Your offer letter says ₹14 LPA. You do the quick math — ₹1,16,667 a month. Sounds solid. Then you join, and your first salary credit is ₹72,000. Where did the rest go?

Variable pay in CTC is often the answer. It is the part of your salary package that looks real on paper but may not reach your bank account every month — or at all, depending on your performance, your team’s output, or how the company has done that quarter.

This article explains what variable pay in CTC actually means, how tax and TDS work when it is paid, and how to estimate your real take-home salary before saying yes to any offer. Whether you are evaluating your first job or comparing two packages, knowing this upfront can save you from some very unpleasant payslip surprises.

Quick Answer: Variable Pay in CTC

Variable pay in CTC is the performance-linked part of your salary package that may be paid monthly, quarterly, annually, or only after targets are met. For example, a ₹14 LPA CTC with ₹2 LPA variable pay does not mean ₹14 LPA is fully guaranteed. Tax and TDS usually apply when paid.

Key Takeaways

- Variable pay is included in your CTC but is typically conditional — your full payout depends on individual performance, team targets, or company results, depending on the employer’s policy.

- On a ₹14 LPA CTC with ₹2 LPA variable, your guaranteed monthly salary is built on ₹12 LPA — roughly ₹72,000–₹80,000 in hand each month, not ₹1,16,667.

- Variable pay is taxable as salary income under the Income Tax Act when it is credited — it is not a tax-free bonus or reimbursement.

- In months when variable pay is paid out, your employer will typically deduct higher TDS to account for the extra income that month.

- Payout frequency varies by employer — quarterly, half-yearly, and annual cycles are all common. Ask HR in writing before comparing offers.

- Resigning before a scheduled payout date may forfeit your variable pay for that cycle entirely, depending on the employer’s HR policy.

- Two offers at the same CTC can feel very different financially — always compare fixed pay first, not headline CTC.

Key Facts at a Glance

Before the full explanation, here is a quick reference. For more on how basic salary drives PF, HRA, and other salary components, see our guide on basic salary meaning.

| Factor | What You Need to Know |

|---|---|

| What is variable pay? | A conditional, performance-linked component included in CTC — not a fixed monthly entitlement |

| Is it part of CTC? | Yes — but it inflates the headline number while reducing your predictable monthly salary |

| Is it guaranteed? | No — payout depends on individual, team, or company performance under the employer’s policy |

| Common payout frequency | Quarterly, half-yearly, or annual — monthly payout exists but is less common |

| Is it taxable? | Yes — taxable as salary income under the Income Tax Act when paid or credited |

| TDS treatment | Employer projects annual income including variable pay and deducts TDS — higher TDS in payout months is typical |

| Does it affect PF? | Generally no — EPF is calculated on basic salary unless the employer’s PF policy specifies otherwise |

| Where to verify rules | Income Tax Department (incometax.gov.in) for tax; EPFO (epfindia.gov.in) for PF; employer HR for payout eligibility |

What Is Variable Pay in CTC — And Why It Changes Your Monthly Reality

When a company makes you a salary offer, the CTC — Cost to Company — is the total annual amount the employer is willing to spend on employing you. It bundles together your basic salary, HRA, allowances, employer’s PF contribution, gratuity provision, insurance premium, and variable pay. Everything adds up to one headline number.

The problem is that not all of it reaches your bank account. Some components are statutory contributions — the employer’s PF share, for example, never appears in your salary credit. Others are conditional. Variable pay is the clearest and most misunderstood example of a conditional component.

Fixed Compensation vs Variable Pay: The Core Difference

Your fixed compensation is the part of your CTC that does not depend on performance or timing. It includes basic salary, HRA, transport allowance, and other regular monthly components. This generates your payslip credit reliably, every month, regardless of how your quarter went.

Variable pay — also called a performance-linked incentive, target incentive, appraisal-linked bonus, or annual bonus payout — is tied to a condition. That condition might be your individual performance rating, your sales team hitting a quarterly number, or the company crossing a profit threshold. If the condition is met, you receive it. If it is not, you may get a partial payout or nothing at all.

