Most salaried investors in India who finally decide to start an index fund SIP hit the same wall almost immediately: should I go with a Nifty 50 index fund, or is Nifty Next 50 worth considering because someone mentioned it returns more? The confusion is understandable. Both are passive equity mutual funds. Both track well-known NSE indices. But the risk profile, portfolio role, and suitability for a beginner are meaningfully different.

Nifty 50 vs Nifty Next 50 index funds is not a question with a universal right answer — it is a question about your risk capacity, your investment horizon, and how you will behave when markets fall 20% in three months. Chasing past returns without understanding these factors is one of the most common and costly mistakes in passive investing India. This article separates the two indices clearly, shows you how allocation decisions actually work, and helps you decide which belongs in your portfolio — and in what proportion.

Quick Answer: Nifty 50 vs Nifty Next 50 Index Funds

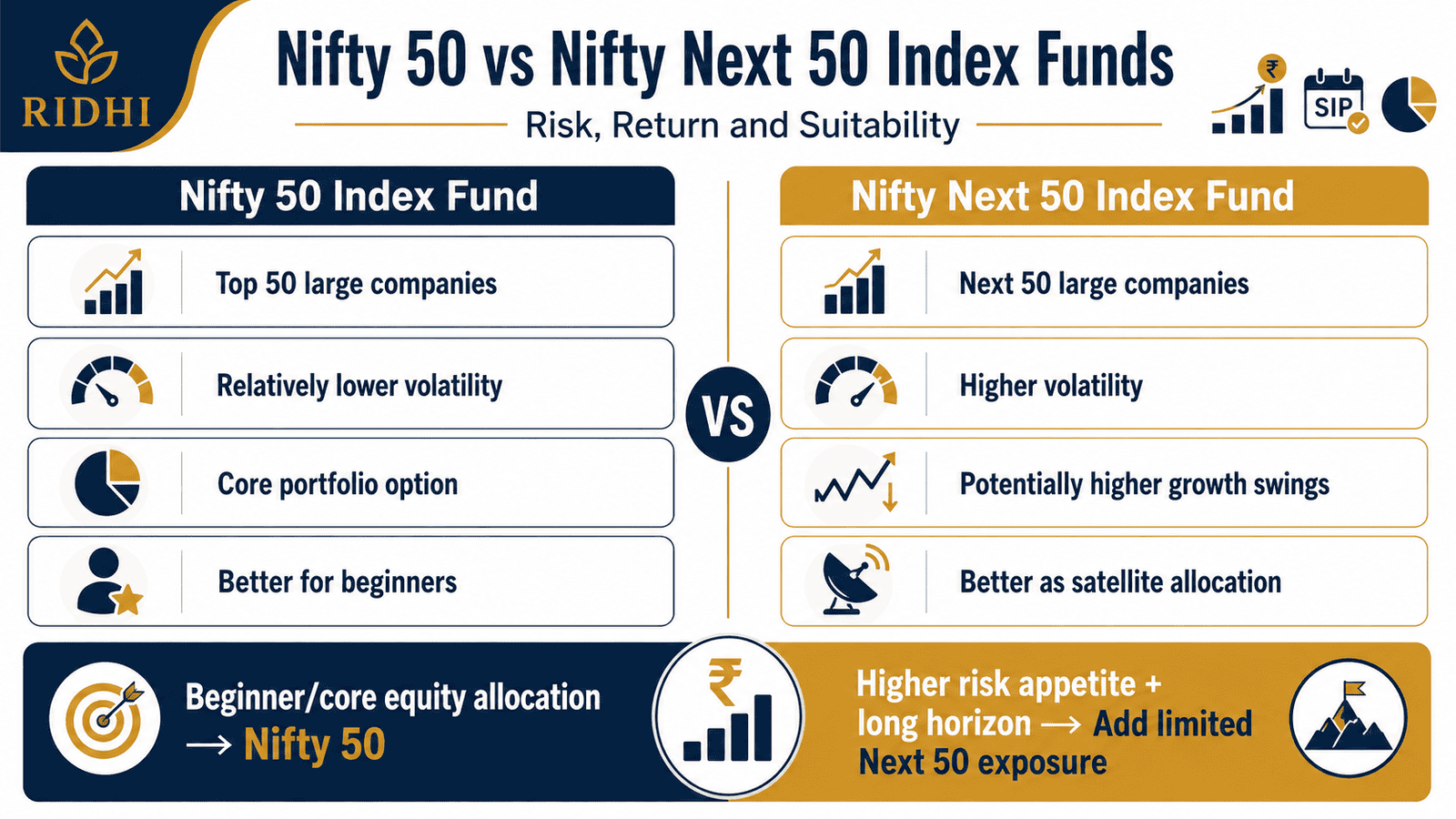

Nifty 50 vs Nifty Next 50 index funds is mainly a core-versus-satellite decision. Nifty 50 funds track the top 50 large companies, while Nifty Next 50 funds track the next 50 companies and usually carry higher volatility. For ₹10,000/month SIP planning, beginners should usually understand risk first, not chase past returns.

