Getting rejected for a credit card because of a low CIBIL score or no credit history is more common than most people realise. If you are a salaried employee who has never taken a loan or used a credit card before, your CIBIL profile may be too thin for banks to approve a regular card — even with a steady income. A secured credit card solves this problem directly: you park a fixed deposit with the bank, and the bank issues a card against that deposit. It is a real Visa or Mastercard credit card, not a prepaid card. Every transaction and payment is reported to credit bureaus. Used correctly, it is one of the most reliable tools available to build or rebuild your CIBIL score from scratch.

Quick Answer: Secured Credit Cards for Low CIBIL Score

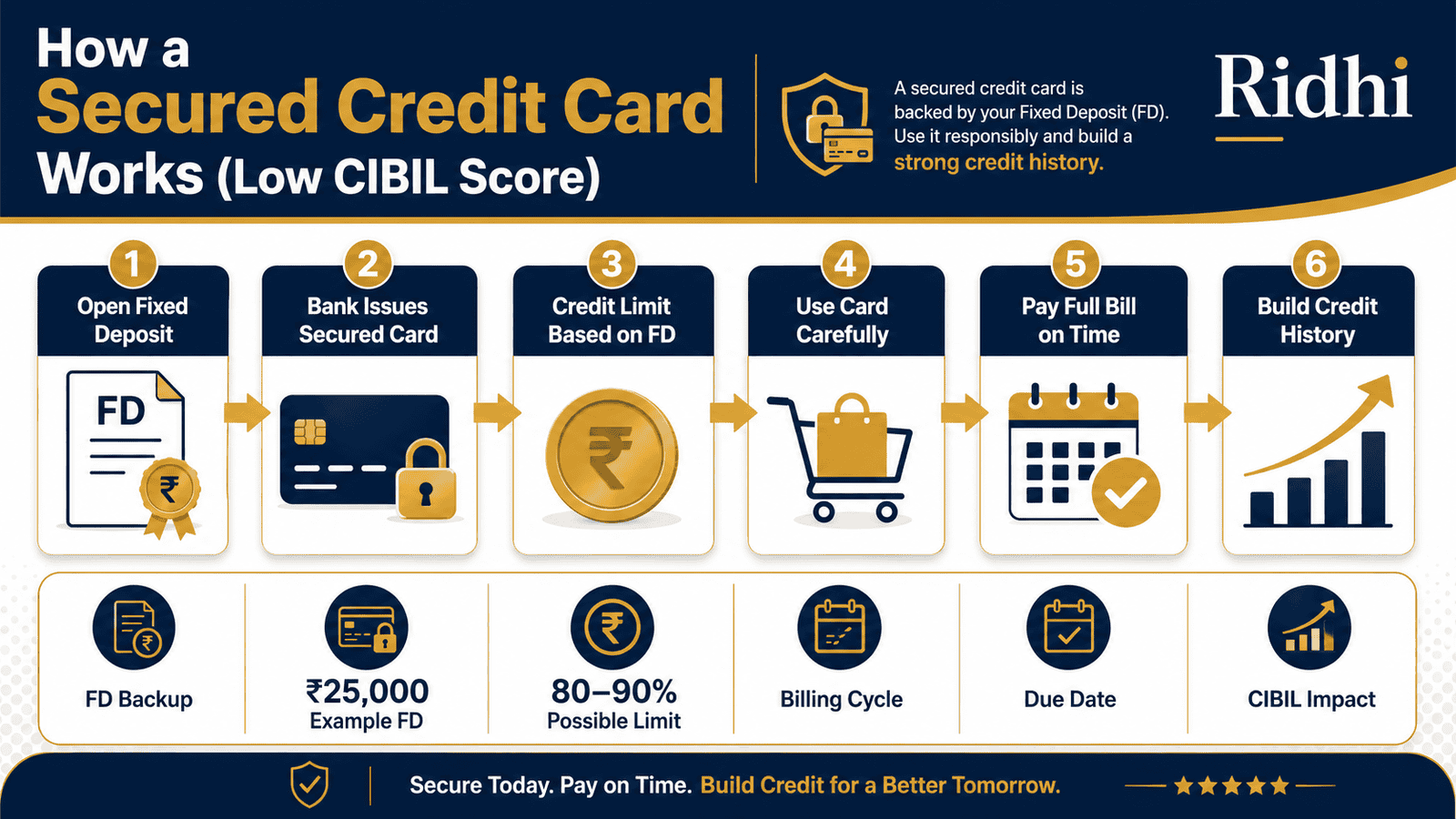

A secured credit card is a credit card issued against a fixed deposit, usually for people with low CIBIL score, no credit history, or limited income proof. For example, a ₹25,000 FD may give a card limit based on the bank’s policy, while timely full payments can help build credit history.

