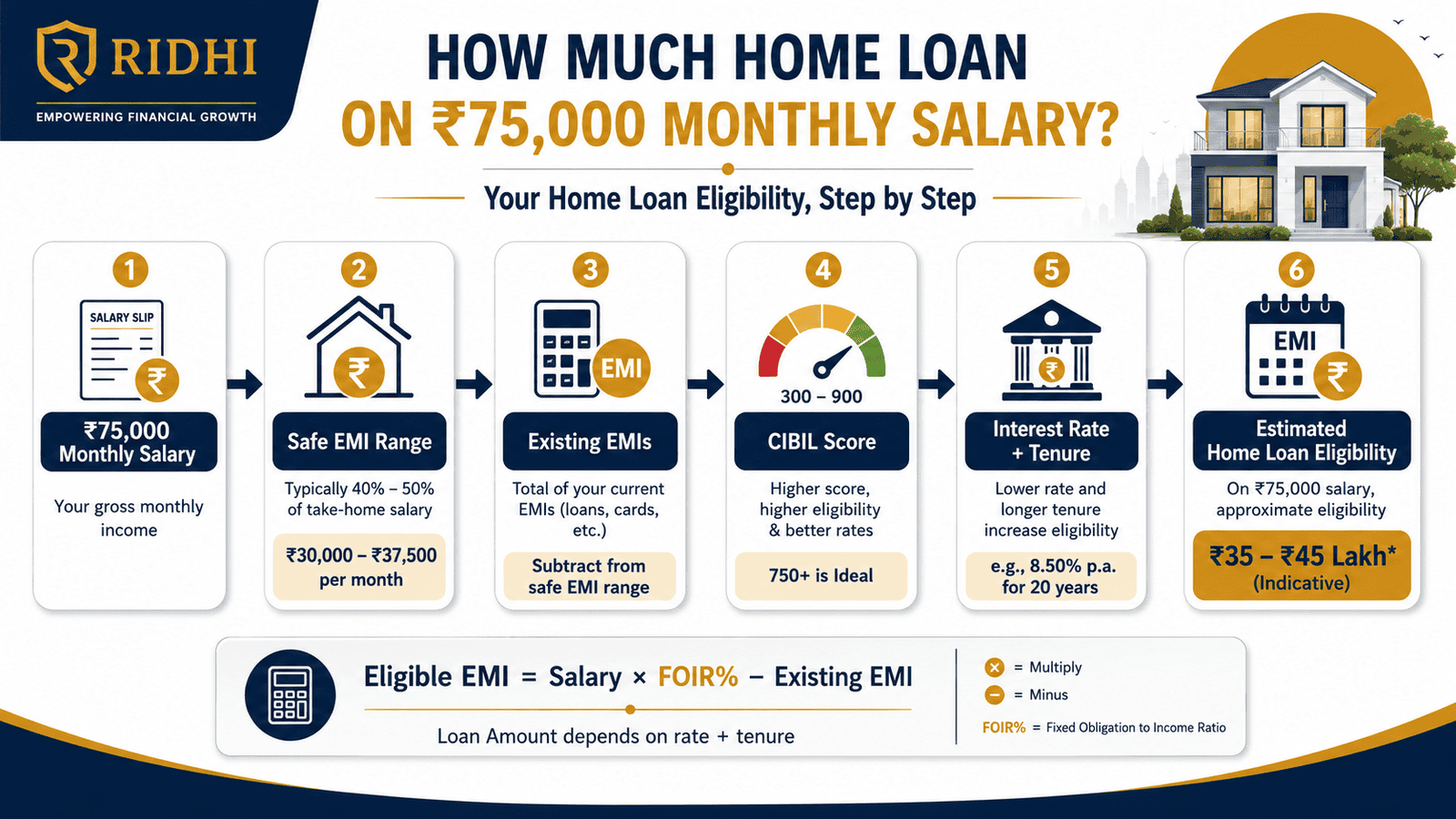

You earn ₹75,000 a month and are looking at property listings. The question is real and immediate: how much home loan can I actually get — and will it cover the apartment I have in mind?

Home loan on ₹75,000 salary is not decided by your income alone. Lenders in India factor in your net take-home pay (not your CTC), existing EMIs, credit score, the interest rate at the time of application, the loan tenure you choose, and the property’s market value. Every one of these variables can move the eligible amount by several lakhs.

This article gives you planning-grade estimates, explains the lender logic behind them, and helps you figure out how much is genuinely safe — not just how much a bank might sanction on paper.

