₹75,000 a month sounds comfortable — until rent, EMI, groceries, insurance, and parents’ support arrive before the 10th. The 75000 monthly salary budget that looked effortless in your head turns stressful the moment you stop planning it deliberately.

The problem is rarely the salary. It is the absence of a plan for where each rupee goes before it is spent. Most salaried earners manage money reactively: spend first, save whatever is left. That “whatever is left” reliably ends up being zero.

This article gives you a practical, India-specific framework for a ₹75,000 monthly salary — covering rent, EMI, groceries, insurance, emergency savings, and SIP investments. You will find a worked example, a step-by-step calculation, and alternate budget models for different life situations so you can pick what fits your reality.

Quick Answer: 75000 Monthly Salary Budget

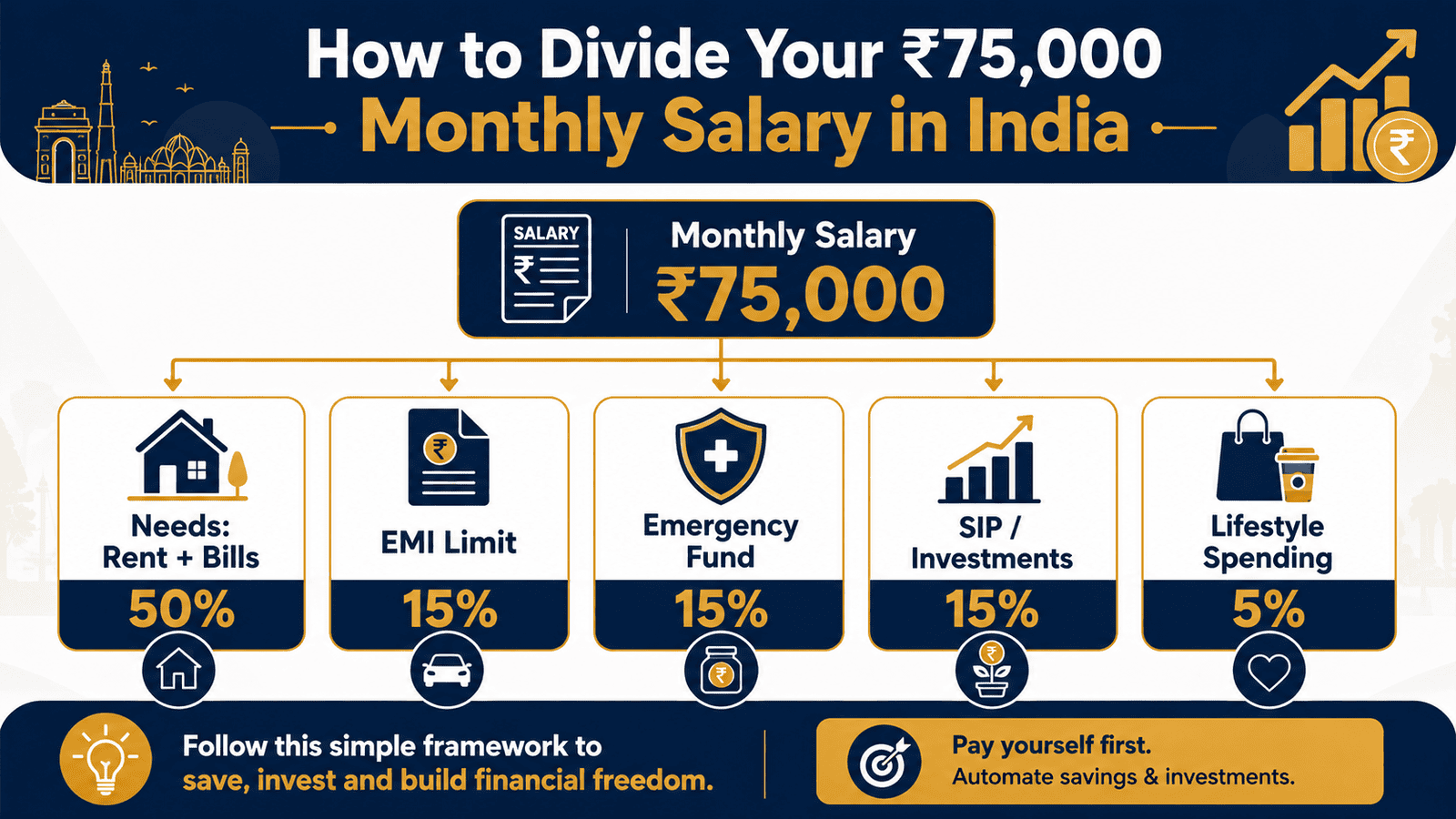

A 75000 monthly salary budget should usually keep essentials near ₹37,500, wants around ₹15,000, and savings or investments around ₹22,500. In India, adjust this based on rent, EMI, dependents and emergency fund status. If EMI is high, protect emergency savings first before increasing SIPs.

Key Takeaways

- A ₹75,000 monthly salary budget works best when rent stays at or below ₹18,750–₹20,000 — roughly 25% of income. Above ₹25,000 in rent, savings face serious pressure.

- Safe EMI on ₹75,000 in-hand salary is typically ₹15,000–₹22,500 per month. Beyond ₹22,500, emergency fund contributions and investments are the first casualties.

- Build an emergency fund of ₹2.25 lakh to ₹4.5 lakh (3–6 months of expenses) before increasing SIP aggressively. The safety buffer comes before wealth building.

- The 50/30/20 rule is a starting framework, not a law. Indian families with dependents, school fees, or metro rent typically operate on a 60/15/25 or 65/10/25 split instead.

- Lifestyle inflation is the biggest silent budget leak: a ₹5,000 monthly lifestyle upgrade costs ₹60,000 a year — money that could otherwise compound in investments over a decade.

