Every year, as March 31 approaches, the same search spike happens: “best ELSS funds for 80C.” Thousands of salaried taxpayers invest hurriedly, picking whichever fund topped a recent return chart. Then they forget that equity markets don’t care about tax-saving season — and that every SIP instalment locks in separately for three years.

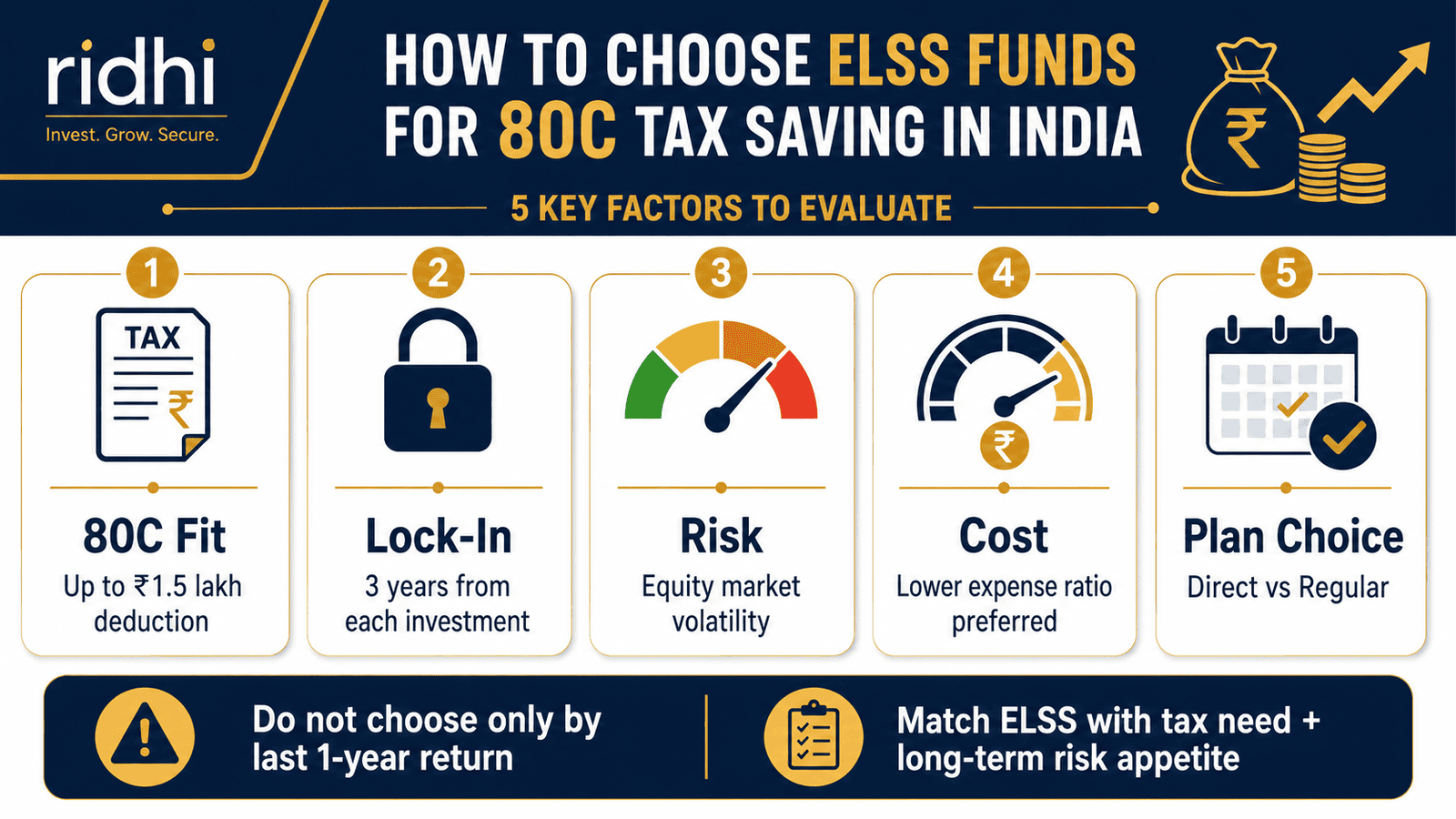

If you’re on the old tax regime and trying to figure out how to choose ELSS funds without blindly trusting a “top 10” list, this article is for you. ELSS — Equity Linked Savings Scheme — is an equity mutual fund, not a fixed-return product. It offers a Section 80C deduction, but the money you put in rides stock market ups and downs. Choosing the right ELSS fund means getting the tax fit right first, then checking cost, consistency, risk, and exit timing — in that order.

