Most salaried employees in India pick a credit card based on the headline number — “5X reward points” or “5% cashback” — and assume the bigger figure automatically wins. The real picture is messier. The reward points vs cashback credit cards decision is a question about net annual value: what actually lands in your pocket after annual fees, monthly caps, excluded spending categories, redemption complexity, and point expiry. A card advertising 5X points on dining can deliver ₹0 in real value if those points are worth ₹0.25 each, expire in 12 months, and your biggest recurring expenses — utilities and rent — are excluded from earning entirely. This article works through both card types using specific ₹ figures so you can match the right structure to your actual spending pattern, not to a marketing banner.

Quick Answer: Reward Points vs Cashback Credit Cards

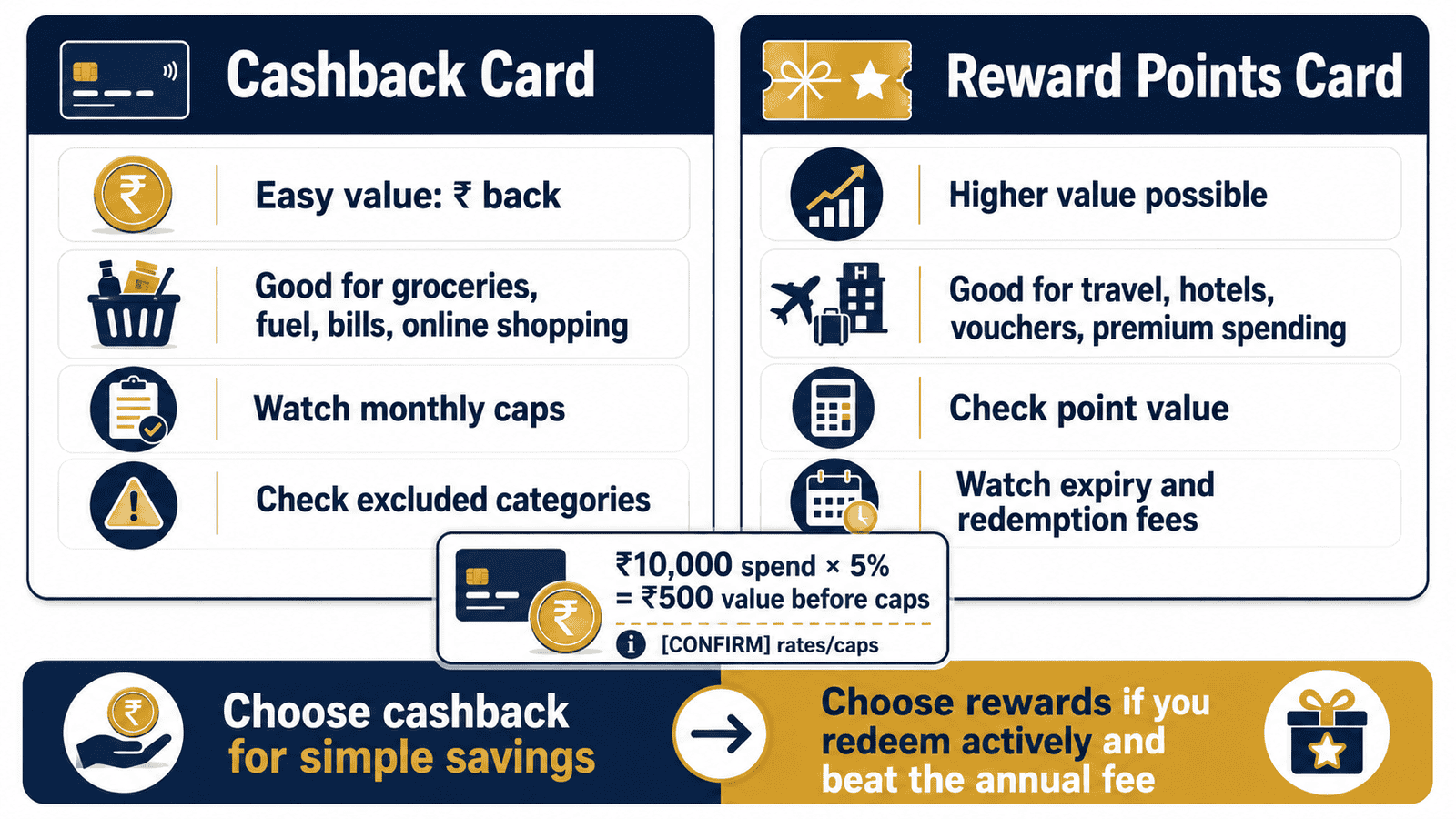

Reward points vs cashback credit cards is mainly a choice between flexible redemption value and simple ₹ savings. Cashback is easier because value appears as statement credit or direct saving, while reward points may beat cashback only when redemption value, fees, caps, expiry, and exclusions are clearly better for your spending.

Key Takeaways

- Cashback cards deliver a fixed ₹ value — typically 1%–5% of eligible spend — credited directly to your statement or bank account with no redemption step required.

- Most Indian reward-point cards price each point at ₹0.25–₹0.50 for merchandise redemption; premium travel redemptions on select cards can push per-point value above ₹1, but only if you book through the bank’s own travel portal.

- Monthly cashback caps — commonly ₹500–₹2,000 per month per category — can neutralise a higher cashback rate the moment eligible spend crosses the cap threshold for that month.

- Reward points typically expire 12–36 months from the earn date; cashback credited as a statement credit does not expire once posted to your account.

- Net annual card value = (total rewards or cashback earned in ₹) minus annual fee. A lifetime-free cashback card earning ₹3,600 per year outperforms a ₹999-fee rewards card earning ₹4,200 in points redeemed at catalogue rates.

- Accelerated reward categories — online shopping, travel, dining — can yield 5X–10X points, but utilities, rent payments, fuel, and government portal transactions are excluded from earning on almost every card in India.

- Always read the MITC terms before applying: confirm the reward conversion ratio, redemption catalogue, excluded categories, and annual fee waiver condition before committing to any card.

