When your parents cross 60, one unplanned hospitalisation can wipe out years of their savings — and yours. Retired parents rarely have a steady income buffer, and medical costs in India have been rising at 12–14% per year. Buying health insurance for senior citizen parents is no longer optional; it is urgent.

The catch: senior citizen health insurance premiums are significantly higher than regular adult plans. That makes Section 80D of the Income Tax Act relevant — premiums paid for parents can qualify for a tax deduction. But too many families buy the cheapest available policy just to claim the deduction, and then discover at the time of a claim that the coverage is almost useless.

This article separates the tax benefit from the coverage question — and shows you exactly what to check before you buy.

Quick Answer: Health Insurance for Senior Citizen Parents

Health insurance for senior citizen parents can give a Section 80D deduction on premiums paid, subject to the senior citizen limit of ₹50,000. But the bigger decision is coverage quality: check waiting periods, co-pay, room rent limits, exclusions, cashless network and claim process before buying.

Key Takeaways

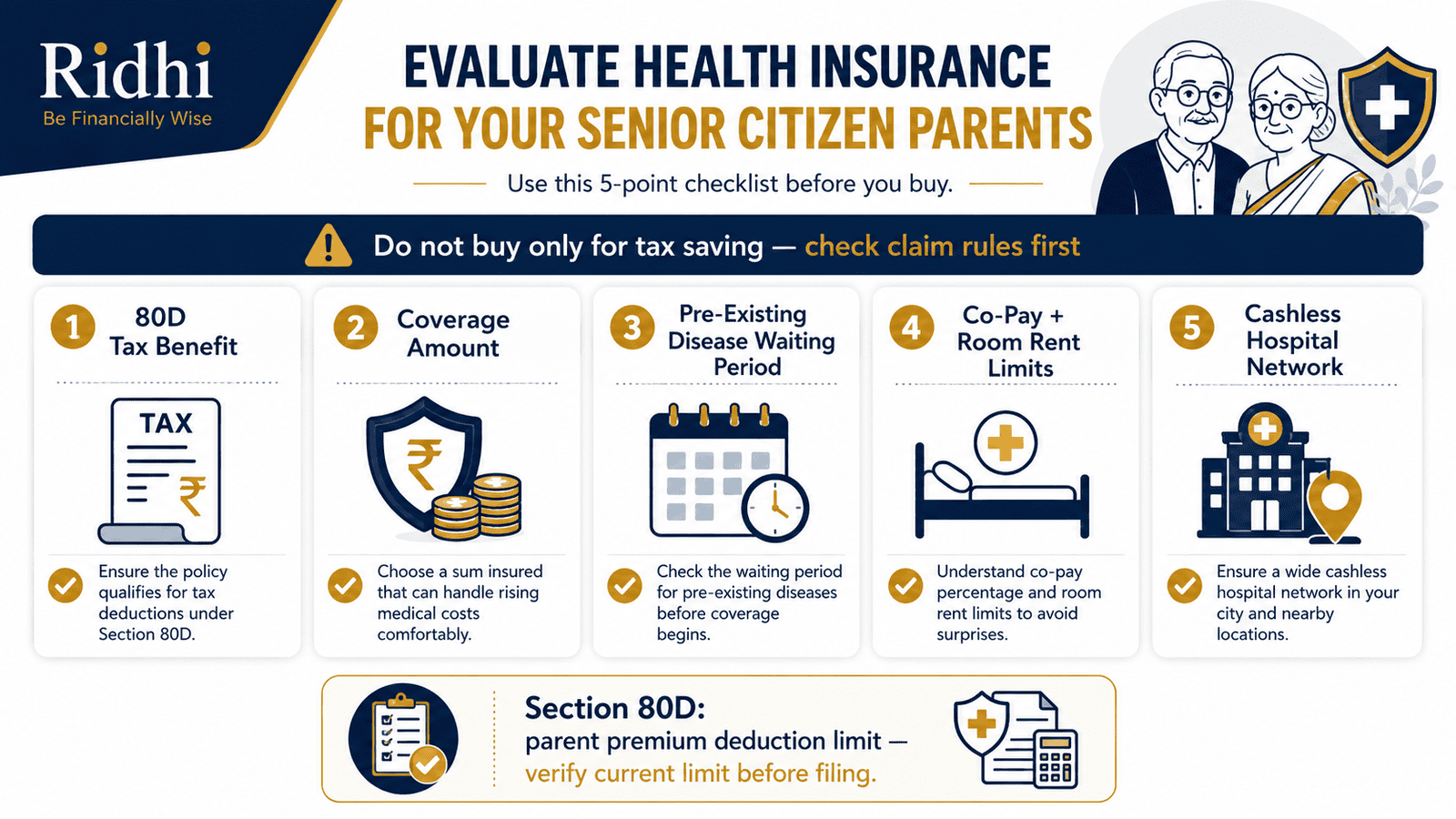

- Buy parent health insurance primarily for hospitalisation protection — not to save tax. A weak policy with a high co-pay or sub-limits can leave you paying most of the bill yourself.

- Section 80D allows a deduction of up to ₹50,000 on premiums paid for senior citizen parents — higher than the ₹25,000 limit that applies to non-senior parents.

- Pre-existing disease waiting periods for senior citizen policies are typically 2–4 years — meaning early claims for conditions like diabetes or hypertension may be rejected.

- A separate policy for elderly parents is usually better than adding them to a young family floater: premiums are cleaner, sums insured are dedicated, and renewals are simpler.

- Employer group health cover almost never extends to parents — and even when it does, it ends when you leave the job. Do not rely on it as the primary cover for your parents.

- Section 80D deduction is available under the old tax regime only. If you have opted for the new regime, you cannot claim this deduction.

