₹50,000 lands in your account on salary day — and within 72 hours, the rent is gone, the EMI auto-payment goes through, and the grocery bill is already waiting. By the 15th, you are staring at ₹6,000 left and wondering where the rest disappeared. That experience is what a 50000 monthly salary budget feels like without a clear plan.

This guide treats ₹50,000 as your monthly take-home pay — the actual amount credited after PF, professional tax, and TDS deductions. If ₹50,000 is your CTC or gross salary, your in-hand figure will be lower, and that gap matters for every number in this plan. A single person renting in Pune, a couple managing household costs in Hyderabad, and a borrower already paying an EMI all need different splits. All three situations are covered here — with specific rupee amounts, not just ratios.

Quick Answer: 50000 Monthly Salary Budget

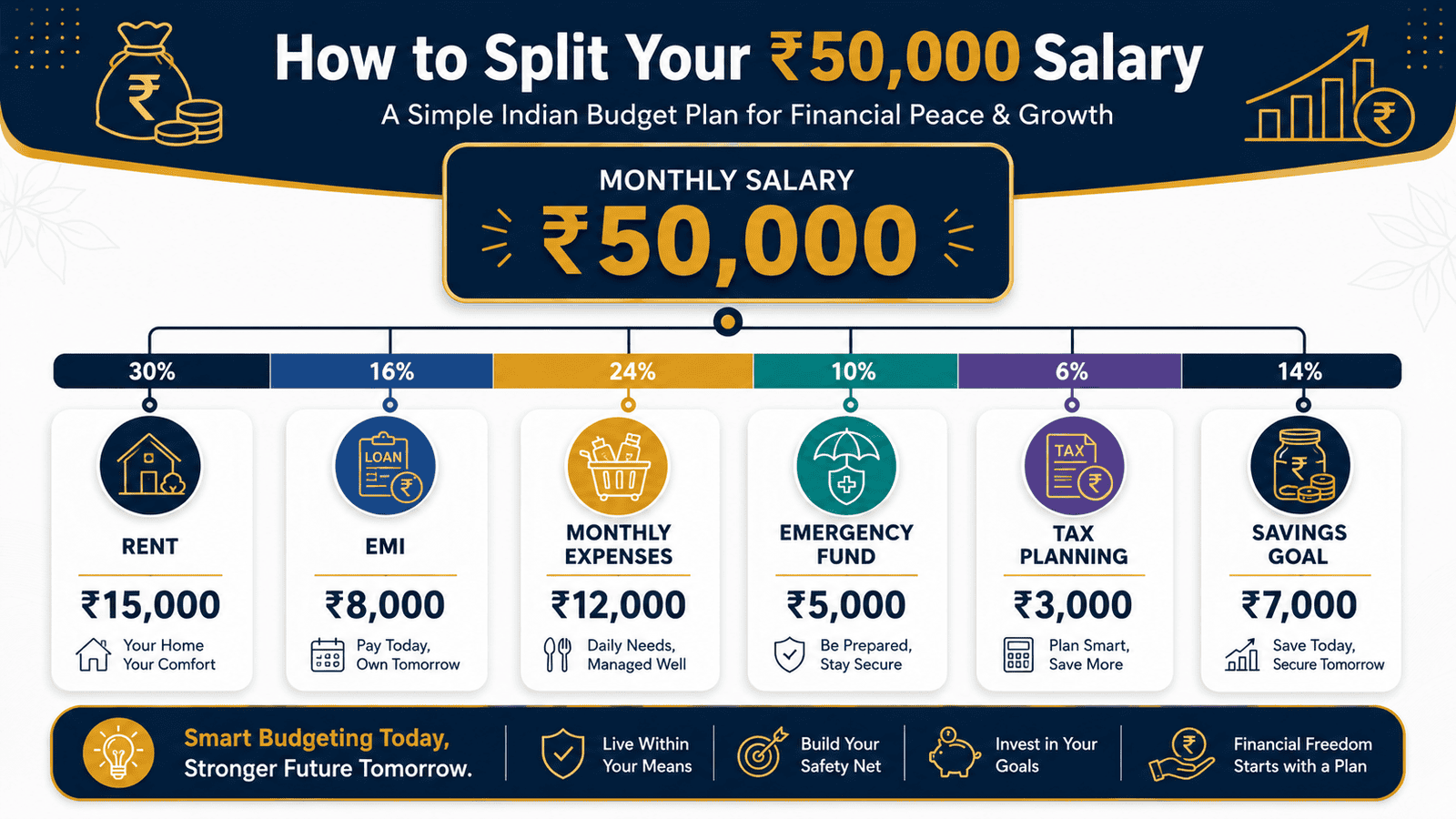

A 50000 monthly salary budget should first cover essentials, then limit rent and EMI before lifestyle spending. A practical split is ₹15,000–₹18,000 for rent, ₹8,000–₹12,000 for groceries and bills, EMI below ₹10,000, and at least ₹5,000–₹8,000 for savings, adjusted for tax, PF and family needs.

Key Takeaways

- Rent should stay within 30–35% of take-home — on ₹50,000 in hand, that means keeping it below ₹17,500 per month.

- Combined EMI across all active loans should stay under ₹10,000; lenders may approve higher amounts, but your household cash flow may not survive them.

- A ₹50,000 gross salary is not ₹50,000 take-home — EPF deductions alone can reduce your monthly credit by ₹2,400 to ₹3,600 depending on your basic salary structure.

- Savings must be the first fixed transfer on salary day — not whatever is left after spending; even ₹5,000 per month invested consistently compounds meaningfully over time.

- Build a ₹75,000–₹1,50,000 emergency fund before committing to any new loan EMI — that is three to six months of your essential monthly expenses.

- The 50/30/20 rule applied to Indian conditions means ₹25,000 for needs, ₹10,000 for savings, ₹15,000 for wants — but rent above ₹15,000 breaks this split immediately in most Tier-1 cities.

- Checking which income tax regime reduces your TDS — old or new — can improve your monthly take-home by ₹3,000–₹5,000 per year without any change in your gross salary.

