If you sold shares this year, you almost certainly owe some amount of stock market tax in India — but whether it is STCG, LTCG, or just an STT charge on your contract note depends entirely on how you traded and for how long you held the shares. Most investors discover this only when they open their broker’s tax P&L report in March and find four or five line items they have never seen before. Before you reach that point, understanding stock market basics alongside India’s share tax rules will save you both confusion and penalties. This article breaks down STCG, LTCG, STT, intraday tax, and dividend tax clearly — so you can classify your trades, estimate your liability, and file your ITR with confidence.

Quick Answer: Stock Market Tax in India

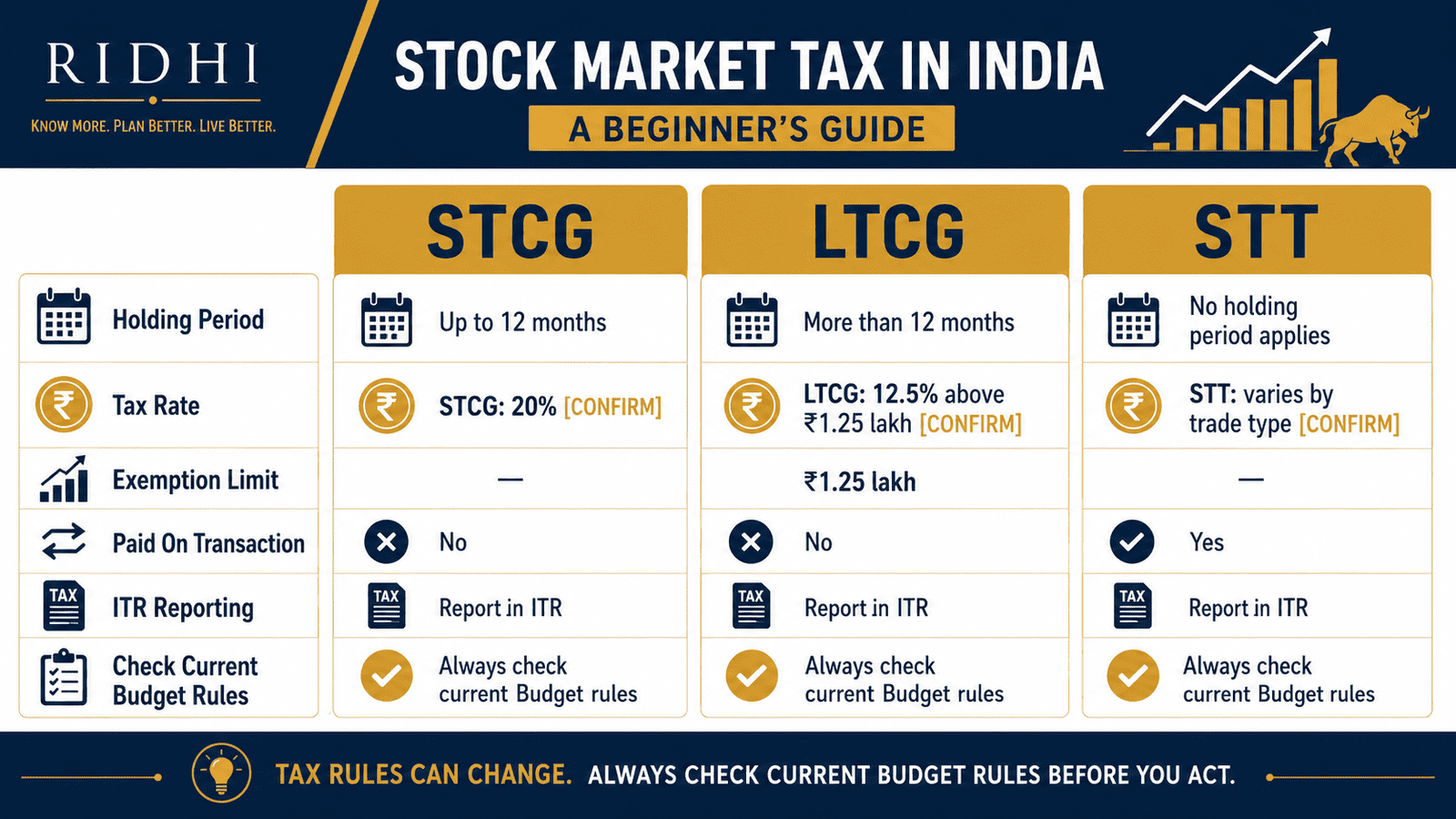

Stock market tax in India includes STCG on short-term listed equity gains, LTCG on long-term listed equity gains, and STT charged on eligible securities transactions. Listed-equity STCG is commonly 20%, while LTCG is commonly 12.5% above ₹1.25 lakh.

Key Takeaways

- Delivery shares held for 12 months or less before selling are taxed as Short-Term Capital Gains (STCG) under Section 111A; shares held beyond 12 months are taxed as Long-Term Capital Gains (LTCG) under Section 112A.

- Listed-equity STCG is commonly taxed at 20% and LTCG at 12.5% on gains above ₹1.25 lakh per financial year — both the rate and exemption limit must be verified for the current assessment year at incometax.gov.in before filing.

- STT (Securities Transaction Tax) is a transaction-level charge applied on eligible stock exchange trades — it is not a profit tax and does not substitute for or reduce your capital gains tax liability.

- Intraday equity trading — buying and selling the same share on the same day without taking delivery — may be classified as speculative business income, not capital gains, and taxed at your income slab rate.

- Dividends received on shares are taxable in your hands as income from other sources at your applicable slab rate — TDS deducted can be claimed as credit when filing your ITR.

- Capital losses can be set off against eligible capital gains and carried forward for up to eight assessment years — but only if you file your ITR on time; verify current rules at incometax.gov.in.

