Selling a property in India can mean receiving ₹60 lakh on one day — and receiving a tax notice six months later. Capital gains tax on property sale applies to the profit you make when you transfer a house, flat, plot, or building, and the tax impact depends on one decision above all others: whether your gain is short-term or long-term. Get that classification right, and you may owe ₹2 lakh. Get it wrong, and the same gain can cost ₹8 lakh or more.

The rules changed significantly around July 2024. The default long-term capital gains rate shifted to 12.5% without indexation, while a grandfathered option — 20% with indexation — may still apply for eligible resident individuals and HUFs who acquired land or buildings before 23 July 2024. These two paths can produce dramatically different results on the same sale, and choosing between them is now one of the most important tax calculations a property seller must do.

Exemptions under Section 54 and Section 54EC exist and can reduce liability to zero in the right scenario — but they come with strict deadlines, investment caps, and documentation requirements that catch many sellers off guard. This article walks through every step: how to classify your gain, how to calculate it, and what exemption routes are realistically available to you. For a full picture of buying, selling, and owning property in India, start with our complete real estate and home buying guide.

Quick Answer: Capital Gains Tax on Property Sale

Capital gains tax on property sale depends mainly on the holding period. If property is held up to 24 months, gains are STCG and taxed at slab rates. If held longer, LTCG rules apply, generally 12.5% without indexation, with limited grandfathered indexation options available for eligible resident individuals and HUFs for land or buildings acquired before 23 July 2024. Verify all applicable rates and conditions at incometax.gov.in before filing.

Key Takeaways

- If you have held a house, flat, or plot for 24 months or less, any profit is a short-term capital gain — it gets added to your total income and taxed at your slab rate, which can reach 30% plus surcharge and cess on a high salary.

- If held for more than 24 months, the gain is long-term and generally taxed at 12.5% without indexation under post-July 2024 rules — significantly lower than most STCG outcomes but still material on a large gain.

- Eligible resident individuals and HUFs may have a grandfathered route: 20% with indexation on land or buildings acquired before 23 July 2024, which can cut taxable gain substantially when inflation has raised the indexed purchase cost over many years.

- Capital gains tax applies to profit — not the full sale price. Sale consideration minus purchase cost, minus improvement cost, minus allowable transfer expenses gives the taxable gain.

- Section 54 can eliminate LTCG if you reinvest the gain in a qualifying residential house within the prescribed window — but timing, investment limits, and documentation are strict, and must be verified before you plan around it.

- The Capital Gains Account Scheme (CGAS) lets you park uninvested proceeds in a designated bank account before the ITR due date, protecting your exemption eligibility while the reinvestment is still in progress.

- The Income Tax Department receives property sale data through registration records and Form 26QB — omitting capital gains from your ITR is a compliance risk with real consequences.