Key Facts at a Glance

| Budget Category | Suggested Range | Notes |

|---|---|---|

| Monthly income assumed | ₹50,000 (take-home) | Deduct PF, professional tax, TDS from gross first |

| Rent | ₹12,000–₹18,000 | 30–36% of take-home; varies sharply by city |

| Groceries and household bills | ₹6,000–₹10,000 | Higher for families or Tier-1 cities |

| Utilities (electricity, gas, internet) | ₹1,500–₹3,000 | Shared accommodation reduces this significantly |

| Transport and commute | ₹1,500–₹3,000 | Public transport vs personal vehicle matters |

| Insurance (term + health) | ₹1,000–₹2,500 | Monthly equivalent of annual premiums |

| Combined EMI ceiling (all loans) | Below ₹10,000 | 20% of take-home is a safe personal maximum |

| Savings and investments | ₹5,000–₹10,000 | Automate on salary day; treat as non-negotiable |

| Family support or remittance | ₹2,000–₹5,000 | Applicable for a significant share of salaried workers |

| Lifestyle and discretionary | ₹3,000–₹6,000 | What remains after all commitments; filled last |

How to Build a 50000 Monthly Salary Budget That Actually Works

Your Real Take-Home Is Not Your CTC or Gross Salary

Before allocating a single rupee, you need one number: your actual take-home pay. Not your CTC. Not the figure on your offer letter. The real amount that lands in your bank account each month.

For most salaried employees in India, three deductions reduce the gross salary before it reaches you. The employee EPF contribution — typically 12% of basic salary — is deducted at source. Professional tax of ₹150–₹200 per month applies in most states. And TDS is deducted based on your declared tax regime and investment proofs. If your basic salary is ₹25,000 within a ₹50,000 gross package, the EPF deduction alone is ₹3,000 per month. Add professional tax and even a modest TDS amount, and your take-home could be ₹44,000–₹46,500 — not ₹50,000. Use the monthly in-hand pay calculator to arrive at your precise figure before you build any budget.

Rent: The Number That Controls Everything Else

Rent is the most powerful line item in any monthly budget for a salaried person. Once set, it is fixed — it does not reduce when your other expenses spike. A widely used guideline keeps rent within 30% of take-home pay. On ₹50,000 in hand, that means staying under ₹15,000 per month.