- Budget changes can alter STCG rates, LTCG exemption thresholds, STT rates, and ITR reporting rules — always verify the applicable assessment year’s figures before filing.

Key Facts at a Glance

| Tax / Charge | What It Applies To | Common Rate / Treatment |

|---|---|---|

| STCG — Section 111A | Listed equity shares or equity mutual funds held ≤12 months before sale | 20% of gain (verify current rate before filing) |

| LTCG — Section 112A | Listed equity shares or equity mutual funds held >12 months before sale | 12.5% on gains above ₹1.25 lakh per year (verify rate and exemption before filing) |

| STT — Equity Delivery | Buy and sell legs of delivery-based equity transactions on recognised exchanges | 0.1% of transaction value per leg (verify current schedule before filing) |

| STT — Equity Intraday | Sell leg of intraday equity transactions only | Rate differs from delivery STT — verify current schedule at sebi.gov.in |

| Speculative Business Income | Profit from intraday equity trading (same-day buy-sell, no delivery) | Taxed at your applicable income slab rate — not capital gains |

| Dividend Income | Dividends received from Indian companies on shares held | Added to total income; taxed at your applicable slab rate |

How Stock Market Tax in India Works

Every time you sell a share on a recognised stock exchange, at least two tax-related events happen simultaneously: a Securities Transaction Tax charge is applied at the point of the trade itself, and a capital gain or loss is recorded that you may need to report in your ITR. These two things are entirely separate. Most beginners confuse STT — which appears on every contract note — with income tax. It is not. STT is a transaction charge collected by the government through your broker at the moment of trading. Capital gains tax is an income tax liability that arises only when you have made a profit on a sale.

Every Buy-Sell Creates a Taxable Event

When you buy shares and later sell them for more than you paid, the difference is a capital gain. When you sell for less, it is a capital loss. The type of capital gain — short-term or long-term — depends entirely on how long you held the shares between purchase and sale. Not the amount of profit. Not the broker you use. Not whether any TDS was deducted. Just the holding period.