- Premium payment must be made by any mode other than cash to be eligible for the Section 80D deduction — keep digital payment receipts.

Key Facts at a Glance

| Parameter | Detail | Notes |

|---|---|---|

| Who can claim 80D for parents | Individual taxpayer who pays the premium | Parent need not be financially dependent |

| Senior citizen age threshold | 60 years and above | As defined under Section 80D of the IT Act |

| 80D deduction limit — senior citizen parents | ₹50,000 per year | Higher limit applies if either parent is 60+ |

| 80D deduction limit — non-senior parents | ₹25,000 per year | Applies if both parents are below 60 |

| Tax regime eligibility | Old regime only | Not available under the new tax regime |

| Payment mode for 80D eligibility | Any mode except cash | UPI, net banking, cheque — all valid |

| Key policy checks before buying | PED waiting period, co-pay %, room rent limit, cashless hospitals, sub-limits | Affects real claim payout heavily |

How Health Insurance for Senior Citizen Parents Actually Works

Health insurance for senior citizen parents is a policy that covers hospitalisation costs — room charges, surgery, ICU, doctor fees, medicines — for one or both of your parents. You pay the premium; the insurer pays (or reimburses) the hospital bills up to the sum insured.

For a broader understanding of what health insurance normally covers and excludes, read our health cover basics guide first.

Three Coverage Options — and What Each Means

Senior citizen separate policy: A standalone policy bought exclusively for one or both parents. It has a dedicated sum insured — say ₹10 lakh for each parent — that does not get depleted by claims from other family members. Most insurers offer this between ages 60 and 80 at entry; some up to 65. Premiums are higher than a regular adult plan.

Family floater including parents: Parents are added to the same floater that covers you, your spouse, and your children. One shared sum insured. If your child gets hospitalised and exhausts a portion of the sum insured, that same pool is reduced for your parents. Insurer pricing usually gets more expensive when elderly parents are added, and renewal can be complicated if parents develop serious conditions.