- Savings and investments serve different purposes: savings are liquid and safe, investments carry market or lock-in risk. Handle safety before wealth creation.

Key Facts at a Glance

| Budget Category | Recommended Range | ₹ Amount (Illustrative) |

|---|---|---|

| Monthly In-Hand Salary | 100% | ₹75,000 |

| Essentials (Needs) | 45–55% | ₹33,750–₹41,250 |

| Rent (within Essentials) | 20–28% | ₹15,000–₹21,000 |

| Total EMI (all loans combined) | 15–25% | ₹11,250–₹18,750 |

| Wants (Lifestyle) | 10–20% | ₹7,500–₹15,000 |

| Savings and Investments | 20–30% | ₹15,000–₹22,500 |

| Emergency Fund Target | 3–6 months of expenses | ₹2.25L–₹4.5L total |

These ranges are illustrative starting points. Your actual split depends on your city, family size, existing loans, and goals. Use the take-home pay estimate to confirm your actual in-hand salary before building your budget — especially if ₹75,000 is a CTC estimate rather than a confirmed bank credit.

How to Build a 75000 Monthly Salary Budget From First Principles

Start with what you actually take home — not CTC

The first and most common error in salary budgeting India is planning with a CTC figure. If ₹75,000 is your in-hand salary — the amount credited to your account — you can budget from it directly. If it is an approximation of your CTC, your actual take-home could be ₹60,000–₹70,000 after EPF contributions, income tax, professional tax, and health insurance deductions. Understanding your salary slip components is the essential first step before any budget planning begins. These deductions are not optional — they are already gone before your salary hits your account.

The 50/30/20 rule and why Indian families need to adapt it

The 50/30/20 budgeting rule — 50% on needs, 30% on wants, 20% on savings — is the most popular personal finance planning framework globally. Applied to ₹75,000, it suggests ₹37,500 for needs, ₹22,500 for wants, and ₹15,000 for savings.

