (up to ₹2,00,000) | Not Allowed |

| Tax Slab Structure | 0% / 5% / 20% / 30% | 0% / 5% / 10% / 15% / 20% / 25% / 30% |

| Best Fit at ₹15 LPA | High deductions + substantial HRA | Low or moderate deductions; simplicity needed |

For a full breakdown of every old-regime deduction and how each works, see our guide on old regime deductions.

Key Facts at a Glance

| Item | Detail | Verification Note |

|---|---|---|

| Financial Year / Assessment Year | FY 2025-26 / AY 2026-27 | Confirm rules are current before filing |

| Gross Salary Assumed | ₹15,00,000 per annum | CTC may differ from gross taxable salary |

| Standard Deduction — New Regime | ₹75,000 | Verify current amount at incometax.gov.in |

| Standard Deduction — Old Regime | ₹50,000 | Verify current amount at incometax.gov.in |

| Section 80C Limit | ₹1,50,000 per year | Old regime only; verify current cap |

| Additional NPS Deduction — 80CCD(1B) | Up to ₹50,000 extra (over 80C) | Old regime self-contribution only |

The salary standard deduction applies to salaried employees under both regimes for FY 2025-26 — the allowed amounts differ between the two.

How Old and New Tax Regimes Work for a ₹15 LPA Salary

Two Approaches to Taxable Income

The old and new regimes are not simply different tax rate tables — they represent fundamentally different methods of calculating what portion of your salary is taxable. The old regime lets you reduce your gross salary through deductions and exemptions before applying tax. The new regime governed by Section 115BAC removes most of those deductions but applies lower slab rates at every income bracket, keeping the calculation straightforward.

At ₹15 LPA, this trade-off is real and the numbers are genuinely close. The new regime’s lower slabs can produce a smaller tax bill even without any deduction beyond the standard deduction. Whether the old regime can beat that depends entirely on how many deductions you are genuinely eligible for — and whether you have the documentation to support each claim when it matters.

Why ₹15 LPA Is a Critical Comparison Point

For FY 2025-26, salaried employees with taxable income up to ₹12,00,000 under the new regime may owe zero tax due to the Section 87A rebate — giving an effective threshold of approximately ₹12,75,000 after standard deduction. At ₹15 LPA, you are clearly above this threshold under both regimes, making the comparison genuinely consequential. Small differences in how you structure deductions can shift your tax bill by thousands of rupees.

The choice at ₹15 LPA is also more nuanced than at lower income levels because you may land in the 30% marginal slab under the old regime — meaning the benefit of each rupee of deduction is higher, but the new regime’s lower slab structure may still counterbalance it. For a broader perspective on how this choice works across income levels, see our full guide on old vs new choice for salaried employees.

CTC Is Not the Same as Taxable Salary

This distinction trips up a large number of salaried employees during regime comparisons. Your CTC includes components that are either non-taxable or taxed differently — employer’s PF contribution, gratuity provisions, leave travel allowance in certain cases, and reimbursements. Your actual gross salary for tax calculation purposes is typically lower than your CTC figure. If your salary structure includes an HRA component and you pay rent, the HRA exemption further reduces your taxable salary under the old regime.

This is why two people at the same ₹15 LPA CTC can have materially different final tax liabilities. The starting point for any meaningful comparison must be your actual gross salary — not your CTC. Your Form 16 Part B, once issued by your employer, shows the taxable gross figure as reported to the Income Tax Department.

Old Regime Deductions That Matter Most at ₹15 LPA

Under the old regime, the deductions that typically have the largest impact at this salary level are Section 80C (up to ₹1,50,000) covering EPF, PPF, ELSS, LIC premiums, and home loan principal repayment; Section 80D for health insurance premiums (₹25,000 for self and family, an additional ₹25,000 for parents, or ₹50,000 if parents are senior citizens); HRA exemption under Section 10(13A) for employees who pay rent in a metro city with a structured HRA component; and Section 80CCD(1B) for NPS self-contributions up to ₹50,000 above the 80C limit.

These deductions can collectively reduce old-regime taxable income by ₹3–6 lakh depending on your actual situation. Whether that saving beats what the new regime’s lower slabs already deliver at ₹15 LPA is answered directly in the calculation section below.