Comparison: Reward Points Cards vs Cashback Cards

| Parameter | Reward Points Cards | Cashback Cards |

|---|---|---|

| How value is delivered | Points accumulated; redeemed via catalogue, travel bookings, or statement credit | ₹ credited directly to statement or bank account automatically |

| Redemption effort | Higher — log in, browse catalogue, initiate redemption before expiry | Lower — automatic or single-click; no action needed |

| Value certainty | Variable — ₹0.25 to ₹1+ per point depending on redemption method chosen | Fixed — 1% cashback always equals ₹1 per ₹100 spent |

| Expiry risk | Yes — typically 12–36 months from earn date; forfeited if unused | None once credited to your statement balance |

| Caps and limits | Accelerated category caps and annual milestone limits apply on many cards | Monthly cashback cap per category is standard — often ₹500–₹2,000 |

| Best suited for | Frequent travellers, high spenders comfortable tracking redemptions actively | Beginners, consistent online shoppers, those who value simplicity and certainty |

| Annual fee sensitivity | Often ₹500–₹5,000+ for meaningful earn rates; waiver possible on spend milestones | Many strong options are lifetime-free; fee waiver thresholds typically easier to meet |

| Transparency | Medium — effective ₹ value depends on how and when you redeem | High — ₹ value is always explicit in the offer and in your statement |

Key Facts at a Glance

| Fact | Reward Points Cards | Cashback Cards |

|---|---|---|

| Typical base earn rate | 1–2 points per ₹100; 5X–10X on select categories | 1%–2% flat; up to 5% on accelerated categories |

| Effective ₹ value at base rate | ₹0.25–₹0.50 per ₹100 spent (at ₹0.25/point) | ₹1–₹2 per ₹100 spent |

| Expiry | 12–36 months from earn date; varies by issuer | Does not expire once credited to statement |

| Common excluded categories | Fuel, rent, utilities, government portals, EMI transactions | Fuel, rent, utilities, government portals, EMI transactions |

| Annual fee range (as of recent data) | ₹0–₹5,000+ depending on card tier and issuer | ₹0–₹1,500 for most popular options |

How Reward Points Actually Work

A reward points card earns points for every eligible rupee you spend. The earn rate is expressed as “X points per ₹100” — for example, 2 points per ₹100 on general spends and 10 points per ₹100 on online shopping. These points accumulate in your card account and can later be redeemed through the bank’s catalogue for merchandise, gift vouchers, flight miles, or as a statement credit against your outstanding dues.