Quick Answer: How to Choose ELSS Funds

How to choose ELSS funds depends on tax fit, fund cost, risk and consistency. Check whether you need Section 80C deduction up to ₹1.5 lakh, compare expense ratio, review the 3-year lock-in per instalment, avoid chasing 1-year returns, and choose a fund matching your equity risk appetite.

Key Takeaways

- ELSS gives a Section 80C deduction only under the old tax regime — if you’ve switched to the new regime, the tax benefit does not apply to you.

- Every SIP instalment in an ELSS fund locks in separately for 3 years — a ₹5,000 SIP started in April 2024 is not free until April 2027.

- The difference in expense ratio between a direct plan and a regular plan of the same ELSS fund is often 0.5%–1% per year — on a ₹1.5 lakh investment held for 10 years, that gap compounds into thousands of rupees.

- 1-year ELSS return rankings shuffle dramatically each year; 3-year, 5-year, and rolling return consistency across market cycles is a far better selection signal.

- You do not need to invest ₹1.5 lakh in ELSS — invest only the unused 80C gap after accounting for EPF, insurance premiums, and home loan principal.

- Mutual fund investments are subject to market risks. Past performance does not guarantee future returns.

- SEBI mandates that all mutual funds display a riskometer — check it before investing, as ELSS funds carry high equity market risk.

ELSS vs Other 80C Options — and ELSS Selection Parameters Compared

| Parameter | ELSS | PPF / Tax-Saving FD |

|---|---|---|

| Return type | Market-linked (equity) | Fixed / guaranteed rate |

| Lock-in period | 3 years per instalment | PPF: 15 years; Tax FD: 5 years |

| Risk level | High — equity risk | Low — fixed income |

| Liquidity after lock-in | Redeemable at market value | PPF: partial after year 7; FD: locked 5 years |

| Tax on returns | LTCG applies above ₹1 lakh per year (verify current rate) | PPF: tax-free; FD interest: taxable as income |

| Section 80C deduction | Yes | Yes |

| Wealth creation potential | Higher over long term | Moderate to low |

| Selection Parameter | What to Check | Why It Matters |

|---|---|---|

| Expense ratio | Direct plan vs regular plan TER | Lower cost = more returns retained annually |

| Return consistency | 3-year, 5-year, rolling returns | Avoids funds that spike one year and underperform the next |

| Fund style | Large-cap heavy vs flexi-cap vs mid-cap tilt | Aligns portfolio risk with your risk tolerance |

| AUM and fund age | Fund should have sufficient track record | Newer or very small funds have limited performance history |

| Riskometer | SEBI-mandated risk label on fund documents | Confirms your risk appetite matches fund category |

| Fund manager continuity | Stable vs recently changed management | Process-driven funds are less dependent on one manager |

For a deeper side-by-side comparison of ELSS and PPF across lock-in, return potential, and suitability, see PPF or ELSS choice.

Key Facts at a Glance

| Feature | Detail |

|---|---|

| Product type | Equity Linked Savings Scheme — an equity mutual fund |

| Section 80C deduction | Up to ₹1.5 lakh per year (verify current limit at incometax.gov.in) |

| Lock-in period | 3 years per investment or SIP instalment (verify at SEBI/AMC SID) |

| Return type | Market-linked; not guaranteed |

| Risk level | High — equity market risk; SEBI riskometer: Very High for most ELSS funds |

| Tax regime fit | Old regime only; new regime does not allow 80C deductions |

| Tax on gains | Long-term capital gains tax applies on redemption — verify current rate |

| Plan options | Direct plan (lower cost) and regular plan (via distributor) |

| Minimum investment | As low as ₹500 via SIP on most platforms |

What Is ELSS and How Does It Fit Into 80C?

ELSS — Equity Linked Savings Scheme — is a category of diversified equity mutual fund that also qualifies for tax deduction under Section 80C of the Income Tax Act. According to the Income Tax Department (incometax.gov.in), Section 80C allows deductions on eligible investments up to a specified annual limit — verify the current limit before publishing, as Budget announcements can revise it.