Holding Period: The Key to STCG vs LTCG for Listed Equity

For listed equity shares traded on a recognised stock exchange, the threshold holding period is 12 months.

- Held 12 months or less — the gain is a Short-Term Capital Gain (STCG) taxed under Section 111A at a commonly applicable rate of 20%.

- Held more than 12 months — the gain is a Long-Term Capital Gain (LTCG) taxed under Section 112A at a commonly applicable rate of 12.5% on the amount exceeding ₹1.25 lakh per financial year across all long-term equity sales.

According to the Income Tax Department (incometax.gov.in), both Section 111A and Section 112A apply specifically to listed equity shares and equity-oriented mutual funds where STT has been paid at the time of sale on a recognised exchange. The 12-month clock starts from the date of purchase — not the settlement date. Your broker’s demat ledger and contract notes are your primary records for establishing purchase dates at filing time. Understanding how those records are generated and stored is essential — the guide on opening a demat account in India explains how contract notes and ledger records are maintained by brokers and depositories.

STT — The Transaction Charge That Is Not Income Tax

Securities Transaction Tax (STT) is levied on transactions in listed securities executed on recognised stock exchanges. It is collected by your broker at the point of the trade and remitted to the government — you never need to calculate or pay it separately. For equity delivery trades, STT is charged on both the buy and sell legs at a commonly applicable rate of 0.1% of the transaction value per leg. For equity intraday trades, STT is charged only on the sell leg at a different rate. F&O, bonds, and other products carry their own STT schedules.

STT appears as a specific line item in every contract note your broker issues. It is a cost of trading — not a credit against your capital gains tax. You cannot deduct the STT you paid from the tax you owe on your share profits. However, for concessional Section 111A and Section 112A rates to apply to your gains, STT must have been paid on the qualifying transactions — so its presence in your contract note is actually a prerequisite for the lower capital gains rates, not just a charge.

Intraday Trading: A Different Tax Classification

If you buy and sell the same share on the same trading day without taking delivery into your demat account, this is intraday equity trading. Under the Income Tax Act, profit from intraday equity trading may be classified as speculative business income — not as capital gains. This distinction matters significantly: speculative business income is added to your total income and taxed at your applicable slab rate, which could be 30% for higher earners versus a commonly applicable 20% STCG rate. Intraday losses can generally only be set off against other speculative income, not against capital gains or salary. If you are unsure whether your trades are delivery-based or intraday, the detailed guide on delivery versus intraday trading — difference, tax, and risk explains the distinction and its filing implications in full.

Dividends: Taxed as Income, Not Capital Gains

Since FY 2020-21, dividends received from Indian companies are fully taxable in the hands of the investor. They are added to your total income under “income from other sources” and taxed at your applicable slab rate. If dividend income from a single company exceeds ₹5,000 in a financial year, TDS may be deducted at source by the company — but this is only a withholding credit you can claim in your ITR, not a final settlement. You must still report all dividend income in your ITR regardless of whether TDS was deducted.

Real Example: Rohan’s Three Share Transactions

Rohan, 31, is a software engineer in Bengaluru earning ₹18 lakh per year. He invests through a discount broker and had three relevant transactions in FY 2024-25.

Transaction 1 — Short-Term Delivery Sale: Rohan bought shares of a listed company in August 2024 for ₹1,00,000 and sold them in January 2025 for ₹1,30,000. Holding period: approximately five months. This is STCG of ₹30,000, taxable at 20% — meaning ₹6,000 in tax before cess and surcharge.

Transaction 2 — Long-Term Delivery Sale: Rohan bought different shares in March 2023 for ₹2,00,000 and sold them in April 2024 for ₹2,90,000. Holding period: over 13 months. This is LTCG of ₹90,000 — which falls below the ₹1.25 lakh annual exemption threshold, so nil LTCG tax is due on this transaction alone for that financial year.

