Your salary is three days late. Rent is due tonight. Your debit card balance will not cover it — but your credit card has a decent unused limit sitting right there. You head to the ATM, insert your credit card, and withdraw ₹10,000.

What you may not realise until your next statement arrives: a credit card cash advance is not the same as a debit card ATM withdrawal. Interest may start the moment the cash leaves the machine. A cash advance fee applies on top. There is no interest-free grace period — unlike every regular purchase you make on the same card. This article explains how credit card cash advance charges work in India, shows you the real cost using a ₹10,000 example, compares it against safer alternatives, and gives you a clear decision framework before you ever hit that ATM button again.

Quick Answer: Credit Card Cash Advance

A credit card cash advance means withdrawing cash from your credit card at an ATM. It is costly because banks usually charge a cash advance fee, GST, and interest from the withdrawal date, with no interest-free grace period. For example, a ₹10,000 withdrawal can start costing extra from day one.

Key Takeaways

- A credit card cash advance is treated differently from regular purchases — interest starts from the date of withdrawal, not from your payment due date, because no grace period applies.

- A cash advance fee and GST are charged upfront on every withdrawal, even if you repay the full amount within two or three days.

- Your cash withdrawal limit is a sub-limit within your total credit limit — typically 20–40% of the total, depending on your issuer and card variant.

- Paying only the minimum amount due after a cash withdrawal allows finance charges to compound daily, turning a ₹10,000 emergency into a much larger liability over a few months.

- Safer and often cheaper alternatives — debit card ATM cash, emergency fund, personal loan, or credit card EMI — are worth checking before you make any ATM withdrawal using a credit card.

- Repeated cash advances every month are a warning sign of a cash-flow problem — and each one makes the underlying problem more expensive to resolve.

Key Facts at a Glance

| Aspect | What It Means | Key Rule / Warning |

|---|---|---|

| Credit Card Cash Advance | Withdrawing cash at an ATM using your credit card | Treated as a loan by the issuer — different billing rules from purchases |

| Grace Period | Interest-free window that applies to regular purchases | Does not apply to cash advances — interest starts on withdrawal date |

| Cash Advance Fee | A flat or percentage-based fee charged on the amount withdrawn | Varies by issuer and card type — check your card’s MITC before withdrawing |

| Finance Charges | Monthly interest on the outstanding cash advance balance | Rate varies by issuer — typically higher than personal loan rates |

| GST on Card Charges | 18% GST applied on cash advance fee and finance charges | Increases actual cost beyond the headline fee — appears as a separate line on your statement |

| Cash Withdrawal Limit | The portion of your credit limit available as ATM cash | Usually lower than your total credit limit — often 20–40% for many card types |

| Best-Use Guideline | Genuine short-term cash emergency only | Repay the full amount as quickly as possible to limit finance charge accumulation |

How Credit Card Cash Advance Works in India

When you insert your credit card at an ATM and select “Cash Withdrawal,” you are not spending your own money — you are borrowing against your credit limit. Your bank treats this as a cash advance transaction, and the billing rules that apply are significantly different from the ones that apply when you swipe the same card at a shop or make an online purchase.

What happens at the ATM

The withdrawal is processed against your card’s cash advance limit — a sub-limit that sits within your overall credit limit. If your total credit limit is ₹1,00,000, your actual cash withdrawal limit may be anywhere from ₹20,000 to ₹40,000, depending on your card type and issuer’s policy. Some premium cards allow a higher cash limit; entry-level cards may offer a lower percentage or even restrict ATM withdrawals entirely. The only reliable way to know your exact limit is to check your card’s Most Important Terms and Conditions document — commonly called the MITC — or log in to your card account online or in the app.

If you are new to credit cards and still building familiarity with how limits, billing cycles, and card features work, reading up on first card basics before using any advanced feature like ATM cash withdrawal is a good starting point.

Why the no interest-free period rule is the real danger

This is the detail that catches most first-time users off guard. When you make a regular purchase on your credit card — groceries, fuel, an online order — you benefit from an interest-free grace period. Depending on where in your billing cycle the purchase falls, that window can be anywhere from 20 to 50 days. Pay the full outstanding balance by your payment due date, and you pay zero interest.