The figure most cardholders ignore is the reward conversion ratio: how much each point is actually worth in ₹ at the time of redemption. At ₹0.25 per point, 10,000 points equal ₹2,500. At ₹0.50, the same 10,000 points equal ₹5,000. At ₹1 or more — achievable primarily through premium travel redemptions on select cards — your value improves further. A card that earns points faster but converts at ₹0.25 will often underperform one that earns more modestly but converts at ₹0.50. The headline earn rate and the redemption conversion rate together determine real value; neither figure alone tells you anything useful.

Two additional factors eat directly into reward-card returns: accelerated category caps and excluded merchant categories. Many cards cap bonus-rate earnings — bonus points on online shopping may be capped at 2,000 additional points per month. Spend above that cap earns only the base rate. Utilities, rent paid via third-party apps, fuel, government portals, and EMI transactions are excluded on almost every card in India. If these categories make up a large share of your monthly spend, the effective earn rate on your total spending will be considerably lower than the advertised headline rate.

How Cashback Cards Work

Cashback cards return a percentage of eligible spend directly as ₹ value — either as a statement credit that reduces your outstanding balance, or in some cases as a transfer to a linked savings account. There is no redemption step and no catalogue to navigate. The saving is automatic.

Most Indian cashback cards operate on a tiered structure: a higher rate — typically 2%–5% — on specific categories such as online shopping, food delivery, or utility bill payments, and a lower flat rate of 0.5%–1% on all other eligible spends. The monthly cashback cap is what most beginners overlook. A card offering 5% cashback on online shopping with a ₹1,000 monthly cap returns the full 5% only on the first ₹20,000 of online spend in that month. Every rupee above ₹20,000 earns the lower base rate. For most salaried employees spending ₹8,000–₹15,000 online per month, the cap is rarely hit — but it must be confirmed before applying.

Excluded categories on cashback cards mirror those on rewards cards: fuel, rent, utilities, government payments, and EMI transactions are the most common. If you are still building your understanding of how credit card structures work, our guide to choosing your first credit card in India covers what to look for before you apply.

reward points vs cashback credit cards: The Number Most People Miss

The most common mistake in this comparison is treating “5X points” as equivalent to “5% cashback.” It almost never is. If a card earns 1 point per ₹100 as its base rate and applies 5X on dining, you earn 5 points per ₹100 on dining spends. At ₹0.25 per point, that is an effective cashback equivalent of 1.25% — less than a flat 2% cashback card on the same transaction. The rewards card advantage only emerges when the per-point redemption value is high enough to overcome the conversion gap, typically only for premium flight or hotel awards on select cards.

Milestone Benefits and Their Real Value

Many rewards cards offer milestone benefits — a gift voucher, bonus points, or an annual fee waiver when cumulative annual spend crosses a threshold such as ₹1 lakh or ₹2 lakh. These can add genuine value — sometimes ₹500–₹2,000 in vouchers — but only if you were going to make that spend regardless. Chasing a milestone by overspending converts a reward benefit into a net financial loss. When running the net annual value calculation, count milestone benefits only at the ₹ value you will realistically redeem them for, not at their face value.

Accelerated Categories: Reading the Fine Print

Both card types advertise accelerated rates on specific categories to attract applicants. The critical discipline is mapping those categories against your own spending. If a cashback card offers 5% on online shopping but your largest monthly expense is a ₹12,000 grocery delivery app that has been reclassified as a food service by the bank — and therefore earns only the base rate — your actual return is far lower than projected. Confirm category classification with the issuer before relying on accelerated rates for your core spend categories.

Real Example: Ankit’s ₹40,000 Monthly Spend

Ankit, 29, a software engineer in Bengaluru earning ₹18 lakh per year, puts approximately ₹40,000 per month through his credit card: ₹12,000 on online shopping and apps, ₹5,000 on food delivery, ₹8,000 on flight and hotel bookings, ₹8,000 on utility and electricity bills, and ₹7,000 on other purchases.