Key Takeaways

- Nifty 50 tracks India’s 50 largest companies by free-float market capitalisation and is commonly used as the core large-cap index exposure in a passive portfolio.

- Nifty Next 50 tracks the next 50 companies by size — ranked 51 to 100 — and has historically shown higher short-term volatility than Nifty 50.

- Past 1-year, 3-year, 5-year, and 10-year index returns must be verified before publishing; these figures change continuously and should be read from the NSE factsheet, not marketing material.

- Expense ratio and tracking error differ across funds tracking the same index — a 0.10% difference in expense ratio compounds significantly over a 10-year SIP horizon.

- A beginner investor does not need to split between multiple index funds on day one — starting with a single low-cost Nifty 50 fund is a legitimate and sensible first step.

- SEBI regulates mutual fund disclosures in India; all scheme information documents (SIDs) are publicly available at amfiindia.com.

Nifty 50 vs Nifty Next 50: Side-by-Side Comparison

| Parameter | Nifty 50 Index Fund | Nifty Next 50 Index Fund |

|---|---|---|

| Index tracked | Nifty 50 TRI | Nifty Next 50 TRI |

| Number of stocks | 50 | 50 |

| Company rank by size | Top 50 by free-float market cap | Ranked 51–100 by free-float market cap |

| Relative volatility | Lower | Higher |

| Portfolio role | Core holding | Satellite / add-on holding |

| Beginner suitability | More suitable | Moderate — with awareness |

| Drawdown risk | Lower in sharp market corrections | Higher — can fall more in downturns |

| Return potential (long-term) | Stable large-cap growth | Potentially higher — but with more variance |

| Expense ratio (direct plans) | Typically 0.05%–0.20% — verify at AMC | Typically 0.10%–0.30% — verify at AMC |

| Tracking error | Generally low — verify fund factsheet | Can be slightly higher — verify fund factsheet |

| AUM (category) | Very large — high liquidity | Smaller — verify at AMFI |

| Nifty 100 as alternative | Nifty 100 = Nifty 50 + Nifty Next 50 combined in one index |

Key Facts at a Glance

| Fact | Nifty 50 | Nifty Next 50 |

|---|---|---|

| Index operator | NSE Indices Ltd | NSE Indices Ltd |

| Rebalancing frequency | Semi-annual | Semi-annual |

| Eligibility to enter Nifty 50 | Already included | Next in line — potential future Nifty 50 entrants |

| Total Return Index (TRI) | Yes — dividends reinvested | Yes — dividends reinvested |

| Regulatory category (SEBI) | Large Cap Index Fund | Large Cap Index Fund |

| Minimum SIP (most funds) | ₹100–₹500 per month | ₹100–₹500 per month |

Understanding Nifty 50 vs Nifty Next 50 Index Funds

Before you pick a fund, it helps to understand what you are actually buying. Both are passive mutual funds that pool investor money and use it to replicate an index — your returns mirror the index, minus the fund’s costs. The difference lies entirely in which index each fund tracks.

What is a Nifty 50 Index Fund?

A Nifty 50 index fund tracks the Nifty 50 TRI — the Total Return Index version of the Nifty 50, which includes dividends reinvested. The Nifty 50 contains India’s 50 largest companies ranked by free-float market capitalisation, as maintained by NSE Indices Ltd. These are household names: Reliance Industries, HDFC Bank, Infosys, ICICI Bank, TCS, and similar blue-chip companies that have been publicly listed for years and account for a large share of India’s equity market value.

Because these companies are large, widely held, and heavily traded, the Nifty 50 tends to be relatively stable compared to mid-cap or small-cap indices. That does not mean it cannot fall — in the March 2020 correction, the Nifty 50 fell roughly 38% from its January 2020 peak. But compared to smaller indices, the recovery has historically been faster and the drawdown somewhat shallower.

What is a Nifty Next 50 Index Fund?