Transaction 3 — STT on Contract Note: For Transaction 1’s sell leg, Rohan notices an STT line item of ₹130 (0.1% of the ₹1,30,000 sale value). This is a transaction cost — not a tax credit. His capital gains tax liability of ₹6,000 on the ₹30,000 STCG is calculated completely separately.

Key insight: Two transactions with similar profit amounts can produce completely different tax outcomes — and a zero-tax outcome in one case — based purely on holding period.

How to Calculate STCG, LTCG, and STT

STCG = Sale Value − Purchase Value − Allowable Transaction Costs

LTCG = Sale Value − Purchase Value (gains above ₹1.25 lakh annual threshold taxed at 12.5%)

STT = Transaction Value × Applicable STT Rate

Using Rohan’s Transaction 1: Sale value ₹1,30,000 minus purchase value ₹1,00,000 = STCG of ₹30,000. Tax at 20% = ₹6,000. Adding 4% health and education cess = ₹240. Total approximate tax: ₹6,240 before surcharge. STT on the sell leg: ₹1,30,000 × 0.1% = ₹130 — a separate transaction cost.

If Rohan had accumulated ₹2,00,000 in total LTCG across all long-term equity sales in the same year, his taxable LTCG would be ₹2,00,000 − ₹1,25,000 = ₹75,000. At 12.5%, the tax would be ₹9,375 before cess.

To see how capital gains interact with your salary income and estimate your combined tax liability, the income tax calculator for FY 2025-26 can help you build a full picture — though it does not replace accurate ITR filing with a professional for complex cases.

| Scenario | Key Inputs | Approximate Tax |

|---|---|---|

| STCG of ₹30,000 | 20% rate; no exemption threshold applies | ₹6,000 + 4% cess = ₹6,240 |

| LTCG of ₹2,00,000 total annual gains | 12.5% on ₹75,000 (after ₹1.25L exemption) | ₹9,375 + 4% cess = ₹9,750 |

| LTCG of ₹1,00,000 total annual gains | ₹1.25L exemption covers the full gain | Nil LTCG tax due |

Comparison: STCG vs LTCG vs STT vs Intraday vs Dividend

The table below maps each tax type to the transaction it applies to and its common treatment — making it easier to classify what you owe before you file. For a detailed walkthrough of the delivery versus intraday distinction and its full tax implications, see the guide on intraday versus delivery trading — difference, tax, and risk.

| Type | When It Applies | Rate / Treatment |

|---|---|---|

| STCG — Section 111A | Listed equity held ≤12 months, then sold on a recognised exchange with STT paid | 20% — verify before filing |

| LTCG — Section 112A | Listed equity held >12 months, then sold on a recognised exchange with STT paid | 12.5% on gains above ₹1.25L — verify |

| STT | Any eligible buy or sell of securities on a recognised exchange | Transaction charge — not a profit tax |

| Intraday Equity Profit | Same-day buy and sell of equity, no delivery taken | Slab rate — speculative business income |

| Dividend Income | Dividends received from Indian listed companies | Slab rate — income from other sources |

How to Decide What’s Right for You

You sold delivery shares within 12 months of the purchase date — THEN your gain is STCG and is taxable at the applicable Section 111A rate; report it in the capital gains schedule of your ITR-2.

You held delivery shares for more than 12 months before selling — THEN your gain is LTCG, and the first ₹1.25 lakh of aggregate long-term equity gains across the financial year is exempt; only the amount above that threshold is taxed.

You see an STT charge in your contract note — THEN acknowledge it as a transaction cost; it does not reduce, replace, or count against your capital gains tax liability for that trade.

You bought and sold the same share on the same day without taking delivery — THEN your profit is likely speculative business income, not capital gains; use ITR-3 and verify the classification with a tax professional before filing.

Your cumulative long-term equity gains for the financial year are below ₹1.25 lakh — THEN no LTCG tax is due on those gains; still report the transactions in your ITR capital gains schedule.