This is precisely why a ₹14 LPA CTC offer with ₹2 LPA variable pay should be read as a ₹12 LPA fixed salary plus a conditional ₹2 LPA opportunity — not as ₹14 LPA guaranteed income. Understanding how this gap plays out month by month is what our detailed guide on real in-hand salary is built around.

Common Forms of Variable Pay in Indian Salary Structures

Variable pay appears in Indian payroll in several different shapes:

- Performance bonus: Linked to your individual appraisal rating — usually paid annually or half-yearly after the review cycle closes.

- Target incentive or sales incentive: Common in sales, BFSI, and FMCG roles — paid monthly or quarterly when target achievement is measurable.

- Quarterly incentive plan (QIP): A fixed variable amount linked to quarterly business outcomes — partly within your control, partly not.

- Profit-sharing bonus: Tied to company-wide profitability — the employer retains significant discretion over the payout amount.

- Retention bonus: Paid if you remain employed through a specified date — not performance-driven but still conditional and often subject to clawback.

Why Employers Build Variable Pay Into CTC

From the employer’s perspective, variable pay does two things. First, it lets them advertise an attractive headline CTC while managing fixed payroll cost — the company pays the full variable only when business performance justifies it. Second, it aligns employee effort with company goals. A salesperson with a high variable component works harder to hit targets; the employer shares the upside only when it exists.

For you as an employee, the potential upside is real. In a good year, strong performance can meaningfully add to your annual earnings. The trade-off is that your monthly take-home becomes less predictable. The larger the variable component in your CTC, the wider the gap between your offer letter number and your regular bank credit.

How Variable Pay Appears on a Salary Slip

In months when variable pay is not disbursed, it does not appear anywhere on your payslip. Your gross salary breakup will show only fixed components — basic, HRA, allowances, and special allowance. Variable pay appears on the payslip only in the month it is actually credited, and that month will typically show a noticeably higher TDS deduction as well. This is an important detail that many employees miss when reading their first variable payout slip. A detailed walkthrough of how all these components appear in a payslip is covered in our guide to salary slip components.

