You earn ₹10 lakh a year — and you are staring at two tax regimes, wondering which one actually saves you more money. Most guides give you a generic old-versus-new comparison. This one does not. It runs the numbers specifically for a ₹10 LPA salaried employee in FY 2025-26 (AY 2026-27), shows you the deduction break-even point, and tells you exactly when old beats new — and when it does not. Tax saving for 10 LPA salary is not about guessing; it is about knowing your own deduction total before your employer locks in your TDS declaration.

Quick Answer: Tax Saving for ₹10 LPA Salary

Tax saving for 10 LPA salary depends on whether your old-regime deductions beat the new regime’s lower slabs and rebate. For FY 2025-26, a salaried ₹10 LPA taxpayer may pay zero tax under the new regime after standard deduction and Section 87A rebate. Whether the old regime saves more depends on your total deductions under Chapter VI-A and exemptions like HRA — run the comparison using your actual numbers for AY 2026-27.

Key Takeaways

- Under the new regime for FY 2025-26, a ₹10 LPA salaried employee with only the standard deduction of ₹75,000 arrives at a taxable income of ₹9,25,000 — tax liability before cess is approximately ₹42,500 at applicable slab rates.

- The old regime gives you deductions: ₹1,50,000 under Section 80C, up to ₹25,000 under Section 80D, and HRA exemption — each one pulls your taxable income lower than the new regime can.

- If your combined deductions under the old regime exceed approximately ₹2,00,000–₹2,50,000 (beyond the standard deduction), the old regime likely saves more tax at ₹10 LPA.

- Section 87A rebate under the new regime applies up to ₹7 lakh taxable income — at ₹10 LPA, your taxable income after standard deduction exceeds this threshold, so full rebate does not apply.

- Health and education cess at 4% applies on top of your final tax liability under both regimes — factor this into every calculation.

- Your employer’s TDS is based on the regime you declare at the start of the year — switch declarations carefully and verify with your HR or payroll team.

- The new regime is now the default; you must actively opt for the old regime when filing your ITR if you want deductions.