You received dividends — THEN add the total amount to your income from other sources in your ITR; claim any TDS deducted as credit against your final tax liability.

You are a frequent trader with a high volume of intraday, F&O, or complex multi-product transactions — the simple delivery-based framework in this article may not be sufficient; your tax situation may involve business income classification, turnover calculations, or a tax audit requirement that needs professional advice.

Common Mistakes to Avoid

Treating STT as Income Tax Already Paid

STT is a transaction-level charge deducted at the point of trade — it is not income tax and cannot be set off against your capital gains tax liability.

Many beginners assume that because STT appeared on every contract note, no further tax is owed on their trading profits. On a ₹30,000 STCG, your tax liability at 20% is ₹6,000 — irrespective of the ₹130 in STT already paid on that transaction. These are entirely separate obligations.

Always treat STT as a trading cost in your records and calculate capital gains tax independently from it.

Ignoring Short-Term Gains Because No TDS Was Deducted

Unlike salary income, brokers do not deduct TDS on capital gains for resident individual investors. This means the full amount of your STCG and LTCG tax liability falls on you to calculate, declare, and pay.

If your total tax payable — salary plus capital gains — exceeds your TDS credits by more than ₹10,000 in a financial year, you are required to pay advance tax in installments. Missing advance tax deadlines attracts interest under Sections 234B and 234C. The guide on advance tax — who needs to pay and how to calculate it explains exactly when this obligation kicks in and how to meet it.

Calculate your estimated capital gains tax before the March 15 advance tax deadline each year — not after.

Confusing Intraday Profit with Short-Term Capital Gains

Intraday equity profit may be classified as speculative business income — taxed at your slab rate — not as STCG at the concessional 20% rate.

If your slab rate is 30% and you mistakenly apply 20% to intraday gains, you understate your tax liability. Using the wrong ITR form or the wrong income head for intraday income is also a common reason the Income Tax Department issues defective return notices to retail investors.

Classify your trades clearly: delivery-based purchases and sales go in the capital gains schedule; intraday trades go in business income.

Forgetting Capital Loss Set-Off and Carry-Forward

If you made losses on share sales, they can be set off against eligible capital gains — reducing your tax outgo for the year.

Short-term capital losses can typically be set off against both STCG and LTCG. Long-term capital losses can generally be set off only against LTCG. Unused capital losses can be carried forward for up to eight assessment years — but only if your ITR is filed by the due date. Missing the deadline forfeits the carry-forward right entirely.

Report all capital losses in your ITR capital gains schedule, even when no tax is owed for that year.

Not Reconciling Your Broker Statement with AIS and Form 26AS

Your Annual Information Statement (AIS) and Form 26AS on incometax.gov.in reflect transaction data reported by your broker to the Income Tax Department. If there is a mismatch between your broker’s tax P&L report and your AIS figures, the ITR will show a discrepancy that can trigger an automated notice.

Before filing, cross-check every sale transaction in your broker report against your AIS. Report discrepancies to your broker first, then file accurate figures supported by your contract notes.

Filing ITR-1 When Capital Gains Require ITR-2 or ITR-3

ITR-1 is for salaried employees with income only from salary, one house property, and interest. If you have any capital gains — even a single share sale — you cannot file ITR-1. Capital gains require ITR-2 at minimum; F&O or intraday business income requires ITR-3.

Filing the wrong form is treated as a defective return, can be rejected, and may result in scrutiny. Verify the correct ITR form for your income profile and the current assessment year on incometax.gov.in before filing.

When This May Not Be the Right Choice

This article’s framework works well for most salaried investors in India who buy and hold listed equity shares or equity-oriented mutual funds on recognised exchanges. However, it may not be sufficient in the following situations:

Frequent traders and F&O participants: If you trade futures, options, or carry a high volume of intraday positions, your income may be classified as business income — with turnover-based calculations, potential tax audit requirements, and different ITR filing obligations that go beyond this article’s scope.