Cash advances do not have this protection. Interest on a credit card cash advance begins from the date of withdrawal — not from the statement date, not from the due date. If you withdraw ₹10,000 on a Tuesday and repay it on Thursday, you will still owe interest for those two days, plus the cash advance fee and GST on top. The billing cycle determines when these charges appear on your statement, but it does not create any interest-free window for the cash portion of your balance.

This distinction is the single most important difference between a purchase transaction and a cash advance. Missing it can make what feels like a minor emergency withdrawal much more expensive than anticipated.

How a cash advance appears on your credit card statement

Your monthly credit card statement will show the cash advance as a separate transaction line — typically labelled “ATM Cash Withdrawal” or “Cash Advance” with the date and amount. The cash advance fee appears as a separate fee entry. Finance charges — the accumulated interest — appear either as a consolidated line or broken down per transaction, depending on how your issuer formats statements. GST on card charges applies to both the fee and the finance charges and may appear as a combined line or itemised separately.

A common confusion arises from the minimum amount due figure. On paper, it looks manageable. But the minimum amount due is structured to keep the account current and avoid a late payment penalty — it is not designed to eliminate interest. If you pay only the minimum after a cash advance, finance charges continue accruing on the full unpaid balance at the cash advance rate. That is how a ₹10,000 ATM withdrawal can become a ₹12,000 or ₹13,000 liability over two or three months if it is not actively repaid in full.

Cash advance limit vs total credit limit

Your total credit limit and your cash advance sub-limit are separate numbers. Banks set a lower ceiling for cash withdrawals as a standard risk management practice. If your card has a ₹2,00,000 credit limit, you may only be permitted to withdraw ₹40,000 to ₹60,000 in cash. Attempting to withdraw beyond your cash advance limit will result in an ATM decline — which is an inconvenient discovery in a genuine emergency. Always check your current cash withdrawal limit in advance rather than assuming the full credit limit is available at any ATM.

Why unused credit limit is not free liquidity

Some cardholders mentally treat an unused credit limit as available cash. It is not — it is a borrowing facility with conditions attached. When you use it for regular purchases, the grace period lets you borrow at zero interest if you repay on time. When you use it for a cash advance, the cost begins immediately. Treating ATM cash withdrawal as routine short-term liquidity — rather than a genuine last resort — is one of the most common ways salaried professionals accumulate revolving credit card debt that becomes difficult to exit.

According to the RBI’s guidelines on credit cards, issuers are required to disclose all applicable charges — including cash advance fees and interest rates — clearly in the cardholder MITC. This document is available on your issuer’s website or can be requested from your bank. Reviewing the cash advance section specifically before you need emergency cash is a practical step that takes less than five minutes.