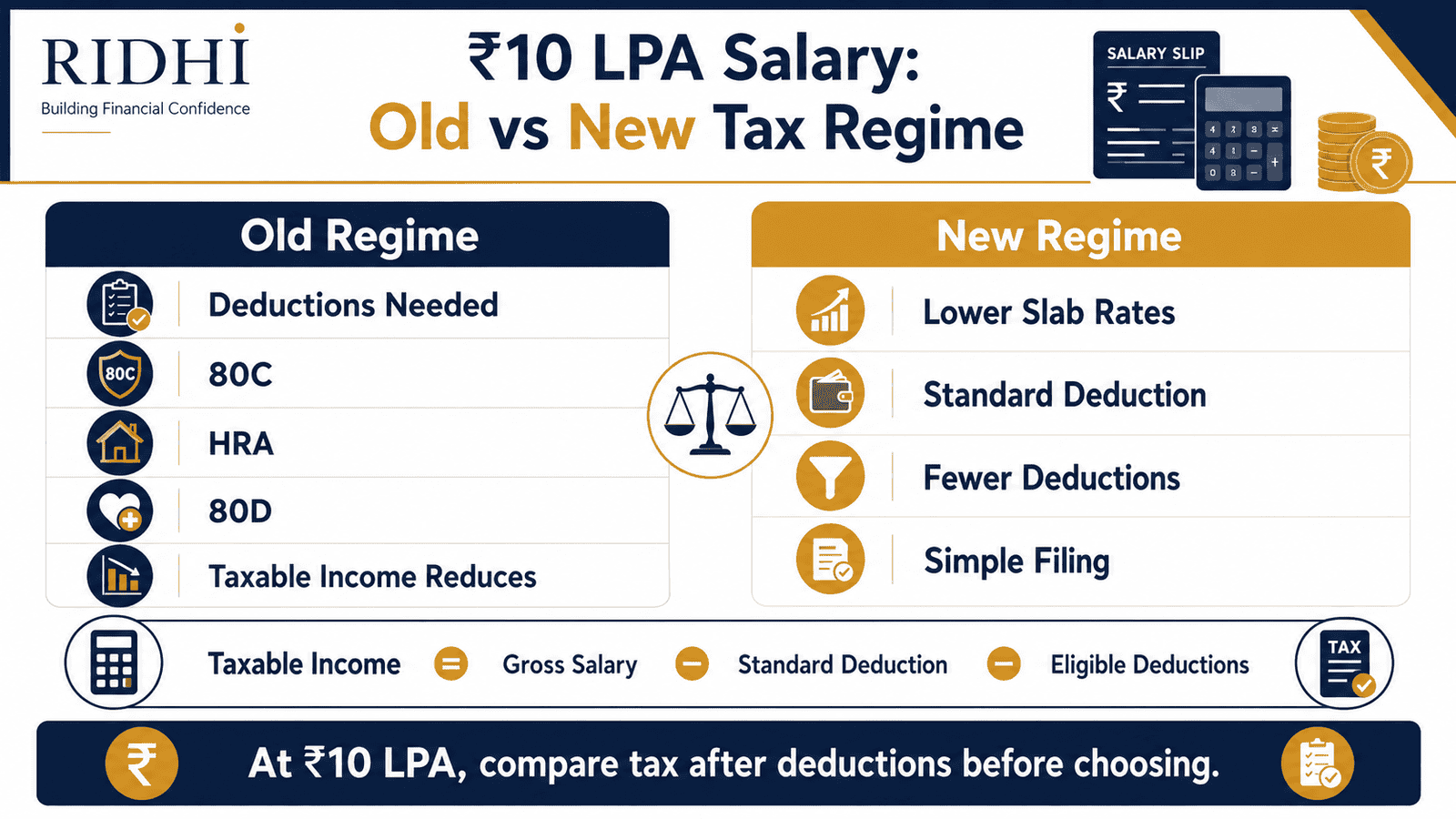

Old Regime vs New Regime: ₹10 LPA Salary Comparison (FY 2025-26)

| Parameter | New Regime | Old Regime |

|---|---|---|

| Gross Salary | ₹10,00,000 | ₹10,00,000 |

| Standard Deduction (Section 16) | ₹75,000 | ₹50,000 |

| Section 80C Deduction | Not available | Up to ₹1,50,000 |

| Section 80D (Health Insurance) | Not available | Up to ₹25,000 |

| HRA Exemption | Not available | Depends on rent, city, salary |

| Taxable Income (with max deductions) | ₹9,25,000 | As low as ~₹5,75,000 (typical case) |

| Section 87A Rebate | Not applicable (income exceeds ₹7L) | Not applicable (income exceeds ₹5L) |

| Approximate Tax Before Cess | ~₹42,500 | ~₹32,500 (with full deductions) |

| Health & Education Cess (4%) | ~₹1,700 | ~₹1,300 |

| Total Approximate Tax | ~₹44,200 | ~₹33,800 |

| Default Regime? | Yes | Must opt in |

| Deduction paperwork required? | No | Yes |

Note: Tax figures above are illustrative for a salaried employee with standard salary structure and maximum common deductions. Verify actual liability using official slab rates from incometax.gov.in for AY 2026-27. See internal link to new regime slabs for full slab breakdown.