He is weighing two cards: a rewards card with a ₹1,499 annual fee, earning 4 points per ₹100 on all eligible spends with utilities excluded and points valued at ₹0.50 per point for travel redemption; and a lifetime-free cashback card offering 5% on online spends (capped at ₹1,000 per month) and 1% on all other eligible spends, with utilities also excluded.

Both cards exclude the ₹8,000 utilities spend, leaving ₹32,000 eligible per month. Ankit clears his full balance every month — meaning interest never offsets his earnings. How you manage your billing cycle directly affects how much your rewards are worth in practice; our guide to billing cycles and due dates explains the mechanics.

How to Calculate Net Annual Card Value

Net Annual Card Value = (Total annual rewards or cashback earned in ₹) − Annual fee

Rewards card — Ankit’s working: Eligible monthly spend ₹32,000 at 4 points per ₹100 = 1,280 points per month = 15,360 points per year. At ₹0.50 per point (travel redemption): ₹7,680 gross value. Minus ₹1,499 annual fee: net annual value = ₹6,181.

Cashback card — Ankit’s working: Online shopping ₹12,000 × 5% = ₹600 per month (below the ₹1,000 cap). Other eligible spend ₹20,000 × 1% = ₹200 per month. Monthly total: ₹800. Annual: ₹9,600. Annual fee: ₹0. Net annual value = ₹9,600.

| Scenario | Rewards Card (₹1,499 fee) | Cashback Card (₹0 fee) |

|---|---|---|

| Ankit redeems points at ₹0.50 (travel) | ₹6,181 net annual value | ₹9,600 net annual value |

| Ankit redeems points at ₹1.00 (premium travel) | ₹13,861 net annual value | ₹9,600 net annual value |

| Ankit redeems points at ₹0.25 (merchandise) | ₹2,341 net annual value | ₹9,600 net annual value |

The key insight for Ankit: the rewards card only wins if he actively books travel through the bank’s portal and achieves ₹1+ per point consistently. For a beginner who won’t manage redemption windows, the cashback card is the safer, higher-value choice across all realistic scenarios.

How to Decide What’s Right for You

You pay your full statement balance every month without exception — THEN both card types are viable; compare purely on net annual value using your actual spend categories.

Your top two spending categories are online shopping and food delivery — THEN a cashback card with accelerated rates on those categories will likely deliver higher, more predictable returns than a standard rewards card.

You book 4–6 flights per year and are willing to redeem points through the bank’s travel portal — THEN a premium rewards card achieving ₹0.75–₹1+ per point on travel redemptions can outperform a cashback card at the same spend level.

Your monthly card spend is under ₹15,000 — THEN annual-fee cards rarely generate enough rewards to break even; check lifetime-free options first. If you already carry a card with an annual fee, understand your eligibility for an annual fee waiver before the next anniversary date.

You have never actively tracked or redeemed credit card rewards before — THEN start with a cashback card; the value is automatic, verifiable every cycle, and cannot expire.

Your biggest monthly expenses are utilities, rent, or fuel — THEN neither card type will reward those spends meaningfully; your effective earn rate on total spend will be significantly lower than the advertised rate regardless of card type.

You regularly carry a balance or occasionally miss due dates — optimising reward type is not the right priority. Interest at 36%–42% per year will erase months of accumulated reward value in a single billing cycle of unpaid dues.

Common Mistakes to Avoid

Comparing headline rates without checking the conversion ratio

Seeing “5X reward points” and assuming it is equivalent to 5% cashback.

At ₹0.25 per point, 5X on a ₹10,000 dining bill earns 500 × 5 = 2,500 points = ₹625 — an effective return of 6.25%. That sounds better than a 5% cashback card returning ₹500 on the same spend. But drop the point value to ₹0.10 (merchandise redemption on many catalogue options) and 2,500 points = ₹250 — suddenly the cashback card wins by ₹250 on a single transaction.

Calculate effective ₹ value per ₹100 spent at the actual point redemption rate you will realistically use before making any comparison.

