Most salaried employees in India have EPF running quietly in the background — but that alone rarely builds a complete retirement plan. The NPS vs EPF vs PPF calculator question comes up because many employees realise, somewhere in their 30s, that salary-linked EPF may not be enough and they need to decide whether to add PPF, NPS, or both as voluntary retirement savings. These are three very different products: one tied to your salary, one a government savings account, and one a market-linked pension system with withdrawal rules you need to understand before you commit. This article compares all three using a common calculator framework — same contribution, same tenure, different rules — and does not crown a single universal winner.

Quick Answer: NPS vs EPF vs PPF Calculator

NPS vs EPF vs PPF calculator compares how the same monthly saving, such as ₹10,000, may grow across NPS, EPF and PPF over your working years. EPF is salary-linked, PPF is voluntary long-term savings, while NPS is market-linked and retirement-focused with withdrawal rules.

NPS vs EPF vs PPF Calculator: How to Estimate Your Retirement Corpus

Before any projected number makes sense, you need to understand the inputs behind it. A reliable NPS vs EPF vs PPF calculator asks for current age, retirement age, monthly contribution, existing account balance, expected annual step-up in contributions, and the return rate assumption for each product. Get these inputs right and the output becomes a useful planning range. Use the wrong assumptions and a large projected figure is simply noise.

What a Good Calculator Returns

The output should show more than just the final corpus number. Look for: total contributions made across the tenure, estimated interest or market gains, liquidity notes per product, and — critically for NPS — the lump sum portion and the annuity portion shown separately. NPS requires a portion of the corpus to be used for annuity purchase at the time of exit. A calculator that shows one blended NPS number without splitting these two is giving you an incomplete picture.