That framework works cleanly on paper. In practice, Indian salaried earners in Tier-1 cities face a different reality: rent alone can consume 25–35% of take-home salary. Add grocery costs, utility bills, transport, health insurance premiums, and monthly support to parents — and the needs bucket can exceed 60% before anyone has spent a rupee on lifestyle. There is simply no room for a 30% wants allocation without gutting savings.

A more realistic adapted model for many Indian salaried families looks like 55–65% on essentials, 10–15% on lifestyle, and 20–30% on savings and investments. The monthly budget rule for Indian families explains when to adapt this framework — and how to do it without feeling like you are failing at personal finance.

Build the budget in the right order

Do not start by deciding how much to spend on dining or weekend trips. Start with what you cannot negotiate: rent, groceries, utilities, school fees, family support payments, and insurance premiums. These fixed essentials set your actual monthly floor.

Next, account for EMI obligations. A home loan, car loan, or personal loan EMI belongs in the essentials bucket — not the lifestyle column. Your total EMI across all loans should ideally stay below 25–30% of your in-hand salary. Combined with rent, total committed outflows should not exceed 50% of income.

After fixed essentials and EMI, assign minimum amounts to your emergency fund and health insurance. These are non-negotiable safety items — not optional savings. Only after covering safety should money flow to investments such as SIPs and mutual funds. Lifestyle spending gets what is genuinely left over.

Saving versus investing: they are not the same thing

Savings and investments serve different purposes and should never be conflated. Savings are for safety: your emergency fund, parked in a liquid fixed deposit or sweep-in savings account, accessible within 24 hours without penalty. Investments are for wealth: money placed in equity mutual funds via SIP, ELSS, index funds, or debt instruments, with a defined time horizon.

If you have no emergency fund or inadequate health cover, redirecting investment money to build safety first is mathematically smarter — even if it feels less exciting. A single medical emergency or job loss without a cash buffer can force you to redeem SIPs at a market low, wiping out months of accumulated gains and compounding.

Rent-to-income ratio and health insurance premium planning

A practical rent-to-income target for Indian salaried earners is 25–30% of take-home salary. On ₹75,000, that puts a comfortable rent range at ₹18,750–₹22,500 per month. In central Mumbai or Bengaluru, finding a well-located 1BHK within this range can be challenging — making commute trade-offs a real part of cash flow planning.

Health insurance premium planning is another category that most salary budget articles ignore. At ₹75,000 per month, an individual ₹5–₹10 lakh health policy costs approximately ₹7,000–₹14,000 per year (roughly ₹600–₹1,200 per month), depending on age and insurer. Verify exact premiums with IRDAI-registered insurers directly. If your employer’s group policy is below ₹5 lakh, a top-up or standalone policy is worth budgeting for — both as a monthly cost and a peace-of-mind investment.

Real Example: Rohan’s Monthly Budget in Pune

Rohan, 30, is a software developer at a mid-sized IT firm in Pune. He takes home ₹75,000 per month after all deductions. He rents a 1BHK in Wakad for ₹18,000 a month, sends ₹8,000 monthly to his parents in Nagpur, and is repaying a two-wheeler loan with an EMI of ₹5,500.

Here is how Rohan structures his monthly budget:

| Category | Item | ₹ Monthly |

|---|---|---|

| Essentials | Rent | ₹18,000 |

| Essentials | Parents’ support | ₹8,000 |

| Essentials | Groceries and household | ₹6,000 |

| Essentials | Utilities and mobile | ₹2,500 |

| Essentials | Petrol and transport | ₹2,500 |

| Loan | Two-wheeler EMI | ₹5,500 |

| Safety | Health insurance (monthly share) | ₹800 |

| Safety | Emergency fund top-up | ₹5,000 |

| Investment | Monthly SIP — equity mutual fund | ₹12,000 |

| Annual buffer | Set aside monthly (travel, insurance, fees) | ₹5,700 |

| Lifestyle | Dining, subscriptions, leisure | ₹9,000 |

Rohan’s essentials — rent, parents’ support, groceries, transport, and utilities — total ₹37,000, about 49% of in-hand salary. His loan EMI is a further 7%. After all fixed costs, safety, and investment contributions, he has ₹9,000 for discretionary spending. His ₹12,000 SIP, if continued for 15 years, has the potential to build meaningful wealth — though mutual fund investments are subject to market risks and past performance does not guarantee future returns. The discipline comes from treating that ₹12,000 as a committed cost on day one, not leftover money.