NRIs and foreign investors: Non-resident Indians and foreign portfolio investors face different TDS rates, applicable tax treaty benefits, and repatriation rules that require jurisdiction-specific professional advice.

ESOPs and unlisted shares: Employee stock options and shares in unlisted companies carry different holding period thresholds, valuation methodologies, and perquisite taxation rules not covered here.

High-value gains with surcharge impact: If your total income significantly exceeds basic threshold levels, a surcharge may apply on top of capital gains tax — materially increasing your effective liability beyond the headline rates referenced in this article.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Stock market tax rules in India — including STCG rates under Section 111A, LTCG exemption limits and rates under Section 112A, STT schedules, and ITR reporting requirements — are set by the government and can be revised with each Union Budget. The figures used in this article are based on rules applicable as of the knowledge date and must be verified for the current assessment year before filing.

- Income Tax Department: incometax.gov.in — for capital gains rules, Section 111A, Section 112A, applicable ITR forms, AIS, Form 26AS, and current tax slabs and rates.

- SEBI: sebi.gov.in — for investor protection guidelines, exchange-related regulations, and STT schedule context.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Before filing your ITR, use the ITR filing checklist for salaried employees to ensure you have collected all required documents — including your broker’s capital gains report, contract notes, AIS download, and Form 26AS — before you begin entering figures in your return.

Expert Tips

- Download your broker’s capital gains report in April, not March: Most discount brokers generate a clean annual capital gains summary only after April 1 for the completed financial year. Attempting to reconstruct it manually from individual contract notes is both error-prone and unnecessary — wait for the official P&L statement.

- Cross-check every sale transaction in AIS before filing: Log in to incometax.gov.in, open your Annual Information Statement, and compare every equity sale entry against your broker statement. Discrepancies between the two are a leading cause of ITR notices for retail investors — address them with your broker before filing.

- Separate your delivery investment records from your intraday trading records from day one: If you run both investment and intraday positions in the same broker account, maintain separate tags or folders for each — so that capital gains and speculative income are not mixed at year-end when filing.

- Calculate advance tax before March 15 if your gains are significant: If your total income tax liability — salary plus capital gains — exceeds what your employer’s TDS covers by more than ₹10,000, advance tax instalments are mandatory. Interest under Sections 234B and 234C applies to shortfalls — estimate early, not late.

- Never discard a contract note: Contract notes are your primary legal proof of a stock transaction’s date, price, and STT paid — all of which matter at the time of ITR filing or tax scrutiny. Store them digitally, organised by broker and financial year, for at least six assessment years.

- If your cumulative LTCG is approaching ₹1.25 lakh for the year, review your positions before March 31: Gains within the annual exemption threshold attract nil LTCG tax. If you are close to but under the limit, consider whether harvesting additional long-term gains makes sense — then verify the current exemption limit and tax implications with a professional before acting.

Frequently Asked Questions

Is STT refundable?

No. Securities Transaction Tax is collected by the government through your broker at the point of trade and is non-refundable under any circumstances. It is a transaction cost — similar to brokerage — not an advance income tax payment you can claim back in your ITR.

Is STT the same as income tax on capital gains?

No. STT and capital gains tax are completely separate obligations. STT is a transaction-level charge on eligible securities trades, deducted at source by your broker. Capital gains tax under the Income Tax Act is a liability that arises on the profit you made — and is calculated independently of STT paid. Paying STT does not reduce your capital gains tax in any way.

How is STCG tax on shares calculated?

Short-term capital gain equals sale value minus purchase value minus allowable transaction costs. That net gain is then taxed at the applicable STCG rate under Section 111A. A commonly referenced rate is 20% for listed equity shares. Always verify the current rate for the relevant assessment year at incometax.gov.in before filing — this rate has been revised in recent Budgets.

How is LTCG tax on shares calculated?