New Regime: What You Give Up and What You Gain

Under the new regime (Section 115BAC), you cannot claim most deductions — no 80C, no 80D, no HRA, no NPS self-contribution. In exchange, you face lower slab rates at every bracket. For FY 2025-26, the new regime introduces more granular slabs than the old regime, with each bracket taxed at a lower marginal rate than the corresponding old-regime bracket for most income ranges up to ₹15 LPA. The result: even modest income levels are taxed less per rupee under the new regime than under the old.

For employees with no home loan, no significant rent commitment, or employers who do not structure salaries around HRA, the simplicity of the new regime translates directly into lower tax — with no investment decisions, no document collection, and no year-end scramble.

Real Example: Ankit, 31, Bengaluru — Software Engineer at ₹15 LPA

Ankit works at a mid-size tech firm in Bengaluru. His annual CTC is ₹15,00,000. His salary structure includes a basic of ₹6,00,000 per year and an HRA component of ₹3,00,000 per year. He pays ₹20,000 per month in rent. His only income source is salary — no capital gains, no business income, no RSUs vested during the year.

His eligible old-regime deductions: EPF contribution (80C) ₹72,000 plus ELSS SIP ₹78,000 — total 80C ₹1,50,000; health insurance premium for self and spouse ₹25,000 under Section 80D; NPS self-contribution via payroll ₹50,000 under Section 80CCD(1B); HRA exemption calculated as the lowest of HRA received (₹3,00,000), rent paid minus 10% of basic (₹2,40,000 minus ₹60,000 = ₹1,80,000), and 50% of basic for metro city (₹3,00,000) — giving an exemption of ₹1,80,000.

Ankit’s scenario is illustrative — actual results change with rent amount, variable pay, employer PF structure, and investment choices. For a direct tax figure based on a ₹15 LPA salary structure, see the 15 lakh salary tax breakdown. The key insight from his example: regime selection is not decided by how many deductions Ankit knows about, but by how many he can claim with valid documentation.

How to Calculate Tax on ₹15 LPA: Old vs New Regime

The calculations below use Ankit’s scenario and FY 2025-26 rules as understood at the time of writing. Verify all slabs, deduction limits, cess, and rebate rules at incometax.gov.in before filing for AY 2026-27.

New Regime Taxable Income = Gross Salary − Standard Deduction (₹75,000)

Ankit’s new regime taxable income: ₹15,00,000 − ₹75,000 = ₹14,25,000

New regime tax on ₹14,25,000 (FY 2025-26 slabs):

- ₹0 to ₹4,00,000: Nil

- ₹4,00,001 to ₹8,00,000: 5% on ₹4,00,000 = ₹20,000

- ₹8,00,001 to ₹12,00,000: 10% on ₹4,00,000 = ₹40,000

- ₹12,00,001 to ₹14,25,000: 15% on ₹2,25,000 = ₹33,750

- Tax before cess: ₹93,750 | Add 4% Health and Education Cess: ₹3,750

- Total new regime tax: ₹97,500

Old Regime Taxable Income = Gross Salary − Standard Deduction (₹50,000) − HRA Exemption − 80C − 80D − 80CCD(1B)

Ankit’s old regime taxable income: ₹15,00,000 − ₹50,000 − ₹1,80,000 − ₹1,50,000 − ₹25,000 − ₹50,000 = ₹10,45,000

Old regime tax on ₹10,45,000:

- ₹0 to ₹2,50,000: Nil

- ₹2,50,001 to ₹5,00,000: 5% on ₹2,50,000 = ₹12,500

- ₹5,00,001 to ₹10,00,000: 20% on ₹5,00,000 = ₹1,00,000

- ₹10,00,001 to ₹10,45,000: 30% on ₹45,000 = ₹13,500

- Tax before cess: ₹1,26,000 | Add 4% Health and Education Cess: ₹5,040

- Total old regime tax (moderate deductions): ₹1,31,040

| Scenario | Key Assumptions | Total Tax (with 4% cess) |

|---|---|---|

| New Regime | ₹75,000 standard deduction only; no other deductions | ₹97,500 |

| Old Regime — Moderate Deductions | ₹50K std + ₹1.8L HRA + ₹1.5L 80C + ₹25K 80D + ₹50K NPS | ₹1,31,040 |

| Old Regime — High Deductions | ₹50K std + ₹3L HRA + ₹1.5L 80C + ₹50K 80D (parents included) + ₹50K NPS | ₹96,200 |

The third row shows that the old regime can edge out the new regime at ₹15 LPA — but only when HRA exemption is at its maximum (full ₹3 lakh), 80D covers parents, and all other deductions are maxed. At moderate deduction levels, the new regime wins by ₹33,540. Use the income tax calculator with your own deduction figures to find your personal break-even point.

