Every month, your salary hits your savings account. Money moves in and out — EMIs, UPI payments, groceries, rent. Then one day you notice a small credit labelled “interest” on your bank statement, and it’s far smaller than you expected. If ₹1–2 lakh sat in that account all quarter, why did you earn only a few hundred rupees?

The answer lies in how banks actually calculate savings account interest — and most people have never been told. Banks in India use the daily balance method, also called the daily product basis, which means your interest is recalculated every single day based on your closing balance that night. Frequent withdrawals, mid-month transfers, and balance fluctuations all affect the final number.

This article covers the savings account interest calculation formula, a step-by-step rupee example, how interest is credited, its tax treatment, and how a savings account compares with an FD or sweep-in FD. Rates and bank terms can change without notice — always verify current figures from your bank directly.

Quick Answer: Savings Account Interest Calculation

Savings account interest calculation in India usually uses the daily balance method: daily interest equals closing balance multiplied by annual rate divided by 365. For example, ₹1,00,000 at 3% p.a. earns about ₹8.22 per day before rounding, and banks generally credit accumulated interest quarterly. Verify the applicable rate with your bank before drawing any conclusions — rates vary by bank and balance slab.

Key Takeaways

- Savings account interest in India is almost always calculated on your daily closing balance — not on a monthly average or minimum balance.

- The formula is simple: Daily interest = Closing balance × Annual rate ÷ 365. On ₹1,00,000 at 3% p.a., that is roughly ₹8.22 per day.

- Most banks credit savings account interest quarterly — but crediting frequency can vary by bank and account type. Check your account terms.

- If your balance drops mid-quarter because of a large withdrawal, your accumulated interest resets to a lower daily run-rate from that day forward.

- Savings account interest is fully taxable as income. Under Section 80TTA, individuals (other than senior citizens) can claim a deduction up to ₹10,000 per year on savings account interest — verify current limits with the Income Tax Department.

- Savings accounts are best kept for liquidity — salary, bills, EMIs, and emergencies. Surplus money left idle for months usually earns significantly less than a comparable fixed deposit.

Key Facts at a Glance

| Parameter | Details | Where to Verify |

|---|---|---|

| Calculation basis | Daily closing balance (daily product basis) | rbi.org.in |

| Formula | Daily interest = Balance × Annual rate ÷ 365 | Your bank’s schedule of charges |

| Crediting frequency | Usually quarterly — check your bank’s terms | Bank statement / passbook |

| Tax treatment | Fully taxable; deduction available under 80TTA / 80TTB (limits — verify) | incometax.gov.in |

| Best suited for | Liquidity: salary, bills, UPI, EMIs, emergency fund | — |

| Not ideal for | Long-term surplus that could earn higher returns elsewhere | — |