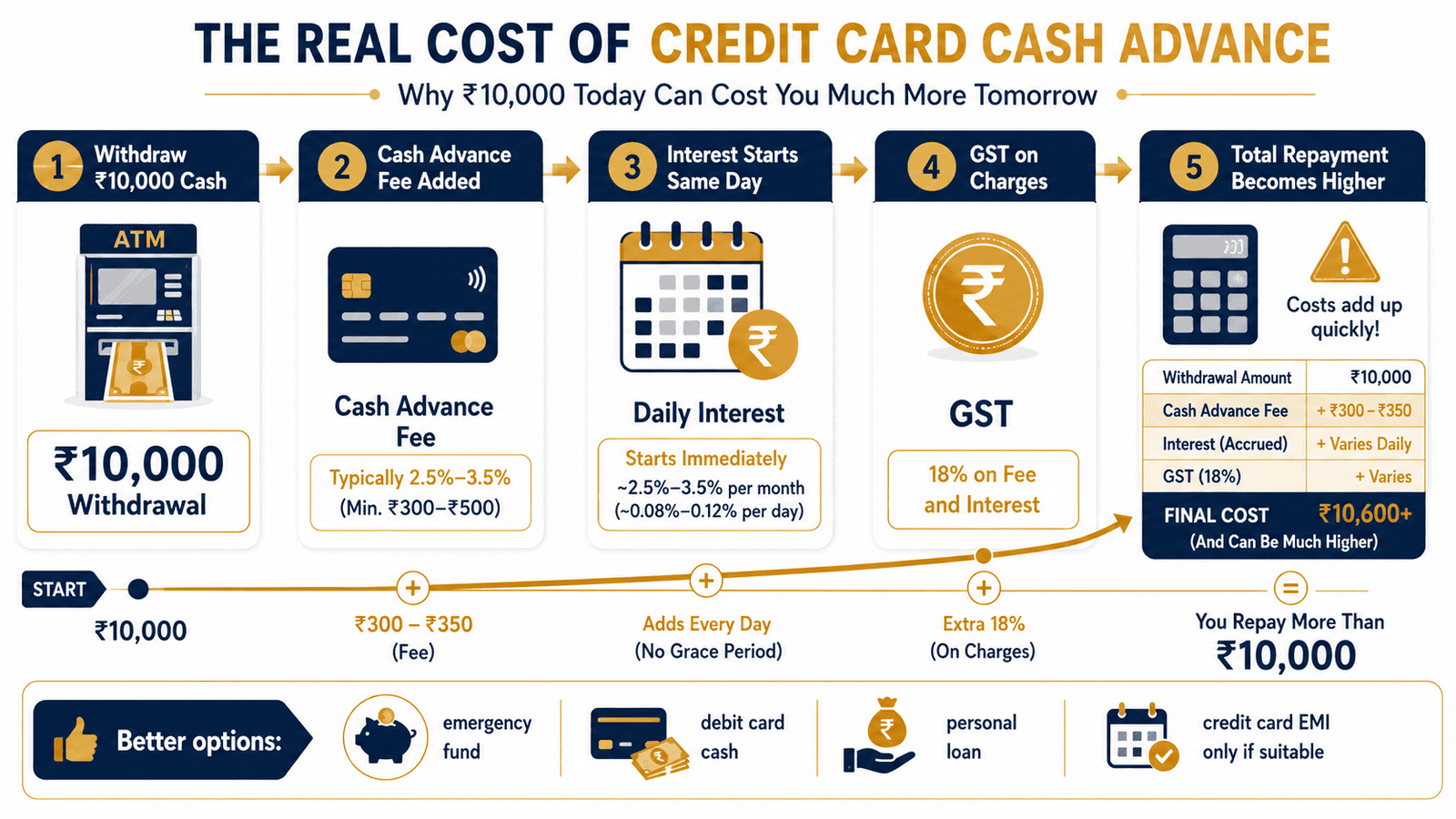

Real Example: Rahul’s ₹10,000 ATM Withdrawal

Rahul is 29 years old, works as an IT analyst in Pune, and earns ₹75,000 per month. His credit card has a ₹1,00,000 total credit limit with a cash advance sub-limit of ₹25,000. On a Tuesday evening, his salary is delayed by two days and his rent of ₹10,000 is due that night. He uses his credit card at an ATM and withdraws ₹10,000.

The table below shows an illustrative breakdown of what appears on Rahul’s next statement. All figures are sample calculations only — actual charges depend on your issuer, card type, and repayment date:

| Charge | Illustrative Amount | Note |

|---|---|---|

| Cash Withdrawn | ₹10,000 | Principal amount to be repaid |

| Cash Advance Fee | ₹250 (2.5% of ₹10,000 — illustrative) | Verify exact rate in your card’s MITC |

| GST on Cash Advance Fee | ₹45 (18% of ₹250) | Applied at current GST rate on applicable charges |

| Finance Charges (30 days) | ₹350 (3.5%/month — illustrative) | Accrues from withdrawal date — verify issuer’s rate |

| Total Repayment (30 days) | ₹10,645 | Illustration only — actual total will vary by issuer and repayment date |

Rahul’s salary arrived two days after the withdrawal and he repaid the full outstanding amount immediately. His actual interest accrued for only two days — a small amount. But the cash advance fee of ₹250 and GST of ₹45 were charged regardless of how quickly he repaid. Those ₹295 were the unavoidable cost of a two-day emergency. Had he delayed repayment to the next payment due date — three weeks away — the total would have been considerably higher.