How to Decide What’s Right for You

You pay less than ₹15,000 per month in rent or no rent at all — THEN the new regime is almost certainly better at ₹15 LPA; without significant HRA, your combined old-regime deductions are unlikely to overcome the new regime’s slab advantage.

You pay ₹28,000 or more per month in rent in a metro city, have maxed 80C, hold health insurance for yourself and your parents, and contribute to NPS — THEN run both calculations carefully; the old regime may save ₹1,000–₹5,000 more depending on your exact HRA structure and basic salary ratio.

You have 80C investments of ₹1,50,000 but no HRA (living in your own home or with family) — THEN the new regime very likely produces lower tax at ₹15 LPA even though 80C is unavailable under it; the new-regime slab benefit at this income level outweighs a single deduction.

You have a home loan with annual interest above ₹1,50,000 — THEN factor Section 24(b) interest deduction into your old-regime calculation separately; this is one of the larger missed deductions at ₹15 LPA and can shift the comparison meaningfully.

Your employer contributes to NPS on your behalf under Section 80CCD(2) — THEN check whether that deduction is available to you under the new regime as well; employer NPS contributions have different rules from self-contributions and may be deductible in both regimes subject to limits.

You cannot produce rent receipts, health insurance premium receipts, or investment proof documents — THEN do not choose the old regime based on expected deductions; claims without documentation will not hold at filing, and you will owe more tax than your employer’s TDS calculation assumed.

Common Mistakes to Avoid

Comparing CTC Instead of Actual Gross Taxable Salary

Your CTC includes employer PF contributions, gratuity provisions, and other components that are not part of your taxable gross salary.

Running a regime comparison on your full CTC figure can produce an error of ₹15,000–₹25,000 or more in the final tax calculation, making one regime appear better than it actually is. Ask your payroll or HR team for the gross salary figure as it will appear in Form 16 — not the CTC.

Form 16 Part B, once issued, is the most reliable figure to use for any comparison before filing.

Assuming 80C Alone Justifies Old Regime at ₹15 LPA

Many employees assume that maxing 80C at ₹1,50,000 is sufficient reason to choose the old regime.

At ₹15 LPA and a 30% marginal rate, 80C saves approximately ₹45,000 in tax under the old regime. But the new regime already delivers a ₹25,000 advantage through the higher standard deduction, and its lower slab rates further narrow the gap. 80C alone — without HRA and other deductions — rarely makes the old regime better at this salary level.

Always run the full calculation before deciding; one deduction is not a strategy.

Claiming HRA Exemption Without Valid Documentation

HRA exemption under Section 10(13A) requires rent receipts for every month and, for annual rent above ₹1 lakh, the landlord’s PAN card details.

Employees who declare an HRA claim at the start of the year without collecting actual receipts often scramble in February and March — and some cannot produce the required documents at all. If you cannot support the claim at filing, the entire HRA exemption is disallowed, and your taxable income under the old regime rises significantly.

Collect rent receipts from April itself, not March of the following year.

Miscounting the Section 80D Health Insurance Limits

Section 80D has specific sub-limits: ₹25,000 for self, spouse, and dependent children; an additional ₹25,000 for parents, rising to ₹50,000 if parents are senior citizens.

Some employees enter their total family insurance premium without checking whether it falls within the applicable sub-limits. Others forget the parents’ sub-limit entirely. Entering the wrong figure inflates the deduction total and leads to an incorrect regime comparison.

Count only what falls within the allowed caps, separately for self-and-family versus parents.

Choosing a Regime in April and Never Reviewing Before ITR

Your employer declaration is a provisional choice — it determines monthly TDS, not your final tax liability.

Salaried employees can generally choose a different regime when filing their ITR, giving a second opportunity to compare both sides with actual numbers from Form 16. Many employees who declared old regime at the start of the year switch to new regime at filing after realising their deductions did not add up to what they expected. Missing this review window means you may pay more tax than required.

Mark a reminder to run both calculations again before the ITR filing deadline.

Treating Employer TDS as the Final Tax Bill

TDS deducted by your employer is an advance estimate based on your declaration and the information available at the time of payroll.

If TDS was deducted under the new regime but your actual liability under old regime is lower, you can claim a refund by filing ITR under the correct regime. Equally, if TDS was under-deducted — because your employer did not account for variable pay or perquisites — you will owe the difference at filing. Never assume that what is deducted from your salary equals your final tax payable.