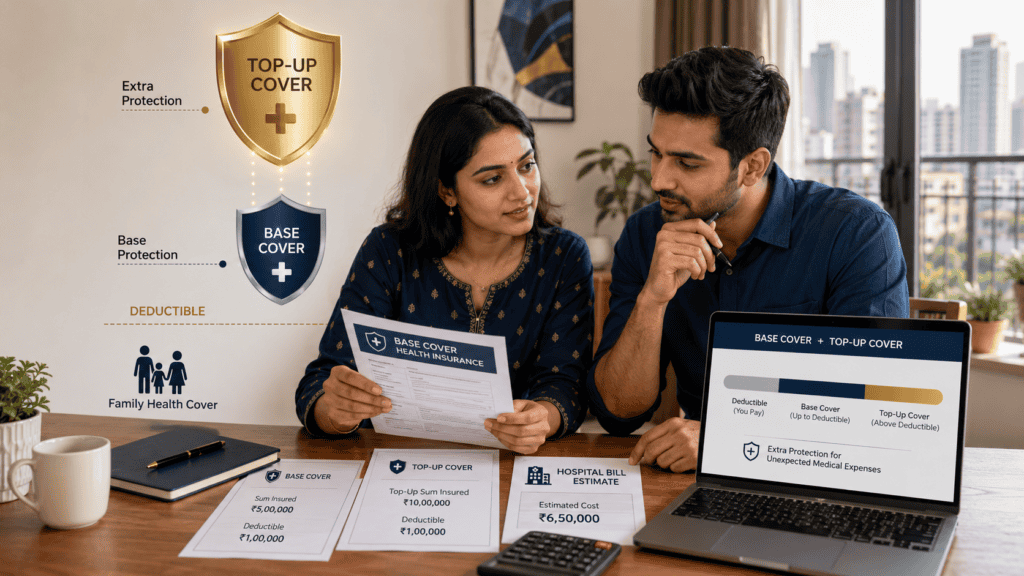

Top-up or super top-up: A top-up policy activates only after a deductible (say ₹5 lakh) is crossed in a policy year. It is cheaper but requires the family to absorb the deductible amount first. A super top-up counts the aggregate hospitalisation spend across the year before triggering. For parents with multiple small hospitalisations, a super top-up may help more than a basic top-up.

How Section 80D Fits into This Decision

According to the Income Tax Department at incometax.gov.in, Section 80D of the Income Tax Act allows a deduction for premiums paid towards health insurance. For premiums paid for senior citizen parents (aged 60 and above), the deduction limit is ₹50,000 per year. For non-senior parents (below 60), the limit is ₹25,000. These deductions are available only under the old tax regime. If you have chosen the new regime, no 80D deduction applies.

For a detailed breakdown of how Section 80D works, including preventive health check-up deductions and exact filing rules, see our 80D deduction rules guide.

The key practical point: the deduction reduces your taxable income, not your premium. If your premium is ₹55,000 and the deduction limit is ₹50,000, you get a deduction of ₹50,000 — not a refund of ₹50,000. The actual tax saving depends on your applicable slab rate and which regime you are in.

Why Coverage Quality Must Come First

A policy with a 20% co-payment clause means that for every ₹1 lakh claim, you pay ₹20,000 yourself. A policy with a room rent cap of ₹3,000/day — when your city’s private hospital rooms start at ₹6,000/day — will pro-rate most of the associated charges as well, leaving a much larger out-of-pocket bill. These restrictions are legal and disclosed in the policy wording. They will not show up in the premium comparison headline.

Premiums vary significantly by age, health status, city, insurer, and chosen sum insured. A premium that looks affordable may carry restrictions that reduce the actual claim payout to a fraction of the sum insured.

IRDAI at irdai.gov.in regulates health insurance products and mandates insurers to disclose exclusions and waiting periods in the policy document. Always read the policy wording — not just the brochure — before buying.

Real Example: Rohit Buys a Policy for His Parents in Pune

Rohit, 38, is an IT manager in Pune earning ₹24 lakh per year. His parents — father aged 64, mother aged 61 — are both retired. His father has type-2 diabetes diagnosed three years ago.

Rohit buys a separate senior citizen policy for both parents at a combined annual premium of ₹55,000. Under Section 80D of the Income Tax Act, he can claim a deduction of ₹50,000 (the senior citizen parent limit). The remaining ₹5,000 is not deductible — it simply exceeds the cap.

In the 30% tax slab under the old regime, this ₹50,000 deduction saves Rohit approximately ₹15,600 in tax (₹50,000 × 31.2%, including 4% cess). That is useful — but it is not the main reason to buy the policy.

More important: Rohit checks the policy wording carefully. He notes a 3-year pre-existing disease waiting period for his father’s diabetes. This means any hospitalisation directly related to diabetes in the first three years will not be covered. He decides to buy the policy now so the waiting period starts ticking — and keeps a separate emergency fund as a buffer for any early diabetes-related hospitalisation.

He also checks that two hospitals near his parents’ home in Pune are on the insurer’s cashless network. That single check could save his parents significant paperwork and advance payment stress at the time of a real emergency.