To understand exactly where these charges appear in your monthly bill and how to read each line item, see our guide on statement line items — it shows you how to identify cash advance fees, finance charges, and GST components on your statement.

How to Calculate Your Credit Card Cash Advance Cost

Total Cost = Cash Withdrawn + Cash Advance Fee + GST on Fee + Finance Charges (Daily Rate × Days Held)

Step-by-step using Rahul’s ₹10,000 withdrawal

Step 1 — Cash withdrawn: ₹10,000. This is the principal you must repay regardless of when or how charges are added.

Step 2 — Cash advance fee: Using an illustrative rate of 2.5%, the fee = ₹250. Some issuers charge a flat fee (for example, ₹500 irrespective of the amount withdrawn, with a different percentage for larger withdrawals). The exact structure is in your MITC under “Schedule of Charges.”

Step 3 — GST on the fee: 18% GST applied to ₹250 = ₹45. GST may also be levied on finance charges depending on how your issuer bills — check your statement for the exact GST line.

Step 4 — Finance charges: Using an illustrative monthly rate of 3.5%, the daily rate is approximately 0.117%. For 30 days: ₹10,000 × 3.5% = ₹350. For just 5 days: ₹10,000 × 0.117% × 5 = approximately ₹58. Repaying quickly significantly reduces this portion — but cannot eliminate the fee and GST already charged.

Step 5 — Total repayment: ₹10,000 + ₹250 + ₹45 + ₹350 = ₹10,645 for a full 30-day hold (illustrative).

| Scenario | Days Held | Illustrative Total Cost |

|---|---|---|

| Repaid in 2 days | 2 days | ≈ ₹10,318 (fee + GST + 2-day interest) |

| Repaid in 15 days | 15 days | ≈ ₹10,470 (fee + GST + 15-day interest) |

| Repaid in 30 days | 30 days | ≈ ₹10,645 (fee + GST + full month interest) |

These figures are illustrative only. Your actual cost depends entirely on your issuer’s cash advance fee structure, current monthly finance charge rate, and whether GST is separately levied on the interest component. For a full explanation of how credit card interest accumulates and how daily compounding works, see our guide on the interest calculation method.

Comparison: Credit Card Cash Advance vs Alternatives

Before withdrawing cash from your credit card, it is worth understanding how it compares to options available to most Indian salaried employees:

| Option | Cost Profile | Best For / Key Risk |

|---|---|---|

| Credit Card Cash Advance | Cash advance fee + GST + immediate interest — may be among the more expensive short-term options | Instant cash when no other option is available; risky if repayment is delayed |

| Debit Card ATM Withdrawal | Small ATM operator fee only (typically ₹20–21 per transaction beyond free monthly limit) — no interest | Always preferable if your savings account has sufficient balance |

| Personal Loan | Processing fee + monthly interest — generally lower than credit card cash advance finance charges | Larger amounts, can wait 1–3 business days for disbursal, structured EMI repayment |

| Credit Card EMI | Conversion fee + EMI interest — may be lower than cash advance rate for purchase transactions | Works for purchases that can be converted to EMI — cannot provide physical cash |

| Emergency Fund | No cost — your own savings | Ideal for genuine short-term emergencies; building even a ₹15,000 buffer eliminates most cash advance scenarios |

For a side-by-side breakdown of when a personal loan is more cost-effective than using your credit card for large expenses, see our guide on the loan comparison option.