Long-term capital gain equals sale value minus purchase value. If your total LTCG across all long-term equity sales in the financial year exceeds the annual exemption threshold — commonly ₹1.25 lakh — the amount above that threshold is taxed at the applicable Section 112A rate, commonly 12.5%. Both the exemption limit and the tax rate must be verified for the current assessment year before filing.

Is intraday trading profit taxed as capital gains?

Generally no. Profit from intraday equity trading — where you buy and sell the same share within the same session without taking delivery — may be classified as speculative business income under the Income Tax Act. This is taxed at your applicable income slab rate, not at the concessional STCG rate. If you do both delivery investing and intraday trading, you will have both capital gains and business income to report in your ITR.

Which ITR form do I use for stock market gains?

If you are a salaried individual with capital gains from listed equity shares, you generally need to file ITR-2 — not ITR-1. If you also have intraday equity profit or F&O income, you will typically need ITR-3. Verify the correct ITR form for your specific income profile and the current assessment year on incometax.gov.in before filing — using the wrong form results in a defective return.

Do I pay tax if I made a capital loss on shares?

No income tax is due on a capital loss. However, you should still report every loss in your ITR capital gains schedule — capital losses can be set off against eligible gains and carried forward for up to eight assessment years. You can only carry forward losses if you file your ITR by the due date for the year the loss arose. Missing the deadline forfeits the carry-forward right permanently.

Are dividends received on shares taxable in India?

Yes. Since FY 2020-21, all dividends received from Indian companies are taxable in your hands. They are added to your total income as “income from other sources” and taxed at your applicable slab rate. If your dividend income from a single company exceeds ₹5,000 in a financial year, TDS may be deducted at source — claim it as credit when filing your ITR. You must report all dividend income regardless of whether TDS was deducted.

Can I set off short-term capital losses against long-term capital gains?

Yes. Short-term capital losses can generally be set off against both short-term and long-term capital gains in the same year. Long-term capital losses can typically be set off only against long-term capital gains. Verify the current set-off rules for the relevant assessment year at incometax.gov.in — these provisions have been updated in recent Budgets and the applicable rules depend on the assessment year you are filing for.

What assessment year applies to income from FY 2024-25?

Income earned during Financial Year 2024-25 (April 2024 to March 2025) is reported and assessed in Assessment Year 2025-26. Always confirm the correct assessment year when downloading your AIS, Form 26AS, or referring to tax rate schedules — using the wrong year when selecting your ITR or checking rates is a common and avoidable error.

Final Verdict

Stock market tax in India is manageable once you understand three things clearly: what type of trade you made, how long you held the asset, and whether your profit falls under capital gains or business income. STCG, LTCG, and STT are separate concepts with different rules — treating any two of them as the same will lead to an incorrect ITR. For most salaried investors using a discount broker for delivery-based equity investing, the core framework is straightforward: classify by holding period, track gains against the annual LTCG exemption, reconcile your broker statement against AIS, and use the right ITR form. For anything more complex — intraday trades, F&O, ESOPs, NRI status, or significant loss positions — professional filing support is worth the cost. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Devika Shah writes about stock market basics for Indian beginners who want to understand equity investing before taking financial risk. Her content is educational and does not provide stock tips, trading calls, price predictions, or personalised investment advice.

She covers topics such as demat account meaning, trading account basics, IPOs, dividends, brokerage charges, delivery vs intraday trading, market orders, limit orders, stock indices, blue-chip stocks, capital gains tax, stock market terminology, risk management, and the difference between long-term investing and short-term speculation.

Devika’s writing is clear, balanced, and risk-conscious. She helps readers understand how the stock market works, what accounts and documents are needed, what charges may apply, and what mistakes beginners should avoid. Her articles are suitable for students, salaried employees, and first-time investors who want a foundation before investing. Since market rules, tax treatment, brokerage fees, IPO processes, and regulatory requirements can change, readers should verify current information from SEBI, exchanges, brokers, and official tax sources.