When your employer hands you a full-and-final settlement statement, leave encashment calculation is usually the line item you stare at longest — and understand least. Your unused earned leave is being converted into salary. But how much of it is taxable? Does it matter whether you are resigning or retiring? And is the employer even using the right formula?

These are not small questions. Get the tax treatment wrong and you could under-report income in your ITR — or overpay tax on an amount that was partly or fully exempt under Section 10(10AA) of the Income Tax Act. The rules draw a sharp line between government employees and private sector employees, and between when the encashment happens. This article walks you through the formula, the four-condition exemption test, and exactly what to verify before you sign your settlement sheet.

Quick Answer: Leave Encashment Calculation

Leave encashment calculation means converting unused earned leave into salary based on your employer’s leave policy and eligible salary. For private employees, tax exemption on retirement or resignation is limited using Section 10(10AA), including a ₹25 lakh cap, actual amount received, eligible leave salary, and 10 months’ average salary.

Key Takeaways

- Government employees (central and state) receive full tax exemption on leave encashment at retirement — no monetary cap applies under Section 10(10AA)(i).

- Private sector employees get conditional exemption at retirement or resignation, limited to the lowest of four amounts including a ₹25 lakh cumulative lifetime cap under Section 10(10AA)(ii).

- Leave encashment received during active employment is generally fully taxable for private sector employees — the exemption applies only at the point of separation from employment.

- The employer payout formula — (Eligible Salary ÷ 30) × Leave Days — is separate from the income tax exemption, which uses a four-condition test that may produce a different figure.

- The ₹25 lakh exemption cap is a cumulative lifetime limit across all employers — exemption claimed at a previous job reduces what is available to you now.

- Only earned leave (privilege leave) qualifies for encashment in most employer policies — casual leave and sick leave are not typically carried forward or encashed.

- Check the exempt allowances section of your Form 16 before filing ITR to confirm whether your employer has applied the Section 10(10AA) exemption at payroll or whether you need to claim it yourself.

Key Facts at a Glance

| Factor | Rule or Limit |

|---|---|

| What is leave encashment? | Payment for unused earned leave, based on salary and leave balance |

| Governing tax section | Section 10(10AA) — Income Tax Act, 1961 |

| Government employee exemption at retirement | Fully exempt — no monetary cap |

| Private employee exemption cap | ₹25 lakh (cumulative, across all employers, lifetime) |

| During-service encashment (private sector) | Fully taxable — no Section 10(10AA) relief |

| Legal heir (on death of employee) | Fully exempt — no tax |

| Leave type eligible for encashment | Earned leave / privilege leave (as per employer HR policy) |

| Salary used for tax exemption formula | Basic salary + Dearness Allowance — last 10 months’ average |

| Maximum leave days for exemption | 30 days per completed year of service |

| Official source | Income Tax Department — incometax.gov.in |

What Is Leave Encashment?

Every year your employer credits you with a fixed number of leave days. You take some. The rest accumulate. Most private sector companies allow employees to carry forward earned leave — typically up to 60, 90, or 120 days, depending on the organisation’s policy. When you resign, retire, or hit the carry-forward ceiling, those unused days are converted into a cash payout. That payment is called leave encashment or leave salary.

It is not a bonus or a windfall. It represents days you worked without taking leave — and your employer is now paying you for them. But how it is taxed depends entirely on your employee category, when the payment is made, and how many days are eligible.

Earned Leave vs Other Leave Types

Not all leave on your balance sheet qualifies for encashment. Most employer policies allow encashment only for earned leave — also called privilege leave or PL. Casual leave (CL) and sick leave (SL) are generally not carried forward and cannot be encashed. This distinction matters enormously in practice.

If your leave statement shows a total balance of 80 days but 25 of those are casual leave, your encashable base may only be 55 days — which directly changes your payout and your tax calculation. Always ask HR for a leave balance breakup, separated by leave type, before accepting any settlement figure. Understanding your salary breakup basics will also help you identify which pay components feed into the encashment calculation and which appear elsewhere in your settlement sheet.