A Nifty Next 50 index fund tracks the Nifty Next 50 TRI — the 50 companies ranked 51st to 100th by free-float market capitalisation on the NSE. These are the companies that have graduated past mid-cap status but have not yet entered the top 50. They include companies in sectors such as capital goods, chemicals, consumer durables, and PSUs that may be on an upward trajectory.

The key difference is composition. The Nifty Next 50 tends to hold companies in less-liquid sectors with more concentrated sector exposure in any given year. When sectors like PSUs or infrastructure are in favour, Nifty Next 50 can significantly outperform Nifty 50. When they fall out of favour, the reverse happens — and the falls can be steeper. According to NSE Indices methodology documents available at nseindia.com, both indices rebalance semi-annually, which means the composition of each index shifts over time.

Why Does “Next 50” Mean More Volatility?

Size matters in equity markets. Smaller free-float means fewer buyers and sellers at any point, which amplifies price swings. The top 50 companies have large institutional holdings, continuous analyst coverage, and deep order books. The next 50 are still large-cap by SEBI classification but trade with somewhat less depth. Additionally, the next 50 companies often have higher earnings variability — some are on a growth path, others are restructuring, and a few may slip back into mid-cap territory at the next rebalancing.

Index Performance vs Fund Performance

This distinction matters enormously when comparing funds. Two funds tracking the same Nifty 50 index can deliver slightly different returns because of tracking error — the deviation between the fund’s actual return and the index return. Tracking error arises from cash drag, dividend reinvestment timing, and rebalancing costs. A well-managed Nifty 50 fund should have a tracking error close to zero. In practice, good direct plan funds are available with tracking errors below 0.10%. For Nifty Next 50 funds, tracking error can be marginally higher due to lower liquidity in the underlying stocks.

The expense ratio also compounds dramatically over time. If Fund A charges 0.10% and Fund B charges 0.25% for the same Nifty 50 index, on a ₹10,000 monthly SIP over 20 years, the difference in cost — while it seems small annually — can amount to a meaningful gap in final corpus. Always check the direct plan expense ratio in the Scheme Information Document (SID), available on amfiindia.com.

Real Example: Rohan’s ₹10,000 Monthly SIP Decision

Rohan, 31, is a software engineer in Bengaluru earning ₹1.6 lakh per month. He wants to start a ₹10,000 monthly SIP in an index fund. His goal is long-term wealth creation over 15–20 years, and he has never invested in equity mutual funds before. His confusion: is Nifty Next 50 better because someone in his office mentioned it had outperformed Nifty 50 over a certain past period?

Rohan has three realistic options. Understanding how SIP investing works helps frame each one clearly.

Option A — 100% Nifty 50: Rohan puts the full ₹10,000 into a single low-cost Nifty 50 direct plan index fund. Simple to track, easy to understand, and he does not need to rebalance two funds. This is the cleanest starting point for a first-time equity investor.

Option B — 80% Nifty 50 + 20% Nifty Next 50: Rohan puts ₹8,000 into Nifty 50 and ₹2,000 into Nifty Next 50. He gets limited exposure to the next 50 companies while keeping his core allocation stable. This adds some complexity but is manageable.

Option C — 70% Nifty 50 + 30% Nifty Next 50: Rohan puts ₹7,000 into Nifty 50 and ₹3,000 into Nifty Next 50. Higher satellite exposure — suits investors who have already experienced a market downturn and are comfortable with the extra volatility.

These are educational allocation examples and not personalised investment advice. The right split depends on Rohan’s actual risk appetite, not his neighbour’s portfolio. Key insight: if Rohan cannot hold his SIP steady during a 30% portfolio drop, Option A is the correct starting point — not the one with the best historical return.

How to Calculate Your Monthly SIP Split

Monthly SIP Split = Total Monthly SIP × Allocation Percentage

For Rohan’s ₹10,000 monthly SIP, here is how the three allocation models break down:

| Allocation Model | Monthly Split | Notes |

|---|---|---|

| 100% Nifty 50 | ₹10,000 → Nifty 50 | Simplest. Recommended starting point for beginners. |

| 80% Nifty 50 + 20% Nifty Next 50 | ₹8,000 → Nifty 50 | ₹2,000 → Nifty Next 50 | Limited satellite exposure. Manageable for aware beginners. |

| 70% Nifty 50 + 30% Nifty Next 50 | ₹7,000 → Nifty 50 | ₹3,000 → Nifty Next 50 | Higher risk. Suits investors with prior equity experience. |

Actual returns depend on market performance, fund expenses, tracking error, and your holding period. These figures do not represent guaranteed outcomes. Use the SIP calculator to test different scenarios with your own assumptions before committing to an allocation.