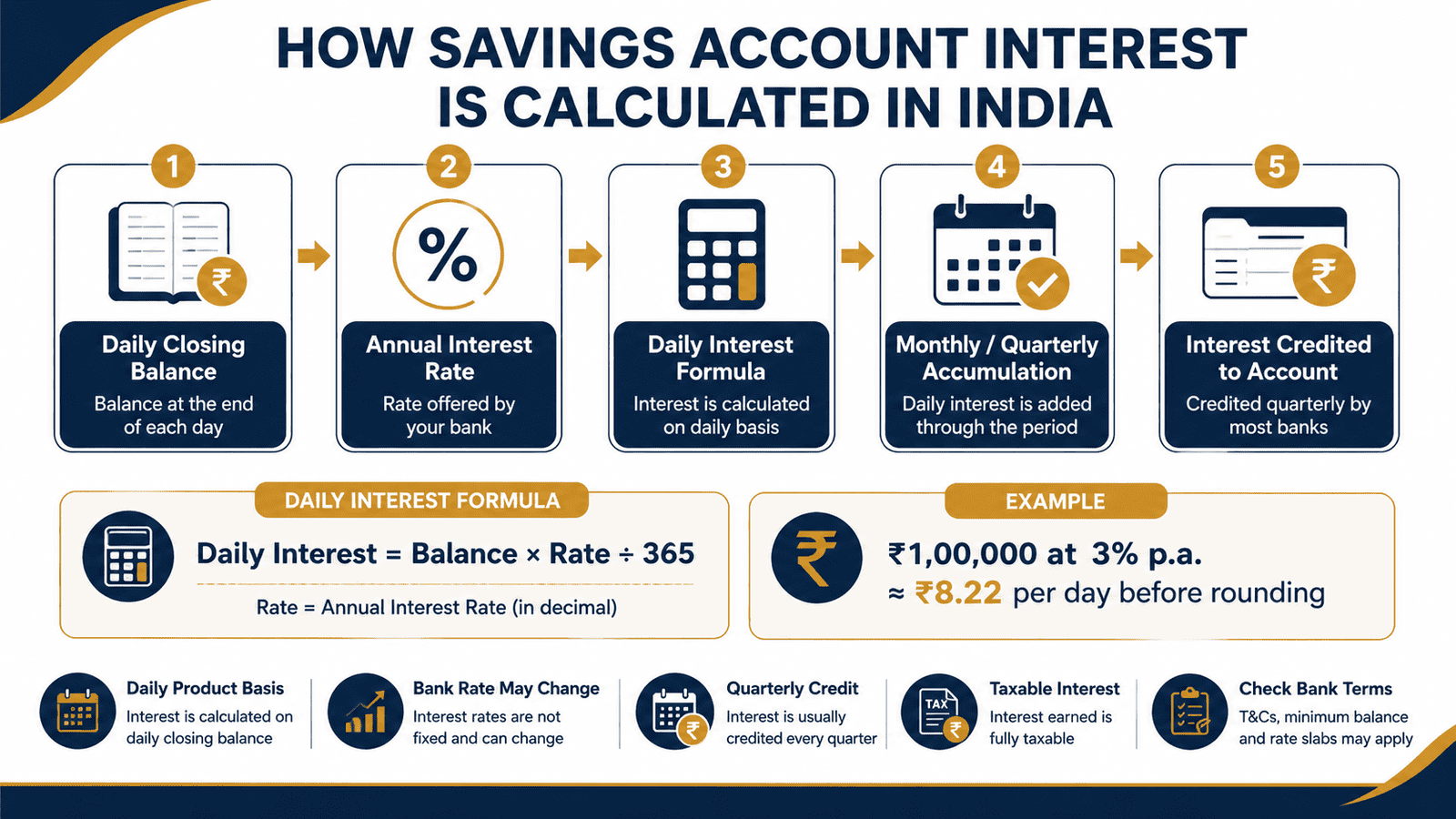

How Banks Calculate Savings Account Interest in India

What Is Savings Account Interest?

When you deposit money in a savings account, the bank pays you interest for keeping your money with them. That interest is not a reward for investing — it is compensation for the use of your funds. Savings account interest rates in India are generally much lower than fixed deposit rates, which is the trade-off for being able to withdraw your money at any time.

The Daily Balance Method Explained

According to RBI guidelines, banks in India have been required to calculate savings bank interest on a daily product basis since April 1, 2010. Before this, many banks used the minimum monthly balance to calculate interest — which meant that even one large withdrawal early in the month could wipe out interest for the entire month.

The daily product basis is far more straightforward. Every night, the bank records your closing balance. Your interest for that day is calculated using just that one number. If ₹80,000 sits in your account at the end of Monday, Monday’s interest is based on ₹80,000. If you deposit ₹20,000 on Tuesday evening and your closing balance becomes ₹1,00,000, Tuesday’s interest is based on ₹1,00,000. Each day stands on its own.

Why Your Balance Changes Daily — and Why That Matters

For a salaried person, the savings account is a working account. Salary credit, EMI debit, UPI payments, ATM withdrawals — the balance moves constantly. Each of these movements changes the daily closing balance, which in turn changes the daily interest earned. This is why two people with the same “average” mental sense of their balance can earn meaningfully different interest in the same quarter.

Understanding the difference between simple and compound interest is also useful here — savings account daily interest is calculated as simple interest on each day’s balance, not compounded daily. The accumulated daily simple interest is what gets credited at the end of the quarter.

Does Average Monthly Balance Affect Interest?

No — and this is one of the most common points of confusion. Average monthly balance (AMB) or minimum balance is a separate requirement that determines whether you are charged a non-maintenance fee. It has nothing to do with how interest is calculated. Interest is calculated purely on your daily closing balance, regardless of whether you maintain the AMB or not.

Interest Rate Slabs by Balance

Many banks offer different interest rates based on your account balance — for example, a lower rate on balances up to ₹1 lakh and a higher rate on balances above ₹1 lakh. These are called incremental balance slabs. Only the portion of your balance falling in each slab earns that slab’s rate. Verify your bank’s current rate slabs directly with the bank, as these rates change without advance notice.

Real Example: Rohan’s Quarterly Interest Calculation

Rohan, 29, a software engineer in Pune, earns ₹85,000 per month. He keeps around ₹1,00,000 in his savings account as a liquid buffer. Let’s say his bank offers 3% p.a. on balances up to ₹1 lakh — verify your actual rate with your bank before using this as a reference.