How to Calculate Your 80D Tax Saving

Tax Saving = Eligible Deduction × Applicable Tax Rate (including surcharge and cess)

Eligible deduction = the lower of: (a) actual premium paid for senior citizen parents, or (b) ₹50,000. If premium paid is ₹55,000, eligible deduction is ₹50,000.

Using Rohit’s numbers as an illustrative example:

| Scenario | Annual Premium Paid | Eligible 80D Deduction |

|---|---|---|

| Premium below limit | ₹40,000 | ₹40,000 (full amount) |

| Premium at limit | ₹50,000 | ₹50,000 (full amount) |

| Premium above limit | ₹55,000 | ₹50,000 (capped at limit) |

The resulting tax saving in the 30% slab (old regime, with 4% cess) would be approximately ₹12,480 on a ₹40,000 deduction, ₹15,600 on a ₹50,000 deduction, and still ₹15,600 on a ₹55,000 premium (since only ₹50,000 is deductible). These figures are illustrative only. Your actual saving depends on your taxable income, slab, and regime. Use our income tax calculator to check your specific situation.

Comparison: Separate Policy vs Family Floater vs Top-Up for Parents

| Option | Key Advantage | Key Risk |

|---|---|---|

| Separate senior citizen policy for parents | Dedicated sum insured; parents’ claims don’t affect rest of family | Higher premium; some insurers have entry age limits and loading |

| Adding parents to family floater | Single policy; one renewal | Shared sum insured depleted by any family member; premium rises sharply; harder to renew if parents develop serious illness |

| Senior citizen super top-up | Lower premium for large sum insured; good for multiple hospitalisations | Deductible must be paid first each year; not ideal as standalone coverage |

| Employer group insurance for parents | May be available for dependent parents at lower cost | High Risk Ends when you change jobs; coverage terms set by employer, not by you |

For a deeper comparison of floater vs individual plans, see our guide on floater or separate plan.

How to Decide What’s Right for You

Both parents are 60 or above and you file under the old tax regime — THEN the ₹50,000 senior citizen parent limit under Section 80D applies; a separate policy is likely the cleanest structure.

Your parents have pre-existing conditions like diabetes, hypertension, or a cardiac history — THEN buy the policy immediately so the waiting period clock starts now; do not wait for a health event.

Your parents live in a smaller city with limited private hospital options — THEN check that the insurer’s cashless hospital network includes hospitals in that specific city before buying. Read our cashless claim process guide to understand what cashless hospitalisation actually means for a patient.

You have opted for the new tax regime — THEN the 80D deduction does not apply; buy the policy for coverage protection, not tax benefit.

Your employer provides a group policy that includes dependent parents — THEN use it as a supplement, not a primary cover; never let it be your only safety net for parents.

If your parents already have a strong, long-running policy with a good insurer at a reasonable premium — THEN do not switch to a new policy only for a slightly lower premium; continuity benefits and completed waiting periods have real value.

Common Mistakes to Avoid

Buying Only for the 80D Tax Deduction

The most common mistake: choosing the cheapest policy that qualifies for 80D, without checking what it actually covers.

A policy with heavy co-pay, sub-limits, and exclusions can pay out as little as 30–40% of a real hospital bill — leaving you to fund the rest from savings. The tax saving of ₹15,600 in the 30% slab is real but modest compared to a hospitalisation bill of ₹3–5 lakh.

Evaluate policies by coverage quality first. Use the tax benefit as a bonus, not a reason to buy.

Ignoring the Pre-Existing Disease Waiting Period

Senior citizen health policies almost always impose a waiting period of 2–4 years for pre-existing diseases like diabetes, hypertension, asthma, or arthritis.

If your father is hospitalised for a diabetes-related complication in Year 1, the insurer can legitimately reject that claim. Many families discover this only after the event — when they needed the money most.

Check the PED waiting period clause in the policy document. Buy earlier rather than later so the waiting period finishes sooner. For a detailed explanation, see our guide on waiting period rules.

Choosing Low Premium With High Co-Payment

Some senior citizen plans reduce their premium by including a 10–30% co-payment clause — meaning you share every claim with the insurer.

A 20% co-pay on a ₹4 lakh hospitalisation means you pay ₹80,000 out of pocket, regardless of the sum insured. Over multiple hospitalisations, this adds up dramatically.

If the policy has a co-pay clause, factor that into the real cost of the policy before comparing premiums.