Inside 80C, ELSS competes with a long list of instruments: Employee Provident Fund (EPF) contributions, Public Provident Fund (PPF), life insurance premiums, home loan principal repayment, National Savings Certificate (NSC), tax-saving fixed deposits, and more. The key difference is that ELSS is the only equity instrument in the 80C basket — every other option is either fixed-income or insurance-linked. For a full map of what fits inside Section 80C, see 80C deduction options.

Being an equity mutual fund means ELSS invests primarily in stocks. Your returns depend on how those stocks perform — there is no capital protection, no maturity value, and no guaranteed interest rate. The “tax-saving” label on the tin does not change what is inside: market-linked returns with all the volatility that comes with equity investing.

Old Regime vs New Regime: The First Question to Answer

Before spending even a minute comparing ELSS funds, answer one question: are you on the old tax regime? Section 80C deductions — including ELSS — are only available under the old regime. If you have already opted for the new regime, investing in ELSS gives you the equity exposure of the fund but zero additional tax deduction. There is no point picking an ELSS fund to “save tax” if you are not using the old regime to begin with. Use the income tax calculator to check which regime is more beneficial for your salary structure before deciding.

If the old regime does benefit you, the next question is: how much of your ₹1.5 lakh 80C limit is already used by EPF contributions and insurance premiums? Most salaried employees automatically contribute to EPF — that amount already counts. Invest only the remaining gap in ELSS, not the full ₹1.5 lakh. For beginners who need a clearer foundation before comparing funds, tax-saving fund basics explains the fundamentals first.

Why ELSS Has the Shortest Lock-In in 80C

At 3 years per instalment, ELSS has the shortest mandatory lock-in of any 80C product. PPF locks in for 15 years with only partial withdrawal provisions after year 7. Tax-saving FDs lock in for 5 years. ELSS at 3 years is relatively liquid — but only after each instalment completes its own 3-year cycle. According to SEBI (sebi.gov.in), each SIP instalment is treated as a separate investment for lock-in calculation purposes. That means flexibility is real, but staggered.

Real Example: Rohit’s ELSS Selection in Pune

Rohit, 31, is a product manager in Pune earning ₹18 lakh per year. He’s on the old tax regime and wants to reduce his taxable income before March 31. His EPF contribution for the year works out to roughly ₹43,200 (employee share at 12% of basic of ₹36,000 per month — illustrative). He also pays ₹18,000 per year in term insurance premiums. That puts him at approximately ₹61,200 of 80C already used — leaving roughly ₹88,800 of unused 80C space (assuming the ₹1.5 lakh limit applies — verify current limit before publishing).

Rohit does not need to invest ₹1.5 lakh in ELSS. He needs to invest only ₹88,800 to exhaust his 80C gap. At a 30% tax bracket (illustrative — verify applicable slab), the tax saving on ₹88,800 is approximately ₹26,640 — not ₹46,800. Investing more than ₹88,800 in ELSS gives additional equity exposure but no additional 80C tax benefit.

When comparing two ELSS fund options, Rohit looks at 3-year and 5-year returns instead of 1-year rankings, checks whether the direct plan expense ratio is at least 0.5% lower than the regular plan, and reviews the fund’s portfolio style — large-cap-heavy funds carry lower volatility than mid-cap-tilted ELSS. Since it is February and he has a lump sum available, he invests in one go rather than spreading into a SIP with multiple lock-in expiry dates. The key insight: the fund with the highest 1-year return was not the same fund that had the best 3-year and 5-year consistency when Rohit checked rolling return data.

How to Calculate Your Actual ELSS Investment Need

ELSS Amount Needed = Section 80C Limit − (EPF + Life Insurance Premium + Home Loan Principal + Other 80C Items)

Step 1: Add up your existing 80C contributions for the year. For a salaried employee, start with EPF — your monthly basic salary × 12% × 12 months gives the annual employee EPF contribution. Add any life insurance premiums, PPF deposits already made, and home loan principal paid.

Step 2: Subtract that total from the current 80C limit (verify at incometax.gov.in before publishing). The remaining amount is your ELSS gap — invest only this much for pure tax-saving purposes.