Key Takeaways

- A secured credit card requires a fixed deposit as collateral — the bank marks a lien on it and issues a credit card in return.

- Your credit limit is set as a percentage of your FD amount, as per the issuing bank’s policy — and can vary significantly across banks.

- All payments and balances are reported to TransUnion CIBIL and other credit bureaus, exactly like a regular credit card.

- Paying the full outstanding amount before the due date every month is what builds your score — paying only the minimum amount keeps your utilisation high and slows score recovery.

- Keeping your monthly card spend below 30% of your credit limit — for example, under ₹6,000 on a ₹20,000-limit card — signals financial discipline to credit bureaus.

- If you miss payments and default, the bank can recover the outstanding amount directly from your pledged FD — and your CIBIL score will fall further.

- With 12–18 months of consistent on-time full payments, many issuers upgrade the card to an unsecured product and release the FD lien.

Key Facts at a Glance

| Feature | Detail |

|---|---|

| Collateral required | Fixed deposit with issuing bank |

| Credit limit basis | Percentage of FD — as per bank’s policy |

| Income proof | Generally not required for FD-backed cards |

| CIBIL score required | Low or no CIBIL accepted by most issuers |

| Bureau reporting | Yes — identical to regular credit cards |

| FD interest during lien | Continues to earn at agreed rate |

| Card network | Visa or Mastercard (accepted globally) |

| Default recovery | Bank deducts from pledged FD |

| Upgrade path | Unsecured card possible after 12–18 months of good usage |

How a Secured Credit Card Works in India

When a bank issues a secured credit card, it places a lien on your fixed deposit. A lien is a legal freeze — the FD is held as collateral and you cannot withdraw or break it while the card is active. The FD continues to earn interest at the rate you locked in, but the principal is inaccessible for the duration of the lien.

The bank then issues a credit card on a Visa or Mastercard network, with a credit limit set as a percentage of your FD value. This percentage and the minimum FD required vary by bank and product — always check the card’s Key Facts Statement (KFS) before applying.

Why Banks Approve Secured Cards for Low CIBIL Profiles

A regular credit card is an unsecured loan — the bank takes on all the default risk. That is why lenders check your good CIBIL score and employment details carefully before approving one.

With a secured card, the risk equation flips entirely. The bank already holds your money. If you stop paying, it simply recovers the outstanding amount from your FD. This is why secured cards are accessible to people with a low score, a thin file (zero credit history), or those who cannot show formal income proof — freelancers, homemakers, students, and new employees still in their probation period.

How Credit Bureau Reporting Works on a Secured Card

This is the detail most beginners misunderstand. A secured credit card is not a prepaid card or a debit card. Every transaction, every payment made or missed, is reported to TransUnion CIBIL and other credit bureaus — in exactly the same format as a regular credit card.

When you pay your full outstanding balance before the due date each month, the bureau records it as an on-time full payment. Over 12–18 months of consistent behaviour, this creates a positive credit history. Your CIBIL score climbs. Banks issuing regular unsecured cards begin viewing you as creditworthy.

If you pay only the minimum amount due and carry a balance forward, the bureau still records a payment — but your credit utilisation stays elevated and your score builds slowly. Miss a payment entirely, and the bureau marks a default. Your score drops, and the bank can begin recovery proceedings against your FD.

FD Lien: What It Restricts in Practice

Once the bank marks a lien, you cannot:

- Withdraw the FD prematurely

- Pledge the same FD as collateral for any other loan

- Renew the FD independently without the bank’s involvement

You can still earn FD interest. The interest will be credited to your linked savings account at the scheduled intervals. But the principal is locked for as long as the card is active and the lien is in place.