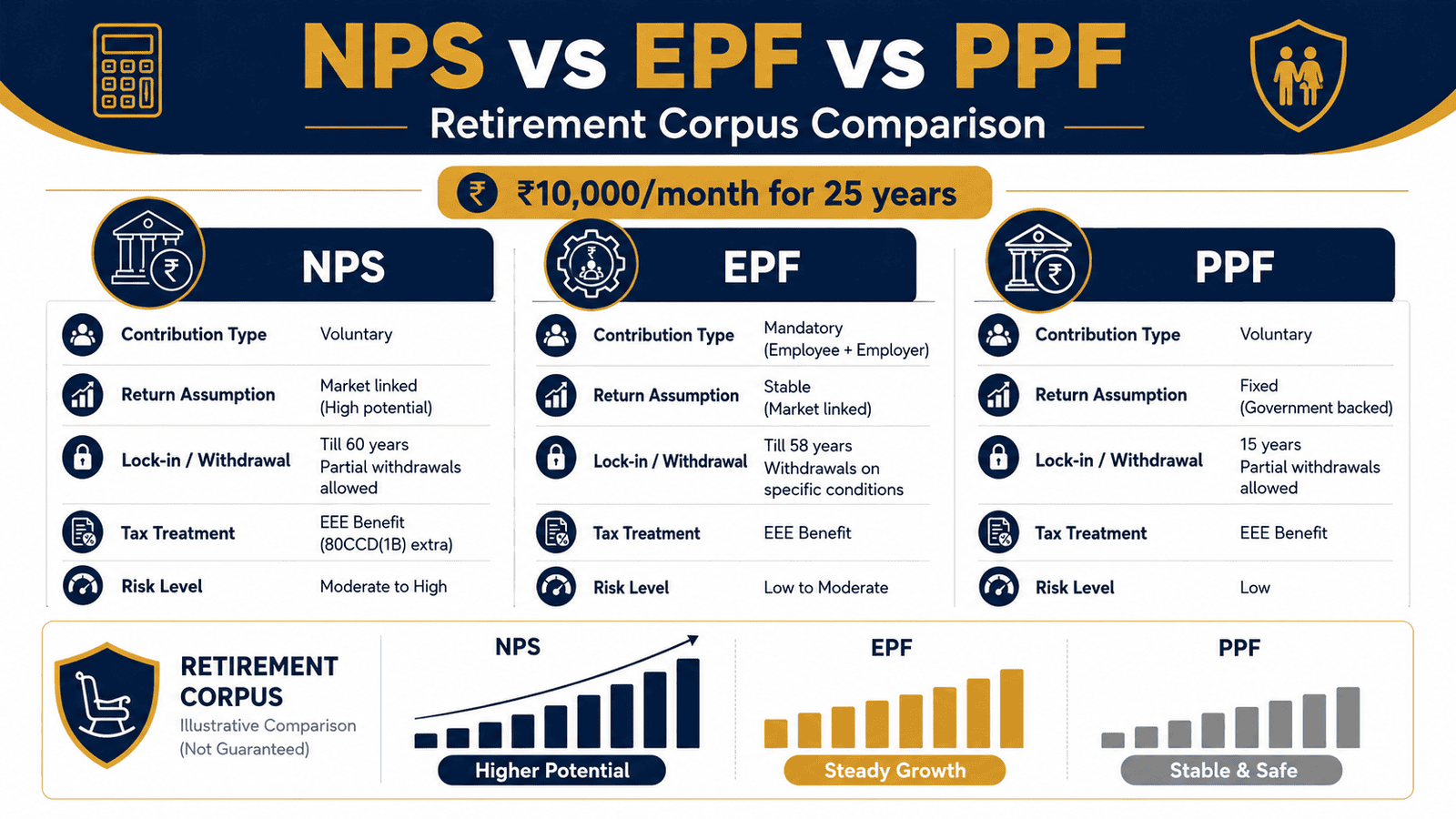

Same ₹10,000 — Three Different Outcomes

Using ₹10,000 per month, a starting age of 33, and a retirement age of 60 — a 27-year tenure — the estimated corpus across the three products using commonly referenced return assumptions looks roughly like this:

| Product | Estimated Corpus | Return Assumption Used |

|---|---|---|

| EPF | ~₹1.19 crore | 8.25% p.a. (declared rate) |

| PPF | ~₹97 lakh | 7.1% p.a. (declared rate) |

| NPS | ~₹1.63 crore | 10% p.a. (market assumption) |

These are estimates only and based on assumptions that can change. EPF and PPF rates are declared periodically by the government and are revised at intervals. The 10% NPS assumption is a planning number — not a guarantee. Market performance, fund choice, and asset allocation all affect the actual NPS outcome. For a detailed salary-specific EPF corpus breakdown, use the EPF corpus estimate tool. For a PPF tenure and maturity breakdown, use the PPF maturity estimate. For NPS-specific projection including pension assumptions, see the NPS pension estimate.

One critical NPS detail: of the ~₹1.63 crore projected NPS corpus, at least 40% must be used to purchase an annuity at retirement. That means the immediate lump sum available is roughly ₹98 lakh — and the rest converts into a monthly pension whose amount depends on annuity rates available at the time of purchase, which cannot be predicted today.

Corpus Formula = Monthly Contribution × [(1 + r)^n − 1] / r × (1 + r)

Where r = annual rate ÷ 12 (monthly rate); n = total number of months invested

Key Takeaways

- EPF is the only retirement option where someone else also contributes — your employer puts in 12% of your basic salary alongside your own 12%, making it the foundation of every eligible salaried employee’s retirement savings.

- PPF contributions are capped at ₹1.5 lakh per year. At 7.1% p.a. over 27 years, ₹10,000 per month may grow to approximately ₹97 lakh — lower than an optimistic NPS projection, but with no market risk and full liquidity at maturity.

- NPS gives an additional tax deduction of up to ₹50,000 under Section 80CCD(1B), entirely separate from the ₹1.5 lakh Section 80C limit — saving up to ₹15,600 per year for someone in the 30% bracket.