Quick Answer: Home Loan on ₹75,000 Salary

Home loan on 75000 salary depends on net income, existing EMIs, credit score, interest rate and tenure. As a rough planning example, if a lender allows ₹30,000–₹37,500 EMI, eligibility may fall around ₹32–₹45 lakh, but approval varies by bank.

How to Calculate Home Loan Eligibility on ₹75,000 Salary

Eligible Home Loan EMI = (Monthly net income × FOIR %) − Existing EMIs

Most Indian lenders use a Fixed Obligation to Income Ratio (FOIR) of 40%–50% of net monthly income. On ₹75,000 take-home, that works out to ₹30,000–₹37,500 as the maximum EMI allowed across all loans. If you already carry a ₹8,000 personal loan EMI, only ₹22,000–₹29,500 is left for your home loan repayment.

The table below shows estimated loan amounts at different tenures, assuming a home loan rate of approximately 8.75% per year. These are planning estimates — actual amounts depend on your lender’s current rate and credit policy.

| Eligible EMI (₹) | Tenure (Years) | Estimated Loan Amount (approx.) |

|---|---|---|

| ₹30,000 | 15 | ₹29.8 lakh |

| ₹30,000 | 20 | ₹33.9 lakh |

| ₹30,000 | 25 | ₹36.5 lakh |

| ₹37,500 | 20 | ₹42.4 lakh |

| ₹37,500 | 25 | ₹45.6 lakh |

Longer tenure raises your eligible loan amount — but at a steep cost. On a ₹34 lakh loan at 8.75% for 20 years, your total payout over the loan period is approximately ₹72 lakh. You pay roughly ₹38 lakh in interest alone — more than the principal. Use our EMI calculator India to test different loan amounts, rates, and tenures before deciding.

Key Takeaways

- A ₹75,000 salary borrower with no existing EMIs may be eligible for an estimated ₹33–₹42 lakh home loan at a 20-year tenure, depending on the lender’s FOIR and prevailing interest rate.

- An existing ₹8,000 personal or car loan EMI can cut your eligible home loan by approximately ₹9–10 lakh — existing obligations matter more than most borrowers realise.

- Lender maximum eligibility and safe affordability are two different numbers. Keeping total EMIs below 40%–45% of take-home income leaves room for savings and emergencies.

- Gross CTC and net take-home are not the same. If your CTC is ₹75,000/month but your bank credit is ₹62,000, lenders use the lower figure.

- A CIBIL score of 750 and above may improve approval chances and help you access better rate offers — but does not guarantee sanction.

- Choosing a 25-year tenure over 20 years adds roughly ₹8–14 lakh to total interest paid on a ₹35 lakh loan.

- Down payment, stamp duty, registration, legal fees, and a six-month emergency fund are not part of the home loan — plan for them separately.

Key Facts at a Glance

| Factor | Detail | Note |

|---|---|---|

| Monthly salary used for assessment | ₹75,000 net take-home | Not gross CTC |

| Typical FOIR range | 40%–50% of net income | Varies by lender and credit profile |

| Eligible EMI range (no existing debt) | ₹30,000–₹37,500 | Before deducting existing EMIs |

| Estimated loan range (planning) | ₹32–₹45 lakh | Tenure and rate dependent |

| CIBIL score preferred | 750 and above | Below 650 may lead to rejection |

| Loan-to-value ratio (LTV) | Up to 75%–90% of property value | Per RBI guidelines; varies by loan size |

What Decides Home Loan Eligibility on ₹75,000 Salary

FOIR: The Number Lenders Actually Use

Fixed Obligation to Income Ratio is the percentage of your monthly net income a lender allows for all combined EMI commitments. At a 40% FOIR on ₹75,000, you get a maximum of ₹30,000 in combined monthly obligations. If a ₹6,000 vehicle loan and a ₹5,000 credit card minimum due already sit on your credit report, only ₹19,000 is available for the home loan EMI — cutting your eligible loan amount significantly.

Before you approach any bank, calculate your own safe EMI limit based on your actual monthly expenses. The lender’s FOIR is a ceiling, not a recommendation.

Net Salary vs. Gross CTC

Banks assess net monthly salary — the amount credited to your account after PF, income tax, and professional tax deductions. If your annual CTC is ₹9 lakh, your gross monthly figure is ₹75,000. But after deductions, your take-home may be ₹62,000–₹68,000. Using CTC to estimate eligibility leads to overconfidence — a difference of ₹7,000–₹10,000 in assessed income can shift your eligible loan by ₹6–9 lakh.