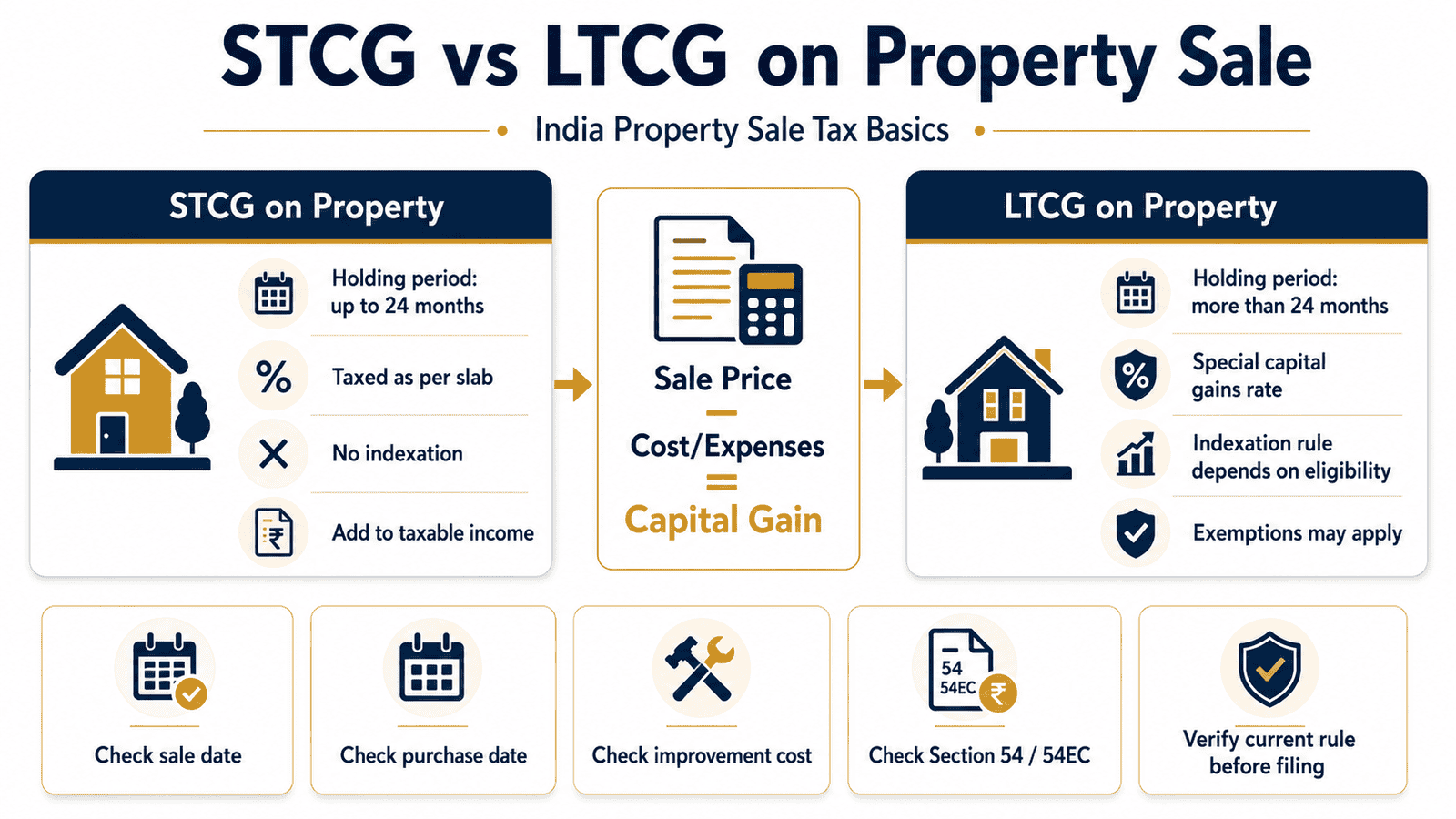

STCG vs LTCG on Property Sale: Key Differences

| Parameter | STCG (Short-Term) | LTCG (Long-Term) |

|---|---|---|

| Holding period | 24 months or less | More than 24 months |

| Tax rate on gain | Slab rate — up to 30% | Generally 12.5% |

| Indexation benefit | Not available | Grandfathered option only |

| Section 54 / 54EC exemption | Generally not available | Available with conditions |

| ITR schedule | Schedule CG in ITR-2 / ITR-3 | Schedule CG in ITR-2 / ITR-3 |

| Surcharge and cess | Applicable based on total income | Applicable based on total income |

| Where it hurts most | Quick resale of flat purchased recently | Large gain with no reinvestment plan |

Key Facts at a Glance

| Aspect | Details |

|---|---|

| Asset types covered | House, flat, plot, land, building, commercial property |

| STCG holding period | 24 months or less from date of acquisition |

| LTCG holding period | More than 24 months from date of acquisition |

| STCG tax rate | Added to total income; taxed at applicable slab rate |

| LTCG tax rate | Generally 12.5% without indexation (post-July 23, 2024) |

| Grandfathered option | 20% with indexation for eligible resident individual/HUF; land or buildings acquired before July 23, 2024 — verify eligibility |

| Main exemption sections | Section 54 (reinvestment in residential house), Section 54EC (specified bonds), Section 54F (non-residential assets) |

| Governing law | Section 45, Section 48, Section 112, Income Tax Act 1961 |

| Official source | incometax.gov.in |

What Is Capital Gains Tax on Property Sale?

Under the Income Tax Act, any profit earned from transferring a capital asset is treated as a capital gain and becomes taxable in the year of transfer. Immovable property — your flat, house, inherited land, plot, or commercial shop — is a capital asset. When you sell it for more than what you paid, the difference, after specified adjustments, is your capital gain.