- NPS corpus projections can swing dramatically based on asset allocation. A 75% equity assumption over 27 years produces a very different result from a 50% equity assumption — always run a conservative scenario alongside an optimistic one.

- At retirement, NPS requires at least 40% of the accumulated corpus to be converted into an annuity — the tax-free lump sum is at most 60% of the total projected figure, not the full amount.

- Tenure contributes more to final corpus than small differences in return rate. Starting at 28 instead of 33 with the same ₹10,000/month can add tens of lakhs to the final number, regardless of which product you choose.

Key Facts at a Glance

| Feature | EPF / PPF | NPS |

|---|---|---|

| Product type | Salary-linked retirement benefit (EPF) / Voluntary government savings scheme (PPF) | Market-linked pension system regulated by PFRDA |

| Who can invest | Salaried employees in covered organisations (EPF); Any Indian citizen aged 18–60 (PPF) | Any Indian citizen aged 18–70; mandatory for central government employees |

| Return type | Government-declared interest rate, announced annually (EPF) or quarterly (PPF) | Market-linked — depends on equity, corporate bond, and government securities allocation |

| Withdrawal restrictions | EPF: on resignation or retirement with conditions; PPF: after 15-year lock-in with partial withdrawal provisions | Tier 1: exit at or after age 60; minimum 40% of corpus must purchase an annuity; partial withdrawals under specific conditions only |

| Tax treatment | Contributions eligible under Section 80C (shared ₹1.5 lakh limit for both EPF and PPF) | Section 80C + additional ₹50,000 under Section 80CCD(1B) + employer contribution separately under Section 80CCD(2) |

How NPS, EPF, and PPF Actually Work

EPF: Automatic, Salary-Linked, and Employer-Backed

For employees working in organisations with 20 or more staff, EPF is not optional — it is mandatory for eligible salary brackets. Every month, you contribute 12% of your basic salary, and your employer matches that amount. However, the employer’s 12% does not go entirely into your EPF corpus. A portion — 8.33% of your basic salary, subject to a wage ceiling — flows into the Employees’ Pension Scheme (EPS). Only the employer’s remaining contribution reaches your EPF account directly. The interest on EPF is declared by the EPFO’s Central Board of Trustees and is credited annually. According to EPFO guidelines, interest is calculated on the monthly running balance.

The key constraint: your EPF accumulation is entirely tied to your basic salary. A ₹22 lakh CTC structured with a low basic component produces a materially smaller EPF corpus than the same CTC with a higher basic. Many employees discover this gap only when they check their EPF balance in their 40s. Also worth noting: the EPS component generates a pension at retirement, not a lump sum — and the pension amount depends on years of service and the EPS formula, not the EPF interest rate.

PPF: Voluntary, Stable, and Genuinely Long-Term

PPF is open to any Indian citizen and requires no employer involvement. You can open a PPF account at a scheduled bank or post office, contribute between ₹500 and ₹1.5 lakh per year, and earn the declared quarterly interest rate on your balance. The lock-in is 15 years — after which you can extend the account in 5-year blocks, continuing to earn interest. Partial withdrawals are permitted from year 7 onwards under specific conditions.

The full PPF corpus — contributions plus interest — is tax-free on maturity. Contributions qualify under Section 80C. There is no market risk: the rate is declared in advance for each quarter, and you always know what you are earning for that period. The trade-off is that the PPF contribution ceiling of ₹1.5 lakh per year limits how much corpus you can build exclusively through PPF.

NPS: Market-Linked, Pension-Focused, and Complex at Exit

NPS — regulated by PFRDA — is fundamentally a pension system, not a savings scheme. You open a Tier 1 account and allocate contributions across three asset classes: equity (E), corporate bonds (C), and government securities (G). You can choose from multiple registered pension fund managers. Returns are not declared — they reflect market performance and your allocation choice. In a strong equity year, NPS Tier 1 returns can exceed 12%. In a market downturn, returns can be negative.