How Your Employer Calculates the Payout

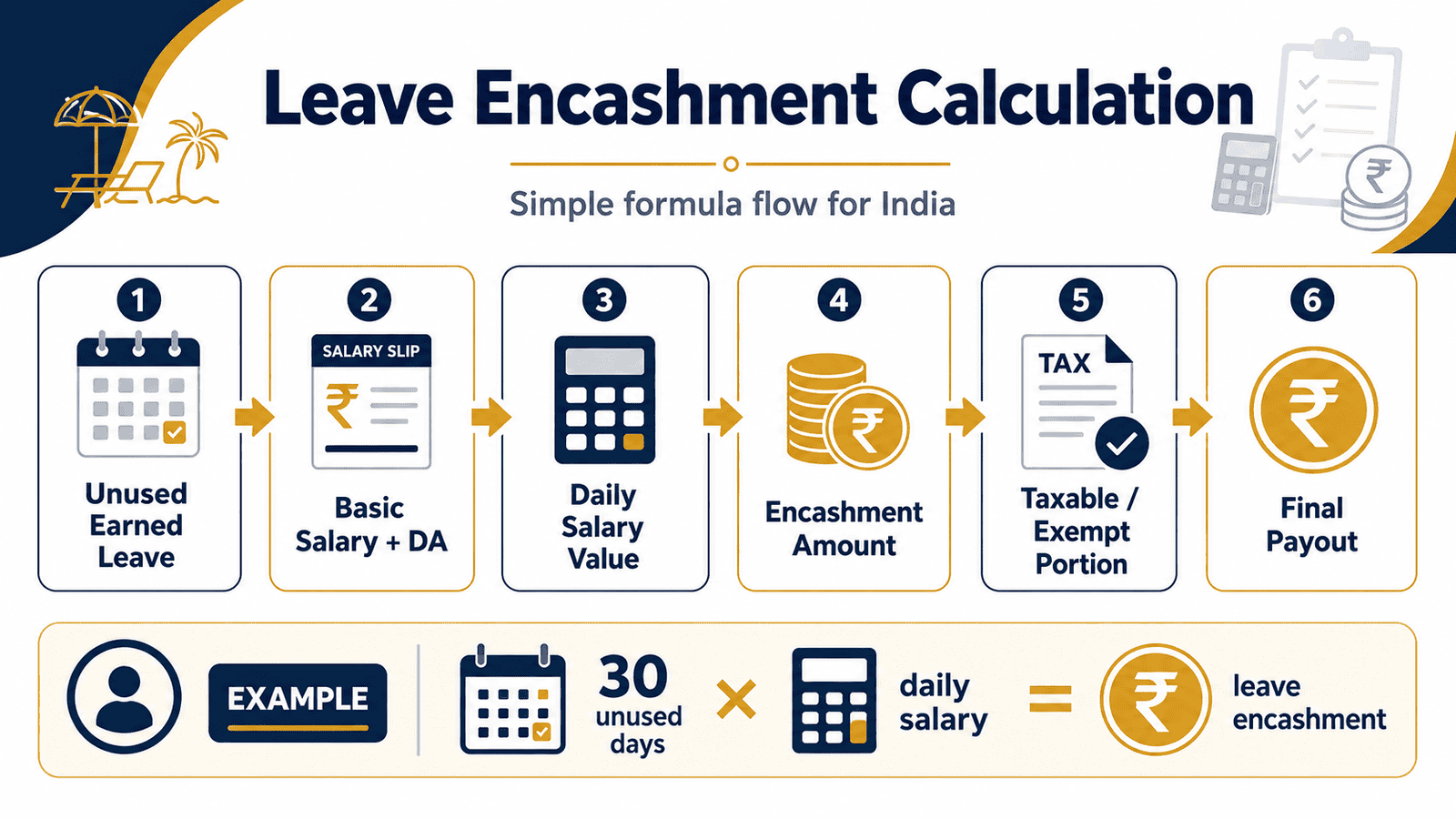

The standard payout formula used by most Indian private sector employers is:

Payout = (Monthly Basic Salary ÷ 30) × Number of Encashable Earned Leave Days

Some companies divide by 26 working days instead of 30 calendar days — which gives a higher per-day rate. The divisor used is set by your HR policy or appointment letter. In terms of which salary figure is used, most employers use only basic salary as the base — not gross salary, not CTC, not in-hand pay. Some public sector units include Dearness Allowance (DA) alongside basic.

This matters because what your employer pays you and what the income tax law exempts can be two very different numbers.