In Tier-1 cities — Bengaluru, Mumbai, Delhi NCR, Pune — a decent 1BHK starts at ₹16,000–₹22,000. If you are paying above ₹17,500 in rent, the excess must come from lifestyle spending, not from savings or insurance. Rent above 40% of take-home — ₹20,000 or more on this income — leaves almost no structural room for the rest of the budget. Moving to shared accommodation, a PG, or a location further from the city centre can recover more financial headroom than any budgeting system you adopt.

HRA — House Rent Allowance — is part of most salary structures and provides partial tax relief on rent paid. If your salary slip includes an HRA component and you pay rent, verify whether you are eligible for HRA exemption under the old tax regime with your employer’s payroll team or a registered tax professional.

EMI: What the Lender Approves and What Your Budget Can Survive Are Two Different Things

This distinction costs many salaried borrowers thousands of rupees every month. Banks and NBFCs calculate loan eligibility at 40–50% of gross monthly income — their threshold exists to protect the lender’s repayment exposure. It does not account for your rent, groceries, utilities, insurance, family support, or savings.

On a ₹50,000 take-home, fixed essential costs — rent, food, utilities, transport, and insurance — typically total ₹25,000–₹30,000. An EMI of ₹15,000 on top of that leaves just ₹5,000–₹10,000 for savings, emergencies, and everything variable. One hospitalisation or vehicle breakdown breaks the month entirely. A sensible personal ceiling for combined EMI is 20% of take-home — approximately ₹10,000 on ₹50,000 in hand.

The 50/30/20 Rule and Why Indian Households Need to Adjust It

The 50/30/20 rule divides income into needs (50%), wants (30%), and savings (20%). On ₹50,000 take-home, that would allocate ₹25,000 to needs, ₹15,000 to lifestyle, and ₹10,000 to savings. The split sounds clean — until Indian household realities enter the calculation.

Rent above ₹15,000 already pushes the needs bucket past 50% before a single grocery item is counted. Add utilities, transport, insurance, and any family support obligation, and the needs bucket reaches ₹28,000–₹33,000 in most Indian cities. The framework is still useful as a starting orientation — but in practice, a more Indian-appropriate version looks like: essentials at 55–60%, savings locked at 10–15% on salary day, and lifestyle spending as whatever remains. Protecting the savings allocation matters more than maintaining the exact 50/30/20 ratio.

Savings and Insurance: Non-Negotiable Allocations

The most common savings mistake among salaried employees at this income level is saving whatever is left at month-end. Some months, the answer is nothing. The fix is automating a fixed transfer on salary day — to a recurring deposit, a monthly SIP, or even a separate savings account — before any discretionary spending happens. At ₹50,000 take-home, ₹5,000–₹7,000 per month in savings is realistic for most single earners. Families may find ₹3,000–₹5,000 more sustainable while covering essential household costs.

Insurance is not optional for anyone with dependents or outstanding loans. A term plan premium for a healthy 29-year-old non-smoker can be as low as ₹700–₹1,200 per month for ₹50 lakh coverage. A personal health insurance policy of ₹3–5 lakh cover adds ₹500–₹1,000 per month. These are small recurring costs relative to the financial risk of carrying neither. As per IRDAI guidelines, insurance is a subject matter of solicitation — read any policy document carefully before purchase.

Real Example: Three Versions of Rohit’s ₹50,000 Budget

Rohit, 29, is an operations executive in Pune. His gross salary is ₹50,000 per month. After EPF employee contribution (12% of basic salary ₹25,000 = ₹3,000) and professional tax (₹200), his take-home is approximately ₹46,500 — before any TDS, which varies by regime choice and investment declarations. Here is how the same income plays out across three real-life situations.