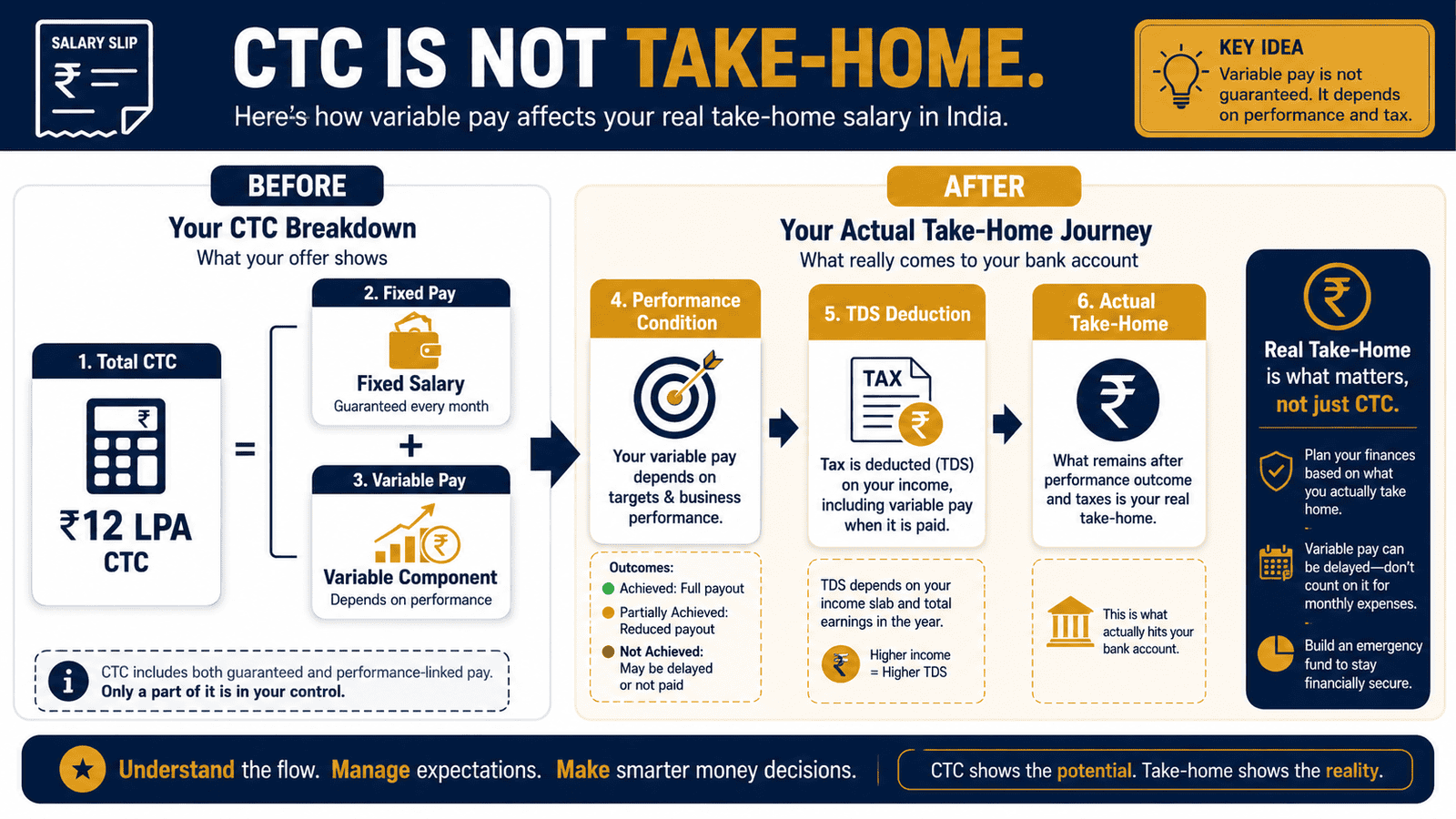

CTC Is an Employer Cost Figure — Not a Bank Credit Promise

This is the foundational concept that most offer-letter readers get wrong. CTC is an accounting figure — it represents the employer’s total annual spend. Fixed pay is the portion most likely to convert into regular monthly salary. Variable pay is conditional, often deferred, and always governed by the employer’s payroll policy. Treat it as an earnings opportunity, not a salary entitlement, and your financial planning will be far more grounded in reality.