This gain is not the same as your sale price. The calculation starts with the sale consideration — generally the actual sale price, or the stamp duty value if higher under Section 50C — and subtracts three key items: the cost of acquisition (what you originally paid, including stamp duty and registration at the time of purchase), the cost of improvement (verified renovation or structural work done after purchase, not routine maintenance), and transfer expenses (brokerage, legal fees, and similar allowable costs).

Many sellers make a costly assumption: they believe the tax obligation disappears if the money is immediately used to repay a loan or buy another asset. That is not how it works. The capital gains obligation is triggered by the transfer — the exemption sections are separate provisions that can reduce or eliminate the tax, but only when specific conditions are met. Receiving the money and spending it elsewhere is not an exemption.

Inherited property follows similar principles, but the original owner’s purchase price and acquisition date become the starting point. If your parents bought a flat in 1995 for ₹8 lakh and you sell it today for ₹80 lakh, the gain — calculated from the original ₹8 lakh (or fair market value as of a specified date, in certain cases) — is taxable, and the holding period typically includes the original owner’s tenure. This makes many inherited properties long-term gains from day one of the heir’s ownership. If you are still weighing whether to sell, hold, or rent out, see our guide on the rent vs buy decision for Indian families.

Short-Term Capital Gain on Property Sale

If the gap between your purchase date and sale date is 24 months or less, the profit is a short-term capital gain. There is no special flat rate for STCG on property — the entire gain is added to your total income for that financial year and taxed at your applicable income slab rate. For a salaried professional already in the 30% bracket, this means every rupee of STCG is taxed at 30%, plus surcharge and 4% health and education cess.

On a ₹20 lakh short-term gain added to a ₹28 lakh salary, the marginal tax on the gain alone approaches ₹6.2 lakh — more than double what LTCG rules would have produced on the same profit with a longer holding period. There is no indexation benefit for short-term gains and no access to Section 54, 54EC, or 54F exemptions. The gain goes straight into your income with no reduction available.

This is why the 24-month boundary carries such weight in property sale planning. Rohan, 35, a Bengaluru-based sales manager earning ₹22 lakh annually, bought a flat in February 2023 for ₹45 lakh and received an attractive offer of ₹62 lakh in November 2024 — 21 months later. His ₹17 lakh gain was short-term, adding it to his income and pushing the effective tax to approximately ₹5.1 lakh. Had he waited three more months past the 24-month mark, the same gain would have qualified for LTCG treatment — and the tax would have been roughly ₹2.1 lakh.

How to Calculate Capital Gains Tax on Property Sale

Capital Gain = Sale Consideration − Cost of Acquisition − Cost of Improvement − Transfer Expenses

Let us apply this using Amit, 42, an IT manager from Pune earning ₹32 lakh per year. He purchased a flat in FY 2016–17 for ₹50 lakh and sold it in FY 2024–25 for ₹80 lakh. Brokerage and legal expenses came to ₹1.5 lakh. There were no verifiable improvement costs.

Step 1 — Establish holding period: Acquired FY 2016–17, sold FY 2024–25 — more than 24 months. This is a long-term capital gain.

Step 2 — LTCG without indexation at 12.5%:

Gain = ₹80 lakh − ₹50 lakh − ₹1.5 lakh = ₹28.5 lakh

Tax at 12.5% = approximately ₹3.56 lakh (plus surcharge and cess)

Step 3 — Grandfathered LTCG with indexation at 20% (if eligible):

Amit acquired this flat before 23 July 2024 and is a resident individual — he may be eligible to compare both methods. Using the official Cost Inflation Index values for FY 2016–17 and FY 2024–25, the indexed purchase cost would be materially higher than ₹50 lakh, substantially reducing the taxable gain. On an illustrative indexed gain of approximately ₹9–11 lakh, tax at 20% would be ₹1.8–₹2.2 lakh — lower than the 12.5% method in this scenario. The correct CII values and eligibility must be verified at incometax.gov.in before choosing.