How to Decide What’s Right for You

Run through these if/then statements before making any credit card ATM withdrawal:

you have sufficient bank balance, a UPI transfer option, or a family member who can send the amount immediately — use that first. A credit card cash advance should never be the first option when cheaper or free alternatives are available.

the need is a genuine cash emergency — medical bill, rent, utility payment — and no bank balance or faster option is available — a cash advance may be acceptable, provided you can repay the full amount within a few days of the withdrawal.

you need a larger amount and can wait one to three business days — a personal loan or a pre-approved salary advance from your employer will almost always cost you less in total interest than a cash advance held for the same period.

you already carry an outstanding balance from last month’s credit card statement — adding a cash advance means interest may accrue on the combined outstanding amount from day one, making the total cost higher than a simple standalone withdrawal calculation would suggest.

you can repay the full withdrawn amount before or shortly after your next payment due date — the fee and a small interest charge may be a reasonable one-time cost for a genuine short-term emergency. But always verify the exact fee and rate in your MITC first.

you cannot realistically repay the full amount within the current billing cycle — do not use a cash advance. Finance charges on revolving credit card debt compound daily and are among the most expensive short-term borrowing costs available in India.

the cash need is for discretionary or lifestyle expenses such as shopping, dining, or travel — do not use a cash advance. Regular card purchases give you a grace period to pay at zero interest; ATM cash withdrawals do not.

Before any withdrawal, check your card’s MITC for the current cash advance fee, monthly finance charge rate, and your cash withdrawal sub-limit. This takes five minutes and tells you exactly what the transaction will cost.

Common Mistakes to Avoid

Assuming cash withdrawal gets the same grace period as purchases

This is the most common and costly misconception about credit card cash advances in India.

A cardholder who makes a ₹10,000 purchase at a store pays zero interest if they clear the balance by the due date. The same cardholder who withdraws ₹10,000 from an ATM using the same card owes interest from the day of withdrawal — even if they repay it two days later. The billing cycle does not create any protection for cash advance transactions.

Check the “Cash Advance” section of your card’s MITC to confirm the exact terms before assuming a grace period applies.

Paying only the minimum amount due after a cash withdrawal

Your statement’s minimum amount due is typically calculated at around 5% of the outstanding balance or a small flat amount. Paying only this after a cash advance does not stop interest from compounding on the remaining balance.

On a ₹10,000 cash advance at an illustrative 3.5% monthly rate, paying only the minimum leaves approximately ₹9,500 attracting full-rate finance charges in the next cycle. Over two or three months, the cumulative interest can be significant. Our detailed breakdown of the minimum due trap shows exactly how this compounding effect works over a six-month period. Always target the full outstanding balance, not just the minimum.

Repeating cash advances every month

A single emergency cash advance is a cost. A monthly cash advance habit is a sign that regular income is not covering regular expenses — and using revolving credit card borrowing to bridge that gap makes the underlying problem progressively worse.

If you find yourself withdrawing cash from your credit card more than once in a quarter, it is worth reviewing your monthly budget and cash flow before the pattern becomes a debt cycle that is difficult to break.

Ignoring GST and ATM fees on your statement

The cash advance fee is one charge. GST at 18% is applied on top of it. Some ATMs operated by third-party networks may levy additional ATM operator charges beyond the issuer’s own fee. These secondary amounts are easily overlooked when mentally estimating the cost of a withdrawal.

Always read the full statement carefully after a cash advance to confirm every charge — including GST on card charges — and verify that the total matches what your MITC indicated.

Not reading the card MITC before withdrawing

Cash advance fees, monthly finance charge rates, and cash withdrawal limits vary by issuer and by card variant. The rate on an entry-level card from one bank may differ significantly from a premium card at the same bank. There is no uniform industry standard you can rely on. The only authoritative source for your card’s exact charges is the MITC document for your specific card.

Spending five minutes on your issuer’s website reading the Schedule of Charges can save you from an unexpected bill.

Using a cash advance to pay another credit card bill

Withdrawing cash from Card A to pay Card B’s dues is one of the clearest debt-spiral warning signs. It does not solve the liquidity problem — it relocates it while adding a cash advance fee, GST, and immediate interest on top of the existing balance.

If you are struggling to repay existing card dues, contact your issuer about hardship repayment options or balance restructuring before adding fresh borrowing to the problem.