Before reading these breakdowns, check your own salary slip deductions to confirm which components apply to your salary structure — PF, HRA, special allowance, and TDS rules differ across employers.

| Expense Category | Single Renter (Pune) | Family of Three (Hyderabad) |

|---|---|---|

| Rent | ₹13,000 | ₹15,000 |

| Groceries and household | ₹5,500 | ₹9,000 |

| Utilities (electricity, gas, internet) | ₹2,000 | ₹2,500 |

| Transport and commute | ₹2,000 | ₹2,000 |

| Insurance (term + health) | ₹1,200 | ₹2,000 |

| Personal loan EMI | ₹8,000 | ₹8,000 |

| Family support / school fees | ₹2,500 | ₹4,000 |

| Savings and investments | ₹7,000 | ₹3,000 |

| Lifestyle and discretionary | ₹5,300 | ₹1,000 |

| Total | ₹46,500 | ₹46,500 |

The key insight: at the same income, the single renter keeps ₹7,000 for savings and ₹5,300 for lifestyle. The family of three has ₹3,000 for savings and ₹1,000 for discretionary spending — with almost no buffer for surprises. A borrower who adds a second EMI of ₹8,000 to the single-renter budget would find savings collapsing to below ₹2,000 per month and lifestyle spending disappearing entirely.

How to Calculate Your Monthly Budget in Five Steps

Lifestyle Budget = Take-Home − Fixed Essentials − EMI − Savings Target

Step 1: Start with your actual take-home — not CTC, not gross. Subtract EPF, professional tax, and TDS to arrive at the credited figure. For Rohit: ₹46,500.

Step 2: Total all fixed essentials — rent, groceries, utilities, transport, insurance, and any recurring family support. For Rohit (single): ₹25,200.

Step 3: Add your combined EMI across all active loans. Rohit has one personal loan: ₹8,000. Keep this below 20% of take-home if possible. Read the detailed framework for the safe EMI limit before taking on new debt.

Step 4: Lock in a savings target and treat it as a fixed cost. Rohit’s target: ₹7,000.

Step 5: What remains is the lifestyle budget. Rohit: ₹46,500 − ₹25,200 − ₹8,000 − ₹7,000 = ₹6,300. That is the real discretionary number — and the ceiling for eating out, streaming, clothing, and personal spending.

| Scenario | Key Inputs | Lifestyle Budget Left |

|---|---|---|

| Single renter, one EMI | Rent ₹13k, EMI ₹8k, Savings ₹7k, Essentials ₹25k | ₹3,500–₹6,500 |

| Family earner, higher essentials | Rent ₹15k, Essentials ₹29k, Savings ₹3k, EMI ₹8k | ₹500–₹2,000 |

| Borrower with two EMIs | Rent ₹13k, Total EMI ₹16k, Savings ₹3k, Essentials ₹25k | Negative or near zero |

Comparison: Four Budget Models for a ₹50,000 Take-Home

| Budget Model | What It Looks Like | Main Risk |

|---|---|---|

| 50/30/20 Standard | ₹25k needs, ₹15k lifestyle, ₹10k savings | Only works if rent is below ₹13,000 — impractical in most metros |

| Rent-heavy city model | ₹20k+ rent, ₹5k lifestyle, ₹3k savings | Savings permanently squeezed; any expense spike empties the account |

| EMI-heavy borrower | ₹13k rent + ₹15k EMIs, ₹2k–₹3k savings | Very high — no buffer for emergencies; missed EMI risks credit score damage |

| Family responsibility model | ₹15k rent + ₹5k family support, ₹3k–₹5k savings | Lifestyle nearly eliminated; sustainable only with strict month-to-month discipline |

How to Decide What’s Right for You

You live with parents and pay no rent — allocate ₹12,000–₹15,000 per month to savings and investments immediately. Use this period to build your emergency fund and start a long-term SIP before independent living begins. See how much you need to accumulate with the emergency fund target calculator.

You rent in a Tier-1 city and your rent exceeds ₹17,000 — your savings are structurally under pressure. Any salary increment should restore the savings allocation to at least 10% before it touches lifestyle spending. Shared accommodation is worth serious consideration.

You are married with one child and ₹50,000 take-home — this is a tight but workable budget if rent stays below ₹15,000 and no new EMI is added. A family health insurance policy becomes non-optional. School fees need to be divided into a monthly provision, not treated as a lump-sum surprise.

You already carry a personal loan or vehicle EMI — do not add a second loan until the first is cleared, unless the new loan replaces the existing one at a meaningfully lower interest rate. Two EMIs totalling above ₹15,000 on this income creates a budget with no recovery room.