This example is illustrative. Actual figures depend on the official CII for each financial year, applicable surcharge, cess, residency status, and current Income Tax rules. Use the Income Tax Calculator for FY 2025–26 to model your wider tax position, and consult a tax professional for the final computation.

| Scenario | Basis | Illustrative Tax on ₹28.5L Gain |

|---|---|---|

| STCG — held under 24 months | Added to income; 30% slab | ~₹8.55 lakh + cess |

| LTCG — 12.5% without indexation | Post-July 2024 standard rate | ~₹3.56 lakh + cess |

| LTCG — 20% with indexation (grandfathered) | Eligible resident individual/HUF only | ~₹1.8–₹2.2 lakh + cess |

Long-Term Capital Gain on Property Sale

A property held for more than 24 months qualifies for LTCG treatment. Under rules announced in Union Budget 2024, the standard LTCG rate for immovable property is 12.5% without indexation, effective for transfers on or after 23 July 2024.

The Budget also retained a grandfathered option for resident individuals and HUFs: if the land or building was acquired before 23 July 2024, the seller may compute tax under both the 12.5% without-indexation method and the older 20% with-indexation method, and use whichever results in lower tax. This option is not available to all categories of taxpayers, nor for all types of immovable property — it is specific to land and buildings, and only for the eligible taxpayer categories. Verify current applicability at incometax.gov.in before relying on it.

Surcharge applies on top of the LTCG rate depending on total income — for individuals with income above ₹50 lakh, the surcharge adds meaningfully to the effective rate. Combined with 4% health and education cess, the actual tax payable on a large property gain can be noticeably higher than the headline 12.5% figure.

If you are buying a new property using the proceeds and taking a home loan for the balance, understanding the interaction between LTCG exemption and home loan tax benefits matters for your overall planning — see our detailed guide on home loan tax benefits under Section 24b and 80C.

Indexation Benefit and the Post-July 2024 Rule

Indexation adjusts your original purchase price upward using the Cost Inflation Index (CII), published annually by the Central Board of Direct Taxes. The logic is straightforward: ₹30 lakh in 2010 is worth more in today’s purchasing power than ₹30 lakh suggests at face value. Indexation inflates the cost of acquisition to reflect this, which shrinks your taxable gain — and the tax on it.

Under the pre-July 2024 rules, LTCG on property was taxed at 20% after indexation, and for properties held over many years, this method often produced a very small taxable gain relative to the nominal sale profit. A flat bought for ₹15 lakh in 2005 and sold for ₹90 lakh in 2024 would have a very different indexed cost than ₹15 lakh, and the tax on the indexed gain was far lower than any flat-rate method would suggest.

The Budget 2024 change means the default is now 12.5% without indexation. For sellers with properties held over many years, especially those acquired in low-inflation-adjusted years, the grandfathered comparison is critically important. Whether 12.5% on the full gain is better or worse than 20% on the indexed gain depends entirely on the specific CII year of acquisition and the degree of price appreciation. There is no universal answer — the two numbers must be calculated and compared for each individual case.

The official CII table, eligibility conditions for the grandfathered option, and any Budget-linked amendments must be verified at incometax.gov.in before filing. This is one calculation where working with a chartered accountant before submission pays dividends.

Exemptions Under Section 54, 54EC and 54F

Three major exemption routes can reduce or eliminate LTCG tax on property sale. None is automatic. Each has its own eligibility criteria, investment timing, monetary limits, and documentary requirements — and meeting some conditions while missing others can result in a full or partial denial of the exemption.

Section 54 — Reinvestment in a Residential House

If you sell a residential house property and invest the long-term capital gain in purchasing or constructing another residential house in India, you can claim exemption under Section 54. The new purchase must happen within one year before or two years after the date of sale. If constructing, completion must occur within three years. The exemption is limited to the capital gain amount reinvested — any surplus gain remains taxable. Verify the current investment cap, number of properties permitted, lock-in conditions, and any recent amendments from incometax.gov.in before planning around this route.

Section 54EC — Specified Bonds

If you prefer not to buy another property, you can invest the long-term capital gain in specified bonds — currently issued by entities such as NHAI and REC, though the eligible issuer list must be verified. Investment must be made within 6 months of the date of sale — not the financial year end, and not the ITR due date. There is a monetary cap on the amount that can be invested per financial year (verify the current limit at incometax.gov.in). The bonds carry a lock-in period during which they cannot be transferred, pledged, or converted. Missing the 6-month window by even a day eliminates the exemption.

