Every SIP calculator gives you a projected maturity value — but that number only means something if you understand the assumed return behind it. If you are planning to invest ₹5,000 per month in a mutual fund for 10 years, this article runs the calculation at 8%, 10%, and 12% annual return assumptions and shows exactly what each scenario produces: the maturity amount, the total gain, and the difference between them. More importantly, it explains what a SIP projection actually is — and what it is not. These are mathematical estimates, not guaranteed outcomes. Markets can deliver more and they can deliver less. The goal here is to give you the clearest, most honest version of this calculation so you can use it as a planning tool, not a return promise.

Quick Answer: SIP Calculator — ₹5,000 Monthly for 10 Years

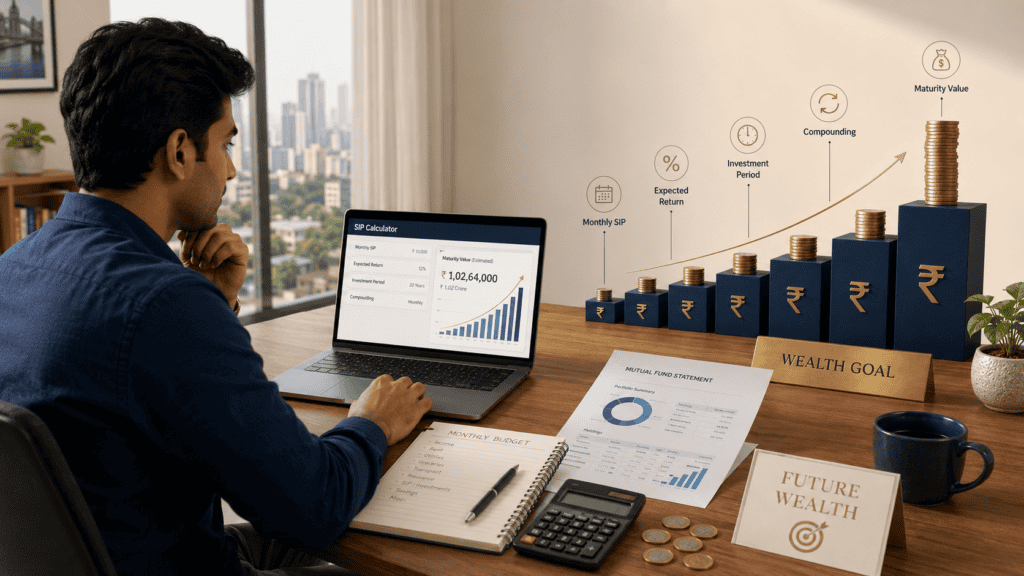

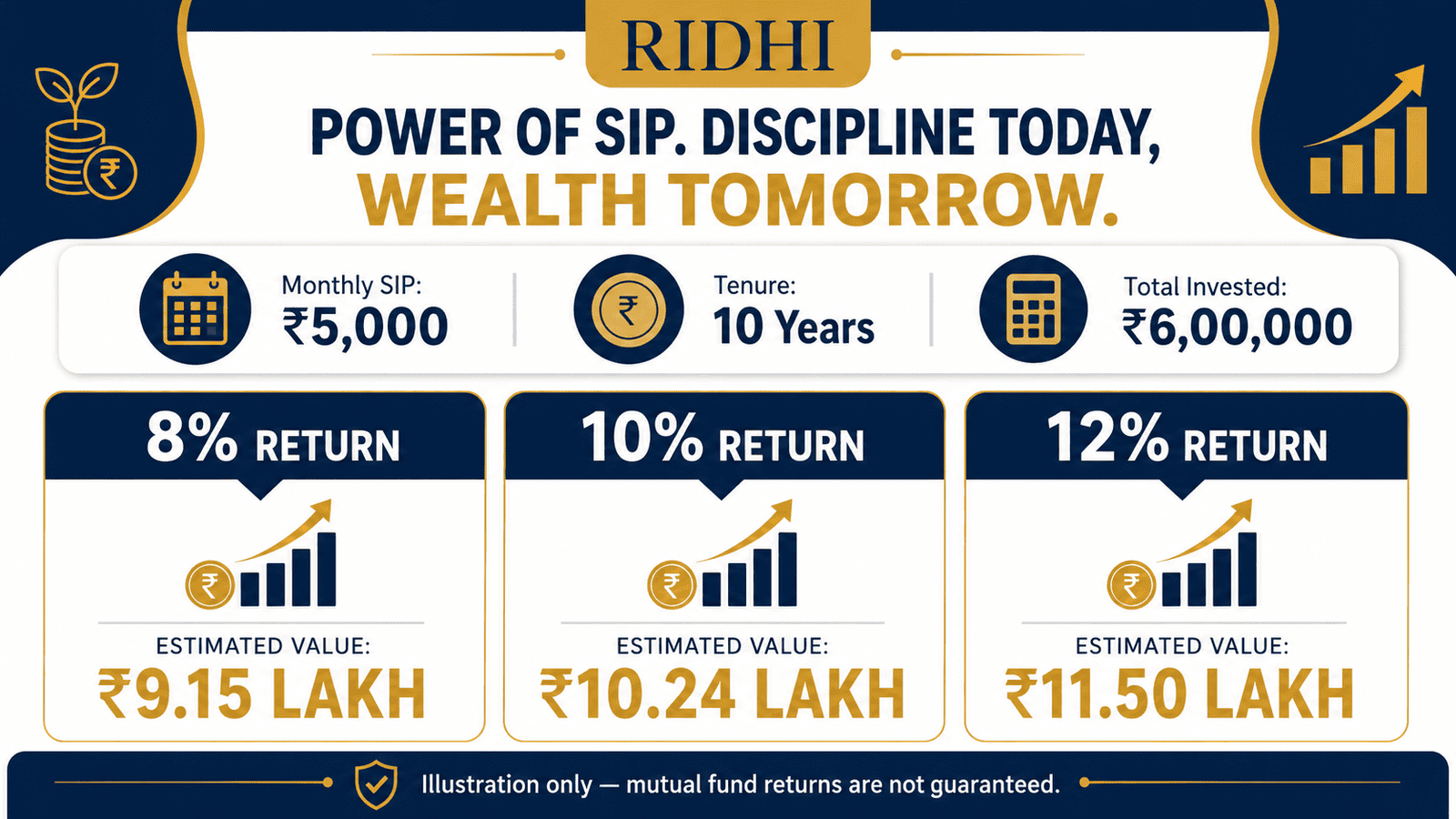

SIP calculator helps estimate how a ₹5,000 monthly SIP may grow over 10 years using assumed annual returns. At 8%, 10%, and 12%, the estimated maturity values are about ₹9.21 lakh, ₹10.33 lakh, and ₹11.62 lakh respectively, before tax or fund costs.

How to Calculate: ₹5,000 Monthly SIP Over 10 Years

SIP Maturity Value = P × [{(1 + r)^n – 1} / r] × (1 + r)

Where: P = monthly SIP amount | r = monthly interest rate (annual rate ÷ 12) | n = total number of months

Applying this formula to a ₹5,000 monthly SIP at 10% assumed annual return:

- P = ₹5,000

- r = 10% ÷ 12 = 0.00833 per month

- n = 10 years × 12 = 120 months

- Estimated maturity ≈ ₹10,33,000

Total amount invested over 120 months = ₹5,000 × 120 = ₹6,00,000. The estimated gain at 10% is approximately ₹4,33,000 — entirely from compounding on a consistent monthly investment, with no increase in the monthly amount.

| Scenario (Assumed Annual Return) | Key Inputs | Estimated Maturity Value |

|---|---|---|

| 8% per year | ₹5,000/month × 120 months = ₹6,00,000 invested | ₹9.21 lakh |

| 10% per year | ₹5,000/month × 120 months = ₹6,00,000 invested | ₹10.33 lakh |

| 12% per year | ₹5,000/month × 120 months = ₹6,00,000 invested | ₹11.62 lakh |

These are illustrative estimates based on assumed constant annual returns. Actual mutual fund returns vary with market conditions and are not guaranteed. To test different SIP amounts, return rates, and tenures interactively, use Ridhi’s monthly investment calculator.

Key Takeaways

- A ₹5,000 monthly SIP over 10 years means a total capital investment of ₹6,00,000 across 120 instalments — the maturity value is everything above that.

- At 8% assumed return, the estimated maturity is ₹9.21 lakh — a gain of ₹3.21 lakh over the invested amount, purely from compounding.

- At 12% assumed return, the estimated maturity rises to ₹11.62 lakh — a gain of ₹5.62 lakh, which is ₹2.41 lakh more than the 8% scenario despite the same monthly investment.