Your income is variable or bonus-driven — build your monthly budget on the base salary only. Bonuses should go toward the emergency fund, loan prepayment, or a lump-sum investment — not lifestyle costs that become permanent monthly commitments.

Standard ₹50,000 budget frameworks do not work well if your city rent exceeds ₹20,000, you support elderly parents with ongoing medical costs, or you carry high-interest debt above ₹4 lakh outstanding. In these cases, the budget needs significant restructuring — and guidance from a qualified financial planner may be more useful than a general framework.

Common Mistakes to Avoid

Borrowing Based on Lender Eligibility, Not Budget Capacity

A bank may approve a personal loan with an EMI of ₹18,000 on a ₹50,000 monthly salary because their eligibility formula is based on gross income, not your post-rent cash flow.

If your actual budget has only ₹8,000–₹10,000 of EMI headroom, accepting a ₹18,000 EMI creates a monthly shortfall of ₹8,000–₹10,000 — every single month for the loan tenure. That gap is typically filled with credit card spending, which compounds the problem.

Run the five-step budget calculation before applying for any loan. Your cash flow capacity is the real borrowing limit, not the bank’s sanction letter.

Saving Whatever Is Left at Month-End

This approach almost always produces zero savings. UPI payments, food delivery, streaming subscriptions, and informal social spending expand to fill whatever income is available.

Over 12 months of skipping a ₹5,000 monthly savings target, the opportunity cost is ₹60,000 — plus any investment growth foregone. The fix is a standing instruction on salary day that moves savings before any spending begins.

Even ₹3,000 per month, automated from day one, builds a meaningful corpus over three to five years.

Ignoring Annual Expenses in the Monthly Plan

Vehicle insurance, health policy renewal, festive purchases, school fee instalments, and annual travel do not appear in the monthly cash flow — until they arrive and empty the account.

Estimate your total annual irregular expenses, divide by 12, and set that amount aside each month in a recurring deposit or separate savings account. For ₹36,000 in annual irregular costs, that is ₹3,000 per month — small enough to manage but decisive enough to prevent budget crises.

Treating Credit Card Limit as Available Income

A ₹1.5 lakh credit card limit can feel like a financial cushion — until revolving balances at 36–42% effective annual interest turn manageable spending into a debt trap.

Use credit cards for cashback and convenience, but clear the full outstanding every month without exception. If you currently carry a revolving balance, treat its clearance as an EMI with a fixed monthly payment — and do not start new investments until the high-interest debt is eliminated.

Confusing CTC with Take-Home Pay

Many salaried employees build budgets on their CTC — the figure on the offer letter — not their take-home. The difference includes the employer’s EPF contribution (also 12% of basic, part of CTC but never credited to your account), gratuity provisioning, and other CTC components that never reach you monthly.

A ₹50,000 CTC package can produce a take-home of ₹41,000–₹44,000 after all deductions. Budgeting from the CTC figure creates a structural monthly deficit from day one.

Skipping Insurance to Free Up Monthly Cash

Cutting a ₹900 monthly term plan premium to gain ₹10,800 per year in spending money is trading a small certain cost for a potentially catastrophic uncertain one — particularly if you carry loan EMIs or have dependents.

Insurance is not savings and cannot be compared to investment returns. It eliminates a specific financial risk. Buy the minimum adequate coverage now and increase it as your income grows.

When This May Not Be the Right Choice

Standard ₹50,000 budgeting frameworks may not apply cleanly in these situations:

High-rent metro living: If your rent alone exceeds ₹20,000 — as it can in central Mumbai, South Delhi, or parts of Bengaluru — the entire framework breaks before groceries are even counted. A different locality, shared accommodation, or a longer commute from a more affordable area may deliver more financial benefit than any budgeting technique.

Single income supporting a family with medical costs: If you are the sole earner for elderly parents requiring regular treatment or medication, a standard budget does not have room for both adequate insurance and normal savings. A family financial plan with supplementary income sources is more appropriate than optimising a tight single-income split.