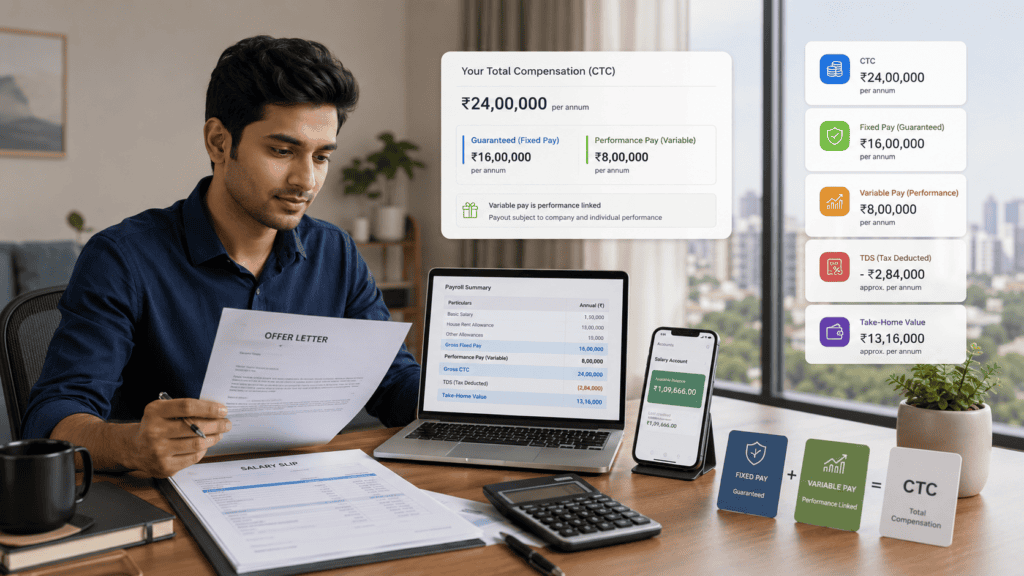

Real Example: Rohit’s ₹14 LPA Offer in Pune

Rohit, 28, is a software analyst in Pune who receives a ₹14 LPA CTC offer from a mid-sized IT services company. His offer letter breaks down the package as ₹12 LPA fixed pay and ₹2 LPA variable pay, paid annually based on his individual performance rating at the end of the appraisal cycle.

Rohit’s monthly fixed gross salary is ₹1,00,000 (₹12,00,000 ÷ 12). After employee EPF contribution on his basic salary of approximately ₹40,000, professional tax applicable in Maharashtra, and estimated monthly TDS based on his projected annual taxable income, his regular monthly bank credit is approximately ₹72,000–₹78,000. That is the number he should use for rent, SIPs, and any EMI planning — not ₹1,16,667.

At the end of the performance year, if Rohit meets his targets and receives the ₹2,00,000 variable payout, his employer adds that amount to his taxable salary income for the year. In that month, TDS is adjusted upward significantly. After applicable income tax and cess, Rohit’s net variable payout may be in the range of ₹1,40,000–₹1,60,000 — not the full ₹2,00,000.

The clearest insight from Rohit’s example: two offers at ₹14 LPA CTC are not the same offer. One with ₹11 LPA fixed and ₹3 LPA variable gives Rohit a much lower and less certain monthly salary than one with ₹13 LPA fixed and ₹1 LPA variable — even though the headline numbers match. For more on this gap, see annual package difference and why your CTC always looks bigger than your in-hand pay.

How to Calculate Variable Pay’s Real Impact on Take-Home Salary

Use these five steps to estimate what variable pay actually means for your monthly and annual take-home before accepting an offer:

Monthly Fixed Take-Home ≈ (Fixed CTC ÷ 12) − Employee EPF − Professional Tax − Monthly TDS

Step 1 — Separate fixed pay from variable pay. If the offer is ₹14 LPA CTC with ₹2 LPA variable, your fixed CTC is ₹12 LPA. This is the number your monthly salary is built on.

Step 2 — Estimate monthly fixed gross salary. ₹12,00,000 ÷ 12 = ₹1,00,000 per month gross before deductions.

Step 3 — Identify standard monthly deductions. Employee EPF contribution is typically 12% of basic salary. If your basic is ₹40,000, that is ₹4,800/month. Professional tax is deducted at rates that vary by state. Your employer also deducts monthly TDS based on your projected annual taxable income, current income tax slabs, and applicable standard deduction — all of which must be verified from current IT Department rules before publishing.

Step 4 — Add variable pay only in the expected payout period. If the ₹2 LPA variable is paid out in March, your March gross salary becomes ₹1,00,000 + ₹2,00,000 = ₹3,00,000. TDS in that month is recalculated to reflect the year’s higher total income.

Step 5 — Estimate post-tax variable income. Variable pay is added to your annual taxable salary and taxed at your applicable marginal income tax slab rate, after standard deduction, plus cess. The exact net amount depends on the current tax regime you are on, the applicable slab, and any other deductions you claim.

| Scenario | Fixed / Variable CTC | Indicative Monthly Take-Home |

|---|---|---|

| Normal month (no variable) | ₹12 LPA fixed / ₹2 LPA variable | ~₹72,000–₹78,000 |

| Variable payout month (annual) | ₹12 LPA fixed + ₹2 LPA paid | Higher credit — but with significantly higher TDS adjustment |

| Alternative offer, same CTC | ₹13 LPA fixed / ₹1 LPA variable | ~₹82,000–₹88,000/month (more predictable) |

All figures above are illustrative estimates. Your actual take-home depends on your salary breakup, state of employment, applicable tax regime, and current IT rules. Use Ridhi’s take-home salary calculator to enter your specific numbers and arrive at a more accurate estimate.

