Your ₹1 lakh monthly salary is a strong starting point for a home loan — but how much you can actually borrow depends on far more than the number on your payslip. Banks and NBFCs look at your FOIR (fixed obligation to income ratio), existing EMIs, CIBIL score, age, employer profile, and the market value of the property you want to buy before sanctioning a single rupee. One lender may approve ₹42 lakh; another may offer ₹55 lakh — based on the same salary, because their internal policies differ. More importantly, what a bank is willing to lend and what you should comfortably borrow are two very different numbers. This article breaks down the home loan on 1 lakh salary calculation step by step — so you can estimate your eligibility realistically and decide how much makes genuine financial sense before you shortlist a property.

Quick Answer: Home Loan on 1 Lakh Salary

For home loan on 1 lakh salary, many lenders may allow about ₹40,000–₹45,000 EMI and roughly ₹40–50 lakh loan for a 20-year tenure at current rates. Final eligibility depends on age, CIBIL score, existing EMIs, property value, employer profile, and lender policy.

How to Calculate Your Home Loan Eligibility on ₹1 Lakh Salary

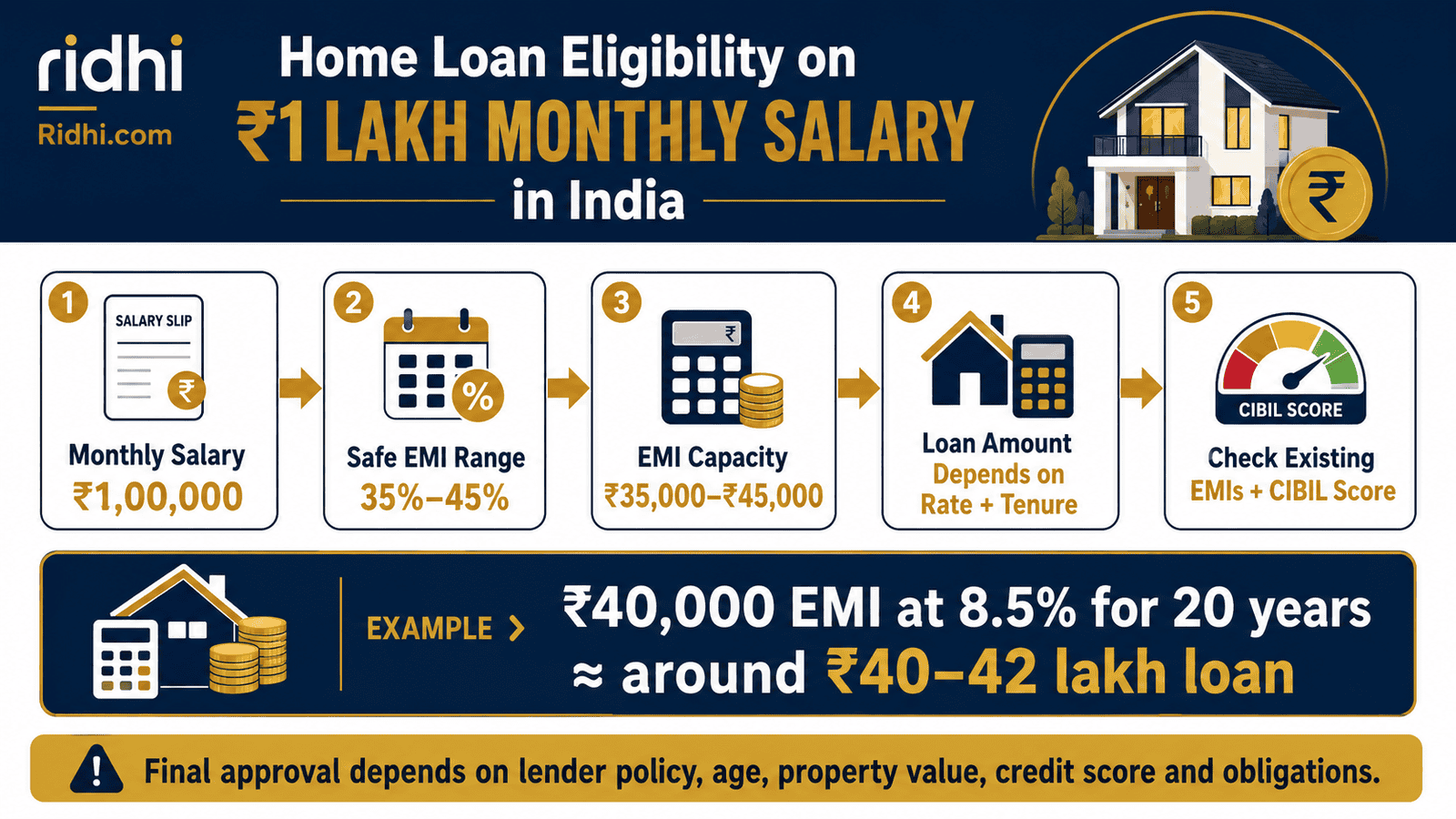

Banks do not start with a loan amount — they start with your EMI capacity and work backwards. Here is the step-by-step path from salary to loan estimate.

Step 1: Confirm your net monthly income. Most lenders assess your in-hand (net) salary, not your CTC. If your gross salary is ₹1,00,000 but in-hand is ₹82,000 after PF and professional tax, the bank uses ₹82,000 for FOIR calculations. For this article, we assume a net in-hand salary of ₹1,00,000.

Step 2: Apply the FOIR range. Lenders typically permit 40%–50% of net monthly income as total EMI. At ₹1,00,000 net, that means ₹40,000–₹50,000 in total EMIs — but a safer planning range is 35%–45%, leaving room for living costs, savings, and unexpected expenses.

Step 3: Deduct existing EMIs. If you already pay ₹10,000 per month on a car loan, your available EMI for the home loan drops to ₹30,000–₹35,000. This directly reduces your eligible loan amount.

Step 4: Use the EMI formula to reverse-engineer the loan.

Loan Amount = EMI × [(1 + r)^n − 1] ÷ [r × (1 + r)^n]

where r = monthly interest rate (annual rate ÷ 12 ÷ 100) and n = loan tenure in months

Step 5: Compare three EMI scenarios. Using an indicative rate of 8.5% per annum and a 20-year tenure, here is how different EMI levels translate to loan amounts. Use the Check your EMI first tool to run the actual numbers for your rate and tenure.