Step 3: Compare expense ratios across two or three shortlisted ELSS funds. The table below is illustrative — actual TERs change and must be verified on AMC websites or AMFI (amfiindia.com):

| Scenario | Expense Ratio (Illustrative) | Impact on ₹88,800 over 10 years at 12% gross return |

|---|---|---|

| Lower-cost direct plan fund | ~0.7% TER (illustrative) | Higher net corpus — more of the 12% gross return is retained |

| Higher-cost regular plan fund | ~1.6% TER (illustrative) | Lower net corpus — ~0.9% drained annually via distributor commission |

These are illustrative figures to show the direction of impact, not a projection of actual returns. For a detailed breakdown of how expense ratio compounds into wealth loss over time, see fund expense impact. The takeaway is directional: lower cost helps, but it is not the only criterion — consistency and fund quality must come first.

How to Decide What’s Right for You

You are on the old tax regime and have unused 80C space after EPF and insurance — THEN ELSS is worth considering as your equity allocation within 80C.

Your 80C limit is already fully used by EPF, PPF, insurance and home loan principal — THEN investing in ELSS gives no additional 80C tax benefit; consider it only as a plain equity mutual fund investment.

You are confident about managing your own investments and do not need distributor guidance — THEN a direct ELSS plan will save you 0.5%–1% in annual expense ratio versus the regular plan, compounding in your favour over the 3-year lock-in and beyond.

You want to reduce timing risk across the year — THEN a monthly SIP spreads market entry across 12 months, though remember each instalment starts its own separate 3-year lock-in clock.

You are comparing two similar ELSS funds and one has 3-year and 5-year rolling returns ahead of the other with a lower expense ratio — THEN cost and consistency together are a stronger signal than 1-year return ranking alone.

You cannot stay invested for at least 3 years or cannot tolerate the possibility of your investment value falling significantly — THEN ELSS is not the right 80C choice for you regardless of recent returns. For the direct vs regular plan decision, see direct regular plan choice.

Common Mistakes to Avoid

Picking the Fund with the Highest 1-Year Return

1-year return rankings in equity funds change dramatically from year to year depending on which market segment performed — large-cap, mid-cap, or sectoral.

A fund that topped the ELSS chart in FY2023 may have been the 15th-ranked fund in FY2024. You end up chasing last year’s winners into this year’s underperformers.

Instead, compare 3-year, 5-year, and rolling returns across at least two market cycles before shortlisting a fund.

Assuming the Entire ₹1.5 Lakh Needs to Go into ELSS

Many salaried employees invest ₹1.5 lakh in ELSS without realising that EPF already covers a large part of their 80C limit.

Over-investing in ELSS for tax purposes means locking more money into a 3-year equity instrument than the tax benefit justifies — the extra amount gets the equity risk but zero additional deduction.

Calculate the actual 80C gap before investing a single rupee in ELSS.

Ignoring the Per-Instalment Lock-In on SIPs

Every SIP instalment has its own independent 3-year lock-in. A ₹10,000 SIP started in April has 12 separate lock-in expiries spread across the next 4+ years — not one single exit date.

If you start an ELSS SIP expecting to redeem the full amount after exactly 3 years from the first instalment, you will find that only the first instalment is free; the rest are still locked.

Plan redemption dates separately for each batch of instalments, or consider a lumpsum investment if you need a clean exit date.

Choosing a Regular Plan Without Understanding the Cost

A regular ELSS plan routes your investment through a distributor who earns a commission — paid out of the fund’s expense ratio, not separately billed to you.

The visible impact: the direct plan’s NAV grows slightly faster every year because no commission is deducted. On a ₹1.5 lakh investment held for 10 years, a 0.8% annual cost difference can mean a gap of ₹15,000–₹25,000 in final corpus (illustrative — depends on actual returns).

If you don’t need distributor guidance, use a direct plan via an AMC website or a direct-plan mutual fund platform.

Redeeming Immediately After the 3-Year Lock-In Regardless of Market Conditions

The lock-in is a minimum holding period — it does not mean you should redeem the moment the clock runs out.

Redeeming in a market downturn immediately post-lock-in crystallises losses that time might have recovered. ELSS is an equity investment; exit when it suits your goal and market conditions, not just because the lock-in expired.

Treat the 3-year lock-in as a floor, not a target.

Not Checking Whether Old Regime Still Benefits You

The new tax regime removed the 80C deduction — if you are now under the new regime or considering switching, ELSS no longer saves you tax.

Investing in ELSS purely for 80C while actually being on the new regime is a mistake that locks your money in equity for 3 years with no tax benefit at all.

Check your regime before every financial year’s tax-saving investments.