How to Calculate Your ₹75,000 Salary Budget

A simple five-step approach gives you a personalised monthly plan:

Savings Available = Monthly In-Hand Salary − Fixed Essentials − Total EMI − Lifestyle Budget

Step 1: Confirm your actual in-hand salary from your last bank credit or salary slip — not your CTC or an estimated figure.

Step 2: List every fixed essential: rent, groceries, utilities, school fees or parents’ support, transport, and insurance premiums. Add them up. This is your non-negotiable monthly floor.

Step 3: Add your total monthly EMI across all loans. If this combined with rent crosses 50% of in-hand salary, your budget has very little margin for errors.

Step 4: Assign a savings and investment target — minimum 20% of in-hand salary. Split it between emergency fund top-up (until you reach 3–6 months of expenses) and SIP. Use the emergency fund amount calculator to find your exact personal target before increasing investments.

Step 5: Whatever remains after Steps 2, 3, and 4 is your real lifestyle budget. Spend freely within that number — but not beyond it.

| Scenario | Key Inputs | Savings Available |

|---|---|---|

| Low rent, no EMI | Rent ₹12,000 — no loan | ~₹28,000–₹30,000 |

| Average rent, moderate EMI | Rent ₹18,000 — EMI ₹10,000 | ~₹18,000–₹22,000 |

| High rent, heavy EMI | Rent ₹25,000 — EMI ₹18,000 | ~₹5,000–₹8,000 |

These figures assume moderate groceries (₹6,000–₹8,000), utilities (₹2,000–₹3,000), and transport (₹2,500). Adjust for your city and family size. The high-rent, heavy-EMI scenario leaves almost nothing for savings — a situation that needs restructuring before adding any investment obligation.

Comparison: Budget Models for Different ₹75,000 Salary Situations

| Profile | Illustrative Monthly Allocation | Best For |

|---|---|---|

| Single, Tier-2 city or shared flat | Needs ₹28,000 | Wants ₹15,000 | Savings ₹32,000 | Aggressive wealth building and goal-based investing |

| Single, metro with average rent | Needs ₹40,000 | Wants ₹12,000 | Savings ₹23,000 | Balanced metro budget with steady SIP habit |

| Married couple, one income | Needs ₹46,000 | Wants ₹9,000 | Savings ₹20,000 | Family stability with minimum investment discipline |

| EMI-heavy borrower | Needs ₹28,000 + EMI ₹20,000 | Wants ₹8,000 | Savings ₹19,000 | Debt repayment priority while protecting safety fund |

| Aggressive saver/goal-focused | Needs ₹35,000 | Wants ₹5,000 | Savings ₹35,000 | Down payment target, FIRE planning, or short-term goal |

All figures are illustrative. Actual numbers depend on your location, lifestyle, dependents, and specific goals. These models show what is possible at different levels of discipline — not what you must do.