Existing high-interest debt above ₹3 lakh: Personal loans at 14–18% or credit card revolving balances at 36–42% annual interest should be cleared before standard savings allocations are made. The guaranteed “return” of eliminating 36% liability exceeds most investment options at this income level.

Irregular or commission-based pay: If ₹50,000 is an average across months that range from ₹30,000 to ₹80,000, budgeting from the average creates a structural shortfall in low-income months. Build the budget on the floor income and treat all income above that floor as surplus.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Several figures affecting a ₹50,000 salary budget are set by government or regulatory bodies and can change with each Union Budget or policy update:

- Income Tax Department (incometax.gov.in): Income tax slabs, standard deduction limits, TDS calculation rules, and HRA exemption eligibility under the old and new tax regimes for salaried employees. Review the old and new regime comparison before declaring your regime choice with your employer at the start of the financial year.

- EPFO (epfindia.gov.in): EPF employee and employer contribution rates, the wage ceiling for mandatory PF applicability, and withdrawal and transfer rules. The 12% employee contribution on basic salary is the current standard — but contribution bases and thresholds are subject to regulatory revision.

- RBI (rbi.org.in): Responsible lending guidelines, debt-to-income norms, and regulatory framework for bank and NBFC lending. Loan interest rates, EMI eligibility norms, and processing fee structures vary by lender and are subject to RBI oversight.

- SEBI (sebi.gov.in): Regulatory standards for mutual funds, investment advisors, and stock brokers. Any investment advice should come from a SEBI-registered professional.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- On salary day, set up two automatic transfers before spending anything: one to your savings or investment account, one to a dedicated bills account for rent, utilities, and EMI. What remains in your primary account is your entire lifestyle budget for the month.

- If your rent exceeds 35% of take-home, prioritise rent reduction over any new investment or spending upgrade. Cutting rent by ₹2,000 per month saves ₹24,000 per year — a number that outperforms many investment options at this income level in terms of certainty.

- Before signing any loan agreement, apply the three-number test: rent + all existing EMIs + new EMI should not exceed 55% of take-home. If it does, your cash flow will not absorb a single month of unexpected costs.

- Divide your total annual irregular expenses — insurance renewals, vehicle servicing, festive purchases, travel — by 12, and save that amount each month in a separate recurring deposit. This eliminates budget-breaking surprise expenses and prevents you from treating irregular costs as emergencies.

- Check your tax regime choice with your employer’s payroll team at the start of every financial year. Declaring the more beneficial regime reduces TDS deductions and improves monthly take-home without any change in gross salary — a zero-effort improvement to your cash flow. Verify the applicable slabs at incometax.gov.in before deciding.

- If you carry any credit card revolving balance, treat the outstanding amount as a loan with a fixed monthly payment target. Credit card interest at 36–42% annually erodes budget discipline faster than any other financial mistake at this income level. For a complete implementation framework, follow our monthly budget steps guide once the high-cost debt is cleared.

Frequently Asked Questions

How much rent is safe on a ₹50,000 monthly salary?

If ₹50,000 is your take-home, keeping rent below ₹15,000–₹17,500 — 30–35% of income — leaves enough room for groceries, utilities, transport, insurance, an EMI, and some savings. In Tier-1 cities where 1BHK rents start at ₹16,000+, rent above this range requires cutting lifestyle spending significantly to protect the savings allocation. Rent above ₹20,000 on ₹50,000 take-home creates a structurally compressed budget with no margin for unplanned expenses.

How much EMI is safe on a ₹50,000 monthly salary?

A safe personal ceiling for combined EMI across all active loans is 20% of take-home — approximately ₹10,000 on ₹50,000. Lenders may approve significantly more based on gross income eligibility criteria, but your actual cash flow after rent, food, utilities, and insurance may not survive an EMI above ₹12,000–₹13,000 at this income level. Always calculate the post-EMI budget before accepting a loan, not after.

Can I save money from a ₹50,000 monthly salary?

Yes — but only if savings are treated as the first fixed allocation on salary day, not whatever is left after spending. A single renter with controlled rent and one manageable EMI can realistically save ₹5,000–₹8,000 per month. A family with higher essential costs may find ₹3,000–₹5,000 more realistic. Zero savings is almost always a result of spending filling the available income before a savings transfer is made — not of income being genuinely insufficient.