For the first 15 days of a month, his closing balance holds steady at ₹1,00,000. Daily interest = ₹1,00,000 × 3% ÷ 365 = approximately ₹8.22 per day. Over 15 days, that is roughly ₹123.29.

On day 16, Rohan pays a large insurance premium and his balance drops to ₹40,000. For the remaining 15 days of the month, daily interest = ₹40,000 × 3% ÷ 365 = approximately ₹3.29 per day. Over 15 days, that is roughly ₹49.32.

Total interest for the month: approximately ₹172.61 — not ₹246.60 that a flat ₹1,00,000 balance would have earned. This is why mid-month withdrawals reduce your quarterly interest credit more than people expect. Exact rounding and crediting methods may differ by bank.

How to Calculate Savings Account Interest Step by Step

Daily Interest = (Closing Balance × Annual Interest Rate) ÷ 365

Here is how to replicate the calculation yourself:

Step 1: Note your closing balance for each day of the quarter from your bank statement or passbook.

Step 2: For each day, multiply the closing balance by your applicable annual interest rate. Use the rate slab that applies to your balance — verify this directly from your bank’s website or schedule of charges.

Step 3: Divide that product by 365 to get the day’s interest amount.

Step 4: Add up all daily interest amounts from the start of the quarter to the crediting date. This total is your gross interest before any tax deduction at source, if applicable.

Step 5: Compare your manual calculation with the interest credit shown in your bank statement. Small differences arise from rounding methods used by the bank’s system.

| Scenario | Balance and Duration | Approximate Interest (at 3% p.a.) |

|---|---|---|

| Stable balance | ₹1,00,000 for 30 days | ~₹246.60 |

| Mid-month withdrawal | ₹1,00,000 for 15 days, ₹40,000 for 15 days | ~₹172.61 |

| Low balance quarter | ₹25,000 for 90 days | ~₹184.93 |

All figures above use an illustrative 3% p.a. rate. Verify your bank’s current rate before drawing any conclusions.

Savings Account vs FD vs RD vs Sweep-In FD

| Feature | Savings Account | Fixed Deposit / Recurring Deposit |

|---|---|---|

| Interest calculation | Daily closing balance | Fixed amount for fixed tenure |

| Typical rate (indicative) | Lower — verify current slab | Usually higher — varies by bank and tenure |

| Liquidity | Full — withdraw anytime | Penalty for early withdrawal |

| Deposit flexibility | Any amount, any time | Fixed at opening / monthly for RD |

| Tax on interest | Taxable; 80TTA / 80TTB deduction available | Taxable; TDS deducted if interest exceeds threshold |

| Best suited for | Salary, bills, EMIs, emergencies | Surplus funds with a defined time horizon |

| Sweep-in FD option | Available at select banks — surplus auto-converted to FD | FD rates apply on swept amount |

Use the FD interest calculator to see exactly how much a fixed deposit would return compared to keeping the same amount in a savings account. For a fuller understanding of how FDs work, see our guide on fixed deposit basics.

How to Decide What’s Right for You

You need the money for salary, monthly bills, UPI payments, and EMIs — THEN keep it in a savings account. Full liquidity is the point.

You are building an emergency fund of 3–6 months’ expenses — THEN a savings account works well for the portion you may need at very short notice. Use the emergency fund calculator to figure out how much that amount should be.

You have surplus money that will sit untouched for 6 months or more — THEN compare FD rates and terms. The interest difference over time can be meaningful.

You want savings account liquidity but FD-style returns on the surplus portion — THEN check whether your bank offers a sweep-in FD option, where balances above a threshold are automatically moved to an FD and swept back when needed.

Your savings account balance stays very low most of the month due to tight cash flow — THEN the interest earned will be minimal. Focus first on building a stable buffer before comparing yield options.

A savings account is not the right primary vehicle if your goal is long-term wealth building. Inflation can erode the real value of money sitting in a low-yield savings account year after year. In that case, compare alternatives suited to your time horizon and risk comfort.

Common Mistakes to Avoid

Assuming Interest Is Credited Monthly

Most banks credit savings account interest quarterly, not monthly. If you are expecting a monthly interest payout and planning your budget around it, you may be disappointed. Check your account terms or bank statement to confirm the crediting schedule for your specific account.

To avoid this: note the interest credit dates in your passbook and plan accordingly.

Confusing Minimum Balance with Daily Closing Balance

Minimum balance (AMB) is the floor your bank requires to avoid a non-maintenance fee. Interest is calculated on your daily closing balance — these are two entirely separate things. Maintaining AMB does not guarantee a higher interest credit.