| Monthly EMI | Estimated Loan Amount (20 yr, 8.5% p.a.) | Total Interest Paid |

|---|---|---|

| ₹35,000 | ~₹40 lakh | ~₹44 lakh |

| ₹40,000 | ~₹46 lakh | ~₹50 lakh |

| ₹45,000 | ~₹52 lakh | ~₹56 lakh |

Notice that for a ₹46 lakh loan at ₹40,000 EMI, you end up paying ₹96 lakh in total over 20 years — ₹50 lakh of which is interest alone. The EMI is just one number. The total cost is the number that matters.

Key Takeaways

- A ₹1 lakh monthly in-hand salary typically supports an EMI of ₹35,000–₹45,000, translating to an indicative home loan of approximately ₹40–52 lakh at a 20-year tenure.

- Every ₹5,000 of existing EMI you already pay reduces your available home loan eligibility by approximately ₹5.8–6 lakh — existing debts cost you more than most borrowers realise.

- A CIBIL score below 700 can either block approval or push your interest rate higher by 0.5%–1%, which meaningfully increases total interest across a 20-year tenure.

- Extending tenure from 20 years to 25 years can increase your eligible loan by roughly ₹8–10 lakh — but adds five more years of interest, significantly raising your total repayment cost.

- Banks use your net in-hand salary for FOIR, not your CTC — verify your net figure before assuming eligibility.

- Lender-approved maximum and your personal safe borrowing limit are not the same number; always plan for EMI increases if you are on a floating rate.

Key Facts at a Glance

| Parameter | Value / Assumption | Notes |

|---|---|---|

| Monthly Salary (Net) | ₹1,00,000 | In-hand after PF, tax, deductions |

| Indicative EMI Capacity | ₹35,000–₹45,000 | 35–45% FOIR; varies by lender |

| Estimated Loan Range | ₹40–52 lakh | At 8.5% p.a. for 20 years |

| Minimum CIBIL Score | 700–750+ | Best rates typically at 750+ |

| Maximum Tenure | Up to 30 years | Subject to retirement age cap |

| Loan-to-Value Ratio | 75%–90% of property value | Varies with loan amount per RBI norms |

How Banks Decide Your Home Loan Eligibility

FOIR: The Number Banks Use First

FOIR — Fixed Obligation to Income Ratio — is the single most important variable in home loan eligibility calculations. It measures how much of your monthly income is already committed to debt repayments. If your net salary is ₹1,00,000 and your car loan EMI is ₹12,000, your FOIR before any home loan is already 12%. A lender permitting a maximum FOIR of 50% will only allow ₹38,000 more in home loan EMI, not ₹50,000.