How to Decide What’s Right for You

your rent is above ₹22,500 (30% of ₹75,000) — THEN reduce lifestyle spending first before cutting emergency savings or insurance contributions. Essentials and safety must be protected.

your total EMI across all loans exceeds ₹18,750 (25% of salary) — THEN pause new borrowing and avoid lifestyle upgrades until at least one loan is closed and the EMI burden drops.

you do not have an emergency fund of at least ₹2.25 lakh (3 months of expenses) — THEN direct your savings to building that buffer before increasing SIP contributions. Use the emergency fund amount calculator to find your exact personal target.

you have dependents who rely entirely on your income — THEN add a term life insurance premium to your essentials, and increase the emergency fund target to at least 6 months before committing to goal-based investing.

your long-term goal is 10 or more years away (retirement, child’s higher education) — THEN a monthly SIP in an equity mutual fund is a reasonable vehicle to consider after your safety needs are covered. Mutual fund investments are subject to market risks. Past performance does not guarantee future returns.

you have a large goal within 1–2 years — like a wedding, house down payment, or vehicle purchase — THEN park savings in a liquid fixed deposit or short-term debt fund, not in equity SIPs that can fall 20–30% in a poor market year.

you have adequate insurance, a full emergency buffer, and zero high-cost debt — this article’s general framework is a starting guide only. A SEBI-registered financial planner can build a customised, goal-specific plan for your exact situation.

Common Mistakes to Avoid

Treating your full ₹75,000 as spendable money

Many earners assume their entire in-hand salary is available for spending, then wonder where it went by the 25th.

In reality, rent, EMI, insurance premiums, and family support are committed obligations — not optional. Without ring-fencing these on day one, the money quietly gets absorbed into daily spending, leaving nothing for savings at month end.

On salary day, transfer your savings and SIP amounts to separate accounts before spending a rupee on lifestyle.

Taking EMI based only on bank eligibility

A lender may approve a personal loan EMI of ₹20,000–₹25,000 on a ₹75,000 in-hand salary. That is their eligibility calculation — not your affordability assessment.

A ₹22,000 EMI stacked onto ₹20,000 rent leaves ₹33,000 for groceries, utilities, transport, insurance, emergency savings, and lifestyle. One medical emergency in this scenario forces either debt or SIP redemption. Review safe EMI limit guidelines before committing to any loan. Keep total EMI below 25–30% of in-hand salary as a personal rule, regardless of what the bank offers.

Investing before building an emergency fund

Starting a ₹12,000 SIP with zero emergency savings is a structural risk that looks fine until it breaks.

Without a cash buffer, any unexpected expense — a hospitalisation, a job loss, a vehicle breakdown — forces SIP redemption at whatever the market is doing that month. A ₹75,000 earner with ₹45,000 in monthly expenses needs at least ₹1.35 lakh as a liquid baseline before starting aggressive investment contributions. Build the buffer first; then invest with confidence.

Ignoring annual expenses in your monthly plan

School fees, term insurance premiums, vehicle servicing, festival gifts, and travel typically arrive as large lump sums — not monthly costs. Treating your budget as “monthly only” means these events feel like financial emergencies every time they appear.

Estimate your total annual irregular expenses and divide by 12. Set aside that amount each month in a separate account. For most ₹75,000 earners, this figure is ₹4,000–₹8,000 per month. The discipline prevents annual spends from derailing an otherwise healthy budget.

Increasing lifestyle after every salary hike

When salary moves from ₹65,000 to ₹75,000, lifestyle spending tends to increase by the same ₹10,000 within three months — a new phone, more frequent dining, faster delivery services.

A ₹5,000 monthly lifestyle upgrade costs ₹60,000 per year. Directed into an SIP instead over 15 years, that amount can compound significantly — though actual outcomes depend entirely on market performance. The rule worth adopting: increase your SIP amount first after any salary hike, then review lifestyle with what remains.

Skipping personal health insurance because the employer covers you

Employer group health insurance typically provides ₹3–₹5 lakh coverage, which may be inadequate for a private hospital admission in a metro city and disappears entirely when you change jobs.

Budget ₹600–₹1,200 per month for an individual top-up policy or standalone cover. Verify premium details directly with an IRDAI-registered insurer. Insurance is a subject matter of solicitation — read the policy document carefully before purchasing.