Key Facts at a Glance

| Item | New Regime | Old Regime |

|---|---|---|

| Standard Deduction (FY 2025-26) | ₹75,000 | ₹50,000 |

| Section 80C Limit | Not allowed | ₹1,50,000 |

| Section 87A Rebate Limit | Up to ₹7 lakh taxable income | Up to ₹5 lakh taxable income |

| Applicable Cess | 4% on tax | 4% on tax |

| Default Regime (salaried) | Yes (from FY 2023-24) | Must opt in at ITR filing |

| Assessment Year | AY 2026-27 | AY 2026-27 |

Understanding Tax Saving for 10 LPA Salary: How Both Regimes Work

At ₹10 LPA, you sit in a tax bracket where both regimes produce meaningfully different outcomes — and the difference depends almost entirely on how many deductions you can legitimately claim. This is not a case where one regime is obviously better. It depends on your rent, your 80C investments, your health insurance premium, and how much of your salary is structured as HRA.

How the New Regime Taxes ₹10 LPA

Under Section 115BAC, the new tax regime applies simplified slab rates. For FY 2025-26, the new regime slabs for income above ₹3 lakh are taxed progressively — you pay 5% on income from ₹3 lakh to ₹7 lakh, 10% from ₹7 lakh to ₹10 lakh, and 15% above ₹10 lakh (verify current slabs at incometax.gov.in for AY 2026-27). As a salaried employee, you get the standard deduction under Section 16 — ₹75,000 for FY 2025-26 — bringing your taxable income to ₹9,25,000. No Chapter VI-A deductions apply. No HRA exemption. No 80C, 80D, or any other deduction is available.

The trade-off is simplicity. You do not need to collect rent receipts, investment proofs, or insurance premium certificates. Your employer deducts TDS based on the new regime by default, and you pay tax on a clean number. For readers who want the full slab breakdown, the new regime slabs guide covers every rate and threshold in detail.

How the Old Regime Taxes ₹10 LPA

The old regime — technically called the regular tax regime — uses higher slab rates but lets you reduce taxable income significantly through deductions and exemptions. For salaried employees at ₹10 LPA, the most impactful ones are:

- Standard Deduction (Section 16): ₹50,000 — available without any paperwork

- Section 80C: Up to ₹1,50,000 — EPF contribution, PPF, ELSS, LIC premium, home loan principal, and more

- Section 80D: Up to ₹25,000 for health insurance premium paid for self and family

- HRA Exemption (Section 10(13A)): Exempt portion of house rent allowance — depends on actual rent paid, HRA received, and city classification

If you live in a metro on rent, pay health insurance, and max your EPF or ELSS contributions, your taxable income under the old regime can drop well below ₹7 lakh — and potentially to a level where Section 87A rebate applies (up to ₹5 lakh taxable income under old regime). For a broader comparison between regimes beyond the ₹10 LPA case, see old versus new rules for salaried employees.

The Break-Even Point: When Does Old Regime Win?

Here is the core question: how much do your old-regime deductions need to total before the old regime saves more tax than the new regime?

At ₹10 LPA, the new regime taxes you on ₹9,25,000 (after ₹75,000 standard deduction). The old regime taxes you on ₹9,50,000 before any Chapter VI-A deductions (after ₹50,000 standard deduction). The new regime’s standard deduction advantage is ₹25,000 more than old regime. So your old-regime deductions beyond standard deduction — 80C, 80D, HRA — need to exceed approximately ₹2,00,000–₹2,50,000 combined to make the old regime more tax-efficient at this income level. The exact break-even shifts based on which slabs apply to which portion of your income, so use the tax calculator comparison tool to find your precise number.

Understanding standard deduction explained is essential here — it is the one deduction that applies in both regimes automatically, and it is the baseline from which your comparison starts.

Real Example: Rohit’s ₹10 LPA Tax Calculation in Pune

Rohit is 29 years old, a software engineer at a mid-sized IT firm in Pune, earning a gross salary of ₹10,00,000 per year. His salary includes an HRA component of ₹1,80,000 annually. He pays rent of ₹15,000 per month (₹1,80,000 per year). He contributes ₹60,000 per year to EPF (employer + employee share on his side), has invested ₹90,000 in ELSS funds, and pays ₹12,000 annually for a health insurance policy for himself and his parents under 60. His total 80C investments: ₹1,50,000. His 80D claim: ₹12,000.