Comparison: Fixed Pay vs Variable Pay

| Parameter | Fixed Pay | Variable Pay |

|---|---|---|

| Monthly credit | Every month | Payout months only |

| Guaranteed? | More predictable — subject to employment terms | Conditional on performance or company results |

| Taxable? | Yes — as salary income | Yes — as salary income when paid |

| TDS timing | Spread evenly across 12 months | Concentrated in payout month — higher TDS that month |

| Affects EPF? | Yes — EPF is on basic salary (part of fixed) | Generally no — unless employer policy includes it |

| Suitable for EMI planning? | Yes — reliable base | No — too unpredictable |

| What to clarify with HR | Monthly gross breakup, standard deductions, TDS estimate | Payout frequency, target criteria, payout history, clawback clauses |

How to Decide What’s Right for You

your fixed CTC is 80% or more of the total offer — your monthly take-home will be relatively stable. Variable pay is then a bonus opportunity rather than a financial risk.

variable pay exceeds 25–30% of your total CTC — your regular monthly income will be meaningfully lower than the headline package suggests. Budget using fixed pay only and treat variable as a possible annual top-up.

you have a home loan EMI, car loan, or other fixed monthly obligation — calculate affordability strictly using your fixed monthly take-home. Do not include expected variable pay in any EMI sizing exercise.

the variable component is individual-performance-based and you have a consistent track record of hitting targets — the upside is real and worth factoring into your annual savings plan, just not your monthly budget.

variable pay is company-performance or profit-linked — you have less direct control over the outcome. Ask HR for the actual variable payout percentage over the last 3 years before accepting the offer.

you have the payout eligibility criteria, target structure, and payout date confirmed in writing — do not treat variable pay as earned income. Request the variable pay policy document from HR before signing your offer letter.

the employer has a reliable track record of paying variable pay in full — a high-variable CTC structure may look attractive on paper but consistently deliver close to fixed pay in practice. Compare every offer on fixed pay first.

Common Mistakes to Avoid

Treating Full CTC as Monthly Take-Home

Many new joiners divide total CTC by 12 and expect that figure to appear in their bank account every month.

This ignores statutory deductions like employee PF, professional tax, TDS, and the fact that variable pay is not a monthly credit. On a ₹14 LPA CTC, your actual monthly bank credit can easily be ₹25,000–₹40,000 lower than simple arithmetic suggests.

Always ask HR for the monthly fixed gross salary and an estimated monthly net take-home before you join.

Assuming Variable Pay Is Tax-Free

Variable pay is sometimes confused with reimbursements or tax-exempt allowances. It is neither.

Once credited to your account, it is treated as salary income and taxed at your applicable income tax slab rate. A ₹2 LPA variable payout does not mean ₹2 LPA in your hand — after applicable income tax and cess, the net amount may be noticeably lower depending on your bracket.

Always plan your finances using the post-tax variable income, not the gross amount stated in the offer letter.

Budgeting EMIs Against Variable Pay

Committing to a home loan or car loan based on total CTC — including variable — is one of the most common and costly payroll misunderstandings.

If your variable pay is reduced or not paid in a cycle, your actual monthly income may fall short of the EMI amount you committed to. Lenders assessing repayment capacity also typically focus on verifiable regular income, not conditional bonus components.

Size every loan EMI to fit your fixed monthly take-home. Full stop.

Ignoring Payout Conditions and Eligibility Rules

Many employees assume variable pay is automatic as long as they complete the year. Most employers have minimum eligibility conditions — a certain number of months in service within the cycle, a minimum performance rating, or active employment on the payout date.

Read your variable pay policy carefully or ask HR before the cycle ends. Employees who resign one month before payout often forfeit the entire year’s variable amount with no recourse.

Forgetting Clawback and Recovery Clauses

Some employers — particularly in BFSI, consulting, and technology — include clawback clauses. If you resign within a set period after receiving variable pay, you may be contractually required to return a portion of the amount received.