When This May Not Be the Right Choice

The budget framework above assumes a reasonably stable income with manageable obligations. Several situations call for a significantly different approach:

Single-income family with multiple dependents: Supporting a spouse, children, and parents on ₹75,000 alone typically pushes the essentials bucket to 65–70% of income. Saving 20–25% may not be realistic without making structural changes to costs — relocating to a smaller city or adjusting lifestyle meaningfully.

High medical expenses or unstable employment: Chronic illness in the family, an ongoing treatment commitment, or contract or freelance work with variable income makes standard budget splits impractical. Cash flow stability and emergency reserves take priority over investment habits during these periods.

Existing high-cost debt: Credit card revolving interest runs in the range of 36–42% per year with most Indian issuers. No equity SIP reliably beats that guaranteed cost. Clearing expensive debt first is almost always the right financial move before routing money to investments.

A major near-term goal within 1–2 years: House down payment, a wedding, or a significant medical procedure requires capital in safe, liquid form — not equity exposure that can swing 20–30% in either direction at short notice.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Budgeting principles are largely stable, but several figures referenced in this article — EPF contribution rates, income tax slabs, mutual fund regulations, and insurance premium rules — can change with each Union Budget or regulatory update.

- Income Tax Department (incometax.gov.in): Tax slabs, standard deduction amounts, Section 80C limits, and the tax treatment of EPF withdrawals.

- EPFO (epfindia.gov.in): Employee PF contribution rate, employer contribution split, and withdrawal eligibility rules.

- RBI (rbi.org.in): Lending rate guidance, home loan and personal loan interest rate policies, and credit regulation.

- SEBI (sebi.gov.in): Mutual fund regulations, SIP guidelines, and SEBI-registered investment adviser requirements.

- IRDAI (irdai.gov.in): Health and life insurance product rules, insurer registration verification, and premium regulation.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Automate savings the moment your salary arrives. Set a standing instruction on your salary account to sweep ₹15,000–₹20,000 to a separate savings account on the 1st or 2nd of every month. SIP mandates also deduct automatically. What you never see in your spending account, you do not spend.

- Open a dedicated bills account. Route rent, EMI auto-debit, insurance premium, and utility bill payments from a separate zero-balance or basic savings account. Fund it with your essentials budget on salary day. Your main account then shows only discretionary money — making overspending immediately obvious.

- Do a 30-minute subscription audit every quarter. OTT platforms, gym memberships, app subscriptions, and food delivery services quietly cost ₹3,000–₹6,000 per month for many urban earners. A simple review of the last two months’ bank statements typically reveals ₹1,500–₹3,000 that can move to savings or investments without any real lifestyle impact.

- Increase your SIP before your lifestyle after every salary hike. When salary increases, commit at least 50% of the increment to a higher SIP or savings target before spending it on anything else. Routed into a monthly SIP and sustained over 15 years, even small increments compound meaningfully — though mutual fund investments are subject to market risks and past performance does not guarantee future returns. Read about SIP basics explained if you are new to starting an investment habit from your salary.

- Create a sinking fund for annual expenses. Insurance premiums, vehicle servicing, travel, and festive spending hit in irregular lumps that feel like budget emergencies. Divide your estimated annual irregular costs by 12 and set that amount aside monthly. For most ₹75,000 earners, this is ₹4,000–₹7,000 per month. It transforms large annual costs into manageable monthly allocations.

- Review your budget every 3–6 months. A budget built in January may be irrelevant by June if rent changes, a family member is added, or an EMI closes. Schedule a 30-minute budget review every quarter — compare actual spending to your plan, adjust category limits, and reset SIP amounts if income has changed.

Frequently Asked Questions

How much should I save from a ₹75,000 monthly salary?

A practical savings target is 20–25% of in-hand salary — roughly ₹15,000 to ₹18,750 per month — covering your emergency fund top-up, insurance, and SIP combined. If fixed costs are genuinely high, starting with even ₹8,000–₹10,000 saved consistently every month is a meaningful foundation. The figure matters less than the consistency and the habit of saving before spending.