Leave Encashment Calculation: Tax Exemption Rules Under Section 10(10AA)

The employer payout and the income tax exemption are separate calculations that follow different logic. Receiving ₹2 lakh from your employer does not automatically mean ₹2 lakh is tax-free. The exempt amount is determined by a four-condition test — the lowest of the four figures is your exemption ceiling. Anything above it is taxable salary income for the assessment year in which the payment is received.

Section 10(10AA)(i) — Government Employees

For central government and state government employees, leave encashment received at retirement or superannuation is fully exempt from income tax. No monetary cap. No formula. No four-condition test. The entire payout is excluded from taxable income, regardless of the amount. According to Income Tax Department guidelines, this benefit applies specifically at retirement — not during the course of service.

Section 10(10AA)(ii) — Private Sector Employees

For private employees, the tax exemption on leave encashment received at retirement or resignation is the least of these four amounts:

- Actual leave encashment amount received from the employer

- ₹25 lakh — the aggregate lifetime cap across all employers, reduced by any Section 10(10AA) exemption already claimed at a previous employer

- 10 months’ average salary, calculated from the last 10 months immediately before the date of retirement or resignation

- Cash equivalent of earned leave to credit — computed as: (Average monthly salary ÷ 30) × Eligible leave days, subject to a maximum of 30 days per completed year of service

The taxable portion is the amount received minus the lowest of the four. This taxable balance is added to your total salary income and taxed at your applicable slab rate. Tax treatment applies based on the assessment year in which the payment is received — always verify current rules at incometax.gov.in before filing your ITR.

What Counts as “Salary” for the Exemption Calculation?

This is the most common source of confusion in the entire leave encashment calculation. For Section 10(10AA) purposes, “salary” means basic salary plus Dearness Allowance only — averaged over the last 10 months before resignation or retirement. HRA, transport allowance, performance bonus, and all other pay components are excluded.

Most private sector employees receive no DA, so eligible salary effectively equals average monthly basic pay for the last 10 months. This is often 40–50% of CTC — a significant difference that changes the exemption calculation materially if you use the wrong figure.

During-Service Encashment — The Exception That Catches People Off Guard

Some companies allow employees to encash a portion of their accumulated earned leave annually, often during festive seasons. For private sector employees, this during-service encashment is fully taxable — there is no Section 10(10AA) relief. The entire amount is added to your salary income for the financial year and taxed at your slab rate.

The exemption is specifically reserved for payments at the point of retirement, superannuation, or resignation. Central government employees do receive a partial concession on during-service earned leave encashment — but private employees do not.

Real Example: Rahul’s Full-and-Final Settlement

Rahul is 34, a Senior Analyst from Bengaluru, earning ₹18 lakh per year with a monthly basic salary of ₹72,000. He resigned after completing exactly 7 years with his employer. At the time of resignation, he had 52 days of unused earned leave. This was his first job — he had not claimed any Section 10(10AA) exemption before.

His employer calculated the payout using the standard formula. Understanding the role of basic pay impact helps clarify why the employer uses basic salary — not CTC — as the base for this calculation.

Employer payout: (₹72,000 ÷ 30) × 52 = ₹2,400 × 52 = ₹1,24,800

Four-condition tax exemption test:

- Actual amount received: ₹1,24,800

- ₹25 lakh lifetime cap: ₹25,00,000

- 10 months’ average basic salary: ₹72,000 × 10 = ₹7,20,000

- Eligible leave salary: (₹72,000 ÷ 30) × 52 days = ₹1,24,800 (52 days is well within the 7 × 30 = 210-day maximum)

The lowest of the four conditions is ₹1,24,800 — which equals the actual amount received. Rahul’s entire leave encashment is exempt from income tax. Taxable portion: ₹0. The key insight: when your leave balance is moderate and your basic salary is not very high, the full payout often qualifies as completely exempt at resignation.

How to Calculate Leave Encashment

Two calculations matter here: what your employer pays, and what the income tax law exempts. They follow different logic and will often produce different numbers.

Employer Payout Formula

Leave Encashment Payout = (Monthly Basic Salary ÷ 30) × Number of Encashable Earned Leave Days

Confirm the divisor with HR — some organisations use 26 working days, which increases the per-day payout rate.