Buying Poor-Quality Products Just to Inflate 80C

Some employees purchase ULIPs, traditional endowment plans, or low-return annuity products they do not need, purely to push their 80C total higher and justify choosing old regime.

At ₹15 LPA, the potential tax saving from extra 80C investments in the old regime rarely exceeds ₹15,000–₹20,000. A product with poor returns held for 15–20 years can cost far more than that saving. If the product does not fit your financial plan independently, the tax benefit does not justify the cost.

When This May Not Be the Right Choice

The comparison in this article assumes a salaried employee with salary income only, standard deductions, and no complex financial arrangements for FY 2025-26. Your calculation may be materially different if any of the following apply:

- You have capital gains, ESOP vesting, or RSU income — these attract special tax rates and can interact with slab calculations in ways this article does not address.

- You have freelance or business income alongside your salary — mixing salary and non-salary income changes which regime you are eligible to choose and how deductions are treated under each.

- You changed employers during the year and have two Form 16s — you need to consolidate income from both employers before comparing regimes, and your effective deduction profile may differ significantly from a single-employer scenario.

- You have rental income or a home loan with rental property — Section 24(b) interest, rental income, and set-off rules create a more complex calculation that a basic salaried comparison does not cover.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

All tax slabs, standard deduction amounts, rebate thresholds, and deduction limits used in this article are published by the Income Tax Department for FY 2025-26. For the current new-regime slab structure applicable for AY 2026-27, see our current new slabs guide. The authoritative source for all rules covered in this article is:

- Income Tax Department — incometax.gov.in

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Cross-check your Form 16 Parts A and B against your Annual Information Statement (AIS) and Form 26AS before filing. The Income Tax portal’s built-in regime comparison calculator is free, updated each assessment year, and the most reliable tool available for your actual numbers.

Expert Tips

- Use the Income Tax portal’s own calculator — not a third-party website — with your actual Form 16 figures for the final decision. The official tool is updated for each AY and eliminates the risk of using outdated slab rates.

- Make your employer regime declaration by February, not April. If you wait until the last payroll cycle, your employer cannot retroactively adjust TDS across all months, and the full shortfall hits in a single deduction in March — which affects your cash flow significantly.

- Check whether employer NPS contributions under Section 80CCD(2) apply to you and whether they are deductible under the new regime up to a limit; this is one of the few deductions that may be available in both regimes and is frequently overlooked during comparison calculations.

- Do not calculate HRA exemption as the full HRA component in your salary. The exemption is the minimum of three formula values — and for employees in non-metro cities or with low rent, the exemption is often much smaller than the HRA received. Entering the HRA component directly inflates the old-regime advantage in your own comparison.

- Store health insurance premium receipts digitally from April itself. Many employees realise in February that they need documentation from the previous April — and the insurer has already generated a new annual document. Keep a folder with each year’s receipts from the moment you renew.

- Review your regime choice every year — a salary hike, a new home loan, a change in living situation, or the addition of a parent’s insurance policy can shift the break-even point meaningfully from one FY to the next. Do not assume last year’s choice is still optimal.

- Avoid topping up 80C investments purely to force old regime eligibility if those investments do not serve your larger financial goals. An ELSS or PPF investment made for the right reason is valuable. An endowment policy bought to inflate a tax comparison is not.

Frequently Asked Questions

Which tax regime is better for a ₹15 LPA salary in FY 2025-26?

Based on FY 2025-26 rules, the new regime produces a lower tax bill for most ₹15 LPA employees — particularly those with moderate or no HRA, no home loan, and straightforward investments. The old regime can be better only when total deductions beyond the standard deduction reach approximately ₹5–6 lakh, which typically requires high metro-city rent, maxed 80C, health insurance covering parents, and NPS contributions. Run both calculations at incometax.gov.in with your actual figures before deciding.

How much deduction do I need for the old regime to beat the new regime at ₹15 LPA?

For FY 2025-26, the old regime needs to bring your taxable income to approximately ₹9 lakh or below to match or beat the new regime’s ₹97,500 tax on ₹14,25,000. To achieve that starting from ₹15,00,000 gross, you need roughly ₹5.5 lakh or more in combined deductions after the standard deduction. This is a high threshold — it generally requires a combination of substantial metro-city HRA, fully utilised 80C, 80D for self and parents, and NPS contributions. Without HRA of at least ₹2.5–3 lakh, it is difficult to reach this bar at ₹15 LPA.

Is Section 80C allowed under the new tax regime?