Section 54F — Sale of Non-Residential Capital Assets

Section 54F applies when you sell a capital asset other than a residential house — such as a plot, commercial property, or non-residential building — and invest the net sale consideration (not just the gain) in a residential house. The conditions and timelines are similar in structure to Section 54 but the trigger asset and investment base differ. If you own more than one residential house at the time of the new purchase (excluding the one being bought), the exemption may be restricted. Verify the current conditions from incometax.gov.in.

If you are reinvesting in a property priced above ₹50 lakh, be aware that TDS obligations fall on the buyer — see our guide on TDS rules on property purchase above ₹50 lakh to understand how the withholding interacts with the sale transaction.

How to Decide: Which Route Is Right for You

You are a resident individual or HUF who acquired land or a building before 23 July 2024 — THEN calculate both 12.5% without indexation and 20% with indexation and file using the method that produces lower tax. Do not assume either is automatically better.

You have significant LTCG and plan to buy another residential house — THEN explore Section 54, open a CGAS account before the ITR due date if the purchase is not yet complete, and keep all reinvestment documentation.

You do not want to buy another property but want to reduce LTCG — THEN consider Section 54EC bonds within 6 months of the sale date, after confirming the current investment cap and eligible issuers from incometax.gov.in.

You are selling a plot or commercial property and want exemption — THEN check whether Section 54F applies based on your reinvestment of net sale consideration in a qualifying residential house, and verify the residency and property-count conditions.

You have held the property for less than 24 months — do not plan your finances on LTCG rates or exemptions. The gain is added to your income and taxed at your slab rate, which at ₹32 lakh annual salary is 30% plus cess on every rupee of gain.

Capital Gains Account Scheme (CGAS)

The Capital Gains Account Scheme exists to solve one specific problem: you have received the sale proceeds, you intend to reinvest under Section 54 or 54F, but the reinvestment will not be complete before the ITR due date for the year of sale.

In practical terms: if Amit sells his flat in January 2025 and receives ₹80 lakh, but the new flat he is purchasing will only be registered in October 2025, his ITR for FY 2024–25 is due by 31 July 2025. If the capital gain is not yet reinvested and he has not deposited the amount in a CGAS account, his Section 54 claim may be disallowed when he files.

The CGAS allows him to deposit the relevant amount in a designated account at an authorised bank before filing the ITR. The deposit preserves his exemption claim and demonstrates intent to reinvest. He then has the prescribed period — from the sale date — to complete the actual purchase or construction and withdraw the CGAS funds for that purpose.

CGAS is not a tax escape. If reinvestment is not completed within the allowed period, the deposited amount is treated as a capital gain in the year the period expires and becomes taxable then. Withdrawals must follow the prescribed procedure. Always verify the current authorised banks, account type requirements, and withdrawal process from incometax.gov.in or your bank before opening an account.

Documents You Need Before Filing

Capital gains from property sale require a clean paper trail. Collect and organise these before filing your ITR or consulting a CA — missing any document at the last moment can delay the return or create problems with exemption claims.

- Sale deed — registered document showing sale consideration and stamp duty valuation

- Original purchase deed — showing acquisition cost, date, and registration; for inherited property, the original owner’s deed

- Stamp duty and registration receipts from original purchase — these form part of the cost of acquisition

- Improvement bills and renovation invoices — bank payment records and contractor bills for structural improvements (not routine maintenance) incurred after purchase

- Brokerage, legal, and transfer expense proofs — commission agreements, advocate invoices, and payment records forming allowable transfer expenses

- Home loan statement — useful for identifying improvement disbursements or principal repayment records linked to the property

- New property purchase documents — sale agreement, builder payment receipts, and registration details if claiming Section 54

- Section 54EC bond certificate and allotment letter — if investing in specified bonds under Section 54EC

- CGAS account passbook or deposit receipt — if amount is parked before ITR due date

- AIS and Form 26AS from incometax.gov.in — verify that the property transaction is reflected, TDS by the buyer is showing correctly, and sale consideration matches your records

When This May Not Be the Right Choice

Pursuing exemptions under Section 54 or 54EC is not always the best financial decision, even when legally available. If your LTCG is ₹30 lakh but the Section 54EC bond limit is lower, partial exemption still leaves a meaningful tax liability — and the remaining capital is locked in bonds for the lock-in period at a fixed return that may not justify the constraint.