When This May Not Be the Right Choice

You are on the new tax regime. Section 80C deductions are not available under the new regime. Investing in ELSS will give you equity exposure but zero tax deduction — you may be better served by a regular equity mutual fund without the 3-year lock-in constraint.

You need the money within 3 years. ELSS locks in each investment for 3 years. If you expect to need this money for a wedding, home purchase, or medical emergency before the lock-in expires, do not invest it in ELSS — the lock-in is strictly enforced, and equity values may also be lower at the point you need funds.

You cannot tolerate equity volatility. ELSS is a Very High risk product on SEBI’s riskometer. If seeing your investment fall 25–40% in a bear market would cause panic selling or financial distress, ELSS is not suitable — consider PPF, tax-saving FDs, or NPS instead for the conservative portion of your 80C.

Your 80C is already exhausted through other instruments. If EPF, PPF, home loan principal, and life insurance already fill your ₹1.5 lakh 80C limit, adding ELSS gives no incremental tax benefit. Invest in equity through regular mutual funds without the lock-in.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- Income Tax Department — incometax.gov.in: Verify the current Section 80C deduction limit, applicable tax regime rules, and long-term capital gains tax treatment on equity mutual fund redemptions.

- SEBI — sebi.gov.in: Verify ELSS category definition, riskometer norms, TER (Total Expense Ratio) regulations, and any changes to lock-in rules for tax-saving mutual funds.

- AMFI — amfiindia.com: Check current Total Expense Ratios for specific ELSS funds and compare direct vs regular plan TER disclosures.

- AMC websites: Download the Scheme Information Document (SID) and Key Information Memorandum (KIM) for the specific ELSS fund you are considering before investing.

Expert Tips

- Start in April, not March. Tax-saving investment decisions made in March are rushed. Start your ELSS SIP in April so you have 11 months of market averaging and no year-end panic. The tax benefit is the same whether you invest in April or March.

- Compare rolling returns, not point-to-point. A fund that returned 18% in one year could have returned 8% in another. Rolling 3-year returns across many rolling periods reveal whether the fund consistently beats its benchmark — that consistency matters more than peak returns.

- Use a direct plan if you invest independently. If you are using a fund aggregator app or AMC website directly, there is little reason to use a regular plan. The 0.5%–1% annual saving on a direct plan adds up across the entire holding period of your ELSS.

- Match fund style to your risk tolerance. ELSS funds vary — some are large-cap-heavy (lower volatility), others hold significant mid-cap allocations (higher return potential, higher risk). Check the fund’s actual portfolio before committing, not just the star rating.

- Remember: lock-in does not equal exit date. Many investors redeem the day the lock-in ends. That may coincide with a market low. If your goal is still years away, staying invested post-lock-in in a good ELSS fund makes as much sense as staying invested in any equity mutual fund. For the SIP vs lumpsum trade-off, see SIP or lumpsum.

- Don’t over-diversify across ELSS funds. Picking 4–5 different ELSS funds to “diversify” often means you’re holding similar large-cap stocks across all of them with higher combined complexity. One or two well-researched ELSS funds are usually enough for the tax-saving allocation.

Frequently Asked Questions

Is ELSS better than PPF for 80C tax saving?

It depends on your risk appetite and goal timeline. ELSS has the potential for higher long-term returns as an equity investment and has a shorter 3-year lock-in, but comes with equity market risk and no guaranteed returns. PPF offers guaranteed, tax-free returns and capital safety but locks your money for 15 years. If you can tolerate equity volatility and have a horizon beyond 3 years, ELSS has historically delivered stronger wealth creation — but past performance does not guarantee future returns. Many investors use both: PPF for safety, ELSS for growth potential.

Is ELSS safe to invest in?

ELSS invests in equity markets and carries high risk — SEBI classifies most ELSS funds as Very High risk on the riskometer. Your principal is not protected, and the value of your investment can fall significantly in market downturns. It is not a safe, capital-protected product. It is suitable only if you can stay invested through market cycles and do not need the money within the 3-year lock-in period.

Should I invest in ELSS through SIP or lumpsum?

Both are valid. SIP spreads your investment across months, reducing the timing risk of investing a large sum at a market peak. Lumpsum is simpler if you have the money available and want a clean single lock-in expiry date. The tax benefit under 80C is the same either way — what changes is your market entry timing and lock-in tracking complexity. For a detailed comparison, the SIP or lumpsum article covers the trade-offs in full.