Ignoring monthly cashback caps

Spending heavily in an accelerated category without checking what the monthly cap actually is.

A card offering 5% cashback on online shopping capped at ₹750 per month returns ₹750 whether you spend ₹15,000 or ₹60,000 in that category. Every rupee above the cap threshold earns the base rate — often 0.5% or 1%. Assuming the full 5% rate applies to all online spend can overestimate your annual cashback by ₹3,000–₹6,000 at higher spend levels.

Always calculate your actual cashback at your real monthly spend volume, including the cap ceiling effect.

Letting reward points expire unused

Accumulating a large points balance over two years and then missing the expiry window.

Points earned in January 2024 may expire in December 2025 on a 24-month expiry card — not in January 2026. A cardholder who forgets to redeem 25,000 points valued at ₹6,250 in travel credit loses that benefit entirely with no reinstatement option. Cashback posted to your statement carries no equivalent forfeiture risk.

Set a calendar reminder three months before your oldest-batch points expire and check point balances quarterly in the banking app.

Overspending to hit a milestone benefit

Spending an extra ₹8,000 specifically to cross the ₹2 lakh annual spend threshold for a ₹500 voucher.

If those purchases were not already planned, the “benefit” costs more than it delivers. Milestone benefits add real value only when your natural spending already comes within striking distance of the threshold — ideally within the final 30 days of the card anniversary year.

Count milestone benefits in your net value calculation only at a realistic ₹ redemption value, not their face value.

Not mapping your spend against excluded categories before applying

Assuming all your monthly card spending earns rewards or cashback at the advertised rate.

If ₹10,000 of your ₹35,000 monthly card spend falls in excluded categories — utilities, rent, government payments, fuel — your effective earn rate on total spend drops sharply even before caps are applied. Overspending on excluded categories also raises your credit utilisation ratio without delivering any reward benefit, which can harm your CIBIL score.

Map your actual 3-month spending to eligible and excluded categories before estimating annual value from any card.

Converting reward points to statement credit at a poor rate

Redeeming points for statement credit when the per-point value is ₹0.10 instead of using the travel portal at ₹0.50.

Statement credit redemption on rewards cards is often the lowest-value option in the catalogue — sometimes 5× worse than travel redemption on the same card. Many cardholders choose it because it feels “safe” or familiar, but they are leaving significant value on the table compared to redeeming for flight vouchers or hotel stays at the higher rate.

Before redeeming, check all options in the bank’s redemption catalogue and calculate the ₹ value per 1,000 points for at least three redemption types.

Picking a card based on brand appeal or aesthetics

Applying for a premium metal card because it looks impressive — without running the net annual value calculation first.

A ₹5,000 annual fee card with airport lounge access delivers ₹0 net value if your spend profile generates ₹3,500 in annual points and you visit an airport lounge twice a year at best. Lounge access, concierge service, and travel insurance have real ₹ value only if you use them regularly and would have paid for them otherwise.

Run the net annual value formula using your own 12-month spending data before applying for any fee-bearing card.

Applying for a card without reading the MITC

Relying on the bank’s highlights page or a comparison portal rather than the full Most Important Terms and Conditions document.

The highlights page is a marketing document. The MITC contains the earn rate, the excluded categories, the cashback cap, the point expiry schedule, the fee waiver condition, the minimum redemption threshold, and the dispute process — none of which are reliably summarised elsewhere. A five-minute MITC review before applying has saved many cardholders from a year of lower-than-expected returns.

Download the MITC from the bank’s official product page and check these six items before submitting an application.

When This May Not Be the Right Choice

A rewards card is not the right priority if you carry a balance month to month. Interest on Indian credit cards typically runs at 36%–42% per year — and a single month of unpaid dues can cost more in interest charges than an entire quarter of accumulated reward points. Before optimising for reward type, make sure you fully understand how credit card interest is calculated in India and what it costs at your balance level.

A cashback card with strict monthly caps may also underperform for very high spenders putting ₹80,000 or more per month through a single card. At that volume, the cap erodes the headline rate so significantly that a well-structured rewards card with no per-category cap can deliver better annual returns — provided redemption is managed actively.