Missing Room Rent Limits and Disease-Wise Sub-Limits

Many policies cap room rent at ₹3,000–₹5,000 per day. If the actual room costs more, the insurer pro-rates all associated charges proportionally — so doctor fees, surgery charges, and ICU costs all get reduced.

Disease-wise sub-limits cap the payout for specific procedures: ₹30,000 for cataract, ₹50,000 for knee replacement. These are disclosed in the policy schedule but rarely highlighted in comparisons.

Ask specifically for a policy with no room rent sub-limits, or understand the cap before buying.

Not Checking Nearby Cashless Hospitals

A 10,000-hospital cashless network looks impressive until you check whether the three hospitals closest to your parents’ home are on it.

A cashless hospitalisation means no advance payment required at admission — critical for senior citizens who may not have liquid funds ready. If the nearest hospital is not on the list, your parents must pay upfront and then file for reimbursement — adding stress to an already difficult situation.

Always verify the insurer’s hospital network in your parents’ specific city before buying.

Concealing Medical History at the Time of Buying

Some families under-declare medical conditions to secure a lower premium or avoid policy loading.

IRDAI regulations allow insurers to repudiate claims if material information was withheld at the time of application. If a claim is rejected for non-disclosure, you lose both the claim payout and potentially the policy — with no recourse.

Disclose all conditions accurately. Buy from an insurer who will accept the risk with loading rather than one who offers clean acceptance and then rejects the claim later.

When This May Not Be the Right Choice

A standard senior citizen health insurance policy may not be the best solution in every situation:

Very severe pre-existing conditions: If a parent has an advanced chronic illness, some insurers may not offer a policy or may quote a premium so high it exceeds expected benefit. In such cases, a critical illness plan or a disease-specific plan may be worth evaluating separately.

Existing policy with strong continuity: If your parents already have a running policy with completed waiting periods and a good claim history, switching to a new policy restarts the waiting period clock. Continuity is valuable — do not discard it lightly.

Covered under a retiree group policy: If one or both parents receive a strong group health policy as part of a retirement benefit from a former employer or government service, a new standalone policy may be redundant or create duplicate premium spend without proportional benefit.

Budget significantly strained by premium: If the annual premium for senior citizen coverage would meaningfully strain the household budget, a super top-up with a reasonable deductible may be a more sustainable structure than a comprehensive standalone policy.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Health insurance for senior citizen parents involves two regulatory domains: tax deduction rules and insurance product rules. Verify figures from both before making a decision.

- Income Tax Department — incometax.gov.in: The authoritative source for Section 80D deduction limits, tax regime eligibility, and ITR filing rules. Check here for current deduction limits before filing.

- IRDAI — irdai.gov.in: Regulates all health insurance products sold in India. Mandates standardised definitions, waiting period disclosures, and policyholder protection norms. Check here if you face a claim dispute or want to verify an insurer’s standing.

- Your insurer’s policy document: The only source of truth for what is covered, what is excluded, what the waiting periods are, and what the sub-limits and co-pay terms are. Brochures are not binding — the policy schedule and wordings document is.

- Insurer’s cashless hospital network list: Check the insurer’s website or call their helpline to verify which hospitals in your parents’ city support cashless treatment.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Compare policy wording, not just premium. Download the sample policy document from two or three insurers and compare the actual co-pay clause, room rent limit, and PED waiting period side by side — not just the premium brochure.

- Buy the policy before a health event, not after. Senior citizen premiums increase with age and health conditions. A policy bought at 61 for your parent will almost always have better terms and a lower premium than one bought at 67 after a cardiac event.

- Check insurer reliability using the claims settlement ratio. IRDAI publishes insurer-wise claim settlement data. An insurer settling 95%+ of claims consistently is a better choice than one offering a marginally lower premium. See how to use this data in our claim ratio meaning guide.

- Verify lifetime renewability explicitly. IRDAI mandates lifetime renewability for most health insurance products, but verify the specific policy’s renewability terms before buying, especially for senior citizen products.

- Keep 80D payment receipts and policy documents organised before March 31. Premium receipts paid via net banking or UPI must be retained for ITR filing under the old regime. Losing receipts means losing the deduction.

- If both parents are alive, buy separate policies rather than a joint plan. Separate policies mean separate sum insureds — so a major hospitalisation for one parent does not deplete the coverage for the other.