CIBIL Score and Credit Profile

A strong credit score — generally 750 and above — may improve approval chances and help you access better rate offers from lenders competing for your business. A score below 650 often results in rejection or a noticeably higher interest rate. A higher rate on a ₹35 lakh loan over 20 years can add ₹5–10 lakh to your total interest bill. However, credit score is one factor among several. Job stability, employer type, repayment history, and property legality all matter too.

Loan Tenure and Total Interest

A 25-year tenure versus a 20-year tenure can raise your eligible loan by ₹2–4 lakh on the same EMI. But on a ₹36 lakh loan at 8.75% for 25 years, total interest paid over the tenure is approximately ₹54 lakh — compared to roughly ₹38 lakh on the same principal over 20 years. Choose the shortest tenure your monthly cash flow can sustain, not the longest available.

Loan-to-Value Ratio and Your Down Payment

Lenders finance only a portion of the property value. Per RBI guidelines, LTV can go up to 90% for loans up to ₹30 lakh, and may be capped at 75%–80% for larger amounts. On a ₹50 lakh flat, you may need to arrange ₹7–12 lakh as a down payment — plus stamp duty and registration, which runs 5%–8% of property value in most states. These costs come entirely from your savings, not from the loan.

Co-Applicant Income

Adding a working spouse as a co-applicant allows the lender to consider combined income for FOIR calculations. A joint household earning ₹75,000 + ₹45,000 may qualify for a significantly larger loan than either applicant alone. Both applicants are assessed individually for credit score and repayment history. If either co-applicant has a poor credit profile, it can reduce the overall offer — or trigger rejection.

Real Example: Rahul, 32, Bengaluru

Rahul is a salaried software developer in Bengaluru with a net take-home salary of ₹75,000 per month. He wants to buy his first apartment and is trying to determine whether to plan for a ₹30 lakh, ₹40 lakh, or higher loan.

Scenario A — No existing EMI: Rahul has no outstanding loans. At a 40% FOIR, eligible EMI is ₹30,000. At a 20-year tenure and an assumed rate of 8.75%, his estimated eligible loan is approximately ₹33.9 lakh.

Scenario B — Existing ₹8,000 personal loan EMI: Rahul carries a personal loan with ₹8,000 monthly outflow. His available home loan EMI drops to ₹22,000. At the same tenure and rate, eligible loan falls to approximately ₹24.9 lakh — a ₹9 lakh reduction for one active obligation.

Scenario C — Joint loan with spouse: Rahul’s spouse earns ₹45,000/month. Combined net income is ₹1,20,000. At 40% FOIR and no existing EMIs, combined eligible EMI is ₹48,000 — potentially supporting a loan of ₹54 lakh or more at a 20-year tenure.

The lesson: existing debt and co-applicant income are the two biggest levers on your home loan eligibility — larger than the difference between lenders in most cases.

Comparison: Safe vs. Moderate vs. Aggressive Borrowing on ₹75,000 Salary

| Approach | Monthly EMI (₹) | Estimated Loan (20 yrs, approx.) |

|---|---|---|

| Safe — 35% FOIR, breathing room | ₹26,250 | ~₹29.7 lakh |

| Moderate — 40% FOIR, planned | ₹30,000 | ~₹33.9 lakh |

| Aggressive — 50% FOIR, stretched | ₹37,500 | ~₹42.4 lakh |

A safe borrower retains room for savings, insurance premiums, and unplanned expenses. An aggressive borrower may face genuine cash-flow stress if rates rise on a floating loan, income is interrupted, or a household emergency arrives. Maximum eligibility is a ceiling a lender will offer — it is not a budget recommendation.

How to Decide What’s Right for You

your total EMI — including the new home loan — will stay below 40% of your actual net take-home — THEN this loan amount is likely within a manageable range for a stable-income salaried borrower.

existing EMIs already consume ₹10,000 or more each month — THEN close or reduce those obligations before applying, or lower your target home loan amount by ₹8–12 lakh accordingly.

you are considering adding your spouse as a co-applicant — THEN read about joint loan benefits first, including shared repayment liability and how both credit scores affect the offer.

your income is partly variable — bonus, incentives, or freelance income — THEN stress-test your affordability using fixed monthly salary only. Plan as if the variable component does not exist.

you do not yet have a six-month emergency fund in place — THEN delay the purchase, save more, and apply for a smaller loan when your financial cushion is solid.

you can cover the down payment, stamp duty, registration, and at least three months of EMI from your existing savings without zeroing out your reserves — a home loan at this stage may leave you dangerously over-exposed to any financial shock.