- The ₹2.41 lakh difference between the 8% and 12% outcomes comes entirely from the higher assumed return compounding over 120 months — not from investing more money.

- 12% is not a guaranteed or typical return for any specific mutual fund — it is an illustrative assumption; equity funds can return significantly more or less over any given 10-year period.

- A standard SIP calculator does not factor in expense ratio, exit load, capital gains tax, or the impact of pausing or stopping your SIP — all of which reduce the actual amount you receive.

Key Facts at a Glance

| Parameter | Value | Note |

|---|---|---|

| Monthly SIP amount | ₹5,000 | Fixed across all three scenarios |

| Investment period | 10 years (120 months) | Illustrative assumption only |

| Total amount invested | ₹6,00,000 | ₹5,000 × 120 instalments |

| Return assumptions used | 8%, 10%, 12% per annum | Illustrative assumptions only |

| Estimated corpus range | ₹9.21 lakh – ₹11.62 lakh | Varies with assumed return rate |

What a SIP Calculator Does — and What It Cannot Do

A Systematic Investment Plan, or SIP, is a method of investing a fixed amount into a mutual fund scheme at regular intervals — typically monthly. Instead of timing the market with a large lump sum, you invest a smaller amount consistently, month after month. Over time, this builds financial discipline and benefits from rupee cost averaging: you buy more mutual fund units when prices are low and fewer units when prices are high, smoothing your average purchase cost over the investment period.

What the calculator actually computes

A SIP calculator is a mathematical estimation tool. You provide three inputs — monthly amount, tenure in years, and an assumed annual return — and it applies the standard SIP compounding formula to produce a projected maturity value. That is all the calculator does.

It does not know which fund you will choose. It does not use the fund’s actual historical performance or account for the fund’s expense ratio, any exit load applicable on early redemption, or the tax on capital gains at the time of withdrawal. It also does not model the very common scenario of an investor skipping or stopping instalments during a market correction — which meaningfully reduces the final corpus compared to the calculator’s projection.

Where the 8%, 10%, and 12% figures come from

These are standard planning assumptions used for illustration in India. They are not endorsed by SEBI or any regulator as guaranteed outcomes. Broadly:

- 8% is a conservative assumption, sometimes used for debt-oriented or hybrid fund scenarios, or as a cautious equity estimate for shorter timeframes.

- 10% is a commonly used moderate assumption for diversified large-cap equity mutual funds over a 10-year horizon in India.

- 12% reflects an optimistic but historically observed range for some equity funds over long periods — not a guaranteed benchmark.

According to SEBI disclosure requirements, all mutual fund communications must clearly state that past performance does not guarantee future returns. Mutual fund investments are subject to market risks. Past performance does not guarantee future returns. This is not a technicality — it reflects the reality that equity fund returns vary considerably across different market cycles. A fund that delivered 14% CAGR in one decade may return 7% in the next, depending on valuations, economic conditions, and sector performance.

Why compounding makes the return assumption so important

The gap between ₹9.21 lakh at 8% and ₹11.62 lakh at 12% represents a 26% difference in the final corpus — from the same ₹6,00,000 investment over the same 10 years. That gap grows further over longer horizons: a 20-year SIP at ₹5,000/month would show a difference of over ₹20 lakh between 8% and 12% scenarios, driven entirely by the higher assumed rate compounding monthly over more periods.

Understanding what you are actually investing in before reading any projection is essential. For a clear foundation, read our guide on mutual fund basics before using any SIP estimate for financial planning.

Real Example: Rohan Starts His First SIP in Pune

Rohan is 29, a software analyst in Pune earning ₹85,000 per month. After reviewing his monthly budget — rent, EMIs, groceries, and an emergency fund contribution — he decides he can comfortably set aside ₹5,000 per month without straining his cash flow.

He opens a SIP calculator and types in ₹5,000, 10 years, and 10% return. The result shows ₹10,33,000. He pauses: he is putting in ₹60,000 a year — ₹6,00,000 total over the decade — and the estimate shows nearly ₹4.33 lakh more than his investment. He runs it at 8% and gets ₹9.21 lakh; at 12%, ₹11.62 lakh.

Rohan then wonders whether an FD might be safer. A lump sum of ₹6 lakh invested in an FD at 7% would return roughly ₹11.8 lakh after 10 years — but that requires having ₹6 lakh available today. The SIP requires only ₹5,000 to start.