Tax Exemption Formula — Private Employees

Exempt Amount = Least of: (a) Actual amount received | (b) ₹25 lakh cap | (c) 10 months’ average salary | (d) Eligible leave salary

For condition (d): Eligible Leave Salary = (Average monthly salary ÷ 30) × Leave days encashed, subject to a ceiling of 30 days × Completed years of service

Taxable leave encashment = Amount received minus the exempt amount. This taxable portion is added to your total income for the assessment year. For a full walkthrough of how this flows into your annual tax position, refer to taxable salary meaning.

Worked Scenarios

| Scenario | Key Inputs | Tax Result |

|---|---|---|

| Rahul — 52 days, ₹72K basic, 7 years | Payout ₹1,24,800 | All four conditions ≥ ₹1,24,800 | Fully exempt — ₹0 taxable |

| Priya — 90 days, ₹1.2L basic, 10 years | Payout ₹3,60,000 | 10 months ₹12L | Eligible ₹3,60,000 | Cap ₹25L | Fully exempt — actual amount is lowest |

| Senior employee — 180 days, ₹2L basic, 15 years | Payout ₹12L | 10 months ₹20L | Eligible ₹9L (15×30 days ceiling) | Cap ₹25L | Exempt ₹9L — taxable ₹3L |

Comparison: Tax Treatment by Situation

| Situation | Employee Type | Tax Treatment |

|---|---|---|

| Retirement / superannuation | Central or state government | Fully Exempt — no cap |

| Retirement / superannuation | Private sector | Conditional Exemption — least of 4 amounts; ₹25L lifetime cap |

| Resignation | Private sector | Conditional Exemption — same four-condition test as retirement |

| During employment (annual encashment) | Private sector | Fully Taxable |

| During employment (earned leave) | Central govt employee | Partially Exempt — up to notified limit |

| Death of employee — paid to legal heir | Any | Fully Exempt |

How to Decide What’s Right for You

You are a central or state government employee retiring or reaching superannuation — your entire leave encashment is fully tax-free. No further tax calculation is required on this component when you file ITR.

You are a private sector employee who has resigned with a moderate earned leave balance (under 90 days) and a basic salary under ₹1.5 lakh per month — run the four-condition test. In most such cases, the full payout qualifies as exempt under Section 10(10AA).

You have changed jobs before and claimed Section 10(10AA) exemption at a previous employer — subtract that earlier claim from the ₹25 lakh lifetime cap before accepting your new settlement. Your remaining exemption may be significantly lower than the full cap.

Your employer is offering annual leave encashment during service and you are in the private sector — the full amount is taxable for that financial year. If your leave balance allows it, taking the leave instead preserves the balance for a potentially exempt payout at resignation or retirement.

Your leave encashment payout is large — ₹8 lakh or more — apply all four conditions manually before accepting the settlement to check whether a taxable portion remains, and ensure your employer deducts the correct TDS.

You have confirmed with HR whether your leave balance includes only earned leave — do not accept the settlement figure at face value. Casual leave and sick leave typically cannot be encashed. Ask for a written leave balance breakup before signing.

Common Mistakes to Avoid

Assuming the Entire Amount Is Tax-Free

Many private sector employees assume leave encashment works like a government retirement benefit — fully exempt with no ceiling.

If your basic salary is high or your leave balance is large, the four-condition test may produce a taxable balance. Filing ITR without accounting for this can trigger demand notices or scrutiny from the Income Tax Department. Understanding your salary TDS rules also helps you check whether your employer has deducted TDS correctly at source — or whether excess TDS was cut on an amount that was actually exempt.

Run the four-condition test before finalising your ITR. Do not assume; calculate.

Using CTC or Gross Salary as the Calculation Base

The Section 10(10AA) exemption formula uses basic salary plus DA, averaged over the last 10 months — not CTC, not gross salary, not in-hand pay.

Using the wrong base inflates condition (d) in the four-condition test, making a portion that is actually taxable appear exempt. For most private sector employees, basic salary is 40–50% of CTC. That difference can mean a significantly overstated exemption and under-reported taxable income in your ITR.

Use only the correct salary definition under Section 10(10AA) — not the figure on your offer letter or payslip gross total.

Not Tracking Previous Section 10(10AA) Claims

The ₹25 lakh cap is cumulative across all employers over your entire career. Claiming ₹6 lakh at your first company and ₹9 lakh at your second leaves only ₹10 lakh available — not the full ₹25 lakh.

Not accounting for this history leads to under-reporting taxable income, which can result in a demand notice. Maintain a record of every Section 10(10AA) exemption in your past ITR filings and prior Form 16 documents. Your new employer’s payroll team will typically ask for a declaration of prior exemptions before processing the settlement.