If you already hold two or more credit cards and struggle to track payment due dates and balances reliably, adding a third card of either type increases complexity without proportional benefit. Consolidating spend on one well-chosen card almost always outperforms spreading across multiple cards that are difficult to track.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit card reward rates, cashback percentages, monthly caps, point conversion ratios, excluded categories, annual fee structures, and MITC terms are set individually by each card-issuing bank or NBFC — not by a single regulator — and can change without advance notice. The RBI (rbi.org.in) provides overarching consumer protection guidelines for credit card issuers in India, including fair practice codes, billing transparency requirements, and dispute resolution frameworks. The specific reward rate, redemption catalogue value, expiry schedule, cap amounts, and exclusions applicable to any card are governed entirely by that issuer’s own terms and conditions.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- RBI — rbi.org.in (consumer protection guidelines, credit card master directions)

- Your card issuer’s official website — MITC section for the specific card you are considering

Once you have verified the correct figures, use your monthly credit card statement to confirm that cashback has been credited or points have been posted as expected. Our guide to reading your credit card statement shows exactly where reward credits, cashback postings, fee charges, and reversals appear — and what to do if a credit is missing.

Expert Tips

- Run the net annual value formula using your own data before applying for any card. Pull your last three months of UPI and debit card statements, categorise the spend, apply the card’s earn rate only to eligible categories, and subtract the annual fee. This 20-minute exercise prevents a poor card decision that silently costs ₹2,000–₹5,000 per year.

- Before redeeming reward points, check the per-point ₹ value for at least three redemption options in the bank’s catalogue — merchandise, vouchers, and travel. Travel redemptions on many cards return 2X–4X more per point than merchandise; the difference between ₹0.25 and ₹1 per point on 15,000 accumulated points is ₹11,250.

- Set a recurring calendar reminder three months before your oldest batch of points expires. Most banking apps now display expiry dates per batch in the rewards dashboard — if yours does not, call the card helpline and ask for the expiry schedule in writing.

- If you hold both a rewards card and a cashback card, route excluded-category spends — utilities, fuel, rent — through whichever card at least earns a minimal base rate. Some cashback cards earn 0.5% even on typically excluded categories; check the MITC to confirm rather than assuming zero.

- For cashback cards with monthly category caps, time large planned purchases before the billing cycle resets. If your ₹1,000 monthly cap on online shopping still has ₹600 unused and you plan a ₹12,000 electronics purchase, making it before cycle reset gives you ₹600 cashback; waiting until the next cycle gives you the same ₹600. Timing rarely matters, but splitting a large purchase across two cycles intentionally wastes no value.

- If your card offers a milestone benefit at ₹2 lakh annual spend and you are at ₹1.90 lakh with 30 days to go, consider prepaying any upcoming subscription renewals, insurance premiums, or annual bills — no extra spending, just pulling forward what you would pay anyway. Confirm these categories earn points or cashback before doing this.

- Never apply for a card purely for the welcome bonus unless the card’s ongoing reward structure also justifies the annual fee after Year 1. Welcome bonuses are one-time; annual fees are permanent until waived or the card is closed.

Frequently Asked Questions

Are reward points better than cashback in India?

Not automatically. Reward points beat cashback only when the per-point redemption value — especially for premium travel bookings — exceeds the cashback equivalent for the same spend. At ₹0.25–₹0.50 per point (standard merchandise or voucher redemption), most rewards cards return less per ₹100 than a good 2%–5% cashback card. The answer depends entirely on your redemption behaviour and how consistently you achieve the higher per-point rate.

What is a reward point worth in rupees on Indian credit cards?

It depends on the card issuer and the redemption option you choose. As of recent data, most mainstream Indian rewards cards price points at ₹0.25–₹0.50 per point for merchandise or voucher redemption. Premium and travel-focused cards can deliver ₹0.75–₹1+ per point on flight and hotel redemptions made through the bank’s own travel portal. The value can differ by 4X or more between the best and worst redemption options on the same card — always check the full catalogue before redeeming.

Can reward points expire?