Under the Old Regime: Gross ₹10,00,000 → minus ₹50,000 standard deduction = ₹9,50,000 → minus ₹1,50,000 (80C) = ₹8,00,000 → minus ₹12,000 (80D) = ₹7,88,000 → minus HRA exemption. Rohit’s HRA exemption is the least of: actual HRA received (₹1,80,000), rent paid minus 10% of basic (say ₹1,80,000 − ₹60,000 = ₹1,20,000), or 40% of basic salary (non-metro Pune). His exemption is approximately ₹1,00,000–₹1,20,000. Taxable income: approximately ₹6,68,000–₹6,88,000. Tax on this under old regime slabs: approximately ₹44,000–₹48,000 before cess — Section 87A rebate does not apply as income exceeds ₹5 lakh. After 4% cess: approximately ₹45,760–₹49,920.

Under the New Regime: Gross ₹10,00,000 → minus ₹75,000 standard deduction = ₹9,25,000 taxable income. Tax at applicable slab rates: approximately ₹42,500 before cess. After 4% cess: approximately ₹44,200.

In Rohit’s case, the new regime saves him approximately ₹1,500–₹5,700 depending on his exact HRA computation. The old regime does not win — primarily because his EPF contribution is partially employer-funded and his HRA exemption in non-metro Pune is moderate. Key insight: at ₹10 LPA, a higher rent in a metro city or a larger 80D claim can flip this outcome entirely.

How to Calculate Your Tax at ₹10 LPA

Taxable Income (New Regime) = Gross Salary − Standard Deduction (₹75,000)

Taxable Income (Old Regime) = Gross Salary − Standard Deduction (₹50,000) − 80C − 80D − HRA Exemption − Other Chapter VI-A deductions

Tax Payable = Tax on Taxable Income (per applicable slabs) + 4% Health & Education Cess

Using Rohit’s figures from the example above:

| Scenario | Taxable Income | Approx Tax (incl. 4% cess) |

|---|---|---|

| New Regime — Rohit (standard deduction only) | ₹9,25,000 | ~₹44,200 |

| Old Regime — Rohit (80C + 80D + moderate HRA) | ~₹6,78,000 | ~₹47,840 |

| Old Regime — Metro renter (₹1.8L HRA + full 80C + 80D) | ~₹5,75,000 | ~₹33,800 |

Notice how the metro renter scenario changes everything. A higher HRA exemption in Mumbai or Delhi — where rent paid is typically much higher — can pull taxable income under ₹6 lakh and create a meaningful old-regime advantage. Use the tax calculator comparison to run your own numbers with your actual HRA and deduction figures for AY 2026-27.

How to Decide What’s Right for You

You pay rent in a metro city (Mumbai, Delhi, Chennai, Kolkata) and your monthly rent is ₹15,000 or more — THEN calculate your HRA exemption first. It is likely your single largest deduction and may tip the old regime in your favour at ₹10 LPA.

Your total deductions under 80C + 80D + HRA + any other Chapter VI-A deductions exceed ₹2,25,000 — THEN the old regime almost certainly saves you more tax at this income level.

You are in a non-metro city, own your home (no HRA), and your 80C investments are mostly EPF contributions you are not actively topping up — THEN the new regime is likely more tax-efficient for you at ₹10 LPA.

You have a home loan and claim both 80C (principal repayment) and Section 24(b) (interest deduction up to ₹2 lakh) — THEN the old regime may save significantly more. Section 24(b) alone can reduce taxable income by ₹2 lakh in old regime, with no equivalent in the new regime.

You prefer simplicity, do not want to track investment proofs, rent receipts, and medical insurance certificates — THEN the new regime is designed for you and reduces compliance burden to near zero.

Your deductions from old regime deductions total under ₹1,75,000 after standard deduction — THEN the new regime almost certainly results in lower tax at ₹10 LPA.