Not Verifying the Leave Balance Breakup

Employers sometimes include non-encashable leave types in the settlement figure, or apply an incorrect total leave balance.

If your settlement shows 75 days but 20 of those are casual leave that cannot be encashed per your HR policy, the correct base is only 55 days. An inflated leave balance overstates your payout and may misrepresent your exemption calculation in ITR.

Request a signed leave balance statement from HR, broken down by leave type, before accepting any settlement document.

Missing Leave Encashment in the ITR Schedule

Even if your leave encashment is fully exempt, it must be reported in the Schedule Salary section of your ITR — with both the exempt and taxable portions disclosed separately.

Omitting it entirely, even when the taxable amount is zero, creates a mismatch with Form 16 and Form 26AS data. The Income Tax Department can flag this discrepancy and issue a notice for the difference.

Match what appears in your Form 16 to what you declare in your ITR salary schedule before submission.

Not Checking Whether TDS Was Deducted Correctly

Some employer payroll systems deduct TDS on the entire leave encashment amount before paying you, without automatically applying the Section 10(10AA) exemption. This is more common at companies with older payroll software.

If excess TDS was cut on an exempt amount, you can reclaim it as a refund when filing ITR — but only if you correctly declare the exempt portion. Check your Form 16 to see whether the exemption was applied by the employer or needs to be claimed by you when you file.

When This May Not Be the Right Choice

If your employer offers annual leave encashment during service and you are a private sector employee, the payment is fully taxable for that financial year. If you are in the 30% slab, every ₹1 lakh encashed costs ₹30,000 in tax. Taking the leave instead costs nothing and preserves the balance for an exempt or lower-tax payout at resignation or retirement.

If your leave encashment is large and arrives in a year where you already have significant other income — a performance bonus, rental income, or capital gains — it can push up your total taxable income considerably and result in a much higher tax outgo than expected for that assessment year.

If your employer’s leave policy caps encashable days at fewer than your actual balance — say 45 days when you have accumulated 110 — the surplus balance will simply lapse. In that situation, using some of that leave before your last working day may preserve more value than leaving it to be capped and forfeited.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Leave encashment tax treatment is governed by Section 10(10AA) of the Income Tax Act, 1961. The Central Government notifies changes to exemption limits — including the aggregate cap applicable to private sector employees — through official notifications and Budget amendments. The Income Tax Department at incometax.gov.in is the authoritative source for current rules, applicable assessment years, and filing guidance.

Before filing your ITR, verify the exempt allowance figure in Part B of your Form 16. The exempt allowances section should reflect the Section 10(10AA) amount your employer applied at payroll. To understand exactly how these entries are structured and where to find them, Read Form 16 carefully before submitting your return.

Your employer’s HR leave policy document and your full-and-final settlement statement are also essential references for verifying the leave balance, the calculation method used, and the TDS treatment applied.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before signing any full-and-final settlement document, ask HR for a written leave balance statement broken down by leave type — earned, casual, and sick. Only earned leave is encashable in most policies, and one incorrect leave type in the tally changes both your payout and your tax position.

- Confirm whether your employer uses 30 calendar days or 26 working days as the divisor in the payout formula. A 26-day divisor gives a higher per-day rate. This is usually stated in your appointment letter or HR policy and makes a meaningful difference on larger leave balances.

- If your employer deducted TDS on the full encashment amount without applying the Section 10(10AA) exemption, do not simply accept the lower net payment. File your ITR with the correct exempt amount declared and claim the excess TDS as a refund through the income tax portal.

- Keep a running record of every leave encashment you receive and every Section 10(10AA) exemption you claim — across all employers, across all financial years. The ₹25 lakh lifetime cap makes this history financially significant every time you change jobs or receive a settlement.

- Match your full-and-final settlement sheet against your Form 16 and Form 26AS before filing ITR. If the leave encashment amount differs across these three documents, resolve the discrepancy with your employer’s payroll team before you submit. A mismatch triggers automated notices from the Income Tax Department.

- If your encashment is large enough to create a taxable portion, use an income tax calculator to estimate how the taxable balance interacts with your total income for the year — especially if you also received a bonus or other irregular income in the same financial year.

Frequently Asked Questions

Is leave encashment taxable in India?