The exit rules are the most important feature to understand before committing to NPS. At age 60, you can withdraw up to 60% of your accumulated corpus as a tax-free lump sum. The remaining 40% must be used to purchase an annuity plan from a PFRDA-registered insurer. The monthly pension this annuity generates depends entirely on annuity rates at the time of retirement — rates that cannot be predicted today. This is the structural complexity that makes NPS different from both EPF and PPF.

For salaried employees, employer NPS contributions under Section 80CCD(2) are a deduction outside the ₹1.5 lakh Section 80C ceiling. This is one of the strongest tax advantages in the Indian personal finance landscape for employees whose companies offer it as part of the CTC. Understanding how salary NPS benefit works in practice — and how it changes the effective cost of NPS contributions — is essential before making any voluntary NPS contribution decision.

Real Example: Rohit’s Retirement Comparison, Pune

Rohit is 33, works as a senior software engineer in Pune, and earns ₹22 lakh per year. His basic salary is ₹8.8 lakh per annum. EPF is already running: both he and his employer contribute 12% of his monthly basic, which is roughly ₹8,800 each — though a portion of the employer’s side flows to EPS, not EPF.

He now has ₹10,000 per month that he wants to invest voluntarily for retirement. The question: PPF or NPS?

If Rohit puts ₹10,000 per month into PPF at 7.1% for 27 years, the estimated corpus at 60 is roughly ₹97 lakh — fully accessible as a lump sum. If he puts the same amount into NPS and assumes 10% annual returns on an equity-heavy allocation, the projected corpus is approximately ₹1.63 crore — but the accessible lump sum is around ₹98 lakh after the 40% annuity requirement. The remaining ~₹65 lakh purchases an annuity; the monthly pension from that annuity depends on rates at retirement.

The practical insight: at a 10% NPS assumption, the total corpus is significantly larger, but the immediately accessible cash at 60 is not dramatically different from PPF. The real NPS advantage for Rohit is the additional ₹50,000 deduction under Section 80CCD(1B), which saves him ₹15,600 per year in tax at the 30% bracket — plus the structured pension income that EPF and PPF do not provide.

Comparison: NPS vs EPF vs PPF Side by Side

| Factor | EPF | PPF |

|---|---|---|

| Best suited for | Mandatory salary-linked retirement accumulation for eligible salaried employees | Voluntary stable long-term savings for any Indian citizen with no market risk |

| Employer contribution | Yes — 12% of basic salary | No employer contribution |

| Return certainty | Declared annually by EPFO board | Declared quarterly by Finance Ministry |

| Premature withdrawal | Permitted with conditions on resignation or specific needs | Partial from year 7; full after 15-year maturity |

| Tax on maturity | Tax-free on retirement (conditions apply) | Fully tax-free at maturity |

| Annual contribution ceiling | Tied to salary structure; no fixed cap | ₹1.5 lakh per financial year |

| Factor | NPS | EPF / PPF |

|---|---|---|

| Return type | Market-linked — not guaranteed | Government-declared rate — known in advance |

| Liquidity before retirement | Low — Tier 1 has significant restrictions | Moderate — both have partial withdrawal provisions |

| Mandatory annuity at exit | Yes — minimum 40% of corpus | No — full lump sum available at exit |

| Additional tax deduction | Yes — ₹50,000 under Section 80CCD(1B) | No — only standard Section 80C benefit |

| Employer contribution benefit | Yes — Section 80CCD(2), outside 80C limit | EPF under 80C only; PPF has no employer component |

| Calculator output type | Range estimate — market-dependent | Point estimate — based on declared rate |

How to Decide What’s Right for You

you are a salaried employee and EPF is already being deducted from your salary — check your EPF balance and projected accumulation first. You may be closer to your retirement target than you think before adding any voluntary savings.

you want stable, government-backed savings with no market volatility and can lock money away for 15 years — PPF is a reliable complement to EPF. The declared-rate structure means no unpleasant surprises and full flexibility at maturity.