Yes. Most Indian credit card reward points expire 12–36 months from the date they were earned — not from the card anniversary. Some cards forfeit all points if your account becomes inactive for a defined period or if you close the card before redeeming. Cashback credited to your statement as a balance reduction does not expire once posted. If you tend to accumulate points slowly and redeem infrequently, expiry is a genuine risk that reduces your effective annual return.

Is 5% cashback actually 5% on everything I spend?

No. The 5% rate applies only to eligible spends in the qualifying category, and only up to the monthly cashback cap. If a card offers 5% on online shopping capped at ₹1,000 per month, you reach maximum cashback at ₹20,000 of qualifying online spend. Beyond that threshold, the base rate — typically 0.5%–1% — applies. Your effective blended cashback rate across all your monthly spending is usually 1%–2%, not 5%, once the cap and excluded categories are factored in.

What spending categories are usually excluded from earning rewards or cashback?

Fuel transactions, rent paid via third-party apps, electricity and utility bill payments (on many cards), government tax payments, EMI transactions billed through the card itself, cash advances, and wallet top-ups are the most commonly excluded categories across both rewards and cashback cards in India. The exact exclusion list varies significantly by issuer and by individual card — always confirm in the MITC for your specific card before relying on earning from any of these categories.

Is it worth paying an annual fee for a rewards credit card?

Only if the net annual value — total rewards earned in ₹ minus the annual fee — is positive after accounting for your actual spend pattern and realistic redemption behaviour. A ₹999 annual fee is justified only when your realistic reward earnings clearly exceed ₹999 per year. If your spend consistently meets the issuer’s spend milestone, also verify your eligibility for an annual fee waiver — a waiver turns the breakeven calculation entirely in your favour.

What happens if I don’t redeem my reward points before the expiry date?

They are permanently forfeited. The bank cancels expired points and there is no reinstatement process in most cases. This is one concrete reason many first-time cardholders find cashback cards more reliable — there is no equivalent risk of losing credited cashback through inaction or inattention. If you know you are unlikely to track expiry dates actively, factor the probability of forfeiture into your net annual value estimate for any rewards card.

Can I convert reward points to cash or statement credit?

Some cards allow this, but usually at a significantly lower rate than travel or voucher redemption. For example, a card might allow 1,000 points to be redeemed as ₹100 statement credit (₹0.10 per point), while the same 1,000 points could redeem a ₹400 flight voucher (₹0.40 per point). Choosing statement credit on a rewards card to get “cash equivalent” value is often the worst redemption choice available — check the full catalogue and calculate per-point value across all options before deciding.

Which card type is better for a first-time cardholder?

A lifetime-free or low-fee cashback card is the more practical starting point for most beginners. The value is automatic and visible on every statement, there is no redemption step to manage, and the risk of losing accumulated value through expiry is zero. Once you have 12 months of real card spending data, you can run a proper net annual value comparison and decide whether a rewards card structure fits your actual behaviour — not just your planned behaviour at the time of applying.

Does carrying a balance cancel my reward points or cashback?

Carrying a balance does not usually cancel earned rewards or cashback — but the interest cost will almost certainly exceed the reward benefit. Interest on Indian credit cards typically runs at 36%–42% per year. A ₹15,000 unpaid balance carried for two months generates approximately ₹900–₹1,050 in interest charges — enough to wipe out two to three months of cashback earnings on the same card. Rewards optimisation is only worthwhile when your balance is cleared in full every month.

Final Verdict

The reward points vs cashback credit cards decision ultimately comes down to one calculation: net annual card value at your actual spending level. For most salaried employees in India spending ₹20,000–₹50,000 per month on online shopping, food delivery, and regular bills, a well-chosen cashback card delivers more predictable, zero-effort value than a rewards card redeemed at catalogue or merchandise rates. Rewards cards win only for disciplined, high-spending travellers who actively manage their points balance and consistently redeem at ₹0.75–₹1+ per point through the bank’s travel portal.

Beginners should start with a lifetime-free cashback card, build 12 months of real spending data, and only then evaluate whether a rewards card structure suits their actual behaviour. Whichever card type you choose, confirm that your biggest spending categories are eligible — and that the annual fee pays for itself before committing. For a structured starting point, read our guide to choosing your first credit card in India.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.