How to Decide What’s Right for You

This is your first equity index fund — THEN start with 100% Nifty 50. Keep it simple, build the investing habit, and revisit allocation after your first full market cycle.

You already invest in a Nifty 50 fund and want slightly higher long-term exposure — THEN consider adding Nifty Next 50 at 20% or less of your total equity SIP.

You want combined large-cap exposure without managing two separate funds — THEN a Nifty 100 index fund may offer a cleaner one-fund approach.

You have a long investment horizon of 10+ years and can stay invested through temporary losses of 30–40% — THEN a moderate Nifty Next 50 allocation may suit your risk capacity.

Your investment goal is 3–5 years away — THEN neither index fund may be appropriate for that specific goal; equity markets can be negative over short periods.

You cannot tolerate watching your portfolio fall significantly without stopping your SIPs — THEN avoid Nifty Next 50 for now. Pausing a SIP at a market low is one of the costliest mistakes in passive investing.

Common Mistakes to Avoid

Choosing a Fund Based Only on Last 1-Year Returns

One-year return rankings rotate unpredictably — the Nifty Next 50 may top a calendar year and underperform the next two years significantly.

Selecting a fund because it appeared on a “top performing funds” list after a bull run typically means buying at a high point for that particular index exposure.

Look at rolling returns over 3, 5, and 10 years instead, and verify them at the AMC factsheet or AMFI before deciding.

Ignoring Expense Ratio and Tracking Error

Both expense ratio and tracking error directly reduce your net returns — they are not administrative details.

On a ₹10,000 monthly SIP over 15 years, even a 0.15% difference in annual expense ratio can translate to a material difference in final corpus. Understand the direct vs regular plan cost difference before selecting a fund.

Always check the direct plan option, and verify current TER in the Scheme Information Document on the AMC website.

Allocating Too Much to Nifty Next 50 Without Understanding Drawdown Risk

Nifty Next 50 can experience sharper drawdowns than Nifty 50 during broad market corrections.

An investor putting 60–70% of their first SIP into Nifty Next 50 based on past return data may panic-stop during the first major correction, locking in losses permanently.

Keep Nifty Next 50 as a satellite allocation — not the bulk of a beginner portfolio.

Mixing Too Many Index Funds With Overlapping Holdings

Holding a Nifty 50 fund, a Nifty 100 fund, and a Nifty Next 50 fund simultaneously creates significant overlap — you may be buying many of the same companies three times.

Nifty 100 already contains the Nifty 50 and Nifty Next 50 stocks, so adding all three gives you heavy duplication without diversification.

Pick one primary approach: Nifty 50, Nifty Next 50 satellite, or Nifty 100 — not all three.

Choosing a Regular Plan Without Understanding Commission Costs

Regular plans of index funds pay distributor commissions that are built into a higher expense ratio — often 0.5%–1.0% higher than the direct plan of the same fund.

On a passive index fund, where the entire point is to minimise costs, selecting a regular plan reduces your advantage significantly.

Invest through direct plans unless you are receiving specific advisory services that justify the commission cost.

Treating Index Funds as Risk-Free Instruments

Index funds are equity mutual funds — they can lose value and have lost significantly during corrections like 2008, 2020, and other periods.

Equity index funds should not be used for emergency funds, near-term goals, or money you cannot afford to keep invested for at least 5–7 years.

Understand equity risk before investing, not after your first 20% portfolio drop.

When This May Not Be the Right Choice

Nifty 50 and Nifty Next 50 index funds are equity instruments. They are not suitable for every investor or every goal. You may want to reconsider these funds if any of the following apply.

If your investment horizon is under 3–5 years, equity index funds introduce a meaningful risk of negative returns over your target period — market corrections can take time to recover.

If you need the money as an emergency fund or for a near-term obligation such as a home down payment within 2 years, equity index funds are not appropriate — capital preservation matters more than growth at that stage.

If you are a low-risk investor who will feel significant distress watching a ₹1 lakh portfolio drop to ₹70,000 temporarily, Nifty Next 50 in particular may cause you to exit at exactly the wrong time.

If your overall portfolio has no debt allocation and you are near retirement, concentrating in equity index funds without a debt cushion can create sequence-of-returns risk at a critical time.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Index fund rules, expense ratio limits, and category definitions are regulated by SEBI. The following official sources should be your first stop before making any decision based on figures in this article — or in any article.