you are in the 30% tax bracket and have already exhausted your ₹1.5 lakh Section 80C limit — NPS under Section 80CCD(1B) gives you up to ₹50,000 in additional deductions, saving ₹15,600 per year in taxes. This benefit alone can make NPS worthwhile even if the returns do not outperform PPF.

your employer contributes to NPS as part of your CTC — accept that employer NPS contribution before making any voluntary PPF or NPS decisions. The Section 80CCD(2) deduction on employer contributions sits entirely outside your personal ₹1.5 lakh limit and is one of the best tax benefits available to salaried employees.

you may need to access some of this money before age 60 for a planned expense like children’s education or housing — NPS Tier 1 is the least flexible of the three options. EPF allows withdrawal on unemployment or specific needs; PPF permits partial withdrawals from year 7.

you are comfortable with market-linked volatility and the compulsory annuity purchase at retirement — NPS may not suit your financial temperament. A combination of EPF and PPF can build a more predictable retirement corpus without the complexity of pension fund management or annuity rate uncertainty.

Common Mistakes to Avoid

Treating NPS Projected Returns as Guaranteed

NPS calculators use assumed annual return rates — commonly 8%, 10%, or 12% — to project a retirement corpus. These are not guaranteed.

A portfolio with 75% equity exposure can deliver negative returns in a given year. Market cycles, fund performance, and your asset allocation all affect the final number. Projecting at 12% and planning your retirement around that figure is a significant risk.

Always run at least two scenarios — a 7% conservative assumption and a 10% moderate assumption — before deciding how much of your retirement plan depends on NPS.

Comparing EPF, PPF, and NPS Purely by Tax Deduction

The tax saving is real, but it is one factor — not the entire decision. A product that saves ₹15,600 in annual tax while locking money into a poorly-performing NPS allocation for 27 years is not automatically better than a declared-rate PPF account.

Compare liquidity, withdrawal rules, return certainty, and actual projected corpus under the same contribution before making a decision based on tax treatment alone.

Ignoring NPS Withdrawal and Annuity Requirements

A common shock at retirement: NPS does not hand over the full corpus as a lump sum. At least 40% must be used to purchase an annuity from an IRDAI-registered insurer — and annuity rates available at the time of retirement are not predictable today. Annuity income is also taxable. Review the rules around NPS account types before committing significant savings to NPS Tier 1.

Applying 12% EPF to CTC Instead of Basic Salary

EPF is calculated on basic salary — not on cost-to-company. If your CTC is ₹22 lakh but your basic is ₹7 lakh, your EPF contribution is 12% of ₹7 lakh, not ₹22 lakh. Many employees overestimate their EPF accumulation by applying the percentage to total CTC. Always check your payslip for the actual monthly EPF deduction before running any retirement calculation.

Using Stale Interest Rate Assumptions

EPF interest rates are declared annually by the EPFO board. PPF rates are revised quarterly by the Finance Ministry. Running a calculator with last year’s rate — or an outdated rate you read in an article — produces a misleading corpus estimate. Always verify current declared rates from official sources before running any projection.

Forgetting the EPS Component in EPF Calculations

Of the employer’s 12% EPF contribution, 8.33% (subject to a wage ceiling) goes to EPS — not your EPF corpus. This significantly reduces the employer contribution that actually compounds in your EPF account. Many online EPF calculators either ignore EPS or include it incorrectly, producing an inflated corpus estimate. Factor in the EPS deduction when assessing your actual EPF accumulation.

When This May Not Be the Right Choice

If you do not have an emergency fund covering at least 3–6 months of expenses, locking additional money into PPF or NPS creates financial exposure you cannot plan around. Build liquidity reserves first.

If you are carrying high-interest personal loan or credit card debt at 15% or above, the mathematical case for paying that down before adding to long-term retirement savings is strong — guaranteed interest savings outweigh uncertain corpus gains.