When you close the card — either by upgrading to an unsecured product or by cancelling — the bank removes the lien. Your FD principal, plus all interest earned during the lien period, becomes fully accessible.

How This Appears on Your CIBIL Report

Your CIBIL report shows the secured card as a credit card account — not a secured loan account. The credit limit, outstanding balance, payment history, and DPD (Days Past Due) record all appear exactly as they would for any unsecured credit card. A lender reviewing your profile cannot tell from the CIBIL report alone whether the card was secured or unsecured. What they evaluate is your payment behaviour and utilisation pattern.

Interest Rate and Annual Fee

Secured cards are not free to use. Most carry an annual fee, and the interest rate on unpaid balances is comparable to regular credit cards — as of recent data, card interest rates in India typically range from 3% to 3.5% per month (annualised at 36%–42%). The FD collateral does not reduce your interest cost. It only makes you eligible for the card in the first place. Paying the full outstanding amount every billing cycle is the only way to avoid interest charges entirely.

Real Example: Rohit’s FD-Backed Card Journey in Pune

Rohit, 27, works as a customer support executive in Pune and earns ₹38,000 per month. He applied for a standard credit card at his bank but was rejected — he had never taken a loan or used a credit card, which left him with a thin CIBIL profile. His bank representative suggested an FD-backed secured card instead.

Rohit placed a ₹25,000 FD with the bank. The bank issued a secured credit card with a credit limit set according to their internal policy. He decided to use the card only for his monthly mobile recharge and one utility bill — keeping his monthly card spend to around ₹4,000 — well below 30% of his limit.

He set a calendar reminder to pay the full outstanding amount three days before the due date each month. To understand exactly when his statement generates and when his payment is due, he read through the billing cycle rules carefully before activating the card.

After 14 months of consistent on-time full payments, Rohit’s CIBIL score had improved significantly. His bank offered to upgrade the card to an unsecured product and released the lien. His ₹25,000 — plus 14 months of FD interest — became fully accessible again.

The key insight: Rohit treated the secured card as a score-building tool, not a credit line. He never spent more than he could repay in full the same month.

How to Calculate Your Ideal Spend on a Secured Credit Card

Safe Monthly Spend = Credit Limit × 30%

Your credit utilisation ratio is the percentage of your available credit limit that you are currently using. Credit bureaus treat utilisation above 30% as a negative signal. Staying below this threshold consistently is one of the fastest ways to improve your CIBIL score — even more so when you are starting from a thin file.

Using Rohit’s example, here is how the calculation works with an illustrative ₹20,000 card limit (actual limits vary by bank and FD amount):

| Scenario | Monthly Spend | Utilisation % |

|---|---|---|

| Ideal — fastest score growth | ₹4,000–₹6,000 | 20–30% |

| Acceptable | Up to ₹6,000 | Up to 30% |

| Hurts score recovery | ₹10,000 and above | 50% and above |

Even if you can comfortably afford to spend more, keep card usage under 30% of your limit throughout the billing cycle — not just at statement generation date. Bureaus can record your balance at different points in the month. Consistently low utilisation signals financial discipline and accelerates score improvement.

To calculate the exact interest on any balance you carry forward, use the credit card interest calculator before deciding whether to revolve a balance.

Comparison: Secured Credit Card vs Unsecured Credit Card

| Parameter | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Collateral required | Yes — FD lien | No |

| CIBIL score needed | Low or none accepted | 700+ typically required |

| Income proof needed | Usually not required | Salary slips or ITR needed |

| Credit limit basis | Percentage of FD amount | Income level and credit profile |

| FD interest on collateral | Continues to earn | Not applicable |

| Default recovery | Bank recovers from pledged FD | Legal or collection process |

| Bureau reporting | Yes — full history | Yes — full history |

| Upgrade path | Unsecured card after 12–18 months | Credit limit increase over time |

How to Decide What’s Right for You

Your CIBIL score is below 650 or you have no credit history at all — THEN a secured credit card is likely the most accessible credit-building option available to you today.

You can park ₹20,000–₹50,000 in a fixed deposit for 12–18 months without needing that money — THEN you can hold a secured card without financial strain, since the FD keeps earning interest throughout the lien period.

You are a freelancer, student, homemaker, or new employee who cannot show formal income proof — THEN a secured card is one of the very few products that does not require a salary slip or ITR for approval.