Common Mistakes to Avoid

Using CTC Instead of Net Take-Home

CTC includes PF contributions, gratuity, and variable components that never credit to your bank account.

Planning EMI affordability on a ₹75,000 gross figure when your actual take-home is ₹63,000 creates a ₹12,000 gap in your estimates — which can get you into a loan you cannot comfortably service.

Always use the “Net Pay” line on your salary slip for all eligibility and affordability calculations.

Ignoring Existing Credit Card and Loan EMIs

Credit card minimum due amounts, buy-now-pay-later instalments, and personal loan EMIs all count toward the FOIR calculation.

A ₹10,000 credit card minimum due and a ₹5,000 consumer loan EMI together can reduce your eligible home loan by ₹15–18 lakh.

Clear short-tenure personal loans before applying and reduce credit card balances to zero if possible.

Assuming Salary Alone Guarantees Approval

Lenders check credit score, employer type, job stability, property documentation, and repayment history alongside income.

A salaried borrower in a company on a lender’s negative list — or with a CIBIL score below 650 — can be declined despite an otherwise adequate salary.

Assess your full credit profile, not just your pay slip, before applying.

Not Checking CIBIL Score Before Applying

Every formal loan application triggers a hard inquiry on your credit report. Several applications in a short window can lower your score.

Understand CIBIL score basics before approaching lenders. If your score is below 700, spend six to twelve months improving it. Moving from 690 to 760 can open better rate offers — saving ₹3–5 lakh in total interest on a ₹35 lakh loan.

Check your score for free through authorised channels before any formal bank visit.

Forgetting One-Time Property Buying Costs

Stamp duty and registration in most Indian states runs 5%–8% of property value, and must be paid at the time of registration — entirely from savings.

On a ₹50 lakh flat, stamp duty and registration alone can cost ₹3–4 lakh. Add legal fees, processing charges, home insurance, and interiors, and the out-of-pocket requirement before moving in may be ₹8–12 lakh.

Budget these costs explicitly in your home-buying plan. They are not part of the loan disbursement.

When This May Not Be the Right Choice

A home loan on ₹75,000 salary may not be financially sound right now if your existing EMIs already consume more than ₹25,000 per month — leaving too little room for a home loan repayment without straining daily expenses.

It is also risky if your employment is on a short-term or contractual basis, you have no emergency fund in place, or your down payment is being funded through a high-interest personal loan. Layering high-cost short-term debt under a long-term home loan creates a fragile financial structure.

If your monthly fixed expenses — rent, EMIs, groceries, school fees, and insurance — already exceed ₹55,000, adding a ₹28,000–₹35,000 home loan EMI may leave almost nothing for savings or unexpected costs.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- Reserve Bank of India — rbi.org.in: Broad home loan lending norms, loan-to-value ratio guidelines, key fact statement requirements, and borrower protection regulations.

- Your chosen bank or NBFC official website: Current floating interest rate, FOIR policy, processing fee, prepayment charges, tenure limits, and specific eligibility criteria. These vary by lender and can change without notice.

- Loan sanction letter and Key Fact Statement (KFS): Read both documents before signing. The KFS discloses total loan cost including fees, insurance, and charges — not just the headline EMI.

Once you have your eligibility estimate, understand what comes next by reading the step-by-step home loan process from application to possession.

Expert Tips

- Borrow below maximum: A lender may approve ₹42 lakh. That does not mean you need ₹42 lakh. Borrowing ₹4–5 lakh less at the same rate over 20 years saves ₹4–7 lakh in total interest and meaningfully reduces monthly pressure.

- Clear short personal loans before applying: A personal loan with 15–18 months remaining is dead weight on your FOIR. Paying it off before your home loan application can increase your eligible amount by ₹8–12 lakh.

- Compare total payout, not just EMI: A 0.25% rate difference on a ₹35 lakh loan over 20 years is roughly ₹1.8–2 lakh in total interest. Always compare lenders on total repayment amount — not the monthly number alone.

- Do not borrow for the tax deduction: Home loan tax benefits under Sections 24(b) and 80C are worth understanding — see home loan tax benefits for current rules — but they should never be the primary justification for taking a larger loan.

- Part-prepay when surplus arrives: Even one extra EMI per year from a bonus or annual increment can cut 2–3 years off a 20-year loan. Check whether your lender charges prepayment fees on floating-rate loans — for most borrowers, floating-rate home loans carry no prepayment penalty.