How much rent is safe on a ₹75,000 salary?

A widely used rent-to-income benchmark is 25–30% of take-home salary. On ₹75,000, that means a comfortable rent range of ₹18,750–₹22,500 per month. Beyond ₹25,000 in rent, savings and emergency fund contributions face significant pressure. If your city forces higher rent, the trade-off must come from discretionary spending — not from insurance or emergency fund allocations.

How much EMI is safe on a ₹75,000 salary?

Most financial guidelines suggest keeping total EMI below 30–40% of in-hand salary. On ₹75,000, the ceiling is roughly ₹22,500–₹30,000. However, this is the maximum ceiling — not a target. When combined with rent, the sum of rent and total EMI should ideally stay below 50% of salary. If it crosses 55%, your budget has very little cushion for emergencies, health costs, or income disruptions.

Can I invest ₹20,000 per month from a ₹75,000 salary?

Yes — if your fixed essentials plus total EMI total under ₹43,000 per month, investing ₹20,000 monthly is achievable. But ensure your emergency fund (at least 3 months of expenses) is already in place before directing this much to investments. Deploying ₹20,000 in SIPs without a cash buffer means any emergency forces you to redeem investments, potentially at a market low.

Is the 50/30/20 rule practical for India?

For earners in metro cities with rent above ₹20,000, the strict 50/30/20 rule is difficult to follow. It works well for earners with low rent — those in shared accommodation, home-owning families, or Tier-2 city residents. A more realistic starting split for many Indian salaried earners is 55–65% needs, 10–15% wants, and 20–25% savings. The rule is a useful framework, not a rigid formula. Adjust it to your city, family size, and obligations without guilt.

Should I save first or invest first from my salary?

Save first — meaning build your emergency fund before committing heavily to market-linked investments. Savings in liquid form are your safety net; investments carry market risk and some carry lock-in periods. Once you have 3–6 months of expenses in a liquid account and adequate insurance in place, you can confidently increase SIP contributions. Think of it as safety first, then growth. Neither cancels the other — they have different roles and both matter.

What happens if my expenses increase and I cannot save?

First, identify whether the increase is temporary or structural. A one-month shortfall is manageable with a small buffer. If expenses have permanently increased — new EMI, new dependent, higher rent — you need to restructure the budget by cutting a discretionary category, not eliminating savings entirely. Cutting savings to zero is the last resort. Reducing savings temporarily to ₹5,000 while addressing the expense cause is a better response than abandoning the habit.

Can I buy a house in a metro city on a ₹75,000 monthly salary?

It depends on down payment size and property value. Banks may approve a home loan in the range of ₹35–₹50 lakh on ₹75,000 in-hand salary at prevailing interest rates, but the resulting EMI of approximately ₹28,000–₹40,000 (depending on tenure and rate) consumes a very large share of income — leaving minimal room for savings, emergency fund, and lifestyle. A larger down payment, a longer savings window, or a co-borrower arrangement typically makes the purchase more manageable. Verify current home loan rates with RBI-regulated lenders before planning.

Final Verdict

A 75000 monthly salary budget can genuinely support a comfortable life, meaningful savings, and consistent investment growth — if you prioritise in the right order. Control rent to 25% of income, keep total EMI within 25–30%, build your emergency fund before scaling SIP contributions, and treat lifestyle spending as what remains after obligations and savings — not as the first claim on your income.

The biggest financial risk at ₹75,000 is not the salary level — it is lifestyle inflation and reactive spending silently consuming the surplus you worked to earn. A consistent ₹10,000–₹15,000 monthly SIP, started early and sustained without interruption, builds real wealth over a 10–15 year horizon. Mutual fund investments are subject to market risks and past performance does not guarantee future returns.

Start by confirming your actual in-hand pay using the take-home pay estimate calculator, list your fixed expenses on paper, assign savings before anything else, then review every three to six months as your income and obligations evolve. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.