- NSE Indices (nseindia.com): Index methodology documents, factsheets, historical data, and semi-annual rebalancing announcements for Nifty 50, Nifty Next 50, and Nifty 100.

- AMC Scheme Information Documents: Current expense ratio, tracking error, AUM, portfolio composition, and exit load for any specific fund — available on the respective AMC website and on amfiindia.com.

- AMFI (amfiindia.com): Mutual fund category details, investor education resources, and consolidated NAV data across all schemes.

- SEBI (sebi.gov.in): Mutual fund regulations, SEBI circular on expense ratios, and investor grievance mechanisms.

- Income Tax Department (incometax.gov.in): Capital gains tax treatment for equity mutual funds — long-term capital gains (LTCG) tax rates and short-term capital gains (STCG) applicability should be verified here as these can change with the Union Budget.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

For reading return data correctly, understand the difference between CAGR, absolute, and XIRR returns before relying on any published performance figure.

Expert Tips

- Start with a single low-cost Nifty 50 direct plan index fund if this is your first equity SIP. Master the habit of investing consistently before you optimise allocation — a ₹10,000 SIP maintained through two corrections is worth more than a complex split portfolio you abandon.

- Add Nifty Next 50 only after you have experienced at least one meaningful market correction in your existing Nifty 50 portfolio. Your emotional response to a 25% drawdown will tell you more about your actual risk appetite than any risk questionnaire.

- If you want the combined exposure of both indices without managing two separate SIPs, a Nifty 100 index fund is worth checking — verify its expense ratio against simply holding both directly, since the cost difference varies by AMC.

- Always prefer direct plan index funds. For a fund tracking the same index, the only meaningful long-term differentiators are expense ratio and tracking error — both are lower in direct plans. Even a 0.20% annual saving on a 20-year SIP compounds materially.

- Review your allocation once or twice a year — not monthly. Monthly rebalancing based on market movements is a form of market timing and typically reduces returns in passive strategies. Annual or semi-annual review is sufficient for index fund portfolios.

- Do not confuse Nifty 100 with a diversified multi-cap fund. Nifty 100 holds only large-cap companies — all 100 stocks are from India’s top 100 by free-float market cap. If you want exposure to mid-cap or small-cap growth, you need separate allocations beyond large-cap index funds.

- When comparing two funds tracking the same Nifty 50 index, tracking difference (TD) — the gap between the fund’s actual annual return and the index return — is more informative than tracking error alone. Check both figures in the fund’s latest factsheet.

Frequently Asked Questions

Is Nifty Next 50 riskier than Nifty 50?

Yes, in general. Nifty Next 50 holds companies ranked 51–100 by free-float market capitalisation, which tend to have lower trading liquidity, higher sector concentration in any given period, and higher earnings variability than the top 50. This means the index typically experiences larger drawdowns during corrections and more pronounced rallies in favourable conditions. It is not a reason to avoid it — but it is a reason to understand it before allocating.

Is a Nifty 50 index fund enough for a beginner in India?

For most beginners, yes. A single low-cost Nifty 50 direct plan index fund gives you diversified exposure to India’s 50 largest companies across sectors. It is simple to track, transparent, regulated by SEBI, and has lower volatility than smaller indices. There is no obligation to add complexity early — starting simple and staying invested is more valuable for a new investor than optimising allocation from day one.

Should I invest in both Nifty 50 and Nifty Next 50?

It depends on your investment horizon and risk capacity. If you have a 10+ year horizon and are comfortable with temporary portfolio drops of 30–40%, a split of 80% Nifty 50 and 20% Nifty Next 50 is a reasonable structure used by many DIY passive investors in India. If you are new to equity investing, a single Nifty 50 fund first is the safer path to building the investing habit before adding complexity.

Is Nifty 100 better than holding Nifty 50 and Nifty Next 50 separately?

It can be, depending on the costs involved. Nifty 100 is essentially the combination of Nifty 50 and Nifty Next 50 — all 100 companies in one index. The advantage is simplicity: one SIP, one fund, one portfolio line to track. The trade-off is that you cannot customise your split — a Nifty 100 fund typically weights stocks by market cap, which means Nifty 50 stocks dominate the allocation automatically. Compare the direct plan expense ratio of a Nifty 100 fund against your two-fund alternative before deciding.

Which gives better returns: Nifty 50 or Nifty Next 50?