Does every SIP instalment in ELSS have a separate lock-in?

Yes. Each SIP instalment is treated as a separate investment with its own 3-year lock-in period starting from the date that instalment is processed. If you start a ₹5,000 monthly SIP in April 2025, your April 2025 instalment unlocks in April 2028, your May 2025 instalment unlocks in May 2028, and so on. You cannot redeem the full SIP corpus after exactly 3 years from the first instalment.

Should I choose the ELSS fund with the lowest expense ratio?

Not exclusively. Expense ratio is an important factor — especially between direct and regular plans of the same fund — but it is one of several criteria. A fund with a slightly higher TER but stronger 5-year rolling return consistency and a stable, process-driven management approach may still be a better choice than the cheapest fund with erratic performance. Use expense ratio as a tie-breaker among similarly performing funds, not as the sole selection criterion.

Can I redeem ELSS after 3 years?

Yes — after each instalment completes its 3-year lock-in, it is available for redemption. There is no exit load typically applied after the lock-in period, but verify with the AMC’s Scheme Information Document for current terms. Also check the applicable long-term capital gains tax on equity mutual fund redemptions at the time of exit — tax rules can change. Verify current LTCG treatment at incometax.gov.in before redeeming.

What happens if I invest in ELSS but I’m on the new tax regime?

Your investment is processed normally and your money is invested in the equity fund. But you receive no Section 80C tax deduction — the new tax regime does not allow 80C deductions. Your money is locked in for 3 years as with any ELSS investment, but the tax-saving purpose is not achieved. If you are on the new regime, consider a regular equity mutual fund without the lock-in constraint instead.

Can I claim 80C deduction on ELSS SIP started last year?

You can claim 80C deduction on ELSS instalments paid during the financial year you are filing taxes for — April 1 to March 31. Instalments paid in April 2024 to March 2025 are eligible for deduction in AY2025-26 (FY2024-25), for example. You cannot carry forward unused deductions from a prior year. Verify the current 80C deduction limit and applicable financial year rules at incometax.gov.in before filing.

Is the growth option better than the IDCW option in ELSS?

For most investors, the growth option is preferable. In the growth option, gains are reinvested in the fund and the NAV compounds over time. In the IDCW (Income Distribution cum Capital Withdrawal) option, dividends are paid out periodically — but these are taxed as ordinary income in the year of receipt, which reduces the compounding benefit. For a long-term investment like ELSS where the lock-in already encourages staying invested, growth option typically delivers better post-tax outcomes. Verify current tax treatment of IDCW payouts with your tax advisor.

Final Verdict

Knowing how to choose ELSS funds starts with one foundational question: do you actually need the 80C deduction? If you are on the old regime with unused 80C space and a 3-plus year horizon, ELSS gives you equity market exposure with a tax benefit — a combination no other 80C instrument offers. But it is not a safe product, and it should not be chosen only because a friend recommended it or a return chart looked impressive.

Select based on this sequence: tax regime fit first → calculate your actual 80C gap → shortlist funds by 3-year and 5-year rolling return consistency → compare expense ratios between direct and regular plans → check fund style and riskometer → then decide SIP or lumpsum based on your cash flow and exit planning needs.

ELSS is not the best 80C option for everyone. If equity risk does not suit your timeline or temperament, PPF, NPS, or a tax-saving FD may serve you better. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Arjun Kapoor writes about mutual funds, SIPs, ELSS, fund categories, investment returns, and beginner investing concepts for Indian readers. His focus is on education, not product promotion or fund recommendations. He helps readers understand how mutual funds work before they start investing or comparing schemes.

He covers topics such as mutual fund meaning, SIP meaning, SIP calculator, direct mutual funds vs regular plans, NAV, ELSS tax-saving funds, CAGR, absolute returns, XIRR, expense ratio, large cap vs mid cap vs small cap funds, flexi cap funds, index funds vs active funds, liquid funds, debt mutual funds, SIP pause vs SIP stop, lumpsum vs SIP, and how to start SIP in India.

Arjun’s writing is simple, risk-aware, and long-term oriented. He avoids guaranteed-return language and explains investment concepts using examples, timelines, and comparison tables. His articles remind readers that mutual fund investments are subject to market risks, and past performance does not guarantee future returns. Readers should verify scheme details from SEBI, AMFI, fund houses, and official scheme documents.