When This May Not Be the Right Choice

You already carry revolving credit card dues from a previous month. Adding a cash advance on top of an existing outstanding balance means finance charges accrue on a larger combined amount from day one. The total cost grows faster than a standalone withdrawal calculation would suggest, and clearing it becomes harder with each cycle.

You cannot repay the full amount quickly. If repayment will stretch over two or more billing cycles, a personal loan with a fixed EMI schedule is almost certainly cheaper and more predictable. The structured repayment of a personal loan also reduces the risk of the balance compounding further.

A lower-cost option is available but less convenient. A salary advance from your employer, a transfer from a family member, or a pre-approved personal loan may require slightly more effort to arrange — but will cost you less in fees and interest. Convenience is not a sufficient reason to pay a premium for a credit card cash advance.

The cash is needed for discretionary or lifestyle spending. Withdrawing cash for shopping, dining, travel, or entertainment is paying extra for a feature that adds no financial benefit — especially when the same card used as a swipe purchase gives you a grace period.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit card cash advance charges — including fees, monthly finance charge rates, GST treatment, and cash withdrawal limits — are set by individual card issuers and must be disclosed in your cardholder MITC. These terms can change over time. Use the following official sources to verify current figures:

- Your card issuer’s website or app: Look for the Schedule of Charges or the Most Important Terms and Conditions (MITC) document specific to your card variant. The cash advance section will list the exact fee and rate applicable to your account.

- RBI — rbi.org.in: The Reserve Bank of India’s Master Directions on Credit Cards set the disclosure and fair practice framework applicable to all scheduled banks issuing credit cards in India. This is the regulatory foundation that governs how issuers must communicate charges to cardholders.

- Your monthly credit card statement: All cash advance fees, finance charges, and GST on card charges appear itemised on your statement after the transaction. Reviewing each line item is the simplest way to confirm what you were actually charged.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Repay the cash advance before adding new card spending. As soon as any salary or income inflow arrives after a cash advance, direct it toward clearing that balance first. Finance charges on the advance accrue daily from the withdrawal date. Understanding how your billing cycle rules interact with your statement helps you identify exactly when and how much to pay to minimise interest accumulation.

- Set a calendar alert the day after your withdrawal. Rather than waiting for your statement, set a reminder to check your card app the following day and plan the repayment date based on your next expected inflow. Even repaying two or three days earlier meaningfully reduces the finance charge portion.

- Do not use the same card for new purchases while the cash advance is outstanding. If cash flow is tight, avoid adding fresh transactions to the card until the advance is fully cleared. Some issuers apply incoming payments to lower-interest balances first, which means new purchases may attract interest even while you think you are repaying the cash advance.

- Build a ₹15,000 emergency liquid buffer. A small emergency reserve in a savings account or liquid mutual fund costs you nothing in fees or interest — and eliminates the need for a credit card cash advance in almost every salary-delay scenario. Starting this fund with ₹2,000–₹3,000 per month gets you there in six to seven months.

- Check your cash advance limit before you need it. Discovering your cash withdrawal sub-limit is lower than expected — or that the feature is disabled on your card — at an ATM during a genuine emergency is the worst possible moment. Log in to your card account today and note the exact limit, so you know what you can actually access.

- If you cannot repay in full, pay as much above the minimum as possible. Full repayment stops all further interest immediately. If that is not possible, every additional rupee paid above the minimum amount due reduces the outstanding balance on which finance charges are calculated, saving you money in the next cycle.

Frequently Asked Questions

Is credit card cash withdrawal allowed in India?

Yes, most credit cards issued in India allow cash withdrawal from ATMs, subject to a cash advance sub-limit set by the issuer. The limit is a portion of your total credit limit and varies by card type and issuer. Some entry-level or co-branded cards may restrict this feature. Check your card’s MITC or log in to your card account to confirm whether ATM cash withdrawal is enabled and what your current sub-limit is.

Is there a grace period on a credit card cash advance?