If you already own two residential houses, the Section 54 exemption may be restricted based on current rules — verify the property-count condition before assuming the full exemption applies. If the property sale involves NRI sellers, joint owners with different residency statuses, inherited property with unclear acquisition dates, or a disputed title, standard exemption logic may not apply without professional advice specific to those facts.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Common Mistakes to Avoid

Treating the entire sale price as the taxable gain

Capital gains tax applies to the profit — not the sale proceeds. Many sellers mentally plan for tax on the full ₹80 lakh received when the actual gain after purchase cost, improvement, and expenses may be ₹25 lakh.

This mistake either leads to panic about a non-existent liability or, in the other direction, to incorrect calculations that inflate the deductions. Always compute net gain before estimating any tax.

Apply the formula: sale consideration minus cost of acquisition minus cost of improvement minus allowable transfer expenses.

Losing improvement cost receipts

Homeowners spend ₹4–10 lakh on kitchen renovation, flooring, or structural additions — and then cannot claim the deduction at the time of sale because they have no documented proof.

On a ₹6 lakh improvement claimed under LTCG at 20% with indexation, the tax saving is ₹1.2 lakh. Without receipts, that saving disappears. Scan and store renovation invoices, bank transfer records, and contractor agreements from the date of expenditure.

Assuming the 20% with-indexation method always applies after July 2024

The default LTCG rate for property transfers on or after 23 July 2024 is 12.5% without indexation. The grandfathered 20% with-indexation option is available only to eligible resident individuals and HUFs for land or buildings acquired before 23 July 2024 — not universally.

Applying indexation in your ITR without first confirming eligibility can result in a defective return or a reassessment notice. Verify your eligibility at incometax.gov.in before choosing the method.

Missing the 6-month window for Section 54EC bonds

Section 54EC requires investment within 6 months of the date of property sale — not the ITR due date, not the financial year end. If you sell on 1 November 2024, the bond investment window closes around 30 April 2025, not 31 July 2025.

Sellers who wait until tax season routinely miss this window and lose the exemption entirely. Note the exact sale date and count 6 months immediately. Verify the precise deadline interpretation from incometax.gov.in.

Omitting capital gains from the ITR

Property sale data flows to the Income Tax Department through stamp duty registration records and through TDS filed by the buyer via Form 26QB. The Annual Information Statement (AIS) at incometax.gov.in typically reflects the transaction within the assessment year.

Filing an ITR-1 or an ITR-2 without Schedule CG when a property sale exists in the AIS is a compliance risk that can trigger notices and interest. Use the correct ITR form — generally ITR-2 for salaried individuals with capital gains — and complete Schedule CG accurately.

Confusing the buyer’s TDS obligation with the seller’s capital gains tax

When a buyer purchases property above ₹50 lakh, the buyer deducts 1% TDS from the payment and deposits it via Form 26QB. This appears in the seller’s Form 26AS as a credit — it is not a final settlement of the seller’s capital gains tax.

A seller who receives ₹80 lakh and sees ₹80,000 TDS deducted may assume their property tax is paid. It is not. The TDS is only a fractional advance against a potentially much larger LTCG liability. The seller must still compute capital gains, file Schedule CG, and pay any balance tax owed.

Expert Tips

- If you are 20–22 months into your holding period and a buyer appears, calculate the STCG vs LTCG difference before agreeing to a sale date. On a ₹22 lakh gain at the 30% slab rate versus 12.5% LTCG rate, waiting two more months saves approximately ₹3.6 lakh — more than most negotiation discounts would recover.

- Download your AIS from incometax.gov.in before the sale closes and confirm the purchase-side transaction is reflected correctly. Catching discrepancies before the sale — not after the ITR is filed — saves significant time and stress during assessment.

- If you acquired the property before 23 July 2024 and are a resident individual or HUF, compute both methods — 12.5% without indexation and 20% with indexation — before filing. In many cases involving older acquisitions with moderate price appreciation, the grandfathered method produces substantially lower tax.