Check your offer letter and employment contract for any recovery or repayment condition before treating a variable payout as freely available to spend or invest.

Comparing Offers Using Only Headline CTC

Offer A at ₹14 LPA (₹11 LPA fixed, ₹3 LPA variable) gives you a much lower monthly salary than Offer B at ₹14 LPA (₹13 LPA fixed, ₹1 LPA variable) — despite identical CTCs. Offer B gives you ₹16,667/month more in reliable income every month, regardless of performance.

Always build your offer comparison on fixed pay first. Variable pay is secondary — assess it only after fixed pay is satisfactory for your monthly needs.

When This May Not Be the Right Choice

A salary structure with a large variable component may not suit every financial situation:

- When you have fixed monthly obligations: If you are servicing a home loan EMI, supporting family members, or paying high rent in a metro city, a high-variable structure creates real cash flow risk during months when the variable is not disbursed.

- When the employer’s payout history is unclear or inconsistent: If a company regularly pays 50–70% of the target variable, the headline CTC is effectively overstated. Ask for the actual payout percentage from the last 2–3 cycles before you accept.

- When the payout is fully discretionary: If the employer decides the variable amount without a clear, formula-linked target or performance rating, the amount you receive can vary widely — or be zero — without any meaningful recourse.

- When clawback or recovery clauses apply: If your role has repayment conditions tied to variable pay, joining for the CTC number and leaving within 12–18 months could result in a net financial loss after returning part of the variable payout received.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Variable pay taxation and salary income rules in India are set by established regulatory frameworks. Here is where to verify the figures that matter before you rely on them:

- Income Tax Department (incometax.gov.in): For current income tax slabs applicable to salary income, standard deduction limits, surcharge thresholds, cess rate, and TDS on salary rules. These figures can change with every Union Budget and must be verified before acting.

- EPFO (epfindia.gov.in): For current EPF contribution rules, the statutory wage ceiling for PF calculation, and whether any variable or allowance components in your specific employer’s structure attract PF deductions.

- Your employer’s HR or payroll department: For variable pay target criteria, payout dates, eligibility conditions, proration rules, and any clawback or recovery clauses — these are employer-specific and not governed by a single national standard.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision. For a detailed explanation of how TDS on salary is calculated and when a refund may apply, see our guide on salary TDS calculation.

Expert Tips

- Ask for the fixed CTC and variable CTC in writing, separately. Many offer letters state only a total CTC figure. Request a salary structure document or breakup email that explicitly separates fixed components from variable components before you sign — this protects you from ambiguity on day one.

- Calculate your monthly net fixed salary before accepting. Divide fixed CTC by 12, subtract estimated employee EPF on your basic, subtract your city’s professional tax, and ask HR for a ballpark monthly TDS figure. That net number is your real monthly life budget — not the headline package.

- Ask about the last 3 years’ actual variable payout percentage. Companies often set variable targets at 100% but pay 60–80% in practice due to market conditions or company performance. Knowing the historical payout range is far more useful than the target figure on the offer letter.

- Check whether joining mid-cycle affects your payout eligibility. If your variable cycle runs April to March and you join in October, you may receive only a prorated payout — or none at all for that cycle, depending on the employer’s minimum service policy. Confirm this before you join.

- Do not resign just before a scheduled variable payout date. If your employer pays variable in March and you submit your resignation in February, you will almost certainly forfeit the full year’s amount. Check the payout date and your notice period before you put in your papers.

- Factor in post-tax variable income when comparing offers. If you are in a higher tax bracket, the net amount from a ₹2 LPA variable payout can be meaningfully lower than the gross figure. Compare offers after applying tax — not before.

- Direct variable payout to goals, not monthly expenses. Treat variable income as an annual windfall. Route it toward loan prepayment, your emergency fund, or a planned long-term investment — not your regular monthly spend. This keeps your household budget stable even in years when variable pay is lower than expected.

Frequently Asked Questions

Is variable pay part of CTC?