This cannot be answered with a fixed number because past return rankings change with the time period measured. Over certain 10-year windows, Nifty Next 50 has delivered higher absolute returns than Nifty 50. Over other periods, particularly those that include sharp corrections, Nifty 50 has held up better. Return comparisons must be verified using current data from NSE factsheets — do not rely on historical figures quoted in articles, including this one.

How much should I allocate to Nifty Next 50 in my portfolio?

There is no universally correct answer, and any specific number depends on your total portfolio size, existing equity exposure, risk tolerance, and time horizon. A common educational framework used by passive investing communities in India suggests treating Nifty Next 50 as a satellite allocation — meaning a smaller percentage than your core Nifty 50 holding. Many investors use 10%–30% of their total equity allocation for Nifty Next 50, but this is illustrative, not prescriptive. Consult a SEBI-registered investment adviser if you need personalised allocation guidance.

What is the difference between Nifty 50 TRI and Nifty 50 index?

The Nifty 50 index tracks only price returns — it does not include dividends paid by the underlying companies. The Nifty 50 TRI (Total Return Index) includes dividends reinvested, which gives a more accurate picture of actual investor returns. SEBI requires mutual funds to benchmark their performance against the TRI rather than the price return index. When comparing your fund’s performance, always check against the TRI figure, not the plain Nifty 50 price index.

Can I start a Nifty Next 50 SIP with ₹500 per month?

Yes. Most Nifty Next 50 direct plan index funds available on major platforms in India allow SIPs starting from ₹100–₹500 per month. The minimum varies by fund and platform — check the specific scheme’s terms on the AMC website or a SEBI-registered investment platform. The low minimum makes it accessible, but accessibility does not reduce the underlying risk of the index itself.

What happens to my Nifty Next 50 fund when a company moves into the Nifty 50?

When a company is promoted from Nifty Next 50 to Nifty 50 at a semi-annual rebalancing, the Nifty Next 50 index drops that stock and adds the next eligible company. Your Nifty Next 50 fund will sell the promoted stock and buy the new entrant to track the updated index. You do not need to do anything — the fund manager handles rebalancing. However, this rebalancing creates some tracking costs and can contribute to tracking error in the fund.

Is investing in Nifty 50 and Nifty Next 50 index funds tax-efficient?

Equity mutual fund returns in India are subject to capital gains tax. Gains on units held for more than 12 months are taxed as long-term capital gains (LTCG), and those held for 12 months or less are taxed as short-term capital gains (STCG). The applicable tax rates should be verified at incometax.gov.in, as these can change with the Union Budget. Index funds do not have additional tax benefits compared to other equity mutual funds — their advantage is low cost and transparency, not preferential tax treatment.

Final Verdict

Nifty 50 vs Nifty Next 50 index funds is not a contest with a single winner — it is a portfolio construction question. For most Indian beginners, a single low-cost Nifty 50 direct plan index fund is the cleaner, less volatile starting point. It gives you exposure to India’s 50 largest, most liquid companies, and it is easy to understand and monitor.

Nifty Next 50 can meaningfully complement a Nifty 50 allocation for investors who have a 10+ year horizon, have already weathered a market correction, and can stay invested through deeper temporary drawdowns. Treat it as a satellite — not a replacement for a core allocation.

If you want combined large-cap exposure without managing two funds, Nifty 100 is worth evaluating. But whichever route you choose, the variables that matter most are cost (expense ratio), consistency (tracking error), and your own behaviour during downturns. For a broader view of where index funds fit in your overall strategy, read the comparison of index funds versus active funds for Indian investors before finalising your allocation.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Arjun Kapoor writes about mutual funds, SIPs, ELSS, fund categories, investment returns, and beginner investing concepts for Indian readers. His focus is on education, not product promotion or fund recommendations. He helps readers understand how mutual funds work before they start investing or comparing schemes.

He covers topics such as mutual fund meaning, SIP meaning, SIP calculator, direct mutual funds vs regular plans, NAV, ELSS tax-saving funds, CAGR, absolute returns, XIRR, expense ratio, large cap vs mid cap vs small cap funds, flexi cap funds, index funds vs active funds, liquid funds, debt mutual funds, SIP pause vs SIP stop, lumpsum vs SIP, and how to start SIP in India.

Arjun’s writing is simple, risk-aware, and long-term oriented. He avoids guaranteed-return language and explains investment concepts using examples, timelines, and comparison tables. His articles remind readers that mutual fund investments are subject to market risks, and past performance does not guarantee future returns. Readers should verify scheme details from SEBI, AMFI, fund houses, and official scheme documents.