If your income is variable or your employment situation is uncertain, the 15-year PPF lock-in and the near-total NPS Tier 1 restriction until age 60 may not suit your current circumstances.

If you are investing in NPS solely to save tax and have no interest in a structured pension income at retirement, the mandatory annuity at exit will likely frustrate your expectations — the product is built around pension income, not lump-sum flexibility.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- EPFO — epfindia.gov.in — for EPF contribution structure, current interest rate, withdrawal rules, EPS provisions, and claim procedures

- PFRDA — pfrda.org.in — for NPS account rules, Tier 1 withdrawal conditions, annuity purchase requirements, pension fund options, contribution minimums, and partial withdrawal guidelines

- Income Tax Department — incometax.gov.in — for current Section 80C, 80CCD(1B), and 80CCD(2) deduction limits and applicable conditions

- SEBI — sebi.gov.in — for market-risk context relevant to equity and corporate bond allocations within NPS pension fund portfolios

Expert Tips

- Run at least three scenarios in any NPS vs EPF vs PPF calculator: conservative (7% NPS assumption), moderate (10%), and optimistic (12%). The difference between 7% and 12% over 27 years can exceed ₹60–70 lakh in corpus — always plan around the conservative output, not the optimistic headline number.

- Check your payslip before comparing. Many employees discover their actual monthly EPF deduction is ₹6,000–₹7,000, not ₹10,000, because basic salary is lower than assumed. Know your real EPF number before you decide how much voluntary retirement saving to add.

- If your employer offers NPS as a CTC component with an employer contribution, prioritise accepting that before making any additional voluntary PPF or NPS investments. The Section 80CCD(2) deduction is outside your personal 80C ceiling — it is effectively free tax saving.

- PPF and NPS are not mutually exclusive. You can contribute the full ₹1.5 lakh annually to PPF and separately contribute ₹50,000 to NPS under 80CCD(1B). These are separate contribution decisions with separate tax treatment.

- Factor the annuity into your NPS planning. If your projected NPS corpus at 60 is ₹1.5 crore, plan your post-retirement cash needs around ₹90 lakh (the 60% lump sum) — not the full amount. The annuity income supplements this but is not a lump sum you can deploy.

- Build a 5–10% annual step-up into your calculator inputs. Increasing your SIP contribution by 5% every year alongside salary increments can add materially to the final corpus — often more than switching between products chasing a marginally higher return assumption.

- Revisit your NPS asset allocation every year after 50. An equity-heavy NPS allocation appropriate at 33 carries significantly higher sequence-of-returns risk as you approach retirement. Most NPS platforms offer auto-choice and lifecycle-based rebalancing options worth reviewing.

Frequently Asked Questions

Is NPS better than EPF and PPF for retirement?

There is no single answer. Under an optimistic return assumption, NPS can project a larger corpus than EPF or PPF. But NPS returns are market-linked and not guaranteed, and the mandatory 40% annuity requirement at exit reduces the accessible lump sum. EPF and PPF offer declared-rate stability. Whether NPS is “better” depends on your risk tolerance, tenure, tax bracket, salary structure, and whether your employer contributes to NPS.

Which gives the highest retirement corpus: NPS, EPF, or PPF?

Under a 10% NPS assumption over 27 years, NPS projects the largest total corpus. However, once the 40% annuity requirement is applied, the immediately available NPS lump sum at 60 can be comparable to PPF maturity value under similar contribution levels. If NPS actual returns come in at 7–8%, the corpus difference narrows significantly. Always compare all three under the same contribution and tenure before drawing conclusions.

Can I invest in NPS, EPF, and PPF at the same time?

Yes. EPF is linked to your salary and runs automatically through your employer. You can open a separate PPF account at any bank or post office and contribute up to ₹1.5 lakh per year. You can also open an NPS Tier 1 account and contribute voluntarily. There is no regulatory restriction on holding all three simultaneously — and combining all three is a common approach among salaried employees who want both stability and market-linked retirement savings.