His key insight: ₹5,000 is just 5.9% of his monthly salary. Starting with an amount he can sustain without interruption is far more valuable than starting with a larger amount he might pause during a rough month. The uninterrupted 10-year compounding is what drives the outcome — not the return assumption alone. To understand exactly what happens each month when your instalment gets invested, read our full guide on how SIP works.

Comparison: 8% vs 10% vs 12% Return Scenarios

| Assumed Annual Return | Estimated 10-Year Maturity | Estimated Gain Over ₹6 Lakh Invested |

|---|---|---|

| 8% per year | ₹9.21 lakh | ₹3.21 lakh |

| 10% per year | ₹10.33 lakh | ₹4.33 lakh |

| 12% per year | ₹11.62 lakh | ₹5.62 lakh |

The ₹2.41 lakh difference between the 8% and 12% outcomes comes entirely from compounding at a higher assumed rate over 120 months — not from investing more money each month. However, a higher expected return assumption typically corresponds to higher market risk. Equity funds capable of delivering 12% over 10 years can also produce significantly negative short-term returns during bear markets. These numbers are planning benchmarks, not outcome guarantees.

How to Decide What’s Right for You

Running the numbers is straightforward. Using them responsibly is the part that takes judgment. Here are practical if/then decisions to guide your interpretation:

your goal is 10 or more years away — THEN using a 10% assumption as your moderate planning estimate for a diversified equity SIP is broadly reasonable, not as a guarantee but as a working benchmark.

your goal is 5 years or fewer — THEN use 8% or lower and consider whether equity mutual funds are even appropriate for that timeline, given short-term volatility risk.

you are investing for a non-negotiable goal such as a child’s college admission fee or a wedding — THEN use the 8% scenario as your base, add a 10–15% buffer to your target corpus, and consider whether pure equity exposure is appropriate.

you are comparing two SIP projections from different sources — THEN always verify both are using the same assumed return and the same tenure before drawing conclusions; a 12% projection over 15 years is not comparable with a 10% projection over 10 years.

you want to understand your actual fund’s projected performance, not just a calculator output — THEN CAGR and XIRR are the metrics that matter for real fund assessment; read our explainer on fund return methods to understand the difference between these measures.

you are comfortable with your invested amount temporarily losing 20–30% of its value during a market downturn without withdrawing — THEN equity SIPs with 10%–12% return assumptions are not suited for you, regardless of what the long-term projection shows.

Common Mistakes to Avoid

Treating 12% as a Guaranteed or Typical Return

12% in a SIP calculator is a mathematical input that you choose — no fund house, regulator, or financial product guarantees it.

Indian equity mutual funds have delivered returns ranging from negative to over 20% CAGR in different 10-year periods depending on market conditions. The same fund can return 15% in one decade and 8% in the next.

Use 12% as a best-case planning scenario only. Build your essential financial goals around 8% or 10%.

Ignoring the Expense Ratio

Every mutual fund charges an annual total expense ratio (TER) — typically 0.5% to 1.5% for equity funds, depending on whether you hold a direct or regular plan.

On a ₹10 lakh projected corpus, a 1% difference in annual TER can reduce your effective maturity value by ₹40,000–₹60,000 over 10 years through reduced compounding.

Always check the TER of the specific scheme in its Scheme Information Document before investing.

Ignoring Capital Gains Tax on Redemption

The SIP calculator shows a pre-tax maturity value. Long-term capital gains on equity mutual funds above ₹1.25 lakh per financial year are taxed at 12.5% without indexation benefit.

On a ₹5.62 lakh gain at 12% return, the applicable LTCG tax could reduce your take-home amount meaningfully. Factor in tax treatment when calculating how much you will actually receive.

Plan your redemption in phases where possible to stay within the annual exemption limit.

Stopping the SIP During a Market Correction

Many first-time investors pause or cancel their SIP when markets fall 15–20%, fearing further losses.

Stopping during a correction destroys the rupee cost averaging benefit — you were buying more units at lower prices, which is exactly when compounding works hardest for you. Interrupting the SIP at this point locks in a lower unit count.

Set an auto-debit and avoid checking NAV movements more than once a month.