You do not pay rent, have no active 80C investments beyond mandatory EPF, and do not have a health insurance policy — THEN do not default to the old regime expecting savings. You will likely pay more tax, not less.

Common Mistakes to Avoid

Assuming the old regime always saves more tax

Many salaried employees at ₹10 LPA assume that more deductions automatically mean lower tax under the old regime.

At ₹10 LPA, the new regime’s lower slab rates and higher standard deduction of ₹75,000 create a strong baseline. If your actual deductions are under ₹2 lakh (which is true for many employees without HRA or active investments), the old regime can result in ₹5,000–₹10,000 more tax, not less.

Run the comparison with your actual deduction numbers before deciding — do not assume.

Forgetting that standard deduction differs between regimes

A common error is using ₹50,000 as the standard deduction for both regimes.

For FY 2025-26, the standard deduction under the new regime is ₹75,000 — ₹25,000 more than the old regime. This ₹25,000 difference alone shifts the break-even point for your deduction total and must be factored into any manual calculation.

Always use the correct figure for each regime — see standard deduction explained for the full rules.

Overclaiming HRA without receipts

Some employees claim HRA exemption for rent they did not actually pay or inflate rent amounts to reduce taxable income.

HRA exemption requires actual rent payment proof — rent receipts and, if annual rent exceeds ₹1 lakh, the landlord’s PAN. Incorrect claims can attract scrutiny, notices, and penalties from the Income Tax Department. For accurate calculation of your HRA exemption, use the HRA tax benefit calculator before filing.

Only claim what you can document.

Missing the regime declaration deadline with your employer

Your employer asks for your regime choice at the start of the financial year — usually in April. If you miss declaring the old regime, TDS is deducted under the new regime by default throughout the year.

You can still switch at the ITR filing stage, but late switching means either a large tax payment at filing or a refund wait — both are avoidable. Declare your regime choice in writing to HR as early as April.

Treating EPF employee contribution as an extra 80C investment

Your EPF employee contribution already counts towards your ₹1,50,000 Section 80C limit. Many employees assume they can claim 80C on top of their EPF contribution.

If your annual EPF contribution is ₹60,000, your remaining 80C headroom is only ₹90,000. Investing ₹1,50,000 in ELSS on top of EPF means ₹60,000 is wasted beyond the cap. Track your 80C total carefully before March 31.

Ignoring Section 87A rebate thresholds

At ₹10 LPA, many employees assume the Section 87A rebate applies to them. Under the new regime, the rebate applies only if taxable income is ₹7 lakh or below — and your new regime taxable income at ₹10 LPA is ₹9,25,000 after standard deduction. No rebate applies.

Under the old regime, the threshold is ₹5 lakh taxable income — also not met at this salary unless deductions are very large. Do not factor in a rebate that does not apply to your situation.

Not verifying figures before filing

Tax slabs, standard deduction amounts, 87A rebate limits, and surcharge thresholds are announced in the Union Budget and can change every year. Using last year’s figures for FY 2025-26 is a common error that results in incorrect TDS or ITR mismatches.

Always verify the current AY 2026-27 figures at incometax.gov.in before calculating or filing. Your Form 16 will reflect the correct TDS computation if your employer has been updated.

When This May Not Be the Right Choice

The old regime — even with deductions — may not be the right choice for every ₹10 LPA salaried employee. If you own your home and have no HRA claim, your deduction total may not cross the break-even threshold that makes old regime worthwhile. If you are in your first job and have just started investing, your 80C portfolio may be too small to create a meaningful old-regime advantage. If your employer does not support a flexible pay structure that separates HRA and basic clearly, your actual HRA exemption may be smaller than you expect. And if you find tax paperwork stressful or routinely miss investment deadlines, the administrative overhead of the old regime — receipts, certificates, declarations — may cost you more in effort than it saves in rupees. If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Tax slabs, standard deduction, Section 87A rebate limits, and Chapter VI-A deduction caps are subject to change with each Union Budget. The figures in this article are based on publicly available information for FY 2025-26 (AY 2026-27). Always verify current figures directly from the official source before making any financial decision.