FOIR limits vary by lender — some private banks cap it at 40%, others go up to 55% for higher-income applicants. There is no universal RBI rule mandating a specific FOIR ceiling; it is a lender-defined internal policy. Understanding what your target lender uses is critical before assuming your eligibility. To understand how this ratio affects borrowing safety, read our guide on safe EMI for salary.

Gross Salary, Net Salary, and What Lenders Actually Use

Many borrowers assume banks will consider their CTC for eligibility. Most do not. Lenders typically work with your net monthly in-hand salary — after PF deductions, professional tax, and income tax TDS. If your CTC is ₹15 lakh per annum but your in-hand is ₹1,00,000 per month, the ₹1,00,000 figure is what gets plugged into the FOIR formula. This distinction can reduce your perceived eligibility significantly if you assumed otherwise.

Why Your CIBIL Score Changes Your Eligible Amount

A high CIBIL score does not increase your loan amount directly — but it affects your interest rate. A borrower with a score of 800 may get 8.5% while a borrower with 680 gets 9.25% from the same bank. That 0.75% difference on a ₹46 lakh loan over 20 years translates to approximately ₹4–5 lakh in additional total interest. A strong credit history also improves your negotiating position on processing fees and prepayment terms. For a full explanation of how scores are calculated, see our article on credit score meaning.

How Existing EMIs Shrink Your Home Loan

This is the most underestimated factor. Consider two borrowers, both earning ₹1,00,000 net: Borrower A has no existing EMIs. Borrower B has a car loan at ₹10,000 and a personal loan at ₹8,000, totalling ₹18,000 per month. If the lender allows a 45% FOIR, Borrower A can service ₹45,000 in home loan EMI, Borrower B only ₹27,000. At 8.5% for 20 years, Borrower A qualifies for ~₹52 lakh; Borrower B for only ~₹31 lakh. The salary is identical. The existing debt makes all the difference.

Property Value and the LTV Cap

Even if your income supports a higher EMI, the bank cannot lend more than the loan-to-value limit on the property. According to RBI guidelines, for home loans between ₹30 lakh and ₹75 lakh, the LTV ratio is capped at 80% of the property’s market value. For loans above ₹75 lakh, it drops to 75%. This means for a property valued at ₹60 lakh, the maximum loan is ₹48 lakh regardless of your income — you must arrange the remaining ₹12 lakh as down payment.

Real Example: Rohit’s Home Loan Estimate in Pune

Rohit, 32, is a senior software engineer in Pune earning ₹1,00,000 per month in-hand. He is looking at a 2BHK priced at ₹65 lakh and wants to understand how much the bank will actually lend him.

Scenario A — No existing EMIs: Rohit has no car loan or personal loan. His lender permits a FOIR of 45%, making ₹45,000 available for home loan EMI. At an indicative rate of 8.5% for 20 years, this translates to a loan of approximately ₹52 lakh. The property is valued at ₹65 lakh; 80% LTV gives a maximum of ₹52 lakh — which aligns. Rohit needs ₹13 lakh as down payment plus stamp duty and registration.

Scenario B — Existing ₹12,000 car EMI: Rohit’s FOIR budget is still ₹45,000 total, but ₹12,000 is already consumed by his car loan. Only ₹33,000 is available for the home loan EMI, reducing his eligible loan amount to approximately ₹38 lakh at the same rate and tenure. Same salary. Same bank. ₹14 lakh less in loan amount — because of one existing obligation.

The key insight: clear or reduce existing EMIs before applying for a home loan. The impact on eligibility is immediate and substantial.