Comparing SIP Maturity Directly with Fixed Deposit Maturity

A SIP projects growth under assumed market-linked returns. An FD guarantees a fixed return on a lump sum. They carry different risk profiles, tax treatments, and liquidity terms. A direct maturity comparison without accounting for these differences misleads more than it informs.

Choosing a Fund Based on the Past One-Year Return

A fund that returned 35% last year may have done so in a narrow bull-market window that will not repeat. SEBI requires disclosures stating past performance does not guarantee future returns precisely because one-year performance is not a predictor of long-term outcomes. Review rolling returns and consistency over 5–7 year periods before making a fund selection.

When This May Not Be the Right Choice

A 10-year equity mutual fund SIP is not suited for every investor or every financial situation:

- Short-term goals (under 3 years): If you need the money within 3 years — for a car purchase, a home down payment, or near-term education fees — equity SIP carries short-term volatility that can significantly erode capital at the point of withdrawal.

- Very low risk tolerance: If a 20–30% temporary drop in your portfolio value would cause you to panic-withdraw or lose sleep, equity SIPs are not suitable for you regardless of their long-term return assumptions.

- No emergency fund in place: Without 3–6 months of expenses in a liquid savings account or liquid fund, a financial shock could force you to break your SIP — eliminating the compounding benefit and potentially incurring exit loads.

- Requirement for guaranteed returns on a fixed date: If you need a specific amount available on a known future date with certainty, market-linked SIPs cannot provide that assurance. PPF, FD, or short-duration debt instruments are more appropriate for such goals.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Mutual funds in India are regulated by the Securities and Exchange Board of India (SEBI). Before investing in any mutual fund scheme, you should:

- Read the Scheme Information Document (SID) for the specific fund, available on the fund house’s website.

- Check the fund’s risk-o-meter — SEBI mandates that every scheme display its risk level using a standardised scale.

- Verify the fund’s expense ratio, benchmark index, category, and fund manager track record directly from the fund house or AMFI’s mutual fund portal at amfiindia.com.

- Confirm tax treatment of gains from the Income Tax Act provisions applicable to your fund type and holding period.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- SEBI (Securities and Exchange Board of India) — sebi.gov.in

Expert Tips

- Start with an amount you will never miss: A ₹5,000 SIP that runs uninterrupted for 10 years delivers a materially better outcome than a ₹10,000 SIP paused twice during corrections. Consistency over 120 months matters more than the starting amount. Start where your budget is comfortable, not where your ambition is.

- Increase your SIP amount gradually as income grows: If your salary rises 6–8% annually, adding even ₹500 to your monthly SIP each year significantly boosts the 10-year corpus through step-up compounding. Read how increasing your SIP yearly works before setting up your first instalment.

- Use the 8% scenario for all non-negotiable goals: For a child’s school fees, a home loan down payment, or any goal with a fixed target date, model the 10-year projection at 8%. Treat anything above ₹9.21 lakh as upside — not your baseline expectation.

- Choose direct plans over regular plans where you can manage your own investments: Direct plans have lower expense ratios — often 0.5% to 1% less per year than regular plans. On a ₹5,000 monthly SIP over 10 years, that difference compounds into a meaningfully higher corpus. Understand the full trade-off between direct and regular plans before choosing where to invest.

- Review once a year — not once a week: SIP works through long-horizon compounding, not through short-term NAV movements. Set a calendar reminder each April: compare your fund’s 3-year rolling return against its benchmark and category peers. That annual review is all the monitoring a SIP investor needs.

- Run all three scenarios before deciding your target corpus: Model 8%, 10%, and 12% for each of your goals separately. This gives you a realistic range — a floor, a middle ground, and a ceiling — rather than a single number to chase. Planning with a range is more honest than planning with a point estimate.

Frequently Asked Questions

How much will a ₹5,000 monthly SIP become in 10 years?

Using the standard SIP compounding formula, the estimated maturity at 8% assumed annual return is approximately ₹9.21 lakh, at 10% it is approximately ₹10.33 lakh, and at 12% it is approximately ₹11.62 lakh. Total capital invested across all three scenarios is ₹6,00,000. These are calculator estimates, not guaranteed amounts — actual mutual fund returns are market-linked and will differ.

Is a 12% SIP return guaranteed?

No. 12% is an assumed annual return that you enter into the calculator for illustration purposes — no mutual fund, regulator, or financial institution guarantees it. SEBI requires all mutual fund communications to state clearly that past performance does not guarantee future returns. Equity funds can return significantly more than 12% or significantly less, depending on the market cycle and fund category.