- Shorten tenure on refinancing if rates fall: If you start with a 25-year tenure and rates drop significantly in year 3–5, request a reduction in tenure rather than EMI when refinancing. Reducing tenure saves far more interest over the remaining loan life.

Frequently Asked Questions

How much home loan can I get on ₹75,000 salary?

At a 40% FOIR and 20-year tenure, a borrower with no existing EMIs may be eligible for an estimated ₹33–₹34 lakh. With a 50% FOIR and 25-year tenure, this could rise to around ₹45 lakh. These are planning estimates. Actual approval depends on your lender’s policy, credit score, and the prevailing interest rate at the time of application.

Is ₹75,000 gross salary or take-home salary considered by lenders?

Most lenders in India assess net take-home salary — the amount credited to your bank account each month after PF, income tax, and deductions. If your monthly gross is ₹75,000 but your take-home is ₹63,000, the lender will use ₹63,000 as the base for FOIR calculations. Always use your net pay figure when estimating eligibility.

How much EMI is safe on ₹75,000 salary?

A widely used rule of thumb is to keep all EMIs combined — including the home loan — below 40%–45% of net income. On ₹75,000, that means total obligations of ₹30,000–₹33,750 per month. Going above 50% leaves very little room for savings, insurance, family expenses, and any financial surprise.

Can a co-applicant increase my home loan eligibility?

Yes. Adding a working spouse or family member as a co-applicant allows the lender to consider combined income, which directly raises the eligible EMI pool and loan amount. Both co-applicants are equally liable for repayment, and both credit profiles are assessed. If either co-applicant has a poor score, it can drag down the offer.

Does CIBIL score affect the home loan amount I get?

Indirectly, yes. A better score may qualify you for a lower interest rate — which raises the loan amount a given EMI can support, and lowers total interest over the tenure. A score below 650 may result in rejection or a significantly higher rate. A score of 750 and above is generally considered favourable by most lenders.

What if I already have a ₹8,000 personal loan EMI running?

That ₹8,000 is subtracted from your eligible EMI pool before the home loan is assessed. If a lender allows ₹30,000 in total obligations, only ₹22,000 is left for the home loan EMI. At a 20-year tenure, this reduces your eligible home loan by approximately ₹9–10 lakh compared to a borrower with no existing debt.

Should I pick a longer tenure to increase my loan eligibility?

A longer tenure does raise eligible loan amount for the same EMI. But it significantly increases total interest. The gap between a 20-year and a 25-year loan on the same ₹35 lakh principal is roughly ₹10–14 lakh in additional interest paid. Choose the shortest tenure your monthly income and expenses can comfortably support.

Can I include bonus or variable pay when estimating eligibility?

Some lenders consider a portion of consistent variable income; others rely on fixed monthly salary only. This varies by lender and is assessed case by case. Do not assume your full bonus will be included — verify directly with the bank during the pre-application stage. Always plan your own affordability on fixed income only.

Final Verdict

Home loan on ₹75,000 salary is achievable and practical — but the right amount is rarely the maximum a lender will sanction. Most borrowers in this bracket can realistically plan for ₹30–₹42 lakh, depending on existing EMIs, credit profile, tenure chosen, and the interest rate at the time of application. Add a co-applicant and that range rises considerably.

Use FOIR, your actual net take-home, total interest over the full tenure, and a realistic household budget together — not just the lender’s eligibility output. The right home loan is the one you can repay comfortably, not the biggest one a lender offers. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Vikram Sethi writes about loans, EMI planning, credit score impact, borrowing costs, and repayment decisions for Indian borrowers. His content helps readers look beyond the monthly EMI and understand the full cost of borrowing, including principal, interest, processing fees, GST, insurance, prepayment charges, foreclosure fees, late payment penalties, and credit score impact.

He covers topics such as EMI calculators, home loan eligibility, personal loan eligibility, debt-to-income ratio, flat interest rate vs reducing balance, missed EMI consequences, loan prepayment vs part payment, home loan balance transfer, processing fees, gold loan vs personal loan, car loan vs cash purchase, top-up home loans, loan against PPF, and credit score basics.

Vikram’s writing style is practical, cautionary, and calculation-driven. He uses Indian examples, ₹ amounts, comparison tables, and decision frameworks to help borrowers compare options more carefully. His articles are educational and do not guarantee loan approval, interest rates, or savings. Readers should verify current rates, charges, eligibility, and terms directly with lenders before applying or refinancing.