No. Section 80C deductions — covering EPF self-contribution, PPF, ELSS, LIC premiums, home loan principal repayment, and more — are not available under the new tax regime for FY 2025-26. Your EPF will still be deducted if your employer mandatorily contributes, but you cannot reduce your taxable income with that amount under the new regime.

Is HRA exemption allowed under the new tax regime?

No. HRA exemption under Section 10(13A) is not available under the new tax regime. If you pay significant rent — particularly in a metro city like Bengaluru, Mumbai, or Delhi — this is typically the strongest single reason to evaluate the old regime carefully at ₹15 LPA. A full HRA exemption of ₹2–3 lakh can shift the regime comparison meaningfully.

Can I change my tax regime when filing my ITR if I declared a different one to my employer?

Salaried employees with only salary income can generally choose their tax regime at the time of filing ITR, not only at employer declaration. This means your TDS deduction during the year does not lock you in. If you declared old regime at the start of the year but the new regime is better, you can file under the new regime and claim a refund for the excess TDS. However, if you have business income, specific restrictions on switching apply — verify the current rules for your income type at incometax.gov.in before filing.

Does my employer’s TDS deduction decide my final tax regime?

No. TDS is your employer’s advance estimate based on the declaration you provided. Your final tax liability is established when you file your ITR with actual, verified deduction figures. If TDS was over-deducted relative to your correct regime and deductions, you will receive a refund. If it was under-deducted, you will owe the difference at filing. The figure on your Form 16 Part A is the amount deducted — it is not the final tax payable.

Can I claim NPS deduction under the new tax regime?

The self-contribution NPS deduction under Section 80CCD(1B) — up to ₹50,000 over and above the 80C limit — is not available under the new tax regime. However, employer contributions to NPS under Section 80CCD(2) have separate rules and may be deductible even under the new regime, subject to a limit. Verify the current rules and sub-limits for AY 2026-27 specifically at incometax.gov.in, as these provisions can change with Budget amendments.

What is the break-even deduction level between old and new regime at ₹15 LPA?

For FY 2025-26, based on a gross salary of ₹15,00,000, the old regime roughly needs to reduce your taxable income to ₹9,25,000 or below to match the new regime’s tax bill. Achieving this requires approximately ₹5.25 lakh in combined deductions after the standard deduction — a level most ₹15 LPA employees can only approach if they are paying high metro-city rent with a well-structured HRA, maxing 80C, insuring their parents under 80D, and contributing to NPS. For most employees without all of these simultaneously, the new regime wins.

What happens if I declare the wrong regime to my employer and realise later?

You can correct this when filing your ITR. Your employer’s TDS calculation is provisional, and for salaried employees with no business income, the regime choice at ITR filing generally takes precedence. If you over-paid TDS under the wrong regime, you will get a refund. Keep all deduction documents regardless of which regime you initially declared — you may need them at filing even if you ultimately decide to switch.

Final Verdict

For most salaried employees earning ₹15 LPA in FY 2025-26, the new tax regime is likely to produce a lower tax bill — particularly for those with moderate HRA, no home loan, and standard 80C investments. The significantly revised new-regime slabs make it the stronger default at this income level for a straightforward salary profile. However, employees paying high metro-city rent, with a large HRA exemption, maxed 80C, and health insurance covering parents may find the old regime saves marginally more tax — sometimes ₹1,000–₹5,000 depending on the exact deduction mix. Tax saving for 15 LPA salary is a specific, calculable question: the margin between regimes can be narrow enough that only running both calculations with your actual figures will give you a reliable answer. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Kavita Mehra writes and edits Ridhi.com’s income tax content for Indian taxpayers, with a special focus on salaried employees and beginners who find tax rules confusing. Her work explains complex tax topics in simple language, helping readers understand how income, deductions, exemptions, rebates, TDS, Form 16, ITR filing, and refunds connect in real life.

She covers topics such as old vs new tax regime, income tax slabs, standard deduction, Section 87A rebate, HRA exemption, 80C, 80D, 80E, 80G, TDS on salary, taxable income, Form 16, AIS, Form 26AS, advance tax, and ITR filing checklists. Her content aims to help readers become more informed before filing returns or discussing tax matters with a professional.

Kavita’s approach is careful, compliance-focused, and official-source oriented. Because Indian tax rules can change after Budgets, circulars, and policy updates, her articles encourage readers to verify current figures, filing deadlines, and rules from the Income Tax Department or a qualified tax professional before acting.