Comparison: Home Loan Eligibility Across EMI Scenarios

If you are near the ₹75,000–₹1 lakh salary band, compare your options — see our detailed guide on ₹75,000 salary eligibility to understand how an income step-up changes borrowing power.

| Scenario | Monthly EMI / Est. Loan (20 yr, 8.5%) | Risk Level |

|---|---|---|

| Conservative — No existing debt, 35% FOIR | ₹35,000 EMI / ~₹40 lakh loan — Total repayment: ~₹84 lakh | Low |

| Moderate — No existing debt, 40% FOIR | ₹40,000 EMI / ~₹46 lakh loan — Total repayment: ~₹96 lakh | Medium |

| Stretched — No existing debt, 45% FOIR | ₹45,000 EMI / ~₹52 lakh loan — Total repayment: ~₹1.08 crore | High |

These are indicative estimates at an assumed 8.5% rate. Your actual rate, lender FOIR policy, and existing obligations will move these numbers. The total repayment column is the number that deserves the most attention — not the EMI.

How to Decide What’s Right for You

You have no existing EMIs and a CIBIL score above 750 — a moderate EMI of ₹38,000–₹42,000 is likely your most balanced starting point, giving you eligibility of ₹44–48 lakh without stretching your monthly budget dangerously thin.

You already pay ₹10,000 or more per month in EMIs — calculate your home loan eligibility after deducting those obligations from your FOIR budget. Do not assume full ₹40–45K EMI availability.

You are on a floating rate home loan — keep your EMI at least 5%–10% below your theoretical maximum so a rate increase of 0.5%–1% does not immediately stress your budget.

Your target property requires a loan above ₹50 lakh — confirm the LTV cap with your lender and ensure you have the full down payment including stamp duty and registration, which together can add 6%–8% of property value in most cities.

You are considering adding a co-applicant — their income can increase combined eligibility, but only if they have a clean credit profile and stable income. A co-applicant with existing debt or poor CIBIL can reduce your chances of approval.

You do not have an emergency fund of at least 3–6 months of expenses — do not stretch to your maximum EMI limit. A job disruption with no buffer and a high EMI is a recipe for default and long-term credit damage.

Common Mistakes to Avoid

Assuming ₹1 Lakh Salary Automatically Guarantees a Large Loan

Salary is one input, not the whole picture. Banks also weigh your employer’s credit rating, employment type (salaried vs self-employed), job stability, and sector. A ₹1 lakh salary from a PSU employee and a ₹1 lakh salary from a startup with irregular payroll are viewed very differently by lenders.

Get a pre-qualification estimate from your target lender before shortlisting a property.

Forgetting to Subtract Existing EMIs from Your FOIR Budget

A car loan of ₹12,000/month and a personal loan of ₹8,000/month together consume ₹20,000 of your FOIR budget. At 45% FOIR, only ₹25,000 remains for home loan EMI — which qualifies you for roughly ₹29 lakh, not ₹52 lakh. Ignoring this gap can derail your property search entirely.

List every current EMI before calculating home loan eligibility.

Choosing the Longest Tenure Only to Inflate the Loan Amount

Stretching from 20 to 30 years increases your eligible loan amount by roughly ₹10–15 lakh — but also dramatically increases total interest paid. A ₹46 lakh loan at 8.5% over 30 years costs approximately ₹77 lakh in interest alone, versus ₹50 lakh over 20 years. That is ₹27 lakh of additional cost in exchange for a lower monthly EMI.

Use tenure extension as a last resort, not a first strategy.

Ignoring Down Payment, Stamp Duty, and Registration Costs

Banks finance 75%–80% of property value for loans in the ₹30–75 lakh range. For a ₹60 lakh property, you need at least ₹12 lakh as down payment — plus stamp duty (4%–6% in most states) and registration fees (1%–2%), which together can add ₹3–4 lakh or more. Many buyers are caught off-guard by this upfront requirement.

Budget for the full upfront cost, not just the loan portion.

Comparing Only EMI Instead of Total Interest

A ₹40,000 EMI sounds manageable — until you realise it means ₹96 lakh repaid over 20 years on a ₹46 lakh loan. Always ask for the total repayment figure, not just the monthly EMI, before committing.

Request a complete amortisation schedule from your lender before signing.

Applying to Multiple Lenders Without Checking Credit Inquiry Impact

Every hard credit inquiry by a lender temporarily reduces your CIBIL score. Applying to five banks simultaneously can lower your score by 20–30 points in a short period, which may affect your rate or approval prospects. Use soft-check eligibility tools first.

Use aggregator eligibility checks that do not trigger hard inquiries before finalising your lender.

When This May Not Be the Right Choice

A ₹1 lakh salary supports a meaningful home loan, but not in every situation. Consider these risk signals before committing:

If your income is variable — commission-based, contractual, or from a startup with uncertain funding — a 20-year fixed obligation is a significant risk. Lenders may also reduce eligible amounts for variable income profiles.

If your combined existing EMIs already consume 30%–35% of your income, adding a home loan EMI will push your FOIR close to or beyond safe limits, leaving very little room for savings, insurance, or emergencies.

If you have not built a basic emergency fund of at least 3 months’ expenses, a home loan commitment at maximum eligibility creates serious vulnerability to any income disruption.

If you are buying primarily because of social pressure or because “property prices will rise,” rather than because the purchase fits your income, timeline, and family plan — it is worth re-evaluating the timing.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Home loan eligibility rules, interest rate structures, FOIR limits, LTV ratios, and processing norms are set by individual lenders within the regulatory framework provided by the Reserve Bank of India. They change with monetary policy, credit cycles, and internal bank policy reviews.

Always verify current rates and terms directly from these official sources before making any financial decision:

- Reserve Bank of India — rbi.org.in (lending norms, LTV guidelines, consumer protection rules)

- Your target bank or NBFC’s official website — for their current home loan rates, FOIR policy, and eligibility calculator

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Once you understand your eligibility, the next step is the application process itself — our detailed guide on the home loan process covers every stage from documentation to possession.

Expert Tips

- Check your CIBIL score 3–6 months before applying. If it is below 750, pay down credit card balances and avoid new loan applications in that window. Even a 30-point improvement can move you into a lower rate bracket, saving thousands in total interest.

- Pay off one high-EMI loan before applying. If you have a personal loan at ₹10,000/month with only 8 months remaining, clearing it before your home loan application may increase your eligible loan amount by ₹11–12 lakh.

- Get a pre-sanction letter before finalising a property. Pre-sanction gives you a negotiating position with the seller and prevents you from committing to a property above your actual eligible range.

- Compare total interest, processing fees, and prepayment terms — not just EMI. A bank offering 8.3% with a 2% prepayment penalty may cost more over 20 years than one offering 8.6% with free prepayment if you plan to make partial payments.

- Understand that tax deductions reduce your net borrowing cost — but do not let that drive your loan size decision. The Section 24(b) deduction of up to ₹2 lakh per year on home loan interest is useful, but it does not make a financially stretched loan manageable. Read our complete breakdown of home loan tax benefit to understand what you can legitimately claim.

- Plan for a floating rate increase of at least 1%–1.5%. If your current EMI at 8.5% is ₹40,000, calculate whether you can still service the loan if the rate moves to 9.5% — which would push the EMI on a ₹46 lakh, 20-year loan to approximately ₹43,800.

Frequently Asked Questions

How much home loan can I get on ₹1 lakh salary?

With no existing EMIs, a clean credit profile, and a CIBIL score above 750, most banks may offer a home loan in the range of ₹40–52 lakh at a 20-year tenure. The exact amount depends on the lender’s FOIR policy, the interest rate applicable to your profile, and the property’s market value. These are indicative estimates — not approval guarantees.

Is ₹40,000 EMI safe on a ₹1 lakh salary?

₹40,000 EMI represents 40% of ₹1 lakh — which is within the FOIR range most lenders permit. Whether it is safe for you depends on your monthly expenses, rent (if applicable), insurance premiums, investments, and whether you have other loan obligations. If ₹40,000 EMI leaves you less than ₹20,000–₹25,000 for all other expenses, it is likely too stretched.

Does CIBIL score affect how much home loan I can get on ₹1 lakh salary?

CIBIL score directly affects your interest rate, not the loan amount formula — but since a higher rate means a higher EMI for the same loan, a low CIBIL score effectively reduces how much you can borrow within your EMI budget. A score below 700 may also result in outright rejection from several lenders. For a full explanation, see our guide on credit score meaning.

Can I get a higher home loan with a co-applicant on ₹1 lakh salary?

Yes — adding a financially eligible co-applicant (typically a spouse or parent with stable income) allows the lender to club both incomes for FOIR calculation, which can significantly increase the eligible loan amount. However, the co-applicant’s CIBIL score and existing EMIs are also considered. A co-applicant with poor credit can reduce, not increase, your approval prospects.

Should I take the maximum home loan the bank offers on ₹1 lakh salary?

Not necessarily. The bank’s maximum is based on income and credit rules — it does not account for your rent, school fees, medical costs, investment goals, or lifestyle expenses. Borrowing the maximum leaves no buffer for interest rate increases, job changes, or emergencies. A practical approach: borrow what makes the EMI comfortable at 1%–1.5% above the current rate, not at today’s rate alone.

Does the bank use gross salary or net salary for home loan eligibility?

Most lenders use your net in-hand salary — the amount credited to your bank account after PF, professional tax, and TDS. Some lenders also consider gross salary for higher-income applicants with clean repayment histories, but this varies. Always clarify with your lender which figure they apply before estimating eligibility yourself.

What happens if I have existing EMIs when applying for a home loan on ₹1 lakh salary?

Existing EMIs directly reduce your available FOIR budget for the home loan. For example, if your lender allows 45% FOIR and you already pay ₹15,000 in existing EMIs, only ₹30,000 remains for the home loan EMI. At 8.5% for 20 years, ₹30,000 EMI supports a loan of approximately ₹34.5 lakh — substantially less than the ₹52 lakh that would be available with no existing debt.

Can I get a home loan on ₹1 lakh salary without a CIBIL score?

A limited number of lenders offer home loans to applicants with no credit history (NTC — new to credit), but the terms are typically less favourable and the loan amount may be lower. Most mainstream banks and leading NBFCs require an established credit history. Building a credit history through a credit card used responsibly for 12–18 months before applying is a practical first step.

Is ₹50 lakh home loan possible on ₹1 lakh salary?

Possibly — but only if you have no significant existing EMIs, a CIBIL score of 750+, a stable employer profile, and the property’s market value supports an LTV-based loan of ₹50 lakh or more. At 8.5% for 20 years, ₹50 lakh requires an EMI of approximately ₹43,400 — which is 43.4% of ₹1 lakh net salary and within the range some lenders permit, though it leaves limited buffer.

What is the minimum CIBIL score to get a home loan on ₹1 lakh salary?

Most banks and NBFCs prefer a CIBIL score of 700 or above to process a home loan application. Scores of 750 and above generally qualify for the most competitive interest rates. Applicants with scores between 650–699 may find fewer lenders willing to approve, and those who do will typically charge a higher rate. Scores below 650 make home loan approval significantly more difficult.

Final Verdict

A home loan on 1 lakh salary is realistic — but the right amount depends entirely on your existing obligations, CIBIL score, lender’s FOIR policy, and the property’s value, not just your salary figure. Most borrowers with clean credit and no significant EMIs can expect a loan range of ₹40–52 lakh for a 20-year tenure. The more important question is not how much the bank will approve, but how much you can comfortably repay given your total monthly expenses — and whether the total interest cost over 20 years fits your long-term financial plan. Use the EMI calculator before shortlisting a property, compare total repayment across tenures, and keep your EMI within a buffer below your maximum eligibility. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Vikram Sethi writes about loans, EMI planning, credit score impact, borrowing costs, and repayment decisions for Indian borrowers. His content helps readers look beyond the monthly EMI and understand the full cost of borrowing, including principal, interest, processing fees, GST, insurance, prepayment charges, foreclosure fees, late payment penalties, and credit score impact.

He covers topics such as EMI calculators, home loan eligibility, personal loan eligibility, debt-to-income ratio, flat interest rate vs reducing balance, missed EMI consequences, loan prepayment vs part payment, home loan balance transfer, processing fees, gold loan vs personal loan, car loan vs cash purchase, top-up home loans, loan against PPF, and credit score basics.

Vikram’s writing style is practical, cautionary, and calculation-driven. He uses Indian examples, ₹ amounts, comparison tables, and decision frameworks to help borrowers compare options more carefully. His articles are educational and do not guarantee loan approval, interest rates, or savings. Readers should verify current rates, charges, eligibility, and terms directly with lenders before applying or refinancing.