- Income Tax Department — incometax.gov.in

- Income Tax India (e-filing portal) — incometaxindia.gov.in

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- If you are in the 20% slab bracket under the old regime, each ₹1,000 of additional deduction you claim saves you ₹200 in tax — plus 4% cess on that amount. That makes topping up your 80C to the full ₹1,50,000 limit worth approximately ₹31,200 in tax saved for most ₹10 LPA employees on the old regime.

- Use your employer’s flexi-benefit or reimbursement structure — if available — to maximise tax-free components before comparing regimes. Phone bills, books and periodicals, and leave travel allowance can reduce your taxable income outside the 80C cap.

- If you pay rent but have not submitted HRA declarations to HR, do it now — even mid-year. Your employer can adjust TDS from the current month onwards. Do not wait until ITR filing to claim HRA; proactive declaration reduces the lump-sum tax shortfall at year-end.

- ELSS mutual funds have the shortest lock-in period (3 years) among all Section 80C options — and historically deliver equity-linked returns. If you are under 35 and have unused 80C headroom, ELSS is the most tax-efficient and wealth-building option before March 31.

- If your taxable income under the old regime comes close to ₹5 lakh after deductions, consider topping up NPS under Section 80CCD(1B) — an additional ₹50,000 deduction over and above 80C — to push taxable income below ₹5 lakh and potentially qualify for Section 87A rebate, making your tax liability zero.

- Cross-check your Form 16 Part B against your own deduction list every year. Employers sometimes miss deductions or apply the wrong regime. Catching an error before filing prevents a mismatch notice from the Income Tax Department.

- Run both regime calculations fresh each financial year — do not rely on last year’s decision. A salary increment, a new home loan, a change in rent, or a Budget announcement can flip which regime saves more for you at ₹10 LPA or beyond.

Frequently Asked Questions

How much income tax do I pay on ₹10 LPA salary under the new regime in FY 2025-26?

Under the new regime for FY 2025-26, your taxable income after the ₹75,000 standard deduction is ₹9,25,000. Applying the progressive slab rates (5% on ₹3L–₹7L, 10% on ₹7L–₹10L, 15% above ₹10L), your tax before cess is approximately ₹42,500. After 4% health and education cess, your total tax liability is approximately ₹44,200. Verify exact slab rates for AY 2026-27 at incometax.gov.in before filing.

Is the old regime always better if I have 80C investments?

Not necessarily. At ₹10 LPA, the new regime’s higher standard deduction (₹75,000) and lower slab rates mean that your old-regime deductions need to exceed roughly ₹2,00,000–₹2,25,000 combined — including 80C, 80D, and HRA — before the old regime saves more tax. If you only have EPF as a 80C component and no HRA claim, the new regime is likely cheaper.

Does Section 87A rebate apply at ₹10 LPA?

Under the new regime, Section 87A rebate applies only if your taxable income is ₹7 lakh or below. At ₹10 LPA, after the ₹75,000 standard deduction, your taxable income is ₹9,25,000 — well above the ₹7 lakh threshold. The rebate does not apply. Under the old regime, the rebate threshold is ₹5 lakh taxable income, which also requires significant deductions to reach from ₹10 LPA gross.

Can I switch tax regimes after submitting my declaration to my employer?

Yes. Even if you declared one regime to your employer, you can switch at the time of ITR filing. If you switch to the old regime at filing, you can claim deductions your employer did not account for in TDS. However, this may result in a tax shortfall or excess TDS — both of which are resolved through refund or additional payment at filing. Salaried employees (without business income) can switch regimes each year at filing.

What is the break-even deduction amount for the old regime at ₹10 LPA?