Yes. Variable pay is included in the Cost to Company (CTC) figure stated in your offer letter. However, it is a conditional component — it may not be paid every month and typically depends on performance or company targets. Your reliable monthly fixed salary is derived from the CTC minus the variable pay component.

Is variable pay taxable in India?

Yes. Variable pay is taxable as salary income under the Income Tax Act. It is added to your other salary income in the year it is received and taxed at your applicable income tax slab rate after eligible deductions. There is no special tax-free treatment for performance bonuses or variable pay components. Current slab rates and standard deduction limits must be verified from incometax.gov.in before publishing.

Is TDS deducted on variable pay?

Yes. Your employer is required to deduct TDS on all salary income, which includes variable pay. When variable pay is credited, the employer recalculates your projected annual taxable income for the year and adjusts TDS accordingly. The TDS deduction in the payout month is typically much higher than in normal months. This is not an error — it is a payroll TDS projection adjustment.

Is variable pay paid monthly or yearly?

It depends entirely on the employer’s policy. Some companies disburse a small variable component monthly as part of the regular payslip. More commonly, variable pay is structured as a quarterly, half-yearly, or annual payout tied to a performance review or business cycle. You should ask HR for the specific payout frequency and cycle dates before you compare offers or plan your finances.

What is better: fixed pay or variable pay?

This depends on your financial position and career situation. Fixed pay gives predictable monthly income — essential if you have EMIs, rent, or family obligations. Variable pay can significantly add to your annual earnings if you consistently hit targets — attractive for high performers in output-measurable roles. Most offers include a combination; the real question is what proportion of variable pay you can afford to treat as uncertain income without stress.

Does variable pay affect PF?

Generally no. Employee Provident Fund contributions are calculated on basic salary, which is a fixed component. Variable pay is not typically included in the EPF wage base unless the employer’s specific PF trust rules or policy includes it. If your offer has a large special allowance or variable component, verify with your employer’s HR or payroll team whether it attracts any PF contribution.

Can variable pay be zero?

Yes, it can. If an employee does not meet the minimum performance rating or threshold defined in the variable pay policy, the payout can be zero for that cycle. Similarly, in profit-linked plans, a company that does not meet its business targets may reduce or eliminate the variable payout for all employees. This is precisely why variable pay should never be treated as guaranteed income in your budgeting.

What happens if I resign before my variable pay is paid?

In most cases, employees who are not on the payroll on the scheduled payout date forfeit that cycle’s variable pay. Some employers prorate the amount if you have completed a minimum number of months in the cycle; others require active employment on the payout date with no exceptions. Read your offer letter, employment contract, and HR policy carefully — and check the variable payout date before submitting your resignation.

Should I include variable pay in my monthly budget?

No. Base your monthly expenses, EMI commitments, and recurring financial obligations on your fixed monthly take-home only. Variable pay is uncertain in both timing and amount. When it is actually received, direct it toward defined annual goals — loan prepayment, emergency fund top-up, or long-term investments — rather than treating it as regular monthly spending money.

Is variable pay the same as a joining bonus?

No. Variable pay is a recurring component linked to performance within each appraisal or incentive cycle. A joining bonus is a one-time payment made when you join, often with a recovery clause if you leave within a specified period. Both are taxable as salary income, but they differ in purpose, frequency, and the conditions that govern them. Conflating the two can lead to significant misreading of an offer’s real value.

Final Verdict

Variable pay in CTC is real earning potential — but it is not a salary guarantee. The headline CTC number in an offer letter can be genuinely misleading if a large portion of it is conditional, deferred, and taxable only on payout. For anyone evaluating a new offer, the right approach is to calculate your fixed monthly take-home first, then assess the variable upside separately — based on payout history, target structure, and tax impact.

High performers in target-driven roles can benefit significantly from variable pay structures over the long term. But for anyone with EMI obligations, family dependents, or limited financial cushion, a higher fixed salary at the same CTC is more valuable than a high-variable offer with an attractive headline. Use fixed pay to build stability. Use variable pay to accelerate goals. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.