To avoid this: track your daily balance movement for a quarter and cross-check with the interest credit.

Comparing the Highest Advertised Rate with Your Actual Balance Slab

Banks often advertise their highest slab rate — for example, 6% or 7% on balances above ₹10 lakh. If you keep ₹50,000, that rate does not apply to you. The lower slab rate does. This mismatch leads to very different interest from what was mentally expected.

To avoid this: check the specific rate slab applicable to your balance range directly from your bank’s schedule of charges — not just the headline rate.

Ignoring Tax on Savings Account Interest

Savings account interest is fully taxable under the head “Income from Other Sources.” Many salaried employees forget to include this in their ITR. If interest earned across all savings accounts exceeds the Section 80TTA deduction limit, the excess is taxable at your slab rate. Verify current limits at incometax.gov.in.

To avoid this: total up all savings account interest from your annual bank statement before filing your return.

Keeping Long-Term Surplus in a Savings Account

Leaving ₹3–4 lakh in a savings account for a year when you do not need that liquidity could mean significantly lower returns compared to a fixed deposit. The gap compounds over time. A sweep-in FD is one way to earn higher interest without sacrificing easy access.

To avoid this: review your savings account balance once a quarter and transfer genuinely idle funds to a suitable instrument.

Not Checking the Interest Credited in Your Statement

Many people never verify whether the interest credit in their statement matches what the daily balance formula should produce. Errors are rare but possible — especially if there were account disputes or system issues in the quarter.

To avoid this: do a rough manual check using the step-by-step method in Section 7 above whenever interest is credited.

When This May Not Be the Right Choice

Relying primarily on a savings account for returns may not suit every situation. If you are saving for a long-term goal — a house down payment in 5 years, retirement, or a child’s education — a savings account’s interest rate is unlikely to keep pace with inflation over time. The real value of money sitting in a low-yield account can erode meaningfully over a decade.

If you have a large surplus — say, ₹5 lakh or more — sitting idle in a savings account, the opportunity cost of not moving it to a higher-yield option can add up to thousands of rupees per year. Review fixed deposit basics as a starting point for comparison.

If your chosen bank’s savings rate is at the lower end of the spectrum and the bank also has thin DICGC cover awareness or unclear charges, it is worth comparing alternatives. And if you are primarily chasing the highest advertised savings rate without checking the slab conditions, charges, and track record of the bank, the actual net return can disappoint.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Savings account interest calculation rules, tax treatment, and bank-specific rates can all change — sometimes with little public notice. Before making any financial decision based on a rate or limit, verify directly from these official sources:

- RBI (rbi.org.in) — For the daily product basis rule, savings bank interest circulars, and banking regulation guidance.

- Income Tax Department (incometax.gov.in) — For current Section 80TTA and Section 80TTB deduction limits, taxability rules, and ITR filing guidance. Check the interest deduction rules on Ridhi for a plain-language summary, but always confirm limits from the official site before filing.

- Your bank’s official website — For the current interest rate slab applicable to your account type and balance, crediting frequency, minimum balance requirements, and any account-specific conditions.

- Your bank statement or passbook — The most reliable record of actual interest credited to your account each quarter.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Check the rate slab that applies to your actual balance — not the headline rate the bank advertises. If your balance is typically ₹50,000–₹80,000, find the rate for that range specifically in your bank’s schedule of charges.

- Review your quarterly interest credit in your bank statement and do a rough back-of-envelope check using the formula. If the numbers look very off, raise a query with your bank before the next quarter closes.

- If your savings account balance consistently stays above ₹1 lakh after expenses, ask your bank about a sweep-in FD facility — surplus amount above a threshold earns FD-linked rates and is swept back automatically when you need it.

- When calculating your actual net return on a savings account, factor in the tax cost. If you are in the 30% tax bracket and your total savings interest across accounts exceeds the 80TTA limit, your effective post-tax return is lower than the headline rate.

- Check DICGC deposit insurance coverage if you are keeping large balances at smaller banks. Verify current insured amount limits at rbi.org.in — this is a basic safety check that most people skip.

- Set a quarterly reminder to review your savings account balance. The goal is not to micro-manage every rupee, but to spot genuinely idle surplus that could be better deployed elsewhere with minimal effort.

Frequently Asked Questions

How is savings account interest calculated in India?

Banks in India calculate savings account interest using the daily balance method (daily product basis), as mandated by RBI guidelines effective April 1, 2010. Your interest for each day equals your closing balance that day multiplied by the annual rate, divided by 365. Daily interest amounts are accumulated and typically credited at the end of each quarter.

Is savings account interest calculated daily or monthly?