- Do not let the no-claim bonus mislead you. Some policies build up a no-claim bonus that increases sum insured over years without claims — useful, but it does not help in Year 1. Evaluate base coverage, not projected future bonuses.

Frequently Asked Questions

Can I claim Section 80D deduction for my parents’ health insurance premium?

Yes. If you pay the health insurance premium for your parents — whether or not they are financially dependent on you — you can claim a deduction under Section 80D of the Income Tax Act, provided you are in the old tax regime. The deduction applies to the actual premium paid, up to the applicable limit.

What is the 80D deduction limit for senior citizen parents?

The Section 80D deduction limit for premiums paid for senior citizen parents (aged 60 years and above) is ₹50,000 per year. For non-senior parents (below 60), the limit is ₹25,000. If even one parent qualifies as a senior citizen, the higher ₹50,000 limit applies for the parent portion of the deduction.

Can I claim 80D if my parents are not financially dependent on me?

Yes. The Income Tax Act does not require financial dependency as a condition for the Section 80D deduction for parents. As long as you have paid the premium, you are eligible to claim the deduction — subject to the applicable limit and tax regime.

Is cash payment allowed for the 80D deduction on parent health insurance?

No. Premium paid in cash does not qualify for the Section 80D deduction. The premium must be paid by any mode other than cash — such as net banking, UPI, cheque, or debit/credit card. Always pay digitally and retain the transaction receipt for filing purposes.

Should I add my parents to a family floater or buy a separate policy?

For most families, a separate policy for elderly parents is cleaner. When parents are added to a family floater, the shared sum insured can be depleted by any family member’s claim, premiums increase significantly, and renewals can be harder if parents develop chronic conditions. A dedicated policy means a dedicated sum insured that is always available for your parents’ use.

Does health insurance cover pre-existing diseases for senior citizens?

Yes — but typically only after a waiting period of 2–4 years (the exact period is stated in the policy document). Hospitalisations directly related to pre-existing conditions like diabetes, hypertension, or cardiac issues may be rejected during this waiting period. This is why buying the policy early — before a health event — is critical for senior citizens.

Is employer group health insurance enough as the only cover for my parents?

Usually not. Employer group policies may not extend to parents at all; when they do, coverage ends when you change or lose the job, and the terms are set by your employer’s group contract — not by your parents’ needs. Treat any employer group cover as a supplement, not a substitute for a standalone policy.

What is a co-payment clause and how does it affect senior citizen health insurance?

A co-payment clause requires you to pay a fixed percentage of every claim yourself — typically 10–30% in senior citizen plans. For a ₹5 lakh hospitalisation with a 20% co-pay, you would pay ₹1 lakh out of pocket regardless of the sum insured. Check the co-pay percentage before buying — it significantly affects the real value of the policy.

What happens if my parents’ insurer rejects a claim?

If a claim is rejected, you have the right to approach the insurer’s grievance redressal mechanism first. If that fails, you can escalate to the Insurance Ombudsman or IRDAI’s Bima Bharosa portal. Keep all hospitalisation records, bills, and discharge summaries — these are critical for any dispute. Rejection risk is highest when pre-existing conditions are undisclosed or when claims fall within the waiting period.

Does the 80D deduction apply if I have chosen the new tax regime?

No. Section 80D deductions — including the ₹50,000 limit for senior citizen parent premiums — are available only under the old tax regime. If you have opted for the new regime for a financial year, you cannot claim this deduction for that year, regardless of how much premium you paid.

Final Verdict

Health insurance for senior citizen parents is one of the most practical financial steps a salaried family can take — but only if the policy is bought for the right reason. The ₹50,000 Section 80D deduction is a genuine tax benefit under the old regime, and it can save ₹10,000–₹15,600 per year depending on your slab. But that saving is meaningless if the policy has a heavy co-pay clause, a room rent cap that pro-rates every claim, or a cashless network that doesn’t cover the hospitals near your parents’ home.

Buy for claim-ready medical protection first. Verify the pre-existing disease waiting period, co-payment terms, room rent limits, and cashless hospital network before you pay a single rupee in premium. Compare at least two to three policies side by side — using the actual policy wording, not just the premium comparison sheet. The 80D deduction then becomes a welcome bonus on top of genuine coverage.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.