Is NPS riskier than EPF and PPF?

Yes, in terms of return certainty. EPF and PPF rates are declared by the government for fixed periods — the rate can change at the next revision, but you always know exactly what your balance earned for the current period. NPS equity fund returns depend on market performance and can be negative in a given year. This is the core trade-off: the potential for a larger corpus with market risk, versus lower but predictable declared-rate returns.

Should I invest in PPF if I already have EPF?

PPF and EPF both fall under the ₹1.5 lakh Section 80C limit, so they compete for the same tax deduction space. However, PPF adds a separate voluntary corpus outside your salary structure, with a declared government rate and full tax-free maturity. If you have 80C capacity remaining after EPF, PPF is a straightforward, low-risk way to add to long-term savings. Many salaried employees with EPF still maintain a PPF account for this reason.

Are calculator results guaranteed?

No. Calculator outputs are estimates based on the return assumptions and contribution inputs you enter. EPF and PPF declared rates can and do change with each government revision. NPS returns are entirely market-dependent and unpredictable. The calculator is a planning tool — not a forecast. Treat the output as a planning range and update your inputs every year as rates change.

What happens if I withdraw from NPS Tier 1 before age 60?

Premature exit from NPS Tier 1 before age 60 is subject to significantly stricter rules than normal retirement exit. At least 80% of the corpus must be used to purchase an annuity — only 20% is available as a lump sum. This is a much less favourable split than the 60/40 rule at age 60. Limited partial withdrawals are permitted under specific conditions — such as treatment of critical illness, higher education, or purchase of a first home — subject to PFRDA guidelines and lock-in conditions.

What is the minimum annual contribution to keep a PPF or NPS account active?

PPF accounts require a minimum contribution of ₹500 per financial year to remain active. If you miss a year, the account becomes discontinued and requires a revival application with a penalty fee per dormant year. NPS Tier 1 accounts also have a minimum annual contribution requirement to remain active — verify the current minimum directly from PFRDA at pfrda.org.in, as this figure can be revised.

Final Verdict

If you are a salaried employee, EPF is already your retirement foundation — understand how much it accumulates before you commit to adding anything else. PPF makes sense as a stable voluntary addition if you have 80C capacity remaining and a 15-year horizon. NPS earns its place primarily through the additional ₹50,000 deduction under Section 80CCD(1B) and through the employer contribution tax benefit under Section 80CCD(2) — not simply because an optimistic market-return assumption produces a larger projected number.

The NPS vs EPF vs PPF calculator is most useful when you run it with conservative assumptions, treat EPF as the mandatory base and PPF or NPS as voluntary choices, and read the output as a planning range rather than a prediction. Before deciding how much total corpus you actually need at retirement, see retirement corpus planning for a full needs-based framework.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Suresh Nair writes about Indian government savings schemes, post office schemes, and conservative long-term savings options. His content is especially useful for families, parents, senior citizens, and low-risk savers who want to understand scheme rules before depositing money.

He covers topics such as Public Provident Fund, Sukanya Samriddhi Yojana, Senior Citizens’ Savings Scheme, National Savings Certificate, Kisan Vikas Patra, Post Office Monthly Income Scheme, National Pension System, post office fixed deposits, post office recurring deposits, child savings schemes, senior citizen savings options, maturity rules, withdrawal rules, lock-in periods, and tax treatment.

Suresh’s writing is mature, rule-focused, and cautious. He explains eligibility, deposit limits, tenure, interest calculation, tax benefits, withdrawal conditions, and practical use cases in simple language. His articles are useful for readers who prefer safety and predictable rules over high-risk investments. Since government scheme interest rates, deposit limits, lock-in rules, and tax treatment may change through official notifications, readers should verify current details from India Post, PFRDA, Income Tax Department, or relevant government sources before investing.