It is calculated daily — based on each day’s closing balance. However, most banks credit the accumulated interest to your account quarterly, not every day or every month. The daily calculation means frequent withdrawals reduce your interest for those specific days.

When is savings account interest credited?

Most banks credit savings account interest quarterly — commonly at the end of March, June, September, and December. However, crediting schedules can vary by bank and account type. Check your bank’s terms or look at the “interest credit” entries in your bank statement to confirm the schedule for your account.

Is savings account interest taxable?

Yes, savings account interest is fully taxable under “Income from Other Sources.” Individuals (other than senior citizens) can claim a deduction of up to ₹10,000 per year under Section 80TTA on savings account interest. Senior citizens can claim a higher deduction under Section 80TTB — verify current limits at incometax.gov.in before filing your ITR.

Is savings account interest better than FD interest?

Generally, fixed deposit interest rates are higher than savings account rates for equivalent amounts and time periods. The trade-off is liquidity — savings accounts allow unlimited withdrawals while FDs have a fixed tenure and premature withdrawal penalties. For short-term liquid money, savings accounts make sense. For surplus funds parked for a defined period, FDs usually offer better returns — but compare actual current rates from your bank before deciding.

What is the daily product basis for savings account interest?

Daily product basis is the RBI-mandated method for calculating savings account interest. “Product” here means the product of your daily closing balance and the annual interest rate. Each day’s product is divided by 365 to get that day’s interest. All daily interest amounts are added up over the quarter and credited to your account. This method is fairer than the old minimum monthly balance method because every rupee in your account earns interest for every day it is there.

Can I calculate my own savings account interest?

Yes. Note your closing balance for each day of the quarter from your passbook or statement. Multiply each day’s balance by your annual rate and divide by 365 to get that day’s interest. Add all daily interest amounts. The total should be close to what your bank credits — small differences come from rounding. If the difference is large, contact your bank.

What is Section 80TTA and does it apply to my savings account?

Section 80TTA of the Income Tax Act allows individuals and Hindu Undivided Families (HUFs) to claim a deduction of up to ₹10,000 per year on interest earned from savings accounts held with banks, co-operative banks, or post offices. This deduction is not available on FD interest. Senior citizens use Section 80TTB instead, which covers a broader range of interest income. Verify current limits and eligibility at incometax.gov.in.

What happens if my savings account balance is zero for a few days?

You earn zero interest for those days — since the daily interest formula multiplies your closing balance by the rate. A zero balance means a zero product and therefore zero interest for that day. This does not affect the rest of the quarter’s interest calculation — only those specific days are missed.

Do all banks in India use the same savings account interest rate?

No. Since October 2011, RBI deregulated savings account interest rates, allowing each bank to set its own rate. Rates vary significantly across public sector banks, private banks, small finance banks, and payments banks. Some banks offer higher rates for higher balance slabs. Always check your specific bank’s current rate schedule — do not assume a rate you saw in an advertisement applies to your balance.

Final Verdict

Savings account interest calculation is simple once you understand the daily balance formula. Your interest for each day depends entirely on your closing balance that night — frequent withdrawals, mid-month transfers, and low-balance periods all reduce what you earn by the end of the quarter.

For most salaried earners, a savings account is the right place for salary, monthly expenses, EMI buffers, and emergency access money. It is not, however, an efficient tool for long-term surplus. If your account consistently holds more than 3–6 months of expenses without touching, it is worth comparing what an FD, RD, or sweep-in arrangement would return on that surplus — keeping in mind that rates, slabs, and tax rules all vary and can change.

The savings account interest calculation comes down to one formula, one daily habit of your balance, and one quarterly credit. Understand those three, and the number on your statement will never surprise you again.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Meera Iyer writes about banking, fixed deposits, recurring deposits, savings accounts, emergency funds, senior citizen deposits, and safe cash management for Indian readers. Her work is especially useful for families, retirees, conservative savers, and beginners who want to understand where to keep short-term or low-risk money.

She covers topics such as FD meaning, FD calculator, RD calculator, FD vs RD, simple interest vs compound interest, savings account interest, sweep-in FD, premature FD withdrawal, senior citizen FD rules, TDS on FD interest, Form 15G, Form 15H, joint account rules, zero balance accounts, minimum balance charges, small finance bank FDs, post office FD vs bank FD, and emergency fund planning.

Meera’s content focuses on safety, liquidity, taxation, and practical decision-making. She avoids hype and explains both benefits and limitations of banking products. Since deposit interest rates, TDS rules, penalty charges, DICGC coverage, and bank policies can change, readers should always confirm the latest details from their bank, RBI, DICGC, India Post, or relevant official sources before making decisions.