Is ₹5,000 per month a good amount to start a SIP with?

For most salaried beginners, ₹5,000 per month is a practical and sustainable starting point. The more important consideration is that the amount does not disrupt your monthly cash flow or emergency fund. A ₹5,000 SIP maintained without interruption for 10 years produces a better outcome than a ₹10,000 SIP started and paused repeatedly. Start at a level you can commit to for the full tenure.

Which return assumption should I use in a SIP calculator?

For goals that are 10 or more years away, 10% is a commonly used moderate assumption for diversified equity mutual funds in India. Use 8% if the goal is critical and you prefer a conservative estimate. Use 12% only as an optimistic best-case scenario. Do not use 12% as your base planning figure for essential financial goals where you cannot afford a shortfall.

Does the SIP calculator include tax and expense ratio?

Standard SIP calculators do not account for the fund’s expense ratio, any exit load on early redemption, or capital gains tax on withdrawal. The maturity value shown is a pre-cost, pre-tax estimate. For equity mutual funds held for more than one year, long-term capital gains above ₹1.25 lakh per financial year are taxable. The actual amount you receive in hand will be lower than the calculator’s projection once these costs are applied.

What is the total amount invested in a ₹5,000 monthly SIP over 10 years?

₹5,000 × 12 months × 10 years = ₹6,00,000. This is your total capital invested. Every rupee above ₹6,00,000 in the maturity value represents your estimated gain from compounding — provided the fund’s actual returns stay close to the assumed rate over the full period.

Can I start a ₹5,000 SIP in any mutual fund in India?

Most mutual fund schemes in India allow SIPs starting from ₹500 to ₹1,000 per month, so ₹5,000 exceeds the minimum requirement for the vast majority of equity funds. You can initiate a SIP directly through a fund house’s official website, through AMFI-registered platforms, or through a SEBI-registered investment adviser. Always check the minimum SIP instalment amount for the specific scheme in its Scheme Information Document before registering.

What happens if I stop my SIP before completing 10 years?

When you stop a SIP, your existing units remain invested and continue to grow or decline with the fund’s performance — you do not lose what you have already accumulated. However, the compounding benefit is severely reduced because new monthly investments stop. If you stop at 5 years instead of 10, your total invested amount drops from ₹6,00,000 to ₹3,00,000 and the estimated corpus at 10% falls from ₹10.33 lakh to roughly ₹3.87 lakh at the 5-year mark — illustrating how tenure is one of the most powerful variables in a SIP outcome.

Final Verdict

A ₹5,000 monthly SIP over 10 years is a disciplined, beginner-accessible way to build a meaningful corpus from a modest monthly commitment. The estimated range of ₹9.21 lakh to ₹11.62 lakh across the 8%, 10%, and 12% return assumptions clearly demonstrates the power of compounding — the same ₹6,00,000 invested at different assumed rates produces a ₹2.41 lakh difference in outcome without any change in the monthly amount. The SIP calculator is a planning reference, not a return promise. What determines your actual outcome is the fund category you choose, the expense ratio you pay, your investment tenure, your ability to stay invested during corrections, and your tax situation at redemption — not which number looks best on a calculator screen. Use these projections to set realistic goal-based targets and test multiple scenarios before deciding. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Arjun Kapoor writes about mutual funds, SIPs, ELSS, fund categories, investment returns, and beginner investing concepts for Indian readers. His focus is on education, not product promotion or fund recommendations. He helps readers understand how mutual funds work before they start investing or comparing schemes.

He covers topics such as mutual fund meaning, SIP meaning, SIP calculator, direct mutual funds vs regular plans, NAV, ELSS tax-saving funds, CAGR, absolute returns, XIRR, expense ratio, large cap vs mid cap vs small cap funds, flexi cap funds, index funds vs active funds, liquid funds, debt mutual funds, SIP pause vs SIP stop, lumpsum vs SIP, and how to start SIP in India.

Arjun’s writing is simple, risk-aware, and long-term oriented. He avoids guaranteed-return language and explains investment concepts using examples, timelines, and comparison tables. His articles remind readers that mutual fund investments are subject to market risks, and past performance does not guarantee future returns. Readers should verify scheme details from SEBI, AMFI, fund houses, and official scheme documents.