- For Section 54 reinvestment: do not rely on oral advice that buying another house is enough. Check the current investment timing rules, property count restrictions, and capital gains account procedure before the sale deed is executed.

- For inherited property: establish the original owner’s purchase price and acquisition year before any sale planning. The cost base and holding period both depend on this, and incorrect figures at the calculation stage can result in underpayment of tax or missed exemptions.

- Consult a chartered accountant for any property sale above ₹50 lakh, especially when joint ownership, NRI status, inherited title, or outstanding disputes are involved. The fee is a fraction of the penalties, interest, and notices that follow incorrect filing.

ITR Reporting and Tax Payment Checklist

Capital gains from property sale must be reported in your ITR for the financial year in which the transfer takes place — generally the year in which the sale deed is executed and registered. For most salaried individuals with a property sale and no business income, the correct form is ITR-2. If you also have business or professional income, use ITR-3. ITR-1 cannot accommodate capital gains — do not use it in the year of a property sale.

In the ITR, fill Schedule CG with the full capital gains details: sale consideration, indexed or non-indexed cost of acquisition, cost of improvement, transfer expenses, holding period classification, applicable tax rate, and any exemption claimed under Section 54, 54EC, or 54F. If you are claiming CGAS deposits as part of an exemption, the details of the deposit must also be reported.

If capital gains tax is payable, do not assume you can wait until July 31. Large capital gains arising during the year may attract advance tax obligations under Sections 234B and 234C. Interest on underpaid advance tax can add meaningfully to the final liability. Verify the advance tax applicability and due dates from incometax.gov.in or with your CA early in the year.

Before submitting the return, reconcile your AIS and Form 26AS: confirm the property transaction and the TDS figure match your records and the sale deed. Any mismatch between what the AIS shows and what your return reports can trigger an automated notice. File through the official income tax e-filing portal at incometax.gov.in.

For high-value sales, inherited property, joint ownership, NRI involvement, or disputed transfers, always work with a qualified chartered accountant — the compliance complexity in these cases goes well beyond standard ITR filing. For a broader preparation list before ITR season, see our ITR filing checklist for salaried employees.

Official Rules and Where to Verify

Capital gains tax on property sale is governed by the Income Tax Act, 1961 and is subject to revision with each Union Budget or government notification. Rates, holding-period rules, exemption limits, CII values, and grandfathering conditions must be confirmed from official sources before filing.

- Income Tax Department — incometax.gov.in

- Press Information Bureau / Ministry of Finance — pib.gov.in

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Final Verdict

Capital gains tax on property sale is one of the largest single tax events most Indian families will ever face — and the difference between short-term and long-term treatment alone can change the bill by several lakh rupees. For property acquired before 23 July 2024, the comparison between 12.5% without indexation and 20% with indexation is not optional: it must be calculated for every eligible resident individual and HUF before filing. Exemptions under Section 54 and 54EC are genuinely powerful tools, but they expire, they have caps, and they require documentation that must be assembled in advance — not after the sale proceeds are spent. Plan the tax before you sign the sale deed, not after. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

Frequently Asked Questions

What is capital gains tax on property sale?

Capital gains tax on property sale is the income tax charged on the profit made from selling a house, flat, plot, or building. The taxable amount is sale consideration minus cost of acquisition, cost of improvement, and allowable transfer expenses — not the full sale price. The rate and available exemptions depend on how long you held the property before selling.

What is the difference between STCG and LTCG on property sale?

STCG (short-term capital gain) applies when property is held for 24 months or less and is taxed at your applicable income slab rate — up to 30% — with no indexation benefit and no access to Section 54 or 54EC exemptions. LTCG (long-term capital gain) applies when property is held for more than 24 months and is generally taxed at 12.5% without indexation, with exemption routes available. The classification hinges entirely on the gap between purchase date and sale date.

What is the holding period for LTCG on property in India?

For immovable property — house, flat, plot, land, or building — the holding period threshold is more than 24 months. Property held for 24 months or less produces STCG. Property held for more than 24 months produces LTCG. Verify the current threshold from incometax.gov.in before filing, since Budget amendments can alter this.

How is long-term capital gain on property taxed after July 2024?