Your goal is to qualify for a home loan or personal loan within 18–24 months — THEN starting with a secured card today and following a disciplined repayment plan can meaningfully improve your score within that window.

You tend to overspend or have difficulty paying bills on time — THEN honestly assess whether you can commit to full repayment every single month before applying. Missing payments on a secured card will drop your score further and allow the bank to recover from your FD.

Your CIBIL score is already 720 or above and you have stable formal income — you likely qualify for a regular unsecured card with better rewards, higher limits, and no FD requirement. A secured card offers no advantage in this situation.

Common Mistakes to Avoid

Paying Only the Minimum Amount Due

This is the single most damaging habit a secured card user can form.

When you pay only the minimum, the bank does not mark a default — but you carry a balance forward that attracts 36%–42% annualised interest. On a ₹20,000-limit card with ₹8,000 outstanding, one month of minimum payments costs roughly ₹240–₹280 in interest alone. Your utilisation stays high and your score builds slowly despite regular payments.

Always pay the full outstanding amount. Read about the minimum amount trap before you apply — understanding this is not optional for secured card users.

Using More Than 30–40% of Your Credit Limit

Because your credit limit is tied to a modest FD — often ₹15,000 to ₹25,000 — it is easy to cross the 30% utilisation threshold without realising it.

Spending close to your limit signals credit dependency to bureaus. Set a personal cap at 25–30% of your limit and treat it as a hard ceiling, not a guideline.

Applying to Multiple Banks Simultaneously

Each credit card application triggers a hard inquiry on your CIBIL report. Multiple hard inquiries within a short window signal credit-hungry behaviour and can reduce your score by 10–20 points. Apply to one bank, wait for the outcome, and only approach another issuer if rejected.

Forgetting the Due Date

There is no grace period once you miss the due date. A missed payment is reported to the bureau and remains in your CIBIL history. Set a calendar reminder or activate auto-payment for the full outstanding amount, 3–4 days before the due date — not the minimum.

Treating the Pledged FD as Available for Emergencies

Some cardholders forget about the lien and attempt to break the FD during a cash crunch. The attempt will fail — and it may trigger card cancellation. Keep a separate emergency fund that is entirely unconnected to your secured card FD.

Closing the Card Too Early

Closing a credit account reduces your average credit history length, which can lower your CIBIL score — especially when you have few accounts. If you have built 12 months of clean history, explore upgrading to an unsecured card rather than closing. Speak with your card issuer before you cancel anything.

When This May Not Be the Right Choice

A secured credit card is not the right move in every situation. Consider alternatives if any of the following apply:

- You are likely to need access to the FD amount within the next 12–18 months for an emergency, planned purchase, or home expense — the lien will block you entirely, with no exceptions.

- Your CIBIL score is already 700 or above and you have formal income proof — you are better placed to explore an unsecured card with stronger rewards and no collateral requirement. Start by reviewing your options as a first credit card applicant instead.

- You are already carrying high-interest debt — a running personal loan EMI or outstanding credit card balance — and your monthly cash flow is under pressure. Adding another credit product in this situation increases default risk on all fronts.

- You cannot realistically commit to full repayment every month — a secured card used without repayment discipline will damage your CIBIL score further, not build it.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Secured credit card terms — including FD minimums, credit limit percentages, interest rates, fees, and repayment rules — are set individually by each bank and can change without notice. Always verify the specific terms of any card directly from the issuing bank’s official website or its Key Facts Statement (KFS), which every bank is required to provide under RBI guidelines.

Verify regulations and credit guidelines from these official sources:

- Reserve Bank of India — rbi.org.in

- TransUnion CIBIL (credit score and report enquiries) — transunioncibil.com

- Issuing bank or NBFC — official bank domain only

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Open the secured card at a bank where you already have a savings account. The bank already holds your KYC and may have a view of your salary credits. Onboarding is faster, and the relationship can help when you request an upgrade after 12 months.

- Set auto-pay for the full statement amount — not the minimum. Most banking apps let you configure auto-payment for the total outstanding. Use this to eliminate any chance of a missed due date, even during a busy month.