No. The interest-free grace period that applies to regular purchase transactions does not apply to cash advances. Interest on a credit card cash advance starts from the date of withdrawal — not from the statement generation date and not from the payment due date. This is the most important distinction between a purchase and a cash advance on the same credit card.

What is the cash advance fee on a credit card in India?

The cash advance fee varies by issuer, card variant, and the amount withdrawn. It is typically structured as a percentage of the withdrawn amount with a minimum fee floor, or as a flat fee. There is no uniform industry standard. The only accurate source for your card’s exact fee is your cardholder MITC or the Schedule of Charges on your issuer’s official website. Checking this before making any ATM withdrawal is strongly recommended.

Does a credit card cash advance affect my CIBIL score?

A cash advance itself does not appear as a separate negative item on your credit report. However, it increases your credit utilisation ratio — the percentage of your available credit you are using at any point — which can negatively affect your credit score if the utilisation becomes high. More significantly, if the cash advance leads to delayed payments or partial payments over subsequent billing cycles, those missed or partial payments will be reported to credit bureaus and can lower your score meaningfully.

Is a credit card cash advance better than a personal loan?

For most amounts and repayment timelines, a personal loan is likely cheaper. Personal loan interest rates in India are generally lower than the finance charges on a credit card cash advance, and interest on a personal loan is calculated on a reducing balance basis with a fixed EMI schedule. The trade-off is processing time — personal loans typically take one to three business days. If you need cash instantly and the amount is small with rapid repayment assured, the cash advance may be faster. Over any extended repayment period, the personal loan will almost certainly cost less.

Can I convert a credit card cash advance into EMI?

Some card issuers offer a cash-to-EMI conversion facility after a cash advance has been made. This converts the outstanding balance into structured monthly instalments, potentially at a lower effective rate than the standard cash advance finance charge. Not all issuers offer this on all card types, and a conversion fee may apply. If you have already made a cash advance and are concerned about repayment, contact your issuer directly to check whether this option is available for your card.

What happens if I pay only the minimum amount due after a cash advance?

Paying only the minimum amount due keeps your account current and avoids a late payment charge — but it does not stop interest from accruing on the remaining unpaid balance. Finance charges continue to compound daily on the full outstanding amount at the cash advance rate. Over two or three billing cycles of paying only the minimum, the total amount owed can increase substantially beyond the original withdrawal. The minimum due is a floor for account health, not a repayment strategy.

Can I use a credit card cash advance to pay off another credit card bill?

Technically possible, but financially counterproductive. Withdrawing cash from one card to pay another card’s dues means you now have two sources of high-interest debt instead of one. The original repayment problem is not resolved — it is relocated while gaining a new cash advance fee, GST, and immediate finance charges on top. If you are struggling to repay existing dues, speak to your card issuer about restructuring options or a hardship repayment plan before adding a cash advance to the situation.

Is credit card cash advance the same as a balance transfer?

No, they are different features. A cash advance involves withdrawing physical cash from an ATM using your credit card. A balance transfer involves moving an existing outstanding balance from one credit card to another — typically to take advantage of a lower or zero-percent promotional interest rate for a fixed period. Both have fees, but their purpose, structure, and cost profile are distinct. If your goal is to reduce the interest rate on existing dues, a balance transfer is the more relevant feature to explore.

Final Verdict

A credit card cash advance is a legitimate and accessible feature — but it is consistently one of the most expensive short-term borrowing options on a standard credit card. The combination of an upfront cash advance fee, GST, and interest that starts from the day of withdrawal means the cost meter runs from the moment you take the cash. There is no grace period, no interest-free window, and no way to reverse the fee even if you repay within 24 hours.

Used for a genuine cash emergency with full repayment in a few days, the total charge may be a reasonable and manageable cost. Used routinely, or when repayment is uncertain, it can quickly become a significant and compounding liability. In most situations, a debit card ATM withdrawal, emergency fund, personal loan, or salary advance will serve you better — at a lower total cost.

Check your card’s MITC before using this feature. Know your cash advance limit. Plan your repayment before you withdraw, not after.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.