For property transferred on or after 23 July 2024, LTCG is generally taxed at 12.5% without indexation. Eligible resident individuals and HUFs who acquired land or buildings before 23 July 2024 may compare this with the older 20% with-indexation method and use whichever results in lower tax. Surcharge and 4% health and education cess apply on top. Verify the current eligibility conditions for the grandfathered option at incometax.gov.in.

Is indexation benefit still available on property sale?

For transfers on or after 23 July 2024, indexation is not available as the default method. A grandfathered option may allow eligible resident individuals and HUFs to apply 20% with indexation for land or buildings acquired before 23 July 2024. For STCG, indexation has never been available. Confirm the current applicability and eligibility conditions from incometax.gov.in before assuming the grandfathered method applies to your case.

Can Section 54 exemption save tax on property sale?

Yes, Section 54 can reduce or eliminate LTCG tax if you sell a residential house and reinvest the capital gain in purchasing or constructing another residential house within the prescribed timeline. The exemption is capped at the capital gain reinvested. Conditions including investment timing, number of houses owned, lock-in, and documentary proof are strict. Verify the current rules from incometax.gov.in before building a tax plan around this exemption.

What are Section 54EC bonds and when must I invest?

Section 54EC bonds are specified government-backed bonds in which you can invest the long-term capital gain from a property sale to claim exemption. Investment must be made within 6 months of the date of sale — not the ITR due date. There is a monetary cap per financial year (verify the current limit). Bonds carry a lock-in period and cannot be transferred or pledged until the lock-in expires. Confirm eligible bond issuers, the current cap, and lock-in period at incometax.gov.in.

What is the Capital Gains Account Scheme and when should I use it?

The Capital Gains Account Scheme (CGAS) is a designated bank account where you can park the uninvested capital gain or net consideration before your ITR due date, preserving your exemption claim under Section 54 or 54F while the actual reinvestment is still in progress. If you sell property but the new property purchase is not complete by the time your ITR is due, CGAS allows you to demonstrate intent and protect the exemption. Verify the current authorised banks and procedural rules from incometax.gov.in before opening the account.

Is inherited property taxed differently when sold?

Inheritance itself is not taxed under capital gains rules. However, when you eventually sell the inherited property, capital gains tax applies on the profit. The cost of acquisition is generally the original price paid by the previous owner, and the holding period typically includes the original owner’s tenure — meaning many inherited properties qualify as long-term from the date the heir sells. For properties received before a specified reference date, fair market value rules may apply. Verify the applicable rules from incometax.gov.in, especially for gifted property or transfers through a will.

Which ITR form is used for income tax on selling house property?

Salaried individuals with capital gains from property sale must generally use ITR-2 if they have no business income, or ITR-3 if they also have business or professional income. ITR-1 does not have a Schedule CG and cannot be used when a property sale is reported in the AIS. Report full capital gains details in Schedule CG — sale consideration, cost of acquisition, type of gain, applicable rate, and any exemption claimed. File through the official portal at incometax.gov.in.

Do I still owe tax if I reinvest the entire sale amount?

Reinvesting the sale amount does not automatically exempt you from capital gains tax. Exemptions under Section 54, 54EC, and 54F each specify what must be reinvested, how much, within what period, and under which conditions. Section 54, for example, requires reinvestment of the capital gain — not the full sale price — in a qualifying residential house. Tax applies on any portion of the gain not covered by a qualifying exemption. The exemption is not triggered by spending the money — it is triggered by meeting the conditions of the applicable section.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Neha Kulkarni writes about the financial side of home buying, renting, property decisions, and real estate costs in India. Her content helps readers think beyond the EMI and understand the total cost of owning or buying a home.

She covers topics such as rent vs buy, home loan planning, down payment, stamp duty, registration charges, brokerage, maintenance cost, property tax, furnishing cost, home insurance, builder payment plans, resale property checks, home loan affordability, total cost of ownership, and hidden costs in property decisions.

Neha’s writing is practical, family-focused, and cost-conscious. She uses Indian city examples, ₹ calculations, and decision checklists to help readers evaluate whether a property decision fits their income, savings, loan eligibility, and long-term plans. Her articles are useful for first-time home buyers, salaried couples, families, and people comparing rent with home ownership. Since property rules, stamp duty, registration charges, local taxes, home loan rates, and legal requirements vary by state and city, readers should verify current details from official state, lender, and legal sources.