It depends on your employee category and when the payment is made. Government employees receive full tax exemption on leave encashment at retirement under Section 10(10AA)(i) — no cap, no formula. For private sector employees, encashment received at retirement or resignation is partly or fully exempt under the four-condition test, subject to a ₹25 lakh lifetime aggregate cap. Leave encashment received during employment is fully taxable for private sector employees — no exemption applies.

Is leave encashment on resignation taxable for private employees?

Not necessarily. Private employees who resign are eligible for the Section 10(10AA)(ii) exemption — the same provision that applies at retirement. The exempt amount is the lowest of four conditions: actual amount received, ₹25 lakh lifetime cap, 10 months’ average salary, and eligible leave salary. If all four conditions exceed the actual payout — which happens frequently for moderate leave balances — the entire amount is exempt and the taxable portion is zero.

Is leave encashment for government employees fully tax-free?

Yes — for central and state government employees, leave encashment received at retirement or superannuation is fully exempt from income tax under Section 10(10AA)(i). No monetary cap applies, and no four-condition formula is used. The full payout is excluded from taxable income. This benefit applies at retirement — not during service, where different rules and limits apply.

What is the formula for earned leave encashment calculation?

The employer payout formula is: (Monthly Basic Salary ÷ 30) × Number of Encashable Earned Leave Days. Some employers use 26 as the divisor instead of 30 — check your HR policy. For income tax, private employees use a separate four-condition exemption test: the lowest of the actual amount received, the ₹25 lakh cap, 10 months’ average salary, and the eligible leave salary calculation. Only the amount above the lowest figure is taxable.

Is leave encashment based on basic salary or gross salary?

For income tax exemption purposes, eligible salary under Section 10(10AA) means basic salary plus Dearness Allowance only — averaged over the last 10 months before resignation or retirement. HRA, allowances, and performance bonuses are excluded. Most private sector employees receive no DA, so eligible salary equals average monthly basic pay for the last 10 months — significantly lower than gross salary or CTC. The employer may use a different base for the payout itself, so always verify the method used.

Where is leave encashment shown in Form 16?

If your employer applied the Section 10(10AA) exemption through payroll, the exempt amount appears in Part B of Form 16 under the exempt allowances section. The taxable portion, if any, is included in the gross salary figure. If the exemption was not applied through payroll — which happens at some companies — the full amount may appear as regular salary income, and you will need to declare and claim the exemption yourself when filing ITR.

Can I claim leave encashment exemption if I have changed jobs multiple times?

Yes, but the ₹25 lakh cap is a cumulative lifetime figure. Each time you claim Section 10(10AA) exemption at any employer, that amount reduces your remaining available cap. If you claimed ₹5 lakh at your first employer and ₹9 lakh at your second, your remaining cap is ₹11 lakh — not the full ₹25 lakh. Most employers ask for a self-declaration of prior exemptions claimed before processing the settlement. Track this history in your ITR records.

What happens if my employer deducts TDS on the full leave encashment amount?

Some employer payroll systems deduct TDS on the entire leave encashment without automatically applying the Section 10(10AA) exemption. You receive a smaller net payment, but the excess TDS can be reclaimed when you file your ITR — by correctly declaring the exempt amount in the salary schedule. The refund is processed through the Income Tax Department’s standard refund mechanism. Do not skip this step; on large encashment amounts, the refund can be significant.

Is leave encashment during employment taxable for private sector employees?

Yes — fully. Leave encashment received during active employment is taxable as salary income for private sector employees in the financial year it is paid. The Section 10(10AA) exemption is specifically designed for payments at the time of retirement, superannuation, or resignation. There is no partial exemption for during-service encashment in the private sector, unlike the limited concession available to central government employees.

Final Verdict

Leave encashment calculation becomes clear once you understand that the employer’s payout formula and the income tax exemption formula are entirely separate processes. Government employees at retirement need not worry — the exemption is full and unconditional. Private sector employees must apply the four-condition test, track their lifetime cap, and verify the salary components used.

For most salaried employees with moderate leave balances and standard basic salaries, the complete payout will be exempt at resignation or retirement. But the assumption is where people get into trouble. Run the numbers, cross-check your Form 16, verify your ITR salary schedule, and confirm the ₹25 lakh lifetime cap against any prior claims. For how this compares with the other key retirement-linked salary benefit, see the Gratuity tax comparison.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.