Is the 50/30/20 budget rule practical in India on this salary?

It is a useful starting framework but rarely works exactly as stated. The 50% needs bucket of ₹25,000 only works if rent is below ₹13,000 — which is uncommon in most Tier-1 cities. In practice, Indian households at this income level work better with needs at 55–60%, savings locked in at 10–15% on salary day, and lifestyle spending as the residual. Protecting the savings percentage matters more than adhering precisely to 50/30/20 ratios.

How should a family manage ₹50,000 monthly income?

A family of three on ₹50,000 take-home faces significant pressure. Rent, groceries, utilities, school fees, and insurance can consume ₹36,000–₹40,000. The family model works best by: keeping rent below ₹15,000, maintaining a family health insurance policy, automating at least ₹3,000 in savings per month, and avoiding new EMIs unless existing ones are cleared. Every salary increment should first restore savings to at least 10% before any lifestyle upgrade is made.

Should I invest or repay debt first on ₹50,000 salary?

It depends on the interest rate of the debt. High-interest liabilities — personal loans at 14–18% or credit card revolving balances at 36–42% annually — should be cleared before starting equity investments, because eliminating a 36% guaranteed liability outperforms most market-linked options on a risk-adjusted basis. If your only debt is a home loan at 8–9% and you have no emergency fund, building a ₹75,000–₹1,00,000 emergency fund simultaneously with standard loan repayment is a reasonable approach.

What happens if my total EMI crosses ₹15,000 on ₹50,000 take-home?

After rent of ₹13,000, essential costs of ₹13,000, and EMI of ₹15,000, only ₹5,000–₹9,000 remains for savings, insurance, and lifestyle. That leaves almost no buffer. A hospitalisation, a vehicle repair, or even a delayed salary can trigger a cash shortfall requiring either loan default or fresh borrowing — both of which worsen the financial position. Run the five-step calculation in this article before crossing ₹12,000 in combined EMI.

Is ₹50,000 monthly salary enough for a single person in a metro city?

It is manageable in most Tier-2 cities and affordable parts of Tier-1 cities outside central business districts. The critical variable is rent — a 1BHK in prime Bengaluru, Mumbai, or Delhi can cost ₹18,000–₹25,000, consuming 36–50% of take-home before a single other expense. Shared accommodation, PG arrangements, or locations with better rent-to-commute ratios make ₹50,000 significantly more workable in metro cities.

Can I get a home loan on ₹50,000 monthly salary?

Most banks and housing finance companies will consider a home loan application at ₹50,000 gross monthly income. The sanctioned loan amount, applicable interest rate, and EMI will depend on your credit score, existing liabilities, property value, co-applicant income if applicable, and individual lender policies. Loan approval depends on lender discretion and is not guaranteed. More importantly, verify that the proposed EMI fits within your monthly budget before applying — bank approval and financial sustainability are separate questions.

How much should I keep in an emergency fund on ₹50,000 salary?

A standard emergency fund covers 3–6 months of essential monthly expenses — not total take-home. If your essential costs (rent + food + utilities + transport + insurance + EMI) total ₹30,000 per month, a 3-month fund is ₹90,000 and a 6-month fund is ₹1,80,000. Keep this in a liquid instrument — a savings account with sweep facility or a liquid mutual fund — so it is accessible within 24–48 hours when needed. Do not invest the emergency fund in equity or fixed-term instruments.

Final Verdict

A 50000 monthly salary budget can work for a single person, a family, and a borrower — as long as rent and EMI are controlled before lifestyle spending is allowed to grow. The critical discipline is automating savings on salary day and treating that transfer as non-negotiable. Rent below 35% of take-home, combined EMI below 20%, and a savings target of at least 10% is a framework that holds across most Indian household situations at this income level.

Families will find the margin tighter — but not impossible — with rent below ₹15,000 and no new EMI commitments. Borrowers with existing EMIs above ₹12,000 should prioritise debt clearance before any lifestyle expansion. And anyone building this budget should start from their actual take-home, not their CTC or gross figure.

Use the monthly in-hand pay calculator to confirm your real take-home before finalising any budget split. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.