Approximately ₹2,00,000–₹2,50,000 in deductions beyond the standard deduction is the rough break-even range at ₹10 LPA. This includes 80C (up to ₹1,50,000), 80D (up to ₹25,000), and HRA exemption. The exact break-even depends on which slabs your income falls into under each regime. Use the online income tax calculator at incometax.gov.in or the Ridhi tax calculator to find your precise number.

Is the new tax regime the default for salaried employees?

Yes. From FY 2023-24 onwards, the new tax regime is the default for salaried employees. If you do not actively declare the old regime to your employer or opt for it at ITR filing, the new regime applies automatically. You must take action to use the old regime — it does not happen by default.

What deductions are available under the new regime for a salaried employee?

The new regime allows very few deductions. The main one available to salaried employees is the standard deduction of ₹75,000 under Section 16. Employer contributions to NPS under Section 80CCD(2) are also allowed. Chapter VI-A deductions — including 80C, 80D, 80E, and 80G — are not available under the new regime. HRA exemption and LTA are also not available.

What happens if I miss the 80C investment deadline?

Section 80C investments must be made by March 31 of the relevant financial year to qualify for deduction in that year. If you miss the deadline, you cannot backdate investments — they will count for the following financial year. Your taxable income for the missed year will be higher, and your employer may deduct higher TDS in the final months of the year once they account for the shortfall.

Can I claim both 80C and HRA exemption together under the old regime?

Yes. These are separate provisions under the Income Tax Act. Section 80C deductions and HRA exemption under Section 10(13A) can both be claimed simultaneously under the old regime, as long as the conditions for each are met — investments must be eligible, and HRA requires actual rent payment with documentation. Together they can significantly reduce your taxable income at ₹10 LPA.

What is the best way to reduce tax on ₹10 LPA salary?

The most effective approach for FY 2025-26 is to calculate both regimes with your actual figures — do not guess. If you pay significant rent, maximise your HRA claim with proper documentation. Max out 80C to ₹1,50,000 using EPF, ELSS, or PPF. Add ₹12,000–₹25,000 of 80D for health insurance. If your old regime taxable income comes close to ₹5 lakh, top up NPS via Section 80CCD(1B) for an extra ₹50,000 deduction. Then compare total tax under each regime and choose accordingly for AY 2026-27.

Final Verdict

Tax saving for 10 LPA salary comes down to one question: how much can you genuinely deduct? If your total deductions — HRA, 80C, 80D, and any NPS contribution — exceed roughly ₹2,25,000 beyond the standard deduction, the old regime will likely save you more tax in FY 2025-26. If your deductions fall short of that threshold, the new regime’s lower slab rates and higher ₹75,000 standard deduction usually win. For most salaried employees in non-metro cities without active HRA claims, the new regime is the simpler and cheaper option. For metro renters who have maxed their 80C and have health insurance, the old regime can save ₹10,000–₹15,000 or more. Neither answer applies to everyone — your actual deduction total is the deciding factor. Use the tax calculator comparison to run your exact numbers for AY 2026-27 before submitting your declaration. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Kavita Mehra writes and edits Ridhi.com’s income tax content for Indian taxpayers, with a special focus on salaried employees and beginners who find tax rules confusing. Her work explains complex tax topics in simple language, helping readers understand how income, deductions, exemptions, rebates, TDS, Form 16, ITR filing, and refunds connect in real life.

She covers topics such as old vs new tax regime, income tax slabs, standard deduction, Section 87A rebate, HRA exemption, 80C, 80D, 80E, 80G, TDS on salary, taxable income, Form 16, AIS, Form 26AS, advance tax, and ITR filing checklists. Her content aims to help readers become more informed before filing returns or discussing tax matters with a professional.

Kavita’s approach is careful, compliance-focused, and official-source oriented. Because Indian tax rules can change after Budgets, circulars, and policy updates, her articles encourage readers to verify current figures, filing deadlines, and rules from the Income Tax Department or a qualified tax professional before acting.