- Do not convert purchases to EMI on a secured card. EMI conversions reduce your available credit limit mid-cycle and increase utilisation. Keep the card reserved for small, predictable spends you can repay in full.

- Check your CIBIL report three months after activation. Confirm the card is appearing correctly — correct credit limit, correct payment history. Bureau reporting errors are more common than people expect, and catching them early avoids months of lost score-building.

- Ask your bank about the upgrade path at the 12-month mark. Some issuers proactively offer conversion to an unsecured card; others require you to formally request it. Don’t wait passively — the sooner the card is converted, the sooner your FD lien is released.

- Use the card only for recurring, predictable expenses. Mobile bill, OTT subscription, utility payment — these are fixed monthly amounts you will always repay in full. They build a clean, consistent payment history without any overspending risk.

Frequently Asked Questions

What is a secured credit card in India?

A secured credit card is issued by a bank against a fixed deposit held with that bank. The FD acts as collateral — the bank places a lien on it and issues a Visa or Mastercard credit card with a limit based on the FD value. It works exactly like a regular credit card: accepted online, offline, and internationally, and fully reported to credit bureaus.

Can I get a secured credit card with a CIBIL score of 0 or -1?

Yes. A score of 0 or -1 means you have no credit history — a thin file — not that you have a poor repayment record. Most banks offering FD-backed secured cards accept applicants with no prior credit history, since the FD collateral covers the bank’s risk regardless of your score.

What happens if I miss a payment on my secured credit card?

The bank will report the missed payment to credit bureaus, which will lower your CIBIL score. If you continue missing payments and formally default, the bank has the right to recover the outstanding amount from your pledged FD. The missed payment remains on your CIBIL record and is visible to future lenders for years.

Is the interest rate on a secured card lower because of the FD?

No. The FD collateral reduces the bank’s default risk but does not translate into a lower interest rate for you. Interest rates on unpaid balances are comparable to regular credit cards — as of recent data, this is typically 3%–3.5% per month (36%–42% annualised) at most Indian banks. Paying the full outstanding amount every month is the only way to avoid interest charges entirely.

How much credit limit will I get on a secured credit card?

Credit limits are calculated as a percentage of your FD amount, based on the issuing bank’s internal policy. This percentage and the minimum FD required vary across banks and can change. Always review the card’s Key Facts Statement (KFS) before applying for the exact terms.

Can I use a secured credit card for online purchases and international transactions?

Yes, in most cases. Secured cards issued on Visa and Mastercard networks work for online purchases, contactless payments, and international transactions — subject to the features of your specific card product. Check the card’s MITC (Most Important Terms and Conditions) for details on international usage fees before travelling.

Does my FD earn interest while the lien is in place?

Yes. The lien restricts withdrawal of the principal, but the FD continues to earn interest at the rate agreed at the time of booking. Interest is typically credited to your linked savings account at the scheduled intervals throughout the lien period.

How long does it take to improve my CIBIL score with a secured credit card?

Most users see a meaningful improvement within 12–18 months of consistent on-time full payments and low credit utilisation below 30%. The exact timeline depends on your starting score, any negative history already on your file, and how disciplined your usage is throughout the period.

Can I get a secured credit card without income proof?

Yes, for most FD-backed secured cards. The bank’s risk is covered by the FD, so formal income documents — salary slips or ITR — are generally not required. Requirements vary by bank, so verify the specific eligibility criteria directly before applying.

What does a lien on a fixed deposit mean?

A lien is a legal freeze placed by the bank on your FD account. While active, you cannot withdraw the FD principal, break it prematurely, or pledge it as collateral elsewhere. The lien is fully released when you close, cancel, or upgrade the secured credit card.

Final Verdict

A secured credit card is the most practical and accessible starting point for anyone with a low CIBIL score, no credit history, or no income proof. It is a real credit card — not a prepaid card — and with disciplined usage it is one of the most reliable ways to build a strong credit profile from scratch. The trade-off is straightforward: an FD locked for 12–18 months, an annual card fee, and the discipline to pay the full outstanding amount every month without fail.

The biggest risk is not the FD lien — it is using the card without repayment discipline. Used correctly, a secured credit card is a stepping stone, not a destination. Once your score is strong enough, upgrade to an unsecured card, recover your FD, and